Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

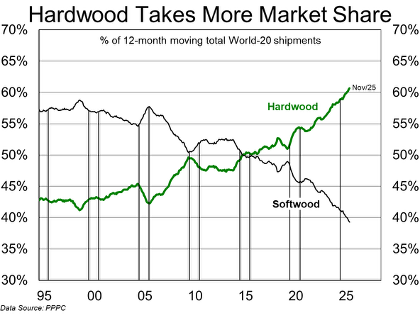

Hardwood gains more market share

The hardwood share of global pulp shipments reached an all-time high in 2025. As global hardwood pulp capacity has grown at a faster rate than softwood and given production costs are ~$300/mt lower, the potential rate of substitution of hardwood into established softwood markets has been a key variable in determining the demand growth rate of each grade. Hardwood pulp producers will clearly benefit, although they have challenges, including exposure to China’s rapid build-out of integrated domestic pulp capacity and the burden of recent huge greenfield mill capex. There’s also the threat that upcoming BHK capacity additions will simply step into expanded hardwood market opportunities. The ERA team see upside in Suzano SA but highlight that R$ swings may require nimble repositioning. They remain cautious on NBSK near pure-play Mercer International Inc given a very stretched balance sheet and little room to manoeuvre. Without more shuts, NBSK prices have little near-term upside.

Edition: 228

- 23 January, 2026

Materials

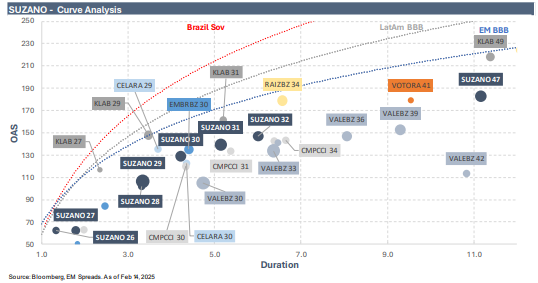

Despite additional industry supply, tight market conditions persist due to low stock levels, maintenance-related production cuts and operational disruptions. Healthy pulp prices, higher sales volumes, controlled costs and a focus on deleveraging should support Suzano’s cash generation and credit profile in 2025, with this trend likely continuing as no major new supply is expected. Within Suzano’s capital structure, EM Spreads prefers the 3.750% 2031 and 3.125% 2032 bonds, which compare favourably to select regional peers, the broader EM BBB Index, and the US BBB Index. Additionally, these notes trade below par at $90.1 and $84.6, respectively, while most of Suzano’s curve remains priced above par.

Edition: 205

- 21 February, 2025

Sustainable plays in a diverging world

Diverging economic activity between EMs and DMs suggests that investors should look for opportunities in EM companies with credible sustainability characteristics. If most of USD strength is behind us, then EM companies with exposure to global markets could benefit from weak exchange rates before they start appreciating against the USD over the medium term – and those with exposure to India’s secular growth story should continue to perform well in the current environment. From a tactical perspective, holding a diversified basket of EM sustainable companies in various industries and countries could offer interesting upside for investors looking to gain exposure outside of traditional DM sustainability plays. In this context, SMS believes that companies such as Hero Motorcorp, Suzano and Klabin offer good value at a reasonable price.

Edition: 161

- 26 May, 2023