Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

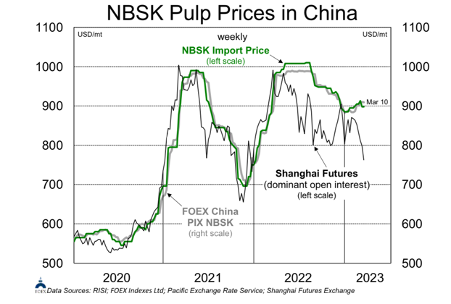

NBSK Pulp prices in China

After a spike in January, the Shanghai pulp futures have reversed course, ending last week at $769, a price level not seen in the front contract since late 2021. Following the Western Canadian closure and downtime announcements, in combination with expectations of robust China demand, an optimism that pulp prices would make early gains had pervaded the market. This has been unmet, largely in part due to extremely soft paper and packaging markets in Europe and North America and poor Chinese demand. Downward pressure may be exacerbated by expectations for market expectations for new hardwood supply from two new greenfield mills coming online in LATAM. Tissue producers will benefit from lower pulp prices, including Cascades and Clearwater Paper. Mercer continues to be the preferred route to pulp exposure for long-term investors, with the softer outlook already priced in valuations.

Edition: 156

- 17 March, 2023

Forest Products: Tough year ahead

Materials

The outlook for lumber / panel producers (Canfor, West Fraser, Boise Cascade, Louisiana-Pacific) is difficult, with no obvious upside catalyst before a recovery in US housing (unlikely before late 2023). ERA expects pulp prices to move lower through 1H23. Anticipated price declines are now almost fully priced into pulp names (Mercer, International Paper). In packaging, more pain lies in store for containerboard (Westrock) and a raft downtime will be needed to combat weaker demand and offset new capacity. Boxboard will outperform (Graphic Packaging, Clearwater Paper), with both demand and prices expected to remain robust.

Edition: 151

- 06 January, 2023