Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Healthcare

While Q4 revenue modestly beat consensus, growth slowed to the lowest level in five years and 2026 guidance points to further deceleration, limited operating leverage and weak FCF. Bulls were clearly disappointed as the stock traded down >20% on the day. In OWS's last update, they wrote that ATEC would struggle to deliver on profitability and cash flow targets without negatively impacting revenue growth, which they expected would decelerate substantially going forward. Moreover, they noted that ATEC’s FCF benefitted from unsustainably low investment in inventory and capex, setting bulls up for disappointment in the coming quarters. Their thesis appears to be playing out. A recent share bounce on takeout speculation following Boston Scientific’s acquisition of Penumbra is seen as misplaced, with large players exiting the spine market in recent years and ATEC is not cheap at ~3.5x EV/S. TP $10.50 (40% downside).

Edition: 228

- 23 January, 2026

Healthcare

While PEN’s 3Q25 beat was driven by a surprise surge in Embolization & Access sales (+22% Y/Y), growth in the key US Thrombectomy business continued to decelerate (+19% Y/Y vs. +23% in Q2, +25% in Q1 and +27% in 4Q24). Despite management suggesting the slowdown was primarily attributable to weakness in the stroke thrombectomy market, US VTE growth also decelerated substantially (+32% Y/Y from +42% in Q2), likely because Stryker/Inari is getting back on its feet and new competitors are entering the market. With FY25 guidance implying PEN’s overall revenue growth will decelerate meaningfully from +18% Y/Y in Q3 to just +14% Y/Y in Q4, OWS sees the post-earnings rally as an attractive shorting opportunity.

Edition: 224

- 14 November, 2025

Healthcare alpha generation

Healthcare

Channel Dynamics has built a strong record of HC alpha generation by leveraging deep channel checks with private company experts and providers. Over the past 12+ months, their calls have consistently delivered meaningful relative alpha from report release through earnings, ahead of major stock moves including: UnitedHealth (flagged negative MLR inflection and UNH exposure before disappointing earnings and stock collapse); DexCom (called negative inflection in DME performance before turning back positive on DME relationship improvements and G7 market share gains); Align (correctly predicted Q/Q shifts in clear aligner and capital equipment purchasing trends); Penumbra (called positive DVT market growth trends and PEN market share gains in DVT, PE and Neuro Segments); and Dentsply Sirona (flagged worsening product/vendor performance and further deterioration from tariff impacts).

Edition: 220

- 19 September, 2025

Consistently generating alpha on the short side

2024 was the largest alpha year in OWS's history - an equal-weighted basket of their short ideas outperformed the inverse of the S&P 500 index by 21.3 percentage points, with Atkore, Nucor and Upwork outperforming the most. They showed an impressive consistency, beating the index in each quarter. In Q4, OWS initiated 4 new short recommendations including Penumbra and Signet Jewelers. At the end of year, they had 17 short recommendations outstanding. For 2025, they see opportunities in cyclical setups, AI and in speculative small caps.

Edition: 202

- 10 January, 2025

Short Shots

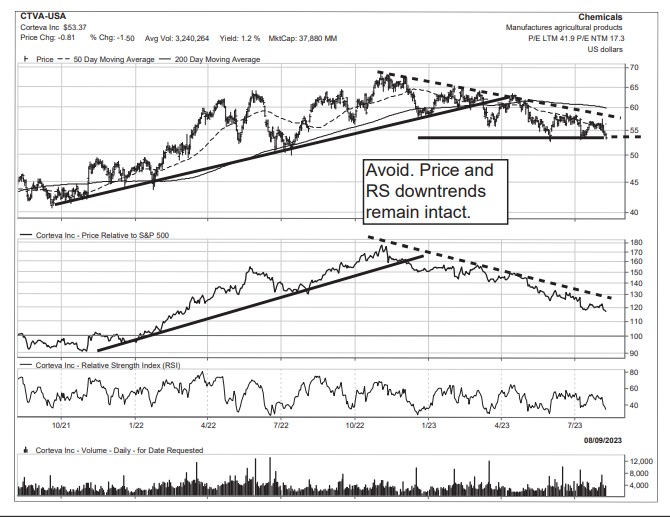

Is a collection of technically vulnerable charts culled from the “Negatively Inflecting” and “Toppy” columns within Vermilion’s Weekly Compass report or from various technical screening processes. The charts contained in this report have developed concerning technical patterns that suggest further price deterioration is likely. For these reasons Short Shots can also be a great source of ideas for investors interested in short-selling candidates.

Charts highlighted include Corteva (see above), Enphase Energy, General Mills, Kraft Heinz, Hershey, MarketAxess, Moderna, Newmont, Penumbra, Roblox, SolarEdge and Valmont Industries.

Edition: 167

- 18 August, 2023