Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Consumer Discretionary

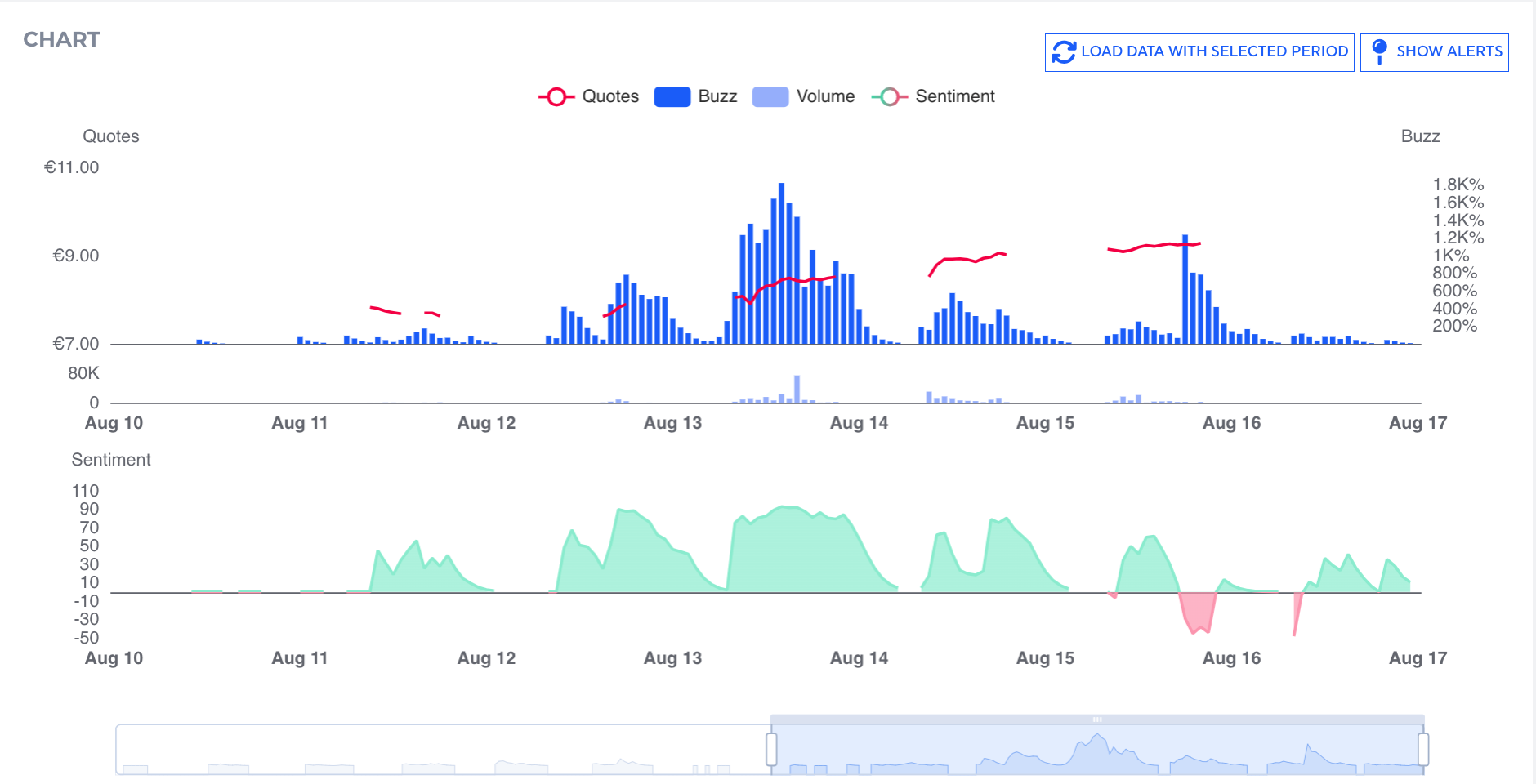

Stockpulse, whose platform provides real-time insights into social media sentiment, highlights a wave of positive attention around TUI. This was particularly apparent on 12th Aug, when the company reported a buzz score of 443% and a sentiment score of 86. This surge in communication and positive mood could be attributed to the company's recent earnings guidance update. Given the significant increase in market sentiment and buzz ahead of the earnings announcement, along with the positive stock price movement and exceeded earnings expectations, TUI's short-term outlook appears bullish. However, the market will need to assess whether this momentum can be sustained in the coming days and weeks.

Edition: 218

- 22 August, 2025

Consumer Discretionary

Recent equity raise not enough to mend fragile balance sheet - €1.1bn rights issue brings the total raised this year to €1.6bn. However, this substantial cash injection is neither sufficient to guarantee covenant compliance nor to allow the firm to delever organically. In the short/medium term Forensic Alpha anticipates a further capital raise as well as materially weaker results vs. competitors. TP €1.20 (58% downside).

Edition: 122

- 29 October, 2021

Jet2 (JET2 LN)

Industrials

‘Blue Skies Ahead’ - StockViews’ 28-page report explains why JET2’s competitive advantage at a local level remains underappreciated. How contrary to perception TUI (Short recommendation) has not benefitted from Thomas Cook's demise and remains vulnerable to JET2’s superior product. The tour operator is also resilient to competition from OTA’s such as On The Beach due to a higher quality experience and competitive pricing. ROIC should rise above 20% as the proportion of package holiday customers grows from 50%+. 70% upside.

Edition: 108

- 16 April, 2021