Why the USD is strong and why it could get even stronger

Michael Howell argues that the US Dollar is being pushed higher by rebounding US private sector cash inflows alongside the tight control of new liquidity supplies by the Fed. Positive US private sector cash flows, in turn, are partly explained by the persistent stream of foreign capital into US dollar assets, but largely by the Biden Administration’s remarkably loose fiscal policy. A strong dollar is not a consensus trade. However, it could prove self-correcting if the resulting disinflationary pressures compel the US Fed to ease monetary policy in 2024, which could help to underpin markets. Despite the widespread assertion that the US dollar system is threatened, the paradox of a potentially stronger US currency needs to be watched.

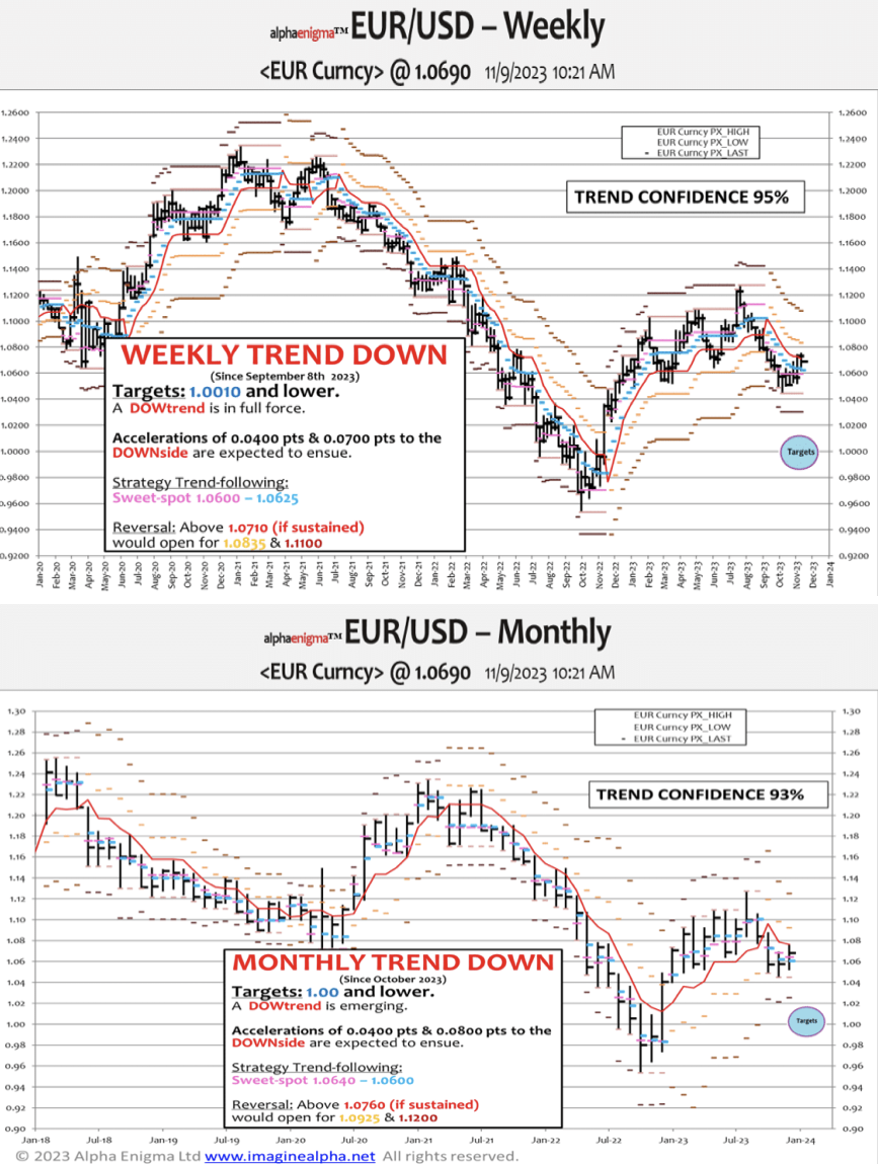

EUR/USD 1.070/60 will resist further favouring 1.00 better than 1.12

The “triple alpha” downtrend was downgraded on October 24th as EUR/USD staged a rally toward 1.0750. That level is very significant as it is a combination of the weekly and monthly timeframes overhead resistance between 1.070 and 1.0760. There is no upside potential for the EUR short of a thrust through that area, explaining the range bound price action that has unfolded recently. In the weekly outlook for the coming 4-13 weeks (chart 1), the timeframe is favouring the downside. In fact, the 1.0700 area is an ideal entry point for intra-quarter traders/hedgers. More work needs to be done for a full reversal. Over the next 3-12 months (chart 2), the overcast resistance is strong (to put it mildly) and 1.00 remains more likely than 1.12 for the time being.

Portugal: Europe’s Japan

Following a 77.5% decline in 22 years, Portugal now has a positive equity story. The Euronext Lisbon PSI is on the verge of breaking out from a 17-month Ascending Triangle, following a shallow retracement of the 2020-22 bull market (chart 1). A weakly close above 6,560 would be viewed as a breakout, targeting 7,900, after which the Grey Investment team would likely recommend a BUY. Looking at chart 2, the secular bear market is over and the weekly chart breakout would take the index clear of key monthly resistance around 5,800. A long secular decline destroys an equity culture among local investors, but there will be plenty of young investors who will not have the bad memories that come with prolonged market losses.

US: Macro headwinds from trade, inventories and customers

Trade volumes have been supported by the auto sector’s extraordinary run. With the auto runway running out, however, non-auto trade volume and paltry inventory breadth speak to further downgrade risk to near-term US growth prospects. Non-autos fell -3.6% and -3.5% in Q2 and Q3, reversing the typical recession pattern of autos falling first and highlighting the magnitude of the chip shortage-induced catchup. Not to be left out, consumers’ nervousness is rising as they contend with higher delinquencies across the consumer debt spectrum. Rising auto delinquencies in particular point to continued implosion of the used vehicle bubble which will push core consumer goods prices into deflation.

Japan: Land of the rising sun

Report by

Musha Research

MU

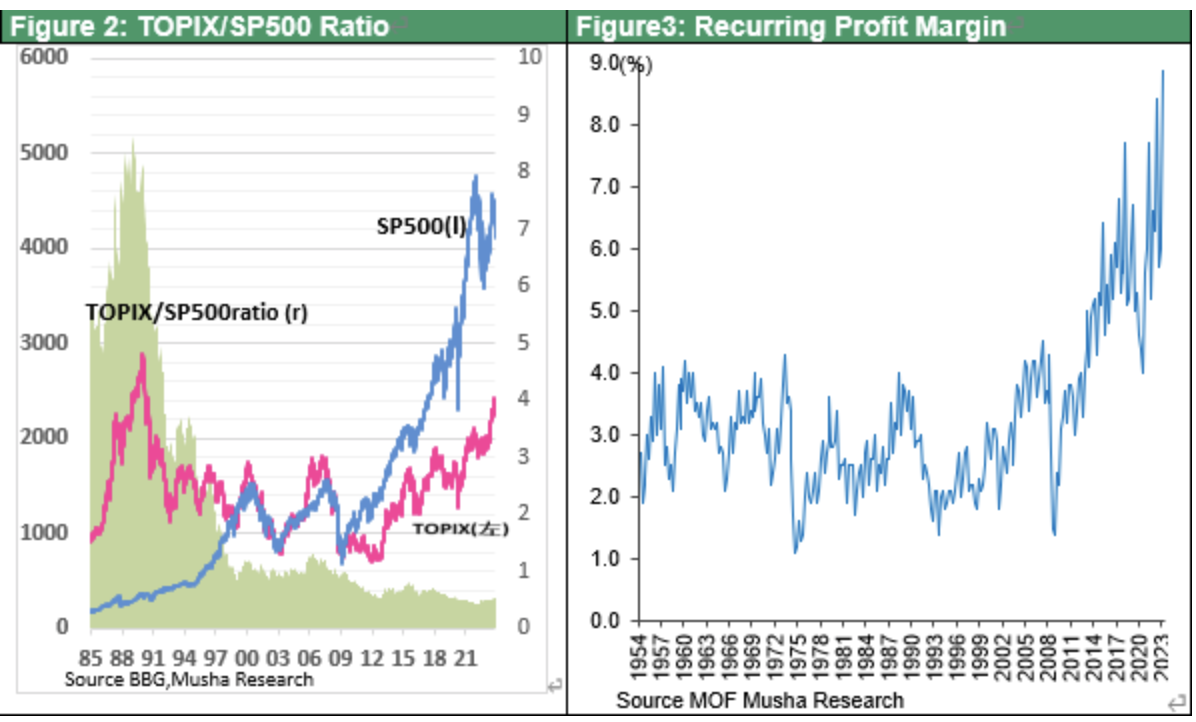

Japan may be the brightest of major economies in both politics and the economy, according to Ryoji Musha. Even though Kishida administration’s approval rating has fallen, its base of power is solid. The economy’s robust performance stands out amidst the downward revisions in China and the Eurozone. Investors around the world have developed an attitude of neglect for Japan over the last 30 years, that is until recently; the chart shows the multiple of TOPIX vs the S&P500, which has seen a recent and rapid increase to 0.54x. Ryoji points to the transformation stemming from evolving attitudes in initiative-taking and major changes in the geopolitical environment. Japan’s time has come.

An underweight in Industrials is rare and often spells trouble

Report by

Harlyn Research

Simon Goodfellow has downgraded the Industrials sector in four regions this week – to neutral in the UK and Pan Europe and to underweight in the Eurozone and Japan. In the last four weeks, it has lost ground in every region. In the 28-year history of Simon’s models, the Industrials sector has had the lowest number of underweight recommendations out of all eleven sectors (incl. Small Caps) and this is normally an indicator that investors are concerned about the onset of a recession. Small Caps have also seen a big reduction in their recommended weight over the same period, which reinforces these fears.