Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Guidance warning season

Despite rising geopolitical risk, European corporate guidance has yet to reflect the potential economic impact. In AIR’s recent management meetings, discussion focused almost entirely on AI, with little attention paid to the Iran conflict despite surging energy prices and supply-chain stress that historically drive earnings revisions. The combination of unpriced macro risk and AI-driven sectoral disruption creates a credible basis for expecting a meaningful wave of 2026 earnings guidance revisions across European equities in the coming weeks. And the performance gap between the companies on the right side of these structural shifts and those on the wrong side will broaden. Stock winners include AI infrastructure beneficiaries such as Arm, Elmos, Aixtron and STM, alongside defence exposure at Exosens and Indra Sistemas. Euronext and Auto1 are also seen as largely insulated. Under pressure are Stroeer, Freenet and SES. In IT services, the sector is splitting between “The Conquerors” (Accenture, Cognizant, Reply) and “The Endangered” (Capgemini, Atos, Sage, Dassault Systemes, SAP).

Edition: 232

- 20 March, 2026

Insider buying in beaten-down Tech stocks

Technology

Smart Insider flags a number of insider buys at Hexagon, Sage and ATOSS following recent share price weakness, ranking all 3 stocks +1 (highest rating). At HEXA, the new CEO, Chief Strategy Officer and Vice Chair made their first purchases, buying a combined €3.4m of stock, shortly after results and the announced spin-off of Octave Intelligence. At SGE, 2 long-serving non-execs bought stock, including one director tripling his holding in a rare purchase and at a higher price than his last buy 5 years ago. At AOF, the CEO invested €11.6m (adding 4% to his stake) and the long-tenured CFO made his first-ever purchase - a notable shift from a series of smaller sales.

Edition: 230

- 20 February, 2026

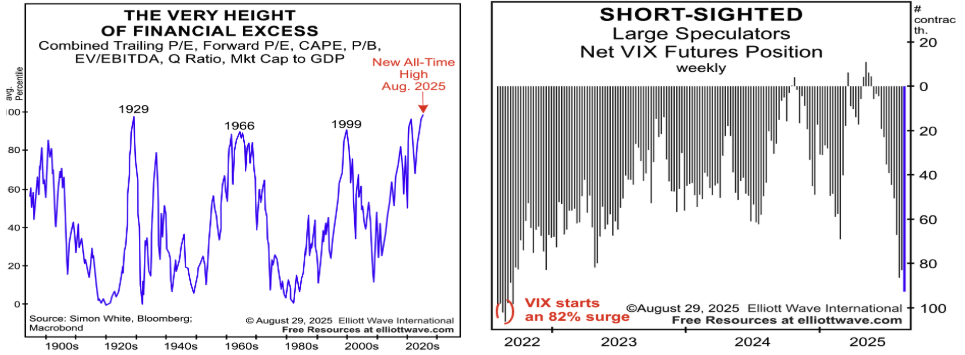

US stocks the most overvalued in 130 years

There is no escaping overvaluation if you are a multi-decade investor. The seven typical valuation measures that Craig Ferguson monitors are now at such an extreme that at nearly a 99th percentile rating the level of US equity market overvaluation is now the highest level seen since 1980 when records pretty much began. The signal is clear: long-term investors should be markedly UW stocks and largely out of US equity markets. This may be against consensus as the globe remains OW equities, but this is at a time when old sage Buffett is raising cash to $35 or more of his portfolio just as he did in the two most recent major overvaluation episodes in 1999 and 1966. Chart 2 shows that large global hedge funds are now nearly as short S&P VIX futures (or volatility) as they were in late 2021, just before the Nasdaq plunged by -38%. This won’t end well for equity markets.

Edition: 219

- 05 September, 2025

Technology

SGE’s AI strategy is taking shape, positioning the company competitively in the SMB software market. While not a first mover, what matters most for the business is having a clear GenAI roadmap and up-to-date AI functionalities. The integration of Sage Copilot with Sage Network enhances customer retention and cloud migration, reinforcing SGE’s ecosystem. However, the monetisation strategy for AI agents remains uncertain. The shares trade at an estimated 21.9x FY25 and 18.8x FY26 adjusted EV/EBIT multiples, which is relatively reasonable given SGE’s successful migration to a subscription model. The challenge for the company now is how AI agents will disrupt its business model and potentially evolve it into a consumption-based model.

Edition: 208

- 04 April, 2025

Technology

Slowing sales - Woozle’s latest channel checks reveal a weaker than expected Q/Q performance, particularly in North America. Resellers highlighted tighter budgets for SMBs, leading to extended deal cycles and deal spillage into 1Q25. Stronger performance in Europe, especially the UK, provided a partial offset. SGE implemented a 6% price increase on Intacct as of 1st Oct, significantly lower than prior years. Larger deal sizes were noted as the company moves upmarket, though deep discounts up to 30% were often required to secure deals. Woozle’s Q4 revenue estimate is +9.5% Y/Y.

Edition: 199

- 15 November, 2024

UK: Plenty of interest

The Willis Welby team revisits their review of UK growth names they put in place at the start of 2023. They have 104 stocks in their UK coverage with market caps north of USD 2.5bn. Nineteen of them make their screen of consensus Y3 revenue growth in excess of 6%, reasonable financial productivity, and an implied Y3 EBITM ratio of less than 110. The performance of this approach has been okay since May 20, with the mean move of the 18 names at -0.8%, which is ahead of the -2.1% return from the FTSE 350. The team remains of the view that the UK has plenty of interesting and growing businesses. And enough of those names are still available at attractive prices, including the likes of Sage, Convatec and IHG.

Edition: 189

- 28 June, 2024

Consumer Staples

ROCGA has recently launched a product that ranks companies using their own CFROI based DCF valuation modelling tools. The list contains the UK’s largest companies ranked according to warranted value, the most undervalued to the most overvalued. CWK appears in the top part of the list, along with Sainsbury, Imperial Brands and ITV. Among others, Sage and Ocado appear at the bottom. ROCGA also covers the US and European markets, with over 2,150 companies in total.

Edition: 168

- 01 September, 2023

Technology

67% of Woozle’s sources* reported positive outlooks for the next 6 months. New business has started to pick up again and SGE appears poised to win market share, especially among SMEs, as well as a growing presence in the enterprise market with the expansion of Intacct. Competitive pricing, product simplicity and flexibility with SaaS has put the software company on pace to beat 1H23 consensus estimates.

*Woozle conducted interviews with ERP software resellers, channel partners and consultants. Their sample evenly reflects both SAP and SGE, with some sources selling both brands, as well as Oracle and Microsoft. Regional split: 60% Europe / 40% N.America.

Edition: 160

- 12 May, 2023

UK growth stocks

One easy response for equity investors faced with such a radical change in the backdrop for equity pricing this year is to assume that growth stocks can get further derated. Willis Welby, who use expectations analysis to help decode share prices, differentiates between duration stocks which require a transformation in business models and growth stocks which do not. They draw particular attention to IHG, Burberry, Compass, Sage, Auto Trader and Experian. Notable absentees from their analysis are the industrial fan club stocks of Croda, Halma and Spirax which did not make their consensus Y3 revenue growth criteria.

Edition: 147

- 28 October, 2022