Europe

Technology

Iron Blue initiates coverage on HEXAB with a score of 34/60, which is top decile (fertile ground for shorting). Key areas of accounting focus include 1) Revenue recognition. 2) Stripped out one-off costs, share payments and PPA amortisation. 3) R&D capitalisations and contingent consideration releases. 4) Acquisition disclosures and strategy of buying HEXAB distributors. Regarding governance, they note the auditor lead partner’s relationship with HEXAB’s largest shareholder network, a non-independent board and committees, 2 classes of shares, CEO / CFO internal succession, Greenbridge relationship and unclear CEO annual bonus payout metrics. Iron Blue also flags a fairly large number of areas where disclosure could be improved.

Technology

Using IFX’s new guidance and Arete’s existing growth assumptions for FY25 which reflect PSS and CSS still below FY23 annual peaks, 24% growth in EV power and ADAS revenues (vs. 34% in FY24) leaving the rest of autos still down 3% from their ’23 levels and assume segment margin still below peak ’23, this implies an adjusted EPS of above €3 leaving IFX on 11x FY25 vs. its 10-year P/E average of 18x. With the needed financial reset in place, Arete sees the path clear for investors to own a heavily discounted but very well positioned growth story into the coming autos / industrial upturn. TP €57.2 (75% upside).

Europe Top 200 Weekly Technical Strategy

The SXXE tests 2021 highs. Both short- and medium-term Breadth are failing at the tops of their ranges, showing negative divergence with the indices. Technology and Media made new highs, while Insurance made a new high but no new relative high. Banks may be struggling, they edge to a new high but now encounter relative resistance. Retail may form short term tops. Energy reasserts short term downtrends, while Health makes a new medium-term relative low. Stockcube’s portfolio remains net long with 42 long positions and 18 short. Recently opened trades include Sartorius Stedim Biotech and Stellantis (both long) and ArcelorMittal (short).

European & UK insider trading trends

Last month saw 446 insider purchases (individuals) from 346 companies, spending a total of €2.2bn. Smart Insider upgraded 15+ stocks, meaning they currently have 70+ ranked stocks and just 2- ranked stocks. Upgrades were spread out among 10 countries with Germany leading. From a sector and industry perspective, sentiment was bullish in Basic Materials and Energy (Sell/Buy Ratio 0.28) and slightly bearish in Technology (S/B Ratio 1.05). The Consumer Sectors (Discretionary & Staples) led upgrades with a combined 8+. Positive ranked stocks based on Jan insider purchases include Syensqo, Colruyt, Technip Energies, Hugo Boss, Pirelli and Ebro Foods.

North America

Fast & accurate analysis of due-diligence documents for their level of deceptiveness and truthfulness

Deception And Truth Analysis (DATA) provides a scientifically based assessment of the deceptive and truthful behaviours of people. Proper assessment of these behaviours is significantly predictive of future outcomes, including stock price increases and decreases. DATA provides a rapid and highly accurate assessment of the 98.3% of financial data that is contained in language, not in numbers. Independent validation of DATA Scores has found that a portfolio constructed of the 200 most truthful components of the S&P 500 provides an average annual excess return advantage of 6.26% from 2008 through 2023. Click here for further information.

Communications

SNAP shares sink 35% amid fears over growth. Craig Huber provides his take on the company’s 4Q23 results and updates his earnings estimates. He remains bearish with a 12-month TP of $8 per share based on 2.3x 2025(E) revenue or 26.6x FCF. Craig continues to view SNAP’s smaller scale as a disadvantage to larger peers in this environment and much prefers Meta’s fundamentals and stock. Despite the law of larger numbers, META saw advertising in 4Q grow 24% vs. SNAP’s total revenue growth of 5%, and for 1Q24 Craig expects 26% ad revenue growth at META vs. only 14% growth for SNAP.

Communications

Iron sharpens iron - the combination of the UFC and WWE assets brings together two unique and exceptionally entrepreneurial leadership teams to create a combined sports juggernaut with the opportunity to leverage each other’s strong suits and propel TKO to new heights. In thinking through the core business of each operator, Northcoast sees a mid-to-high-single digit organic growth rate excluding any major step in rights renewals. Given this growth rate and roughly 70% of revenues contractually positioned each year, they feel the quality of earnings and cash flow is high. Northcoast initiates coverage with a Buy rating and TP of $105.

Consumer Discretionary

Where BOOT's latest results diverged from John Zolidis’ expectations, was in the Mar quarter outlook, which was worse than expected. Despite the cut to forecasts, he is still more than $1 below the Street in EPS for the Mar 2025 fiscal year. There is also little (or no) sign of any turn in the business. Comps are deeply negative. And the company continues to try to offset the decline in demand by accelerating unit growth, shifting more of the assortment to private brands and by reducing staffing in stores. Absent a change in top-line, John continues to see risk of much lower earnings and a further negative re-rating of the shares.

Consumer Discretionary

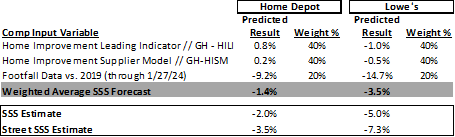

GHRA’s 3-factor predictive model points to upside potential to their 4Q23 SSS estimates for HD and LOW. Based on the weighted average results from their 1) Home Improvement Leading Indicator; 2) Home Improvement Supplier Model; and 3) Footfall traffic data, GHRA believes there could be upside to their estimate for HD of -2.0% (vs. predictive model of -1.4%) and LOW of -5.0% (vs. -3.5%). GHRA is bullish on both stocks, but leans more favourably towards HD given its significantly higher PRO penetration (as DIY faces steeper headwinds while PRO backlogs remain healthy); accelerating store growth; and incremental $500m of cost savings in FY24 that help mitigate EPS downside.

Financials: 24 things to think about in 2024

Capital Alpha financials policy analyst Ian Katz has compiled a comprehensive list of his thoughts on 24 financials topics he’ll be watching this year including: 1) Court Battles, 2) Congressional Review Act, 3) Basel Endgame, 4) Bank Mergers, 5) CFPB vs. Big Tech, 6) Equity Market Structure, 7) Crypto Legislation, 8) Credit Card Competition Act/Durbin 2.0/Durbin-Marshall, 9) FedNow, 10) Insurance Regulation, 11) FSOC Designations and Non-Banks, 12) Housing Finance, 13) Cannabis Banking, 14) Other Bank Issues: Liquidity, Long-Term Debt, Stress Tests.

Financials

BN is a work in progress. Today, it is complex and messy, but that is the opportunity. Abacus sees a potential 20% IRR over the next 5 years based on: 15% NAV growth, plus 5% from closing of the 30% discount to NAV. They are attracted to alternative asset managers in general as the structural tailwinds are strong. Cyclically, alt managers should see earnings recover in 2024 and 2025 with M&A transactions and fund-raising recovering. Abacus believes exaggerated real estate fears are providing BN at a discount to their estimated fair value. Management has the cash flow and is motivated to close this discount. TP $65 (60% upside).

Financials

The actions by the OCC reinforce Veritas’ preference for RBC to remain focused on Canadian banking and for the divestiture of its US subsidiary, City National Bank. However, this seems increasingly unlikely as it will take several years for the bank to resolve issues outlined by the OCC. Additionally, further monetary penalties may be levied if sufficient progress is not made. These actions will likely also weigh on CNB's profitability as costs associated with resolving these issues place upward pressure on CNB's efficiency ratio. These actions by the OCC may serve as prelude for potential actions against TD Bank with a substantial monetary penalty and a cease-and-desist order likely in play.

Industrials

Specified, niche, asset-light manufacturer, with high barriers of entry, driving leading share and superior cash generation in fast growing end markets. Each of WOR’s divisions should benefit from key drivers of US “Golden Era” for construction: 1) increased government stimulus and support; 2) environmental investment; 3) population shift; and 4) re-shoring / near shoring. EBITDA margins stack up favourably vs. peers (21% vs. peer median of 18%); FCF conversion (86%) also compares favourably peers (83%); and net debt leverage of 0.3x provides ample room for acquisitions. Despite its favourable position, WOR trades at a significant discount to peers (~8.6x EV/EBITDA vs. peers at ~12.5x).

Technology

4Q23 sales declined 4% q/q, but MPWR's position in AI was able to offset demand weakness in many of its other end markets. Kinngai Chan believes the company will remain well positioned in the AI-related and computing markets and expects both areas to support future quarters' outperformance. Additionally, he expects gross margin will improve to the high-50% range in 2H24 as next-generation design wins ramp coupled with lower pricing from the foundry. MPWR can continue to grow faster than its peers and outperform consensus expectations in the near to medium, driven by content growth, share gains and new markets.

Technology

Report by

Pernas Research

RELY is the leader in cross border digital remittances for migrants and has a long revenue runway with attractive scale economics. Q4 earnings are scheduled for 28th Feb and will be an intense point of market focus. Recent sentiment is exceedingly negative as the company's increased marketing spend is viewed by the street as defensive. Pernas believes increased marketing spend is a positive given attractive LTV/CAC economics and this coming earnings should mark a meaningful shift in sentiment. 100% upside.

Since inception in 2017, the Pernas Portfolio has significantly outperformed the S&P 500 by an annualised 13.06%. Recent successful calls include: Donnelley Financial (+580%), Centrus Energy (+350%), Franklin Covey (+118%) and Meta (+70%).

Technology

Andrew Freedman sees a limited growth market, pricing pushback on renewals and underwhelming AI debut as key concerns. His view is supported by a detailed TAM analysis where he estimates / aggregates the ACV for ~20,000 global customer / prospects based on SKU level pricing information. Additionally, his primary research efforts suggest NOW's "assertive" pricing and bundling tactics will be met with greater pushback as the company attempts to pass through another ~30% price increase onto existing customers. Even though there is much left on the AI product roadmap in 2024 and beyond, Andrew believes investors will be disappointed in NOW's ability to monetise. 30% downside.

10Q / 10K text analysis

By utilising AI, NLP, data analytics and qualitative analyst oversight, 280First can glean material and actionable insights on companies which will be missed by most institutional investors. Recent highlights include: 1) Lockheed Martin - changing expectations for future aircraft delivery; LMT’s 2023 10K no longer references its previously expected 156 per year delivery rate. 2) Adobe - brighter capital resources outlook. Acquisitions planned? 3) Alphabet - higher expectations for operating margin trend. 4) Comcast - concerns on multichannel video provider agreements. 5) Mondelez - losing shelf space due to disputes. Delay / unable to raise prices. 6) Sysco - dialling back growth expectations.

Emerging Markets

1Q24 eCommerce Consumer Survey

Consumer Discretionary

Report by

RedTech Advisors

While consumers are more pessimistic in RedTech’s latest quarterly survey, last order trends and grocery preferences highlight continued disruption under the surface of eCommerce. Short video continues to make clear gains with Douyin leading the way, while CGB and local service are again advancing. The gains for short video are almost exclusively driven by Douyin, with Kuaishou making no progress in recent surveys. PDD and Meituan are also making gains in their corners of the eCommerce landscape while Alibaba, the biggest incumbent, continues its inexorable decline.

Consumer Discretionary

Report by

Blue Lotus Research Institute

Now, is not the time for bottom fishing - Blues Lotus expects Meituan’s operating profit margin to remain under pressure in the medium term due to intensified competition. They lower their 4Q23 non-IFRS NI estimate by 23% and lower 2024/25 non-IFRS NI by 19%/21% to factor in the margin dilution effect from the company’s continued low-price strategy in food delivery and IHT, and slow progress in cost reduction in Meituan Select. Blue Lotus’ earnings estimates for 2024/25 are 20%/25% lower than consensus. The stock trades at 16x PE in 2024, at the high end among peers.

Financials

Triple jeopardy in play for 2024? Victor Galliano thinks management’s guidance for this year is overly optimistic due to: 1) Structurally rising capex and opex, especially in view of the launch of digital bank Bineo this month, but also to support the growth of Rappicard; this is at least partly in response to intensifying competition from the likes of Nu Mexico. 2) NIM pressure - expects more widespread competition for deposits from other commercial banks as well as fintechs to pressure system margins further. 3) With system delinquency trends deteriorating, Victor believes this will catch up with Banorte in coming quarters in the form of a steadily rising cost of risk.

Multi-patterning is an economic dead end

Technology

In his latest note on the Semiconductor Wars: US vs. China, Richard Windsor argues that the media is not being clear in terms of where the real ability of the Chinese semiconductor industry to compete lies. He believes the economics for SMIC in making chips at both 7nm and 5nm are truly awful and that yields are below 10%. This is unsustainable especially given the weakness of the Chinese economy and the other crises that the Chinese state is having to deal with. Consequently, there is no danger of the Chinese competing with leading-edge semiconductor makers outside of China and Richard is sceptical whether they will be able to do so at any node below 20nm.

Developed Markets

UK: Bordering on the rough

Sunak finally delivered on what Boris Johnson had promised the DUP in Northern Ireland (NI), a compromise that is acceptable to everyone – the EU, Brexiteers and the DUP. Two new pieces of legislation are expected to be agreed by the UK-EU Joint Committee, which will ensure no checks for goods destined for NI and confirm its place in the UK. However, Wolfgang Münchau sees the real test coming in the future. The commitment may discourage the UK from diverging too much from EU regulation if they have to do an impact assessment each time. There’s also the introduction of the Stormfront brake, giving the NI assembly the ability to object to new EU rules that could affect NI’s trade agreements – should the EU take a different regulatory course to the UK, expect objections to come forth from the assembly.

UK: Cheap cheap

Data on the UK economy was a bit mixed back in November, but Tony Willis feels better now. His consumer squeeze graph has moved into positive territory, PMI surveys are back over 50, house prices rose in Q4/2023. Tony isn’t as optimistic about short rates or long rates as some others; the BoE is right to take care, and bond markets have got to swallow a lot of government debt issuance across the Western world. Tony doesn’t see interest rates structures as much of an issue for the progress of companies. And while the median implied to Y3 EBITM ratio for his global large cap coverage is now close to 100, his UK equity coverage stands in at just 68.5 for those with market caps between USD0.3bn and USD0.5bn. UK equities are seriously cheap.

UK: Understanding the shrinking money supply

On the M4 definition of the UK money supply, there has been a £125bn contraction (~4%) since September 2022. Some of those who sounded the inflationary alarm when annual money growth hit 12% in 2021 are now predicting a collapse into deflation. However, a careful examination of the monetary data suggests that the unwinding of leveraged LDI strategies after September 2022 is largely responsible for today’s negative money supply comparisons. M4 holdings of Other Financial Corporations (including LDI vehicles) have fallen by more than 16% since the crisis erupted. While broad money growth, excluding other finance corporations, has slowed to a crawl, this is a natural reaction to a sudden tightening of credit conditions. The ratio of household and non-financial company deposits to nominal GDP remains elevated: the UK retains an inflationary bias in 2024.

Czech revival needs more CNB help

The ECB, BoE and Riksbank are all banking on higher real wage growth to revive consumption and restore growth, allowing for a more gradual easing cycle. The CNB is no different, but Manoj Pradhan believes it may have to ease by much more than it thinks it has to. The current policy mix isn’t supportive for growth, the growth mix (consumption revival vs inventory correction) is unconvincing, and the country will be dragged down by Germany’s austerity and China’s ailments. The CNB will slowly acknowledge that r* has fallen and that reviving growth will require r to fall below r*. Over the course of 2024, receiving 2y Czech vs Poland and/or being LONG CZK vs PLN will pay off, but now may not be the right time to enter the trade if you haven’t already.

The German mess

As Niall Ferguson has been warning for some time, the age of predictable, consensus-oriented German politics is over. Political conflicts about money and migration threaten to boil over, provoking large-scale protests and strikes. Chancellor Olaf Scholz’s zombie government is unlikely to regain traction, which means that growth-oriented economic and fiscal policy is unlikely until 2026 at the earliest. Germany is therefore set to enter the 2025 federal election year with an economy in trouble and a far-right party in the ascendancy, and it is likely that Olaf will become the country’s first one-term chancellor since the 1960s. It is hardly the Weimar Republic. But it is a long way from the once-dependable powerhouse of Europe.

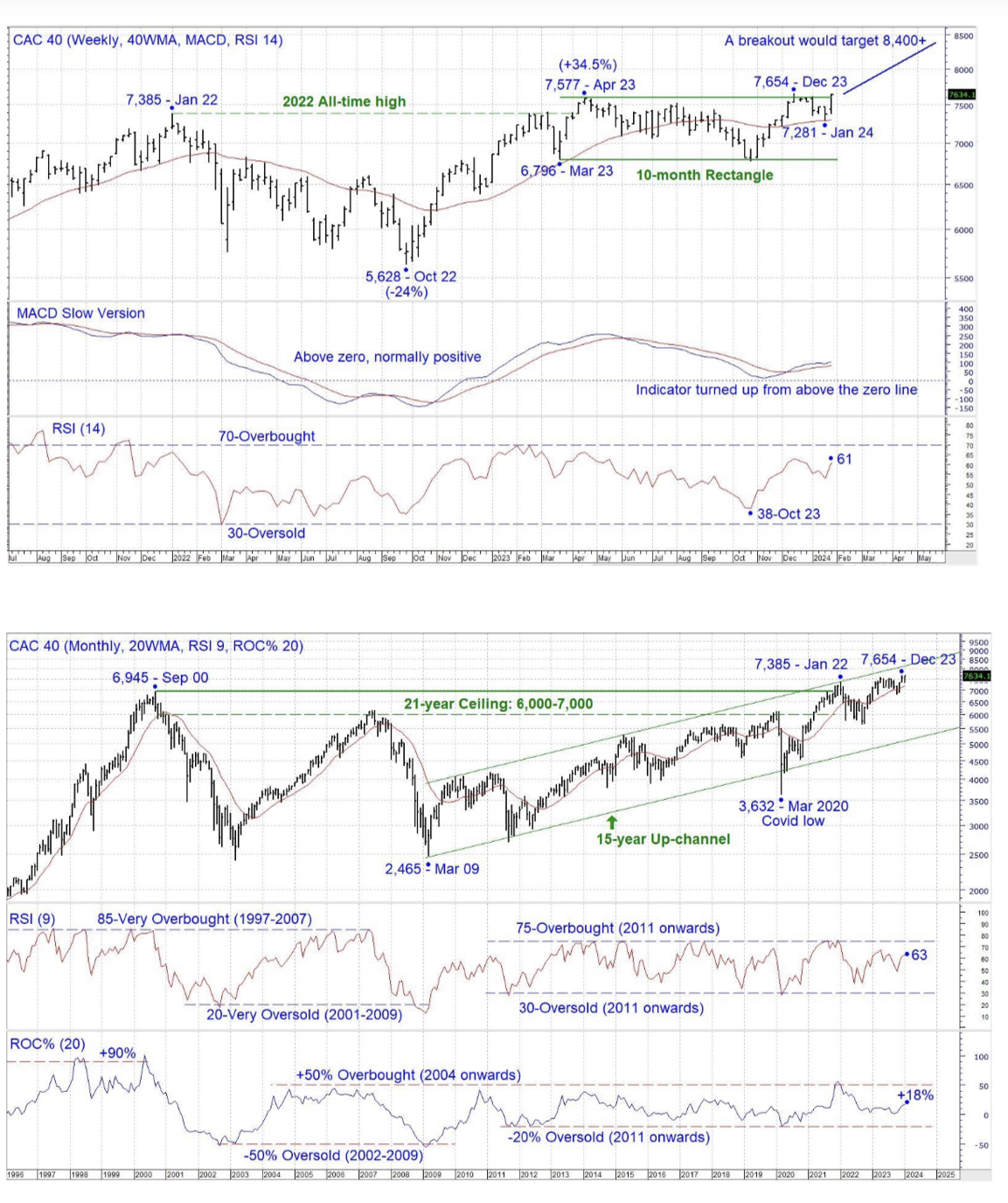

France: Possible breakout?

The CAC 40 set a new all time high of 7,654 in December, closing in on a breakout above the 21-year ceiling which would have a minimum target of 12,000-14,000. The index is just below the top of the 15-year Up-channel, a potential barrier. Chris Roberts will use a buy strategy that is building on the weekly chart; a weekly close above 7,800 would be viewed as a breakout, targeting 8,400+, which will trigger a BUY. The stop loss for a breakout would be a daily close below 7,208.

US earnings forecasts are too high if the economy slows

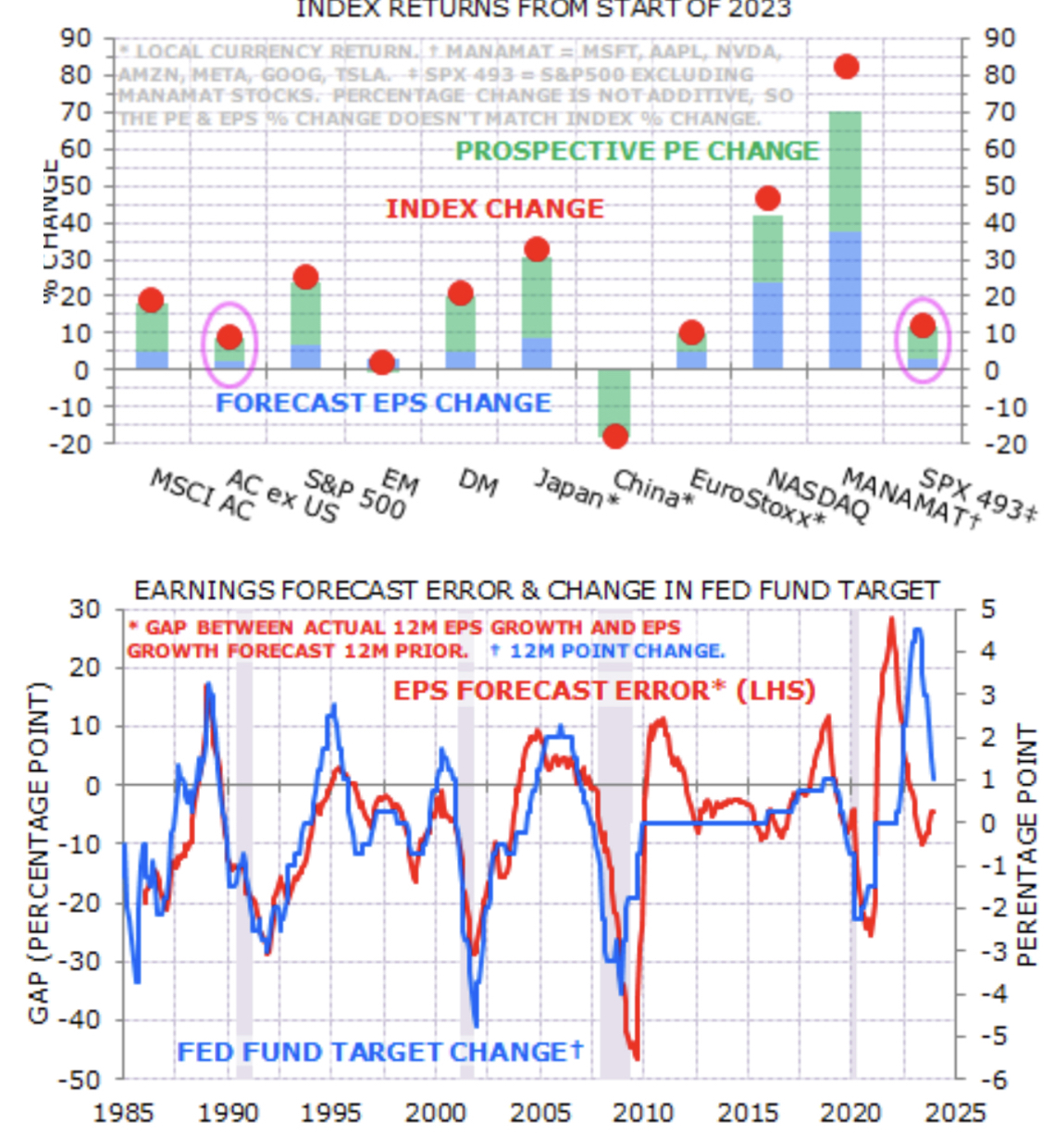

Gerard Minack explains how strong EPS growth has been the key to US equity outperformance since the GFC, largely in part due to the magnificent 7. 2023 was no exception, with S&P493 (S&P500 minus Mag 7) performance (chart 1, far right bar) looking similar to the all-country ex-US performance (second bar from left). The sell-side consensus now expects a significant acceleration in S&P493 growth this year, in addition to further EPS growth from the big 7. However, Gerard does not see this level of EPS growth occurring, especially if there is a hard landing – a much higher possibility than many believe. He also sees a chance that a full-blown market bubble inflates in 2024; the key to such bubbles is not low interest rates, but rising earnings optimism. With AI optimism potentially upgrading US IT sector EPS forecasts even further beyond the already sharp increase, higher interest rates may not stop a further rerating of US equities.

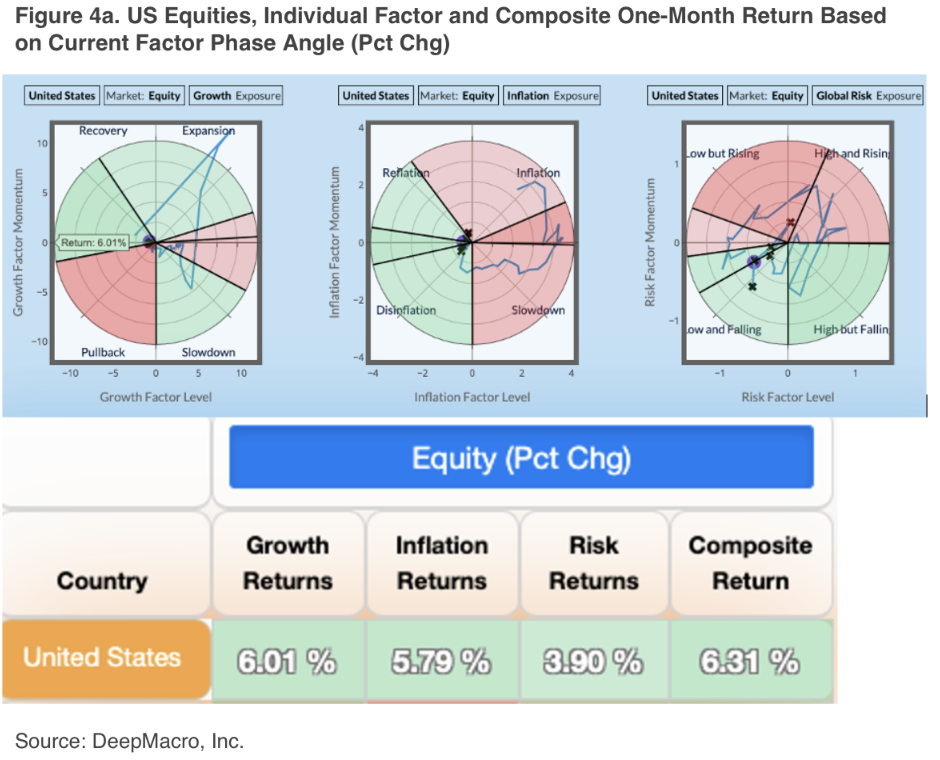

US mini upcycle is positive for equities

DeepMacro’s Turning Points Trade Tool has a BUY on US equities. According to Jeffrey Young, the growth factor, the US inflation factor, and the Global Risk factor are all at phases of their cycles that have been associated with positive 1-month forward equity market returns in the past. What happened is that we saw growth, inflation and risk aversion all fall. Once that happened, growth could begin to pick up, further improving risk sentiment. The decline of inflation and risk aversion have been self-reinforcing and have put the US economy in a good position for the equity market. So even though in the DeepMacro system growth is below trend, it is not a negative for risk assets.

Japan: FOMO

Report by

Musha Research

MU

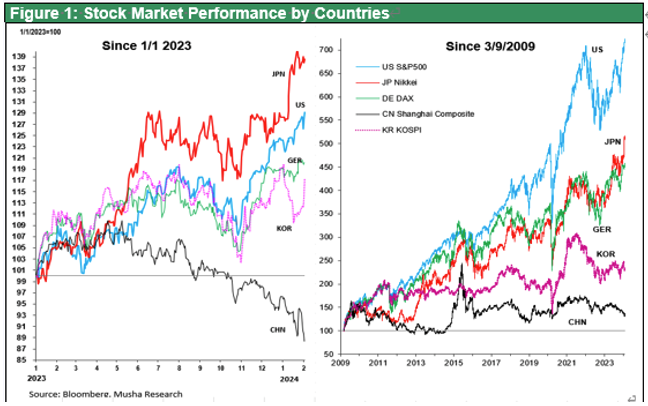

Ryoji Musha says the Japanese stock market is now entering a phase where there is a growing fear of missing out (FOMO). Investors have finally realised how ridiculously undervalued Japanese stocks are and are rushing to increase their exposure (see figure 1). We are also seeing individual investors experience a boom due to the start of NISA reform, and corporations are buying back their own shares under pressure from the Financial Services Agency and the TSE. Additionally, pension funds and other institutional investors are forced to reduce their investment ratios in JGBs, shifting instead to stocks in the face of inflation entrenchment and rising inflation rates. The equity-driven fund management system has begun in Japan.

Playing steep vs safe: CHF/JPY

Andreas Steno finds it increasingly likely that the BoJ will kill the world's last negative policy rates. As an anchor to this view, he finds the CHF safe haven to be a tad overstretched. While Andreas doesn't see any massive inflation problem in Japan, he notes that vanilla forecasts are hinting at higher core pressure and that the services component has yet to capitulate. As a result, he thinks it prudent to be long JPY in relatively carry neutral expressions. The SNB will likely have to follow suit when the G10 cutting cycle commences, while the BoJ can accept to be the odd hawks out for a while due to the exceptional weakness in the JPY over the past few years. He opens a new FX position: SHORT CHF/JPY, target 159.60, S&L 172.35 (spot-ref 170.55).

Emerging Markets

China: Off the grid

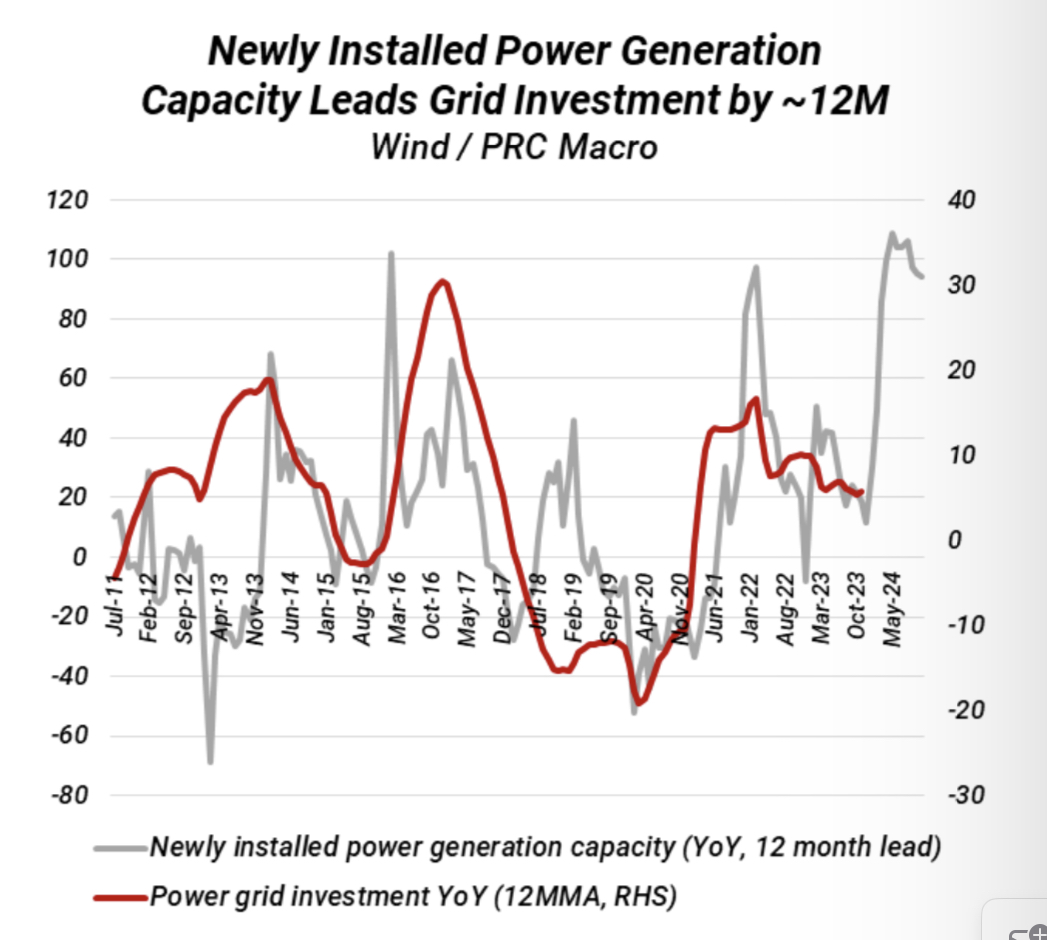

Investors have been worried about a potential contraction to grid investment in China after the State Grid (SGCC) suggested no incremental growth to investment this year. However, William Hess believes the State Grid only provided vague language as a result of the central government’s 2024 targets not yet being finalised. In the context of a massive build-up to renewable energy generation capacity against low connectivity, SGCC is one of the main actors who can close the gap, a glaring imbalance that will need to be resolved in the final budget. William reiterates his call that grid investment in China has been substantially underpriced by markets and could grow by 10% YoY or even higher. As a result, he continues to believe that copper prices could retest former resistance of USD 10,000 per metric ton as early as Q2 this year.

China: The rebound of dividends and the decline of growth

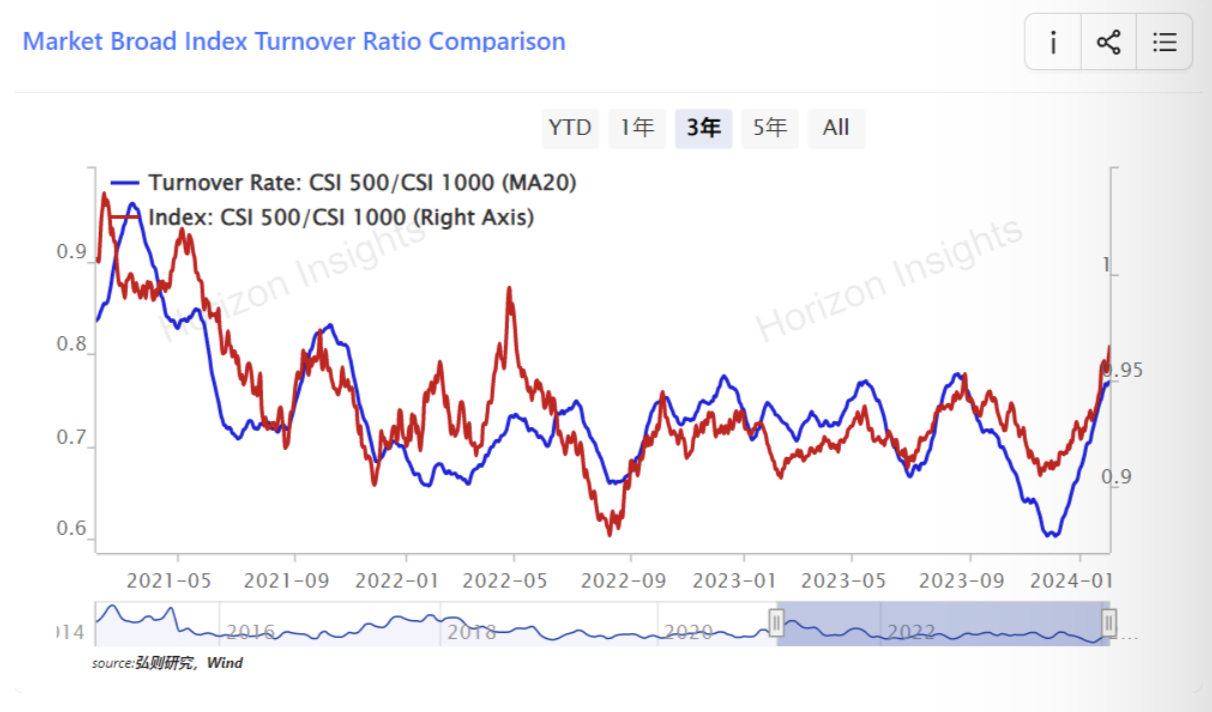

Amidst the extreme trading behaviour in the A-share market, there is a significant overcrowding in dividend stocks, with investors moving away from small- and mid-caps; a trading reversal may take place soon. Despite the recent sharp decline in the A-share market, its turnover has shown a consistent increase and investors should not be rash to run away and explore alternatives. The Horizon Insights team believes that sectors like agricultural and forestry industries, social services, and transportation should be positioned for better performance, driven by improving ROEs and valuation growth.

India: Unravelling the tacit threads in the pre-election budget

India’s Finance Minister recently presented the interim budget ahead of the general elections to be held in April-May. On the surface, the budget looks apolitical, eschewing any grand announcements typical to pre-election budgets and enabling the central bank to concentrate on controlling domestic price trends and international events. However, the accounts send a clear electoral message to key groups of voters. Strategically, the budget marries fiscal prudence with targeted support for the middle class, recognizing their electoral influence amid post-Covid economic challenges. With inclusive language and region-specific gestures, the budget tactically addresses swing voters in southern India, countering religious polarisation perceptions for electoral expansion. Balancing the continuity of benefits for low-income groups and fiscal responsibility, the budget signals the continuation and periodic expansion of income-support schemes.

Kenya: The good news and the bad news

The good news is that Kenya continues to show positive near-term macro adjustment, with monetary tightening at home and improvement in fiscal and external positions. The bad news is that, as before, there’s no medium-term exit strategy from Kenya’s foreign debt burden; Jonathan Anderson continues to see the country as an eventual debt restructuring/default case. Spreads could continue to narrow this year and the shilling could stabilise depending on global market conditions, but Jonathan does not see Kenya as a structural buy.

South Africa: Keeping the lights on

In recent years, South Africa’s economic growth has been constrained by frequent blackouts due to the poor performance of Eskom, the national power utility. Eskom’s failure is also a major political problem for the governing African National Congress (ANC). Niall Ferguson expects the government to postpone decisive action, burning expensive diesel and avoiding controversial reforms before this year’s general election, which will likely be held in May. After the election, he expects further bailouts of Eskom but an eventual unbundling and partial privatisation of the South African power industry. The gradual process will result in better energy availability and higher growth potential, but only in the longer term (2025 onwards).

Commodities

Oil: The war premium

When Al Jazeera tweeted that Israel had agreed to pause the war in Gaza as part of a ceasefire agreement, Brent futures pummelled down to $78 from a recent high above $83. That crude was in mild recovery mode on the following Friday but far from staging a strong rebound suggests the market was already starting to price in a truce sooner or later. Should a deal not materialise soon, one can expect the risk premium to creep back in, but Vandana Hari has been working on the assumption that the parties might be closing in on an agreement. She takes up a NEUTRAL position in the near-term, corresponding with Brent hovering in the $77-$79 range. For the second half of February, she is mildly bearish, corresponding to Brent sliding to $75 or potentially slightly lower in the wake of a deal.

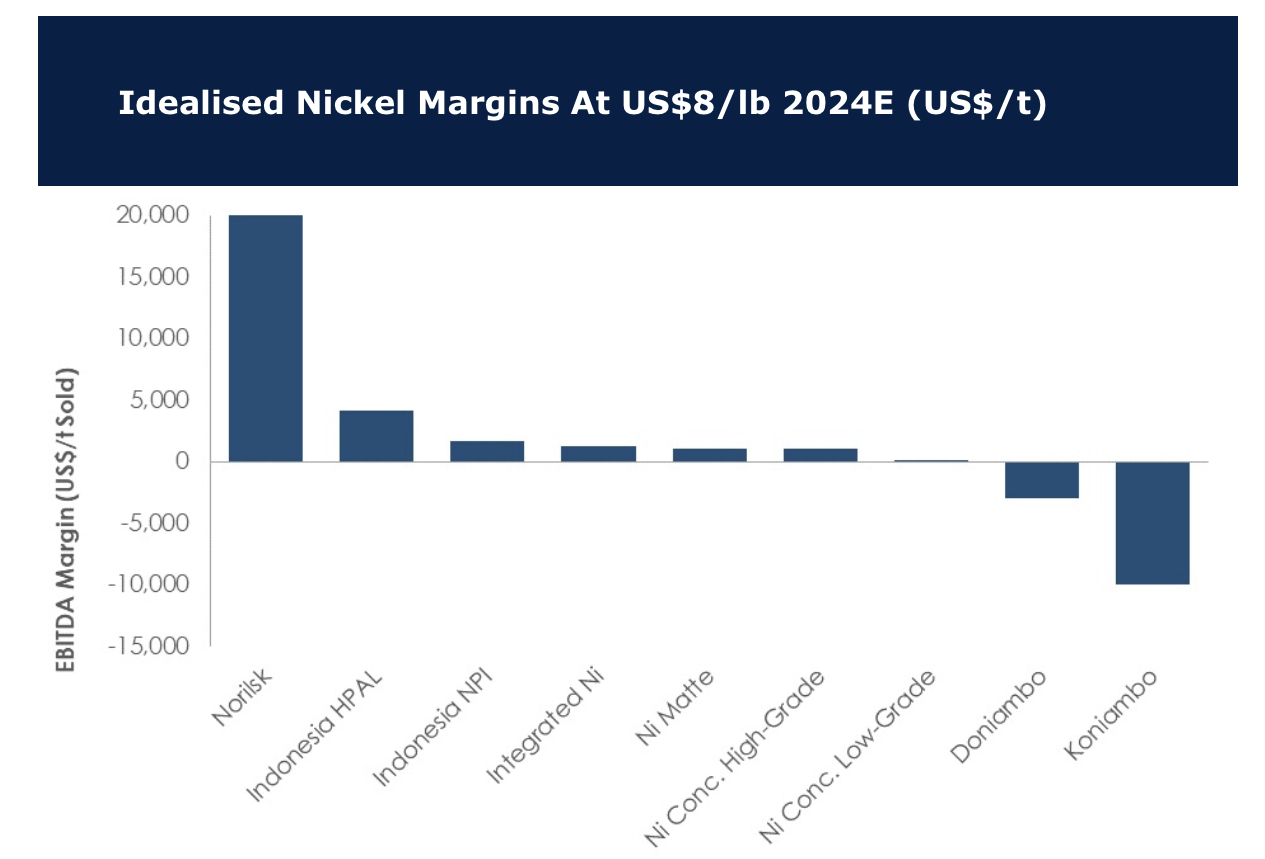

Wrecking ball demolishing the house of nickel

A year ago, nickel stood at US$13.00/lb, now it stands at ~US$7.30/lb. David Radclyffe turned bearish in July 2023 – since then producers have been hit hard, with projects across the board facing closure or review. The chart shows some idealised EBITDA margins for 2024; even at US$8.00/lb, some operations are already under water. With lower prices of US$7.50/lb or US$7.00/lb, only a few would not be in the red, including Norilsk, the Indonesian HPAL plants and some other Indonesian plants with cheap power. With so much pain in the industry, investors will no doubt be asking whether it’s a good time to start buying at the bottom? Before rushing in, remember Indonesia production is still ramping up and not enough production is being taken off-line. The wrecking ball will continue to swing for some time more and do further damage to the house of nickel.

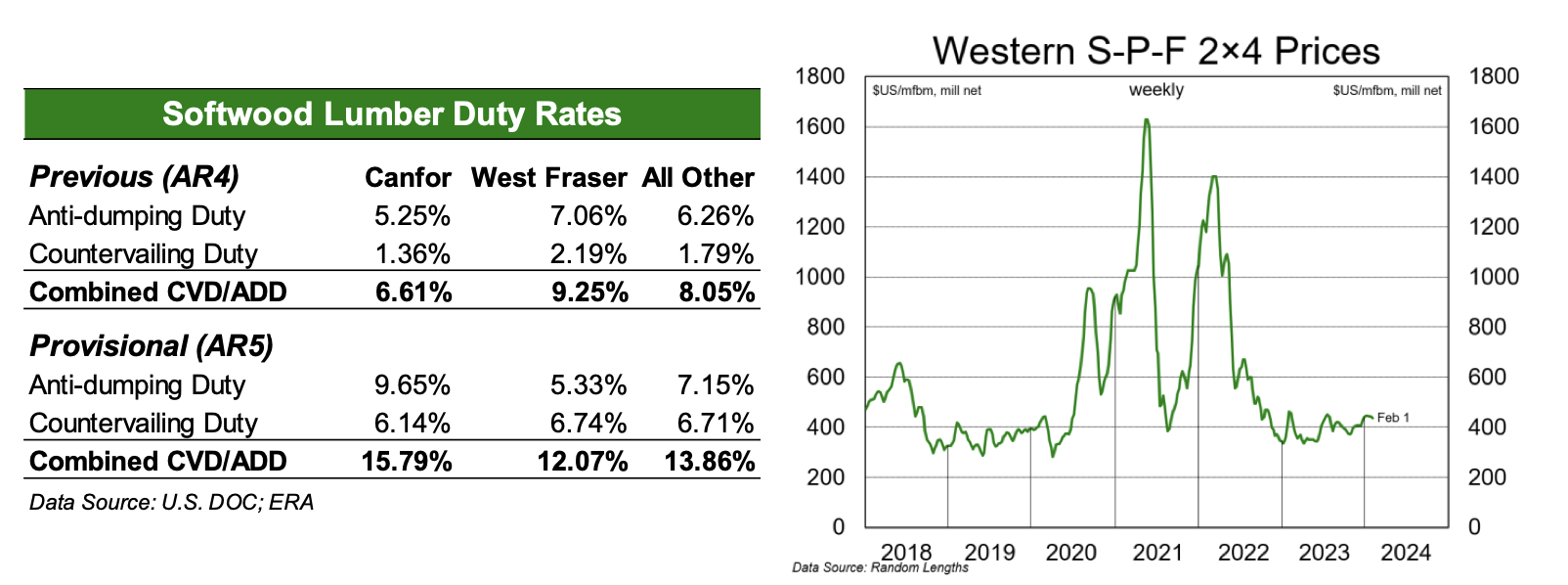

Softwood lumber duties set to move higher this summer

Preliminary results of the US Department of Commerce’s fifth administrative review into the 2022 North American lumber market sees an increase in combined duty rates, pointing to the potential for significant rate increases for next year’s review. Looking to 2023, S-P-F 2x4 prices averaged just $391 and spent most of the year near, or below, cash-cost levels; the ERA team expect that overall duties could increase sharply for the next review. So, who wins? US-based lumber mills (and perhaps Europeans exporting to the US) are the only winners as onerous softwood lumber duties increase Canadian producers’ costs. The release of the preliminary duties does not change ERA’s view on lumber equities, who sees upside from current levels for all lumber names given expectations for a sustained recovery in US housing. Interfor remains their top pick (target price $28), with West Fraser (TP: $116) and Canfor (TP $25) also seeing upside.