Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

A broken IPO trading ~60% below its $25 listing price, with potential to double over the next year and deliver a 3x return over 4 years. Recent share price weakness is due to a market that has indiscriminately punished the entire software sector, as well as the company's usage yield compressing, which bearish analysts have misinterpreted as an erosion in pricing power. NAVN is the technological leader in a $185bn corporate travel and expense market, disrupting legacy incumbents with a unified platform and a differentiated model. The stock trades at ~2.9x EV/FY26 sales based on guided revenue of ~$685m - a clear dislocation for a platform growing ~29% with 74% gross margins and 13% operating margins. A path to 30%+ margins exists at scale. The setup is likened to Booking.com in 2009 when it was trading under $100/share.

Edition: 232

- 20 March, 2026

OpenClaw drives AI shift, but disruption risk overstated

Communications

86Research argues the rise of OpenClaw and AI agents is reshaping China’s internet ecosystem but believes market concerns are overstated. While agent frameworks could emerge as new traffic gateways and LLM platforms have already captured 8-10ppt of global traffic share, the firm sees disruption as more incremental than structural in core consumer use cases. China’s low software penetration supports rapid AI adoption but also limits near-term cannibalisation. Despite execution premiums being assigned to startups and ByteDance, 86Research believes incumbents such as Tencent and Alibaba retain strong underlying advantages and sufficient time to adapt. Recent share price weakness is therefore seen as a buying opportunity. However, they turn more cautious on Kuaishou, removing it from their Top Buy list amid intensifying competitive pressures.

Edition: 232

- 20 March, 2026

Salik (SALIK UH) United Arab Emirates

Industrials

Dubai’s growth story is only temporarily disrupted by the US-Iran war, according to Robert Crimes, who updates his long-term model for Salik. Revenue is cut by -13% in 2026E and -11% in 2031E, while traffic declines -6.5% and -6%, respectively. Estimates for 2027-30E follow a similar trend, reflecting regional pressures and a revised assumption of one new toll gate in 2028E (five over 2027-41E unchanged). EBITDA is reduced by -14% in 2026E and -8% in 2031E. Despite this, Salik rises to 3/23 on Insight’s Stock Ranking System; with shares ~20% lower YTD, the stock offers ~145% upside to Robert's TP of AED12.9. The long-term case remains intact, supported by exclusive tolling rights to 2071 and a high FCF, asset-light model

Edition: 232

- 20 March, 2026

Nickel may yet surprise

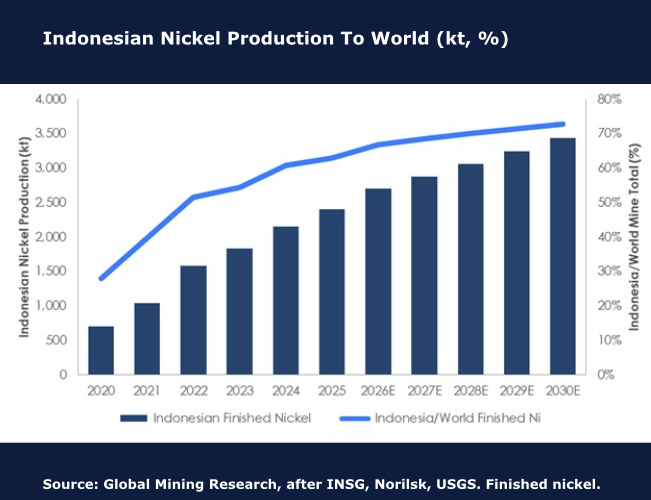

Recent events brought spot nickel up to ~US7.80/lbafterabriefreturnto US8.00/lb. The three major developments that led to this are the Iran war, a decision by the Indonesian government to dramatically cut thermal coal mining permits from 790Mt to 600Mt, and another decision to cut laterite nickel mining permits to 260-270Mt versus 2025 at 379Mt. GMR has calculated an annual nickel demand growth rate at 6.2% CAGR over the last decade, but the unceasing volumes from Indonesia (see chart) have been the issue. New changes may see parts of the global nickel cash cost curve move by ~US$1.50/lb. If laterite ore is really cut back heavily, then the price impact should add to that, but very large inventories could limit substantive price moves for some time. This is all potential; good news for producers like Vale SA, Glencore PLC or MMG Ltd. It’s too late for the Cuban producers where the lack of fuel is triggering closures.

Edition: 232

- 20 March, 2026

Silver futures (SIK26) forecasts

With the attainment of the new low under 78.06, the Technical Analysis Group have closed half of their NT Strategic Short position, established into strength at 95/96, and are placing a trailing stop at 87.70 on the remainder of the trade. Price action from 97.30 has yet to reveal any urgency or impulsiveness to the downside. The team are expecting near term relative outperformance in gold vs silver, and are bullish the 'RATIO' whilst above 57.59, seeking upside in the near term to 67 +/-, and 72.66+. Since raising risk, they have seen a +12% rise to 64.47. The team continues to remain long term bullish and regardless of whether or not they’re in the higher degree 4th wave, they do not expect downside under their proposed 60 +/- 10 LT Long Term Range Base, before ultimately eclipsing this year’s 121.78+ high in the resumption of the underlying bull trend, exposing their next major upside attraction levels of 138 and 165 (see chart).

Edition: 232

- 20 March, 2026

Energy shocks are disinflationary

Barry Knapp examines how the current energy price spike functions as an adverse aggregate demand shock rather than a traditional inflationary driver. The US economy was already showing signs of weakening, causing rising energy costs to act as a “tax” on consumers, suppressing economic activity and threatening to push a fragile economy into a deeper slowdown. The USD is rising alongside energy prices, causing the cost of energy to increase even further. The popular idea that energy shocks automatically bring about long-term inflation can be refuted by looking at history through a different lens: the high inflation of the 1970s was a result of fiscal policy, and the 2022 surge in foods prices actually saw goods prices peak at the moment of the inflation but the disinflationary shock was masked as fiscal spending was still flooding the market. He is waiting for a 10% drop in the S&P500 before considering entry into cyclical sectors.

Edition: 232

- 20 March, 2026

Oil: The price of war

James Burdass senses that the timeframe for any resolution is being significantly pushed back. The White House claims to have "totally obliterated" military installations on Kharg Island while, for now, sparing the oil infrastructure. James believes that there is the increasing inevitability of deploying Marines to Kharg Island, not for a full-scale invasion of the mainland, but as a "Physical Lock" on Iran's economic jugular. The US may be concerned that it has run out of immediate options to end this conflict without significant loss of life and is attempting to pressure its reluctant allies into the fray. We are currently witnessing scenarios James modelled in previous features (mines in the channel, Kharg Island targeted) but considered extreme tail risks. Yet, oil prices remain remarkably anchored around the $100 mark, whereas he would have modelled a spike to $120+ lasting for the duration of the closure, not just for a day.

Edition: 232

- 20 March, 2026

China’s modest uptick

China’s Jan-Feb macroeconomic data pointed to a modest improvement in economic activity, with industrial production, retail sales, and fixed-asset investment all exceeding market expectations, although persistent weakness in the property sector and a slight rise in unemployment highlight ongoing structural challenges. Manufacturing growth was broad-based, led by strong gains in computers and communications equipment (14.2%), railway and shipbuilding (13.7%), and general equipment manufacturing (8.9%), suggesting continued resilience in China’s industrial sector despite external headwinds. Retail sales rose 2.8% year-over-year, accelerating from 0.9% in December. Overall, John Fagan notes the latest data suggests that China’s economy is showing signs of stabilisation early in 2026, supported by industrial momentum, infrastructure spending, and a holiday-driven pickup in consumption. However, he says the persistent downturn in the property market and rising unemployment indicate that underlying growth remains uneven, leaving policymakers likely to maintain targeted policy support to sustain economic momentum in the months ahead.

Edition: 232

- 20 March, 2026

Output growth and the real price of crude oil

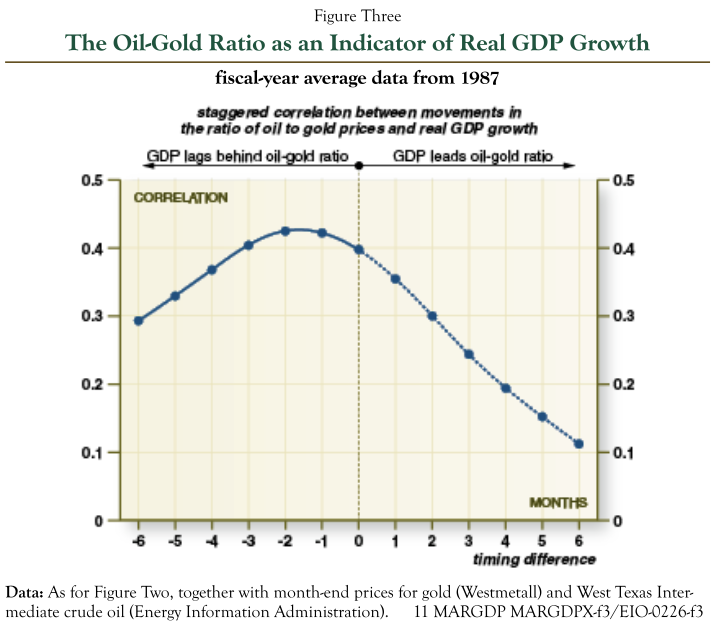

HCWE’s latest report explores the empirical links that connect economic growth with movements in some prominent market-driven prices. They examine the explanatory power of credit spreads, but the data shows that there is a chain of causation that runs mainly from the economy to credit risk; it’s difficult seeing credit spreads having much power to anticipate economic growth. Another source is crude oil prices, which receives much less attention than it deserves when it comes to its explanatory and predictive value. They claim that oil prices lead GDP by an average of two months, with an annual correlation of +0.47. However, many economists convert GDP from current to constant dollars but fail to do this with crude prices, so the team express the real oil price as a ratio between its nominal price and the price of gold. This provides a higher correlation of +0.59 (see chart). There is a strong case for using real oil prices to anticipate the economy.

Edition: 232

- 20 March, 2026

Nigeria: Oil prices present another story

Jonathan Anderson remarks that, again, Nigeria has exceeded expectations on macro adjustment in a low oil price world. Over the past two years the authorities unified and stabilised the NGN rate, hiked rates to positive real levels, tightened fiscal policy, reduced money and credit growth, squeezed import demand, put the external balance in surplus and brought inflation down at home. Even so, Jonathan wasn’t enthused about asset markets with oil at $65/barrel. Sovereign bond and local equity prices already ran aggressively last year, and coming into 2026 he felt both markets were overdone at then-prevailing oil prices. Even the naira trade was likely "running out of steam" with potential fiscal pressures rebuilding. With oil over US$100/barrel, however, it's another story. If global crude prices stay in the triple digits, this makes every market look cheaper - and Jonathan would be particularly interested in FX carry and dollar debt once again.

Edition: 232

- 20 March, 2026

Iran: Hormuz Hold ‘Em

Given continued Iranian escalation, Niall Ferguson likens the US’s choice as one familiar to any poker player: call, re-raise, or fold. Both sides have reason to assess the conflict has validated their theory of victory. Washington has heavily degraded Iranian missile and drone capacity; Tehran has kept the Strait of Hormuz functionally closed. But the current tempo of the war is indecisive. For both sides, to avoid folding—accepting a ceasefire on unsatisfactory terms—escalation becomes necessary. For Tehran, this means mining the Strait given the diminishing effectiveness of its drones and missiles. For Washington, it means a ground campaign in southern Iran to restore freedom of passage before global economic and political disaster. In casino terms, Niall sees little prospect of a diplomatic fold and thus upholds his view that the re-opening of the Strait becomes more likely than not only by mid-April.

Edition: 232

- 20 March, 2026

The upcoming LatAm bank rally

LatAm bank stocks have outperformed EM and DM peers in common currency terms over the past 12 months (see chart). The rally has been driven by both domestic and external factors, and these tailwinds are expected to persist over the medium- to long-term. Falling bond yields due to interest rate cuts and fiscal orthodoxy, reviving domestic demand, robust bank profitability, potential for credit expansion, supportive political backdrops and attractive valuations (despite the recent rally) all point to bank stocks (ex Brazil) being on the eve of a multi-year outperformance relative to global bank stocks. The team recommend going long LatAm ex-Brazil banks / short global bank stocks. Mexican bank equities remain the team’s favourite, followed by Chilean and Peruvian options. The team are also bearish on Brazilian bank stocks due to a poor and worsening domestic macro backdrop and an uninspiring political outlook.

Edition: 232

- 20 March, 2026

Japan’s monetary stability as oil prices rise

Andrew Hunt points out how Japan’s economy is over-monetised, with households therefore diversifying away from cash and fixed income into equities and some foreign assets. He firmly believes this diversification effort has supported equity prices until recent days. Higher oil prices and politics could now accelerate the move out of cash; the BoJ will want to resist this via higher rates and continued QT. Monetary stability would seem to demand this course of action. Higher rates would be (implicitly) designed to dent the flow into equities but would stabilise the JPY & inflation longer term. If higher rates are not enacted and QE returns, could saver confidence in the JPY be lost? This would be problematic for equities over the long term, and for inflation and the JPY, but positive for property prices and perhaps even PCE trends in the near-term. Andrew fears that fiscal primacy will rule the day over the coming months…. Good news for equities near term but not on a three-year view.

Edition: 232

- 20 March, 2026

US: The case for 10% unemployment

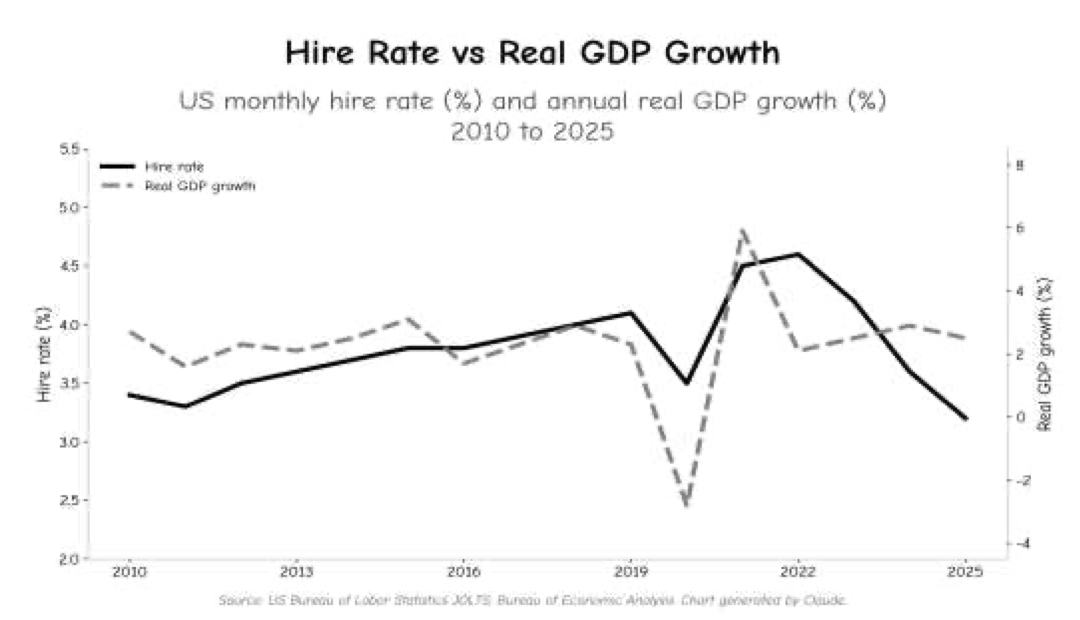

Paul Krake’s latest report rebukes the argument that AI-driven job displacement will be absorbed by new industries generating new work. It is an argument that Paul claims is taken seriously in policy circles, investment committees, and corporate boardrooms, yet it is deeply flawed. The hiring data already shows this, with the hire rate having falling 29% since the post-pandemic peak yet GDP has grown by 8% (see chart). AI is amplifying the pattern that labour is not required for growth. Just a 1 in 10 displacement of knowledge workers, which represent 45% of the US labour force, is enough to push unemployment towards 9% without a recession. Paul claims that the frameworks used to detect labour market stress are not built for an economy where growth and hiring decouple permanently. By the time the unemployment rate confirms what the hire rate has been signalling since 2022, the adjustment will have been compounding for a decade. 10% unemployment in the years ahead is not a tail risk, it is the base case.

Edition: 232

- 20 March, 2026

Black Swans vs Blue Owls

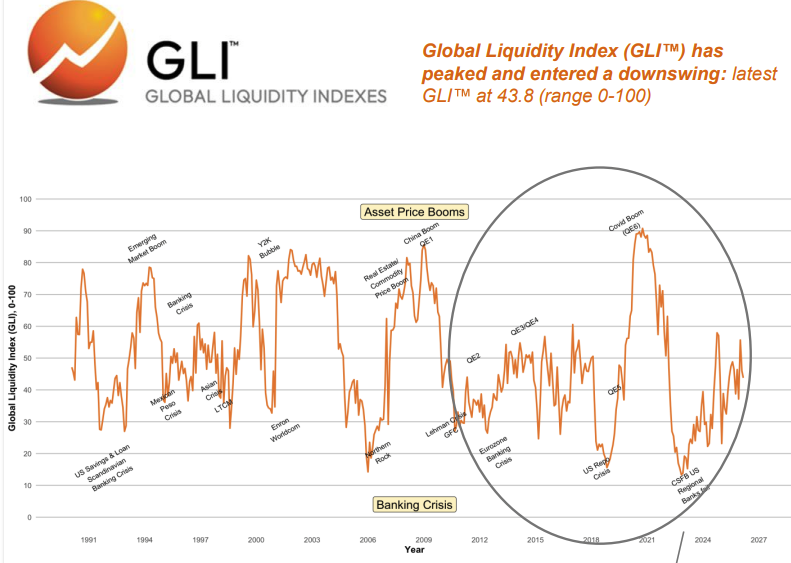

Michael Howell’s Global Liquidity Index (GLI) has peaked and entered a downswing, pushing market conditions towards a ‘Risk Off’ environment. This systemic downturn, rather than the oil spike alone, is the primary force eroding portfolio performance and explains growing stresses in private credit, as exemplified by troubles at firms like Blue Owl. While the Iran conflict-driven oil price spike acts as a negative Black Swan shock, its impact is compounded by the already weakening liquidity cycle. The Fed is managing liquidity to avoid market crashes, while the PBoC is aggressively injecting liquidity. This divergence justifies holding gold and explains why Chinese markets are at an earlier, more favourable stage of the investment cycle. With the liquidity downturn expected to last 12-15 months, the recommended strategy is to pare back credit and US tech exposure. Investors should rotate towards defensive assets like commodities (gold, oil), gradually add to mid-duration Treasuries, and increase holdings in Chinese stocks.

Edition: 232

- 20 March, 2026

Space: A slow burn for investors

Industrials

Japan’s space sector remains in transition: technically ambitious, strategically important and increasingly commercial, but still fundamentally dependent on launch reliability and policy execution, with recent progress overshadowed by several high-profile setbacks. Looking ahead, Neil Newman highlights 3 developments which would signal meaningful acceleration in the sector and potentially justify thematic investment consideration: 1) improving the reliability and cadence of H3 launches; 2) continued deployment and monetisation of Earth-observation and SAR constellations; and 3) stronger government procurement as space capabilities become embedded in national infrastructure and security policy. Companies flagged in Neil’s report include Mitsubishi Heavy Industries, Mitsubishi Electric, NEC, IHI, iSpace, Astroscale, Synspective and Axelspace.

Edition: 232

- 20 March, 2026

A World War III involving China is increasingly inevitable

David Murrin believes that the US could secure the Strait of Hormuz in three to four months should it utilise the full range of sensors and combat assets outlined in David’s latest report. However, he anticipates that the US will struggle to deploy and sustain such a high operational tempo, potentially extending the conflict well beyond that timeframe. In addition, there is a high probability that the depletion of American mid-course interceptors, the concentration of US naval and missile defence assets in the Gulf at the cost of Pacific and Atlantic deployments, and the disruption of oil flows as production facilities are damaged during missile/bomb exchanges will generate significant strategic compression. This will, in high probability, provide China with an opportunity to launch a major military campaign across the Pacific without warning to seize control out to the third island chain, potentially in parallel with a Russian escalation against NATO. In his latest report, David explores the possibility of the Iran situation sparking a global war.

Edition: 232

- 20 March, 2026

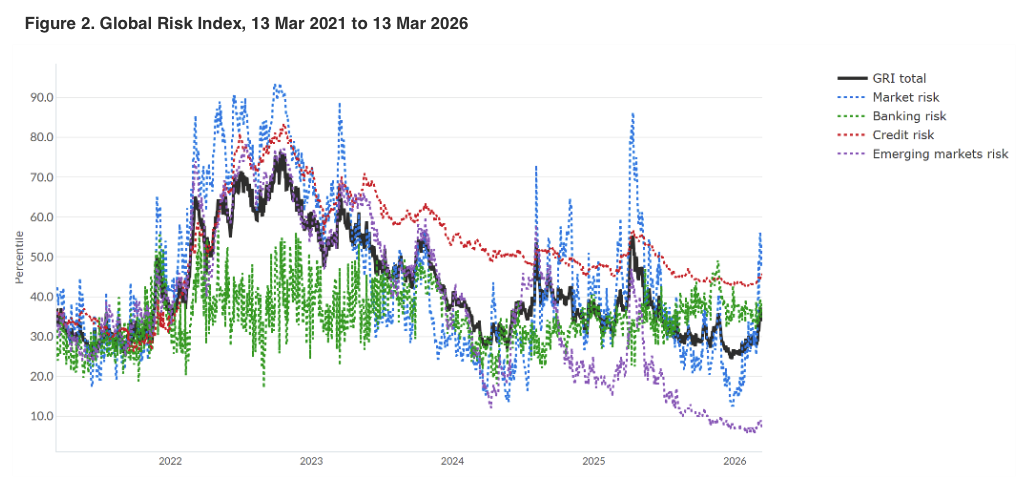

Risk rising, but so far contained

Jeffrey Young’s Global Risk Index (GRI) signals an increasingly risky macro environment, brought on by the prospect of extended disruption to Middle East energy supplies and the Strait of Hormuz. Importantly, however, a dispassionate assessment using various DeepMacro metrics suggests that actual shifts in the global macro backdrop to date are muted. The GRI has risen from what was a very low level in late February to a reading that is in the mid-30s, a level that is relatively muted by historical standards (see chart). Indeed, the rising figure is nearly entirely due to rising financial market volatility, not to credit risk or financial sector risk – increases in the latter would signal a potentially significant deterioration in the environment ahead. Whilst market expectations have worsened towards future economic growth and inflation, Jeffrey’s factors are yet to show any deviation from recent trends.

Edition: 232

- 20 March, 2026

Financials

Galliano's Financials Research

Victor Galliano upgrades the stock to Buy, arguing that the recent partial disposal of its stake in Nintendo could mark the start of a broader unwind of the bank’s large strategic equity portfolio - its primary source of potential shareholder value creation. The sale generated a ¥75.1bn gain (c.¥90bn proceeds) and reduced Kyoto’s stake from 4.2% to 3.3%, though the remaining holding still represents more than 30% of the bank’s market value. With ¥160bn in gains on stock sales, Kyoto has also been able to crystallise roughly ¥90bn of losses on government bonds, bringing its unrealised losses on the domestic government bonds still on its balance sheet close to zero. Kyoto trades at the lowest PBV among Japan’s top ten banks, while its 4.1% dividend yield also has scope to rise.

Edition: 232

- 20 March, 2026

The Euro’s extremely important juncture

The Euro’s (€1.1416) monthly chart shows a breakout from a 17-year Down-channel, with the currency trading as high as €1.2083 in January this year, up 27% from the Sep 2022 low. Chris Roberts comments how a sustained breakout from the channel, following the 14-year, 40%+ fall in 2008-22, could potentially be very bullish. The near 6% fall from the recent high has taken the Euro back to the rising 20-month WMA and the 9-month RSI back to Neutral 50. Chris is 40% long from €1.1572 and would look to add on a break above the Jan high. His stop stays at a daily close below €1.0954.

Edition: 232

- 20 March, 2026

Technology

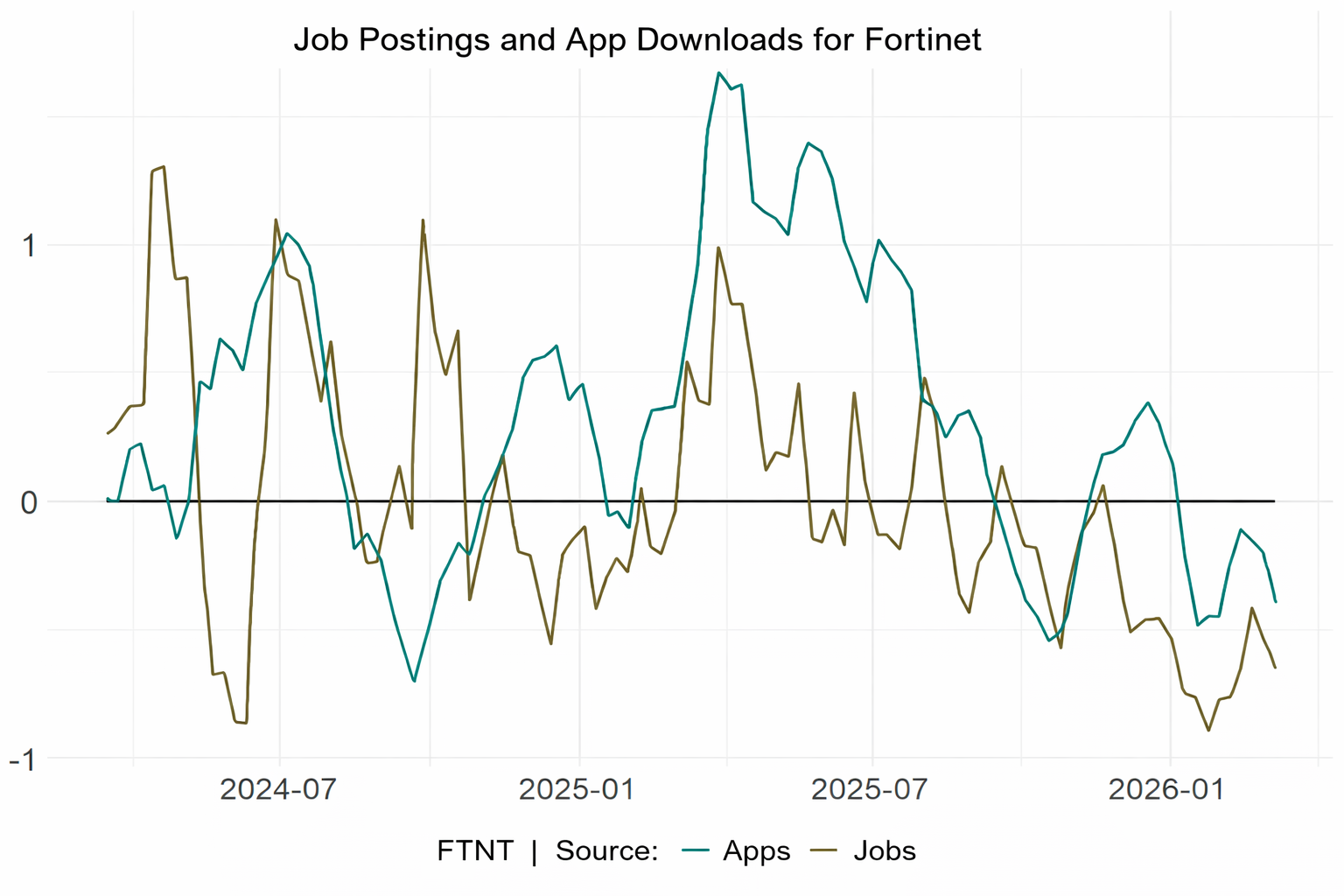

Structurally exposed to the shift from hardware firewalls to cloud-based security platforms and from network-based to an identity-based model, FTNT is losing ground to Zscaler and Cloudflare. Alternative data signals reinforce this view with FTNT ranking in the lowest quartile of AnteData’s measurement of coding activity trends, while freelancer job demand tied to its technologies is declining and downloads of its authentication app are falling. Although the company still holds ~18% of the global firewall market, revenue growth has slowed from ~20% in 2023 to ~12% currently, with AnteData expecting normalisation towards ~5%. With a net income margin already at 27%, they see limited scope for further expansion, making the ~34x earnings valuation appear demanding.

Edition: 232

- 20 March, 2026

Aviation credit markets underpricing geopolitical risk

Industrials

Reno Bianchi’s Aviation Weekly highlights a growing divergence across aviation markets amid rising geopolitical tensions. Airlines have experienced a sharp equity rout, while oil prices have risen by over 40%, with jet fuel surging even more dramatically - up ~70% domestically, ~80% in Europe and more than doubling in Asia. Despite this, from a fixed-income trading perspective, the aggregate market reaction has remained muted. Reno believes this response is overly restrained. It appears fixed-income investors are anticipating a much quicker resolution to the conflict than the equity markets, which may ultimately prove to be a miscalculation. Included in his report is a “post-war monitor” he uses to track key market, oil and jet fuel statistics, as well as trading recommendations, where he continues to recommend maximum caution.

Edition: 232

- 20 March, 2026

ITV (ITV LN) UK

Communications

While ITV describes itself as strongly cash generative, FY25 results tell a different story. Cash inflow from operating activities fell sharply from £333m to £202m. Forensic Alpha also identified several other red flags, pushing ITV’s Risk Score from '8' to '10' (max. rating). Working capital has been a persistent drag, with the headwind widening from £144m in 2024 to £196m in 2025. Trade receivables rose 12% to £500m despite flat sales, driven largely by long-term balances now representing 18% of the total. Contract assets increased 33%, including a jump in non-current contract assets from £4m to £39m. Meanwhile, exceptional charges related to restructuring and M&A rose from £65m to £107m, further weighing on cash flow. For now, the market is focused on the potential sale of the M&E business. If it falls through, attention will shift back to the company’s underlying fundamentals.

Edition: 232

- 20 March, 2026

Guidance warning season

Despite rising geopolitical risk, European corporate guidance has yet to reflect the potential economic impact. In AIR’s recent management meetings, discussion focused almost entirely on AI, with little attention paid to the Iran conflict despite surging energy prices and supply-chain stress that historically drive earnings revisions. The combination of unpriced macro risk and AI-driven sectoral disruption creates a credible basis for expecting a meaningful wave of 2026 earnings guidance revisions across European equities in the coming weeks. And the performance gap between the companies on the right side of these structural shifts and those on the wrong side will broaden. Stock winners include AI infrastructure beneficiaries such as Arm, Elmos, Aixtron and STM, alongside defence exposure at Exosens and Indra Sistemas. Euronext and Auto1 are also seen as largely insulated. Under pressure are Stroeer, Freenet and SES. In IT services, the sector is splitting between “The Conquerors” (Accenture, Cognizant, Reply) and “The Endangered” (Capgemini, Atos, Sage, Dassault Systemes, SAP).

Edition: 232

- 20 March, 2026

Bear’s Den Idea Forum

Short-focused events consistently rank among MYST’s best-performing Idea Forums with their last one yielding a ~70% hit rate and ~8.7% average positive alpha. The dominant theme at this meeting centred on companies confronting new competition driving share loss and margin compression, while other high-level topics included businesses facing AI-related challenges; “fading” cyclical recoveries; and GLP-1-driven demand destruction. MYST felt Calix (BEAD subsidy unwind favours lower-cost solutions + forensic red flags) and TransMedics (organ transplant tech leader facing share loss amid new competition) were “unique” and worth investigating, while convincing bearish arguments were also presented on A O Smith, Dollar General, Old Dominion Freight Line and Uber.

Edition: 232

- 20 March, 2026

Japan: The balance of payments and the yen’s outlook

Andrew Hunt says that is difficult to gain a clear picture of Japan’s true Balance of Payments trends; some of the relevant data seems contradictory. Rising JGB yields have slowed capital outflows from Japan (predictable) but not reversed them. Elsewhere, foreign investors have been moving back into JGBs (intriguing) and Japanese equities (interesting). The foreign interest in Japanese equities and the importance of these flows within the BoP data arguably makes the JPY more of a “risk on” currency than safe haven. In the near term, Andrew expects the JPY to remain “choppy” with a bias towards being positively correlated with risk appetite, but any sharp falls would likely be resisted in the near term by foreign central banks. Longer term, Andrew says that the fate of the JPY is inexorably linked with that of the BoJ’s credibility, something that he expects to be undermined over time by fiscal primacy.

Edition: 231

- 06 March, 2026

US manufacturing PMI does not set a new trend

Carl Weinberg points out that the US manufacturing PMI for February printed above its break-even level for a second month in a row, signalling an expansion in the sector. This is a surprise, and a positive one at that. However, Carl notes that the uncomfortable truth is that the correlation between headline ISM manufacturing and current-quarter GDP growth over the last decade is below 0.30. The economy has demonstrated it can grow without industrial growth, which has declined as a share of overall economic activity. The manufacturing sector is sick, barely growing at all. It has been contracting for a long time, and a print or two above 50 does not set a new trend. In short, manufacturing does not appear to be responding well to Trump’s economic policies. Tariffs do not seem to be increasing the business of existing firms, as this survey suggests, or creating new jobs in new firms as the payroll employment data suggest.

Edition: 231

- 06 March, 2026

Making sense of the Citrini AI debate

Cam Hui reviews the controversial report recently published by Citrini Research that rhetorically asked, “What if our AI bullishness continues to be right...and what if that’s actually bearish?” The Citrini report postulates a scenario where AI wipes out millions of jobs, while AI boosters assume widespread productivity gains without disruption. Cam notes that the history of the adoption of disruptive technology indicates that outcomes are never utopian nor apocalyptic. He therefore prefers to adopt a middle ground. Artificial intelligence is a very real technology and its adoption will dramatically change society. There will be some degree of disruption in capital markets and return expectations. Cam points out that the AI bubble never reached the excessive levels of the dot-com bubble, and the degree of price adjustment will be lower. In all likelihood, its collapse will not cause a recession.

Edition: 231

- 06 March, 2026

Approaching peak AI hysteria

People are gregarious and instinctively follow the impulses of the herd, remarks James Aitken. The past two weeks have been a reminder of the mob mentality, and with dystopian projections on AI hysteria reaching millions of views, James believes we are approaching peak AI hysteria. Just remember when scouring the news: why am I reading this now and who benefits? XAI, Anthropic and OpenAI are all in windows to raise absurd amounts of money at lofty valuations, so it’s no surprise everyone is getting almost daily updates on LLMs about their improvements. DRAM, NAND and H100 rental prices suggest the AI juggernaut and associated memory shortage continues, yet so violent has been the recent shakedown that companies that would seem to have little risk of being disrupted by AI have been smashed, too. Just look at the current P/E of Microsoft (green) vs the current P/E of Colgate (red).

Edition: 231

- 06 March, 2026

The West’s plague of idiots

From David Murrin’s five stages of Empire perspective, the West is suffering from a “Plague of Idiots”. David says it is increasingly evident that the leadership and Western society are experiencing a profound crisis of competence, judgment, and cortisol with which to drive our sense of collective danger and motivation to see and react to the oncoming threats. This crisis extends well beyond individual policy failures; it reflects a civilisation in the late stages of institutional decay and declining effectiveness. The Western order now appears weakened by a loss of strategic understanding and professional competence, and is increasingly marked by complacency, self-absorption, and managerial mediocrity. In an era defined by great-power competition, missile warfare, and systemic instability, such leadership deficits materially increase strategic risk. If left unaddressed, the imbalance may prove the most serious long-term threat of all, and the “Plague of Idiots” will inevitably sabotage the existence of our Western democratic civilisation.

Edition: 231

- 06 March, 2026

China: Channel checks on leading coffee & tea brands

Consumer Discretionary

The competitive environment across the country's leading beverage chains appears to be shifting from aggressive subsidy-led share grabs towards more rational pricing and product-led differentiation. For global investors, this suggests: 1) margin recovery potential after a prolonged discount cycle; 2) strengthened positioning for category leaders with innovation capabilities; and 3) continued consolidation towards scaled operators with diversified product offerings. Luckin’s near-term fundamentals look resilient with Jan SSSG likely >10% and pricing/ASP recovering sequentially. Mixue was modestly softer due to the CNY timing shift, while Guming was a clear relative winner among tea chains with SSSG/GMV +10-15% (still HSD even ex delivery fees) and momentum likely improved further in Feb on holiday & platform campaign effects.

Edition: 231

- 06 March, 2026

Brazil: Stagnation ahead

In the fourth quarter of 2025 Brazil’s GDP rose 0.1% QoQ s.a., broadly in line with the market median (0.1%) and BuySideBrazil’s projection (0.0%). Compared to 4Q/2024, GDP increased 1.8%. In Q4/2025 Brazil’s economic growth relative to 3Q/2025 was mainly driven by stronger exports and services. Services, slightly above expectations, posted a positive performance in the quarter, supported by higher consumer income amid a still-robust labour market. However, Andrea Damico says this momentum already shows signs of exhaustion, with a potential turning point in H1/2026. The key highlight is the sharp slowdown in domestic demand, with the weakest marginal performance in domestic absorption and private consumption since the end of the pandemic in 2021. The clearest sign of this fragility was the sharp decline in imports. Overall, this data reinforces Andrea’s view of cooling economic activity and stagnation in the first half of 2026. BSB’s projection for 1Q/2026 is 1.1% QoQ s.a.

Edition: 231

- 06 March, 2026

Energy

A large-cap trading at just ~11x earnings, with a ~12% FCF yield and will pay owners a 10% yield in the very near future. The Coterra deal markedly increases DVN’s stature and shale production in the Delaware Basin without incremental acquisition debt, adding ~4,600 high-return drilling locations, nearly half with sub-$40/bbl breakevens. The combined company expects $1bn+ in annual synergies and plans a $5bn buyback, materially lifting FCF/share and NAV/share. Nevertheless, investors have yet to adequately reflect DVN’s improved fundamentals in its share price, with it continuing to trade at a sharp discount to other E&P players in terms of both P/OCF and at a high required FCF yield. For each 0.5x improvement in its P/OCF multiple or a 1pp decrease in its FCF yield, DVN’s share price will rise by ~$5.

Edition: 231

- 06 March, 2026

G-III Apparel Group (GIII US), VF Corp (VFC US), Dillard's (DDS US) US

Consumer Discretionary

Hedgeye provides updates on 3 of their top Retail shorts. For GIII, they expect the next guide for the year to be an absolute disaster; forecasting a 20%+ cash flow hit from the the loss of major Calvin Klein and Tommy Hilfiger licenses back to PVH, while prior channel stuffing and tougher retail conditions could force the company to increase markdown support to key partners. Meanwhile, VFC is caught between a heavy debt burden and weakening brand momentum; Hedgeye believes a massively dilutive equity raise will ultimately be required. And finally, DDS remains a mispriced security, trading at ~12x EBITDA despite a sharply decelerating model and the company overearning by 800-1,000bp. That suggests that the real earnings power is between $10-20 per share. 5x earnings, is an appropriate department store multiple, suggesting 80-90% downside.

Edition: 231

- 06 March, 2026

Consumer Staples

Scott Mushkin remains cautious on TGT despite management acknowledging some operational challenges flagged in his field research. Recent store visits continue to reveal poor endcap execution, high levels of discarded items, long checkout lines, out-of-stocks and even extreme messiness. These nagging store operating challenges are likely to take more effort to overcome than management currently believes. He also sees several structural pressures ahead. TGT may need to sacrifice gross margin to improve price competitiveness, while everyday essentials could face deflation in 2026 amid heightened competition. Meanwhile, Walmart and Amazon are unlikely to cede share and TGT’s core demographic offers limited growth. Scott believes the recent swing to positive sales reflects easy comps and short-term consumer spending variability rather than a structural improvement in demand.

Edition: 231

- 06 March, 2026

China Internet: Opportunity after KWEB’s ~30% drop from its Oct peak

Sector valuation, as measured by 86Research’s proxy basket, now stands at a distressed 15.4x. Over the past 3 years, there has been 5 KWEB drawdowns >20% and each peak-to-trough episode lasting 3-6 months, suggesting the current correction could be nearing its end. Several catalysts may also help stabilise sentiment including Trump’s visit to China, the upcoming Two Sessions (additional stimulus) and improving economics from China’s AI leaders. In this issue of 86TradeIdeas, the team highlights several quality names that could command significantly higher multiples in a normalised market, including Trip.com, Atour and DiDi, alongside Beike, which could benefit from further housing policy support. Kuaishou and Baidu offer differentiated exposure to key AI verticals. Despite near-term geopolitical uncertainty, they see compelling re-rating potential across these names in the coming months.

Edition: 231

- 06 March, 2026

Oil: Into triple digits

Vandana Hari sees a risk of the conflict sliding into a war of attrition in the Gulf, with both sides expending missiles, drones and air-defence interceptors while testing each other’s stockpiles and endurance. The US may have already missed the window for a “strike hard and fast” outcome. Tehran is willing to stake everything and has mistakenly expected Gulf states to pressure Trump’s administration into standing down. For oil prices, the worst may still lie ahead; the market is still pricing in a least-bad outcome, one where the Strait of Hormuz reopens before long. One reason Washington may have refrained from unveiling sweeping measures to cool prices is that it is keeping its powder dry for a potential — perhaps expected — surge towards triple digits. Crude, products and refining cracks risk being bid into a vacuum if physical flows remain paralysed. Stay tuned.

Edition: 231

- 06 March, 2026

Wheat joins the bull market

Spot wheat stands at USD5.91. Chris Roberts points out how the USD4.50-5.50 area is viewed as a floor, based on price action since 2007 (floors and ceilings can be penetrated but sustained moves are needed to change them). The 64% decline in 2022-25 is in line with other major falls since 1996, that range from -63% to -73%. The 9-Quarter RSI bottomed just below Low Neutral 40, similar to the 2016 low. Chris’s base case is that commodity bull market has resumed and he has a number of commodity-related longs. In the Grains and Oilseed complex, he has longs in soybean and soymeal and is now looking to add wheat.

Edition: 231

- 06 March, 2026

Iran: The War in English

The “War in English”, as jokingly referred to by Israeli officials, has settled into an intense but steady pace. Niall Ferguson believes that US and Israeli objectives remain on track despite a geopolitical expansion of the war. Should Iran prove unable to muster larger missile or drone salvos by the end of the week, it would seem likely that it has no remaining capacity to do so. This should give shipping firms and insurers more confidence to begin transiting the Strait of Hormuz next week. If disruptions to the Strait continue into next week, Niall expects a major and coordinated SPR release from net importers to take place to reduce the stress in global crude markets. However, the potential costs of a protracted conflict and closure of the Strait is being underestimated by markets. It is imperative not only for the Trump administration’s political self-interest but also for global economic stability that the duration of this war be measured in weeks, not months.

Edition: 231

- 06 March, 2026

Online travel & AI

Consumer Discretionary

Gordon Haskett Research Advisors

Robert Mollins examines how OTAs are adapting to a rapidly changing environment driven by rising AI adoption. He focuses on 4 key themes: 1) AI as an emerging traffic channel; 2) structural advantages limiting disintermediation risk; 3) consumer-facing AI development across travel platforms; and 4) internal AI initiatives driving monetisation and cost-saving opportunities. AI companies have rapidly integrated tools into their assistants, raising concern over the technology’s ability to replicate functionality and reduce dependency on established platforms. Investor concern has extended beyond software into sectors with significant digital exposure, including online travel. While Robert acknowledges these risks, he believes AI assistants are more likely to evolve into a paid traffic channel rather than a vertically integrated travel marketplace capable of displacing Booking, Expedia and Airbnb.

Edition: 231

- 06 March, 2026

Helium: A commodity on the rise

Ben Finegold points out how the global helium market is a structural oligopoly, Qatar accounting for ~30% of the world’s helium supply. A prolonged conflict in the Middle East that disrupts production or shipments through the Strait of Hormuz could put a third of the world’s supply at risk. More importantly, the availability of helium iso-containers – critical to maintaining a global supply/demand balance – could be disrupted for at least 6 months. Demand for the commodity is accelerating, particularly in the aerospace industry where it is irreplaceable as a propellant of fuel. It is also used in semiconductor manufacturing and healthcare, where substitutes have yet to be found. How should investors play it? The Renergen Helium project, owned by ASP Isotopes Inc, produces both LNG and high-purity liquid helium from the same gas field, and is one of the world’s most significant helium developments and aims to become a major supplier.

Edition: 231

- 06 March, 2026

Industrials

With a market cap of $3.6bn, Nichias is an industrial insulation company that Asymmetric has followed for over 20 years. While the shares have outperformed the TOPIX over the long term, the performance gap has widened materially in recent periods, a trend Asymmetric believes can continue, highlighting the group’s: 1) cash-rich balance sheet and strong FCF, supporting rising shareholder returns; 2) ability to raise margins across its business segments; 3) exposure to maintenance work related to nuclear restarts in Japan; and 4) earnings gearing to the slower than initially expected SPE cyclical pick up.

Edition: 231

- 06 March, 2026

Nvidia's "Flammable Items"

Technology

Following NVDA's Q4 earnings release, Veritas believes several “Flammable Items” (these are items found in a company’s financial statements or within its operations that are waiting for a spark to ignite) it has previously identified are burning brighter and warrant continued investor attention. Their report examines whether supplier-funded demand is accelerating through channels including equity investments, a step-up in purchase commitments and expanded facility lease guarantees. The scale of these funding channels has increased materially, to the point where NVDA can effectively self-fund most of its reported revenue growth in the quarter. Veritas also isolates the contribution of “other income” in Q4 and presents an adjusted EPS intended to better reflect underlying operating performance. On this basis, they suggest that nearly the entirety of the Q4 EPS beat was attributable to “other income”.

Edition: 231

- 06 March, 2026

Gross margins are rolling over, but net margin expectations remain high

Median gross margins for the Top 500 peaked at 46.4% in Feb 25 and have since fallen to 44.9% in Jan 26, yet bottom-up forecasts imply continued strong net income growth - likely reflecting embedded AI-driven productivity assumptions. Historically, Trivariate finds valuation multiples correlate more closely with gross profit growth than net income growth, implying further multiple expansion will require renewed gross margin strength or a structural shift in how markets reward earnings. Their quantitatively derived longs (e.g. Merck, T-Mobile, McDonald’s) have had recent multiple expansion and are forecasted to have margin expansion, but not more net margin than gross margin expansion. While shorts (e.g. Amphenol, Salesforce, Arista Networks, Las Vegas Sands) screen for gross margin contraction but net margin expansion, reducing estimate achievability.

Edition: 231

- 06 March, 2026

South Korea: Words of warning

Jonathan Anderson observes that Korean equities shot up another 50% in the first two months, making Korea the best-performing market on the planet in 2026 so far. He notes that this is heavily due to the AI boom and Samsung, but "domestic Korea" has continued to rally this year as well. However, there's still no support from domestic macro. As before, Korea's economy is flatlining or contracting almost everywhere he looks: durables, construction, retail, credit, earnings. And while exports are rebounding, memory prices still haven't been able to bring Korea back to the EM-wide average trend. Jonathan says it will be hard to motivate further gains in local names. Equity multiples have already eliminated the famed "Korea discount" and continue to rise at the margin, i.e., corporate reforms have already been priced in well in advance of actual results - and there's no sign that the rally is boosting earnings and growth potential as of yet.

Edition: 231

- 06 March, 2026

Applied Optoelectronics (AAOI US) US

Technology

Rosenblatt reiterates their Buy rating and Top Pick status on AAOI. The company invested $209m in capex in 2026 with a focus on increasing laser and transceiver capacity in Texas. This ongoing investment is poised to drive a tripling of Data Centre revenues in 2026 and even faster growth in 2027. Amazon and Oracle 800G demand are the primary revenue drivers in 2026 along with Microsoft's solid 100G and recently renewed 400G demand. By 2027, all these customers should also be buying 1.6T. Rosenblatt’s 2026 revenues/EPS estimates increase to $1.02bn/$1.18. For 2027 their respective figures are $3.3bn/$6.25. Their new TP of $125 is based on 20x CY27 EPS forecast - a conservative multiple to account for execution risk.

Edition: 231

- 06 March, 2026

Real Estate

CEO Andrew Florance’s destructive leadership style makes him unfit to lead CSGP’s costly residential pivot. His rigid, totalitarian micromanaging is incompatible with the disciplined, multi-front execution now required, making his past strengths his current greatest liabilities. CSGP would be better served with Florance receding into an Executive Chairman role, where his visionary strategic brilliance could be offset by a disciplined operational CEO more focused on ROI than empire building. Paragon’s research includes interviews with former senior executives at CSGP who worked with Florance for more than 36 years combined.

Edition: 231

- 06 March, 2026

LeMaitre Vascular (LMAT US) US

Healthcare

Sidoti reiterates their constructive stance on LMAT, arguing the company’s increasingly dominant niche positioning supports durable pricing power, margin expansion and visible multi-year growth. With price increases contributing meaningfully to organic growth and ~8% additional pricing expected in 2026, Sidoti sees LMAT as insulated from reimbursement and tariff pressures given its focus on critical, non-deferrable vascular procedures and predominantly single-use devices. The company will continue to benefit from the continued sales force expansion and additional European product approvals over the next several years. Backed by a strong balance sheet and capacity for accretive M&A, Sidoti increases their 2026 revenue estimate to $275.5m (from $264m) and EPS estimate to $2.86 (from $2.39). For 2027, they raise their revenue estimate to $291m (from $278m) and EPS estimate to $3.09 (from $2.67).

Edition: 231

- 06 March, 2026

A new Gulf war begins

For months, Jawad Mian has been writing about the situation in the Middle East and about the likelihood that Iran would eventually face an attack. He says this is not another short episode, but the beginning of a far longer cycle of instability. For the US, rising oil prices or market disruption could become a political liability ahead of the November mid-term congressional elections. With the joint US and Israeli strikes on Iran intensifying and the killing of Iran’s Ayatollah Ali Khamenei, the entire strategic landscape of the Middle East has tilted. Jawad sees three objectives driving this conflict: regime change, neutralising Iran’s nuclear threat and controlling Iran’s oil exports. However, regime change requires troops being on the ground; instead Jawad observes that what we have is a heavy intelligence footprint, targeted strikes, leadership decapitation efforts and infrastructure degradation. This can destabilise a system, but it does not automatically produce a new one.

Edition: 231

- 06 March, 2026

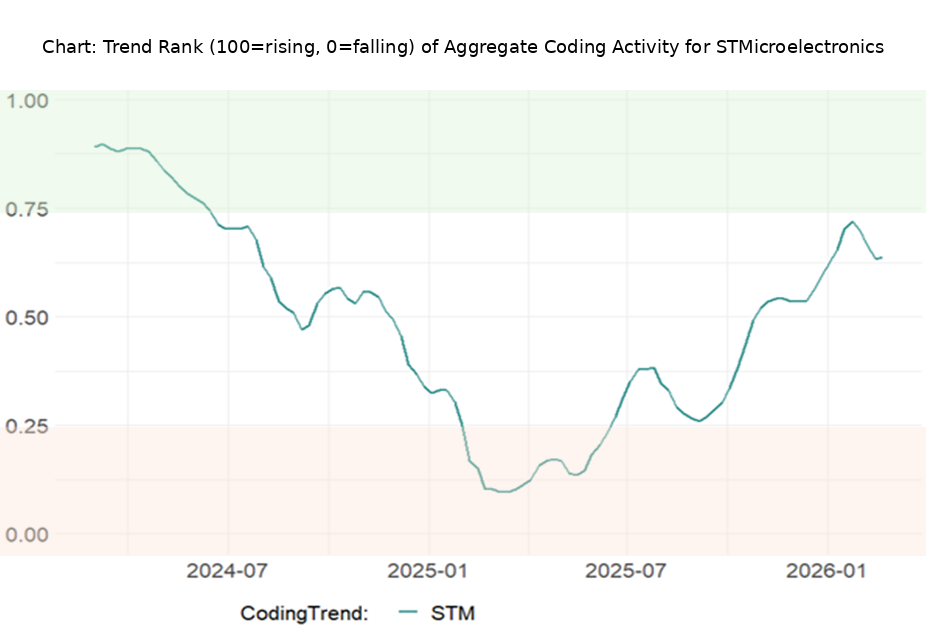

STMicroelectronics (STMPA FP) France

Technology

STM ranks in the upper tier of AnteData’s Coding Trend Ranking. Coding activity is trending on GitHub, showing rising developer interest in the company’s microcontroller platform. These projects typically focus on motor control, sensor reading and basic communication as used in robots, drones, cars and industrial machines. Besides, StackOverflow discussions and Google search trends are also positive, suggesting sustained ecosystem relevance and technical inquiry. In a bullish scenario (10% revenue CAGR over 5 years), operating leverage could materially expand margins, implying meaningful upside vs. today’s ~$30bn market cap.

Edition: 231

- 06 March, 2026