Remain overweight Taiwan, China and Korea

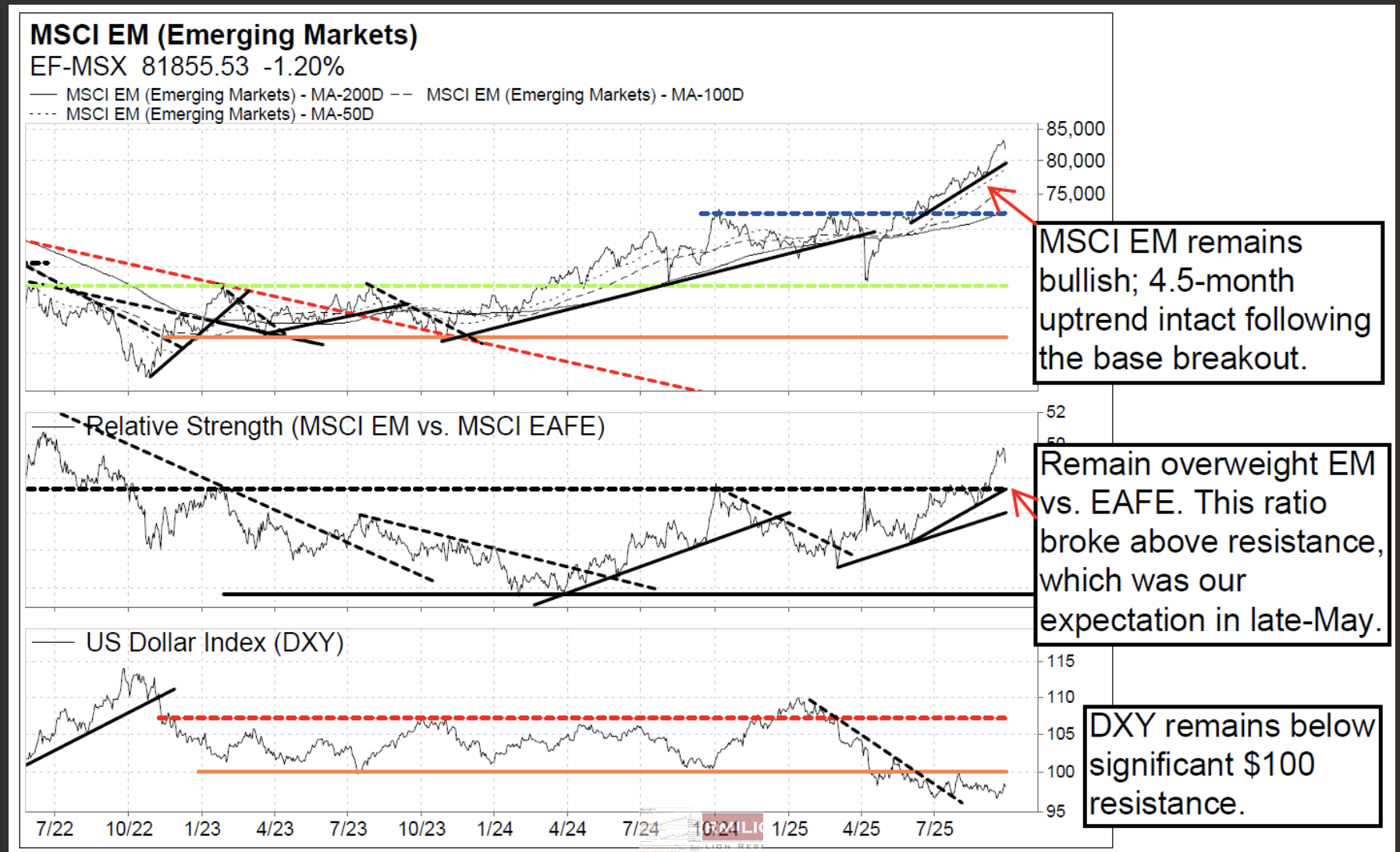

According to David Nicoski, the MSCI Emerging Markets index (local currency) and EEM-US (USD) are both trading within 4.5-month uptrends, and he remains bullish. David expects support at the uptrend, which also coincides with the 50-day MA and $50.65 horizontal support on EEM-US. He would view any pullback to $48 support on EEM-US as a buying opportunity. For EM countries, while price remains attractive, he is downgrading Greece to market weight due to RS deterioration. EM countries where he remains overweight include Taiwan, China, and South Korea. Additional leadership countries include Vietnam, Romania, and Pakistan. For EM sectors, defensive EM sectors (staples and utilities) continue to underperform and are at YTD RS lows; underperformance has continued, as expected -- avoid. Meanwhile, attractive EM sectors where David expects outperformance include: MSCI EM technology, consumer discretionary, materials, and communications. He is also monitoring for a RS bottom on EM health care.

Argentina tries… orthodoxy

From a muddle-through approach fraught with renewed peso and inflation risk, to more classically orthodox measures, Jonathan remarks just how much the policy stance has changed in the past three months. This is the best chance of getting money growth and inflation back down into low double and ideally single digits, at the cost of keeping the economy in recession. In the face of the country’s anaemic export economy, the only hope for external stabilisation is to keep overall demand and import spending weak. Even if Argentina holds course, it doesn’t guarantee a stable peso, and the needs to give up the USDARS 1,500 "ceiling" and let the exchange rate find its level without endless borrowing support. The recent backup in dollar yields has opened tactical value, but not necessarily a structural buying opportunity; there's a big difference between successfully stabilizing the macro position and finding an exit strategy for external indebtedness.

Brazil: Benefitting from uncertainty

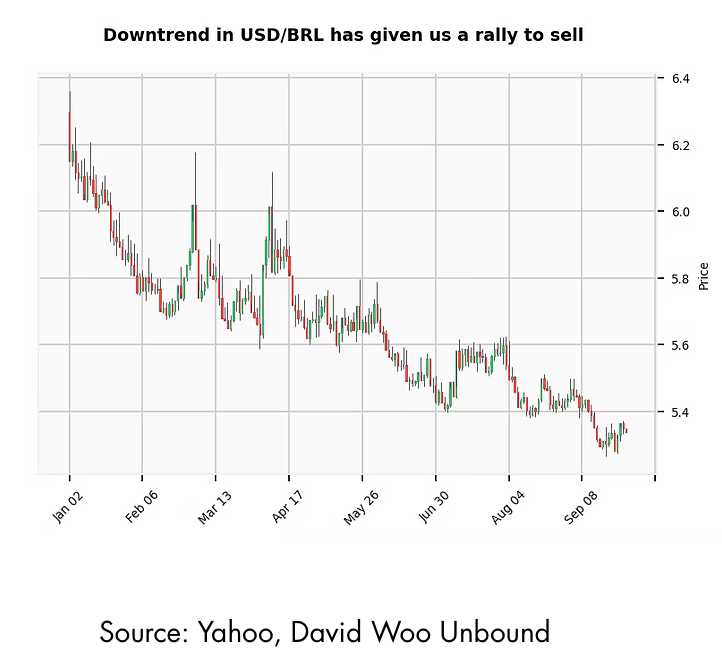

The short-term trend in the dollar switched to a bull trend against most currencies as rates reversed higher last week. This wasn't the case for MXN and BRL however, where David Woo points out that the correction to the trend wasn't sufficient to reverse it. BRL in particular failed to get above pivotal resistance at 5.40. Brazil has been a beneficiary of the trade war between US and China, with China choosing to purchase soybeans from Brazil. Uncertainty about the future of the government in Argentina has also been a tailwind for BRL. A shutdown in the US should be beneficial for carry trades as markets will have little guidance from data to change macro views. David bought the November BRL future at 0.18625. He’ll take profit on a move to 0.1930 and stop out at 0.1820.

China: Holding against resistance

Chris Roberts comments on the Shanghai Composite (3,828), which has been ranging above 10-year resistance at 3,500–3,732 for five weeks. Daily chart indicators have now unwound very overbought readings (14-day RSI reached 88, just below extremely overbought 90), and the area of the rising 40-day WMA has been acting as support since May. The ranging above major resistance is seen as a sign of strength, and there is a low-risk entry here that allows Chris to try an initial long position. Go 50% long at market. His initial stop is a daily close below 3,695.

How will China monetise AI differently?

Report by

Blue Lotus Research Institute

China will be a close and capable AI follower, focusing on downstream implementation as the US focuses on upstream. This means the two will not run head-to-head encounters right away, and China can lead in the application of AGI in manufacturing and logistics. Its monetisation path will be more complex but can exist. However, as it stands, China is under-monetising AI vs the US. The Blue Lotus team estimate that consumer (2C) AI applications generated $2.0–3.5bn in the US and $0.3–0.5bn in China (excluding AI-enabled advertising and much of video AI). The US monetises AI globally, with global 2C revenues bringing in ~12x that of China. However, the gap will shorten significantly by 2030, in part by taking a lead on robotics+AGI. The team reiterate their top picks of

Alibaba,

Hesai,

CATL and

Kuaishou.

Baidu stays as a sell.

Should investors re-enter India?

Jonathan Anderson’s growth proxy index has rebounded to around 5% y/y in the past few months, with a renewed pickup in credit activity and earnings. It may be below the official 8% real GDP growth rate, but is a very respectable pace nonetheless. The external balance is back in surplus on the back of weak imports and low oil prices, inflation continues to fall, the fiscal balance is "just enough" to avoid serious trouble, and the RBI still has room to cut rates at the margin. Jonathan sold his Indian equity position a year ago, and the index has underperformed since then. This is still an expensive market on any valuation metric - but if he really sees the cycle stabilizing and growth maintaining at 5% or more, he is certainly considering a re-entry. Stay tuned.