Upside surprises expected from some central banks

Report by

MRB Partners

MR

Most central banks will be welcoming of currency appreciation to dampen inflationary pressures. In the short-term, there is greater room for upside surprises from other central banks, particularly the ECB, providing support for select pro-growth currencies. However, central banks in economies with greater household debt imbalances will be unable to lift policy rates the same degree cyclically without causing significant disruption. Netting out these crosscurrents, Phillip Colmar recommends mild overweight exposure to the euro on a 6-12 month horizon, but barbell this with the more defensive Swiss franc. Avoid commodity-based currencies and the pound.

Inflation pressures show no signs of easing

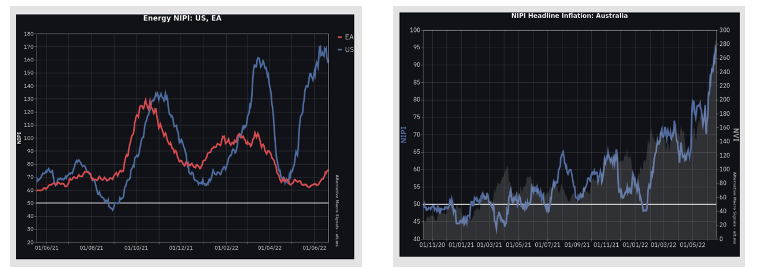

The News Inflation Pressure Indices (NIPI), developed by Alternative Macro Signals, scans an extensive range of new sources to track and forecast inflation across the globe. In their latest report, they find that US energy price pressures remain very strong and that consumers should expect sharp rises in utility bills this summer, a potential source of upside risk relative to consensus (see graph 1). Meanwhile the euro area shows no signs of easing and Australia stands out among DMs as inflation momentum strengthens considerably as the country’s NIPIs reach fresh all-time highs (see graph 2).

Euro set to fall below parity

Large imbalances, no embedded fiscal transfer mechanisms and a lack of safe assets are all some of the Euro’s underlying structural flaws that are now again being exposed by the latest global monetary tensions. Could a political fix solve the issue? Michael Howell doesn’t think so, especially with the anti-inflationary instincts embedded in Northern Europe. The only practical path for policymakers is to ‘do a Japan’ and crash the Euro. Michael is staying SHORT EUR.

As safe as houses

Historically, housing has proven a good hedge against inflation, but this does not mean that frothy housing markets are exempt from sharp declines, especially during a steep hiking cycle. As central banks tighten in response to the recent surge of inflation, warning signs are flashing across global housing markets. New Zealand, Canada, and Australia are now experiencing the start of a housing market correction. The housing markets in the UK and Ireland are also starting to cool. Niall Ferguson expects US residential real estate prices to flatline and then moderately decline over the next year.

US: Blowing up the bubble

Michael Belkin believes excessive US stimulus pumped up an enormous speculative bubble in US risk assets and turned investors into bubble people. Sure, dominoes are already falling but sentiment has yet to grasp what happens in a severe recession, which is now developing: ‘good news’ on inflation becomes bad news for earnings, stocks and the economy. A rude awakening awaits. Michael recommends selling and shorting into brief market stock market bounces, shifting LONG exposure into defensive consumer staples, utilities and health care and SHORTING tech, consumer discretionary, materials and energy.

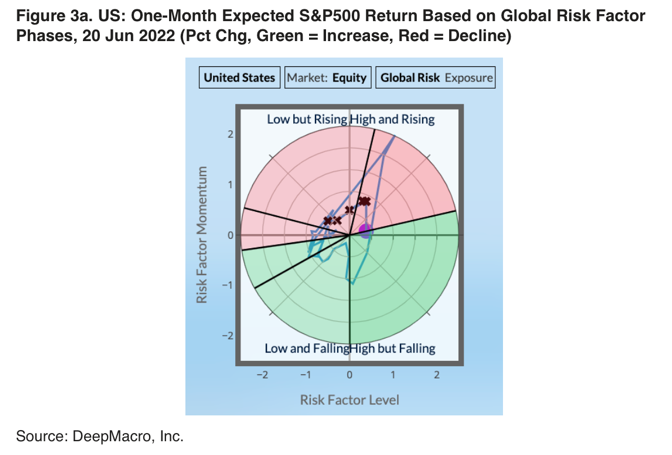

Questions on US equities

The growth outlook isn’t necessarily the problem facing equities, claims Jeffrey Young. Data has been slowing for many months and the equity market has been declining. Surprisingly, the risk outlook isn’t the problem either with risk levels today the same as over the last few months (see marked graph). The real issue is inflation; in order for it to be less of a threat to the market, it needs to develop significantly more negative momentum. Expect this to take a quarter or two before the short-term outlook for equities improves.

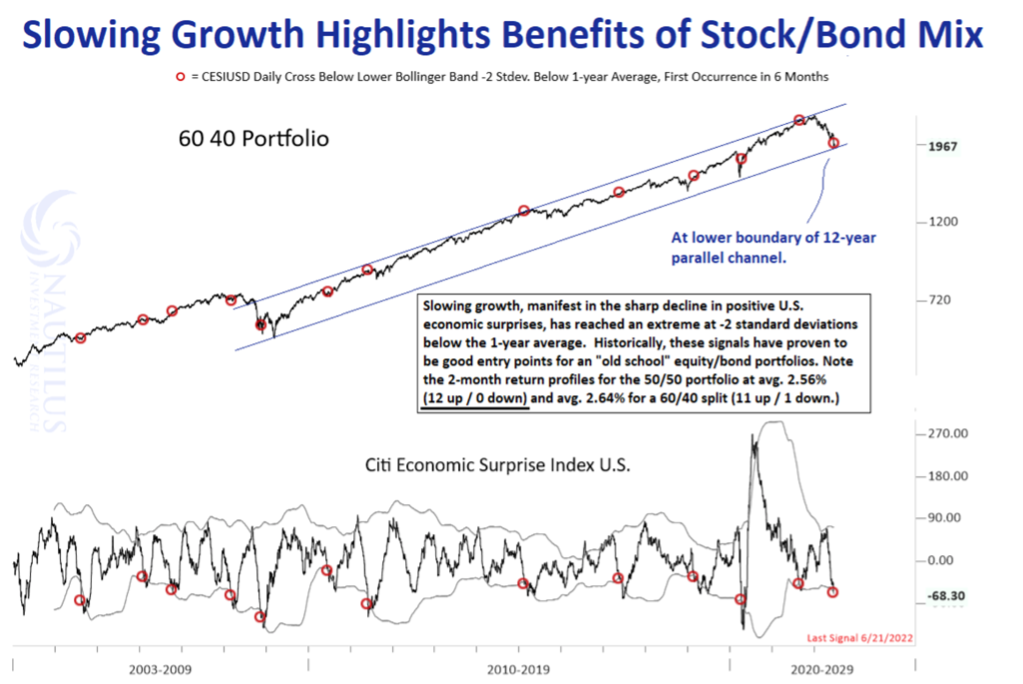

US: Bonds typically add value when economic data slows

Bonds have become more attractive as the Fed hikes rates to combat inflation and recession becomes increasingly likely. In historical observations when US economic data was much worse than expected for an extended period, a classic 60/40 portfolio including the S&P500 and the S&P Aggregate Bond Index returned 2.64% two months out, while a 50/50 mix produces a 2.56% return; a mix of stocks and bonds typically produces a positive outcome over the short-term more often than a portfolio entirely consisting of one or the other.

Australia unlikely to tighten aggressively as Fed

After a surprise 50bp hike in the RBA’s last meeting, futures pricing indicate they will tighten more aggressively than the Fed (see graph). Gerard Minack disagrees; Australia doesn’t have the same underlying inflation than the US, and the economy is more sensitive to changes in short rates. The RBA is right to tighten policy but were it to do so as much as the market expects, it would threaten to explode the housing market.