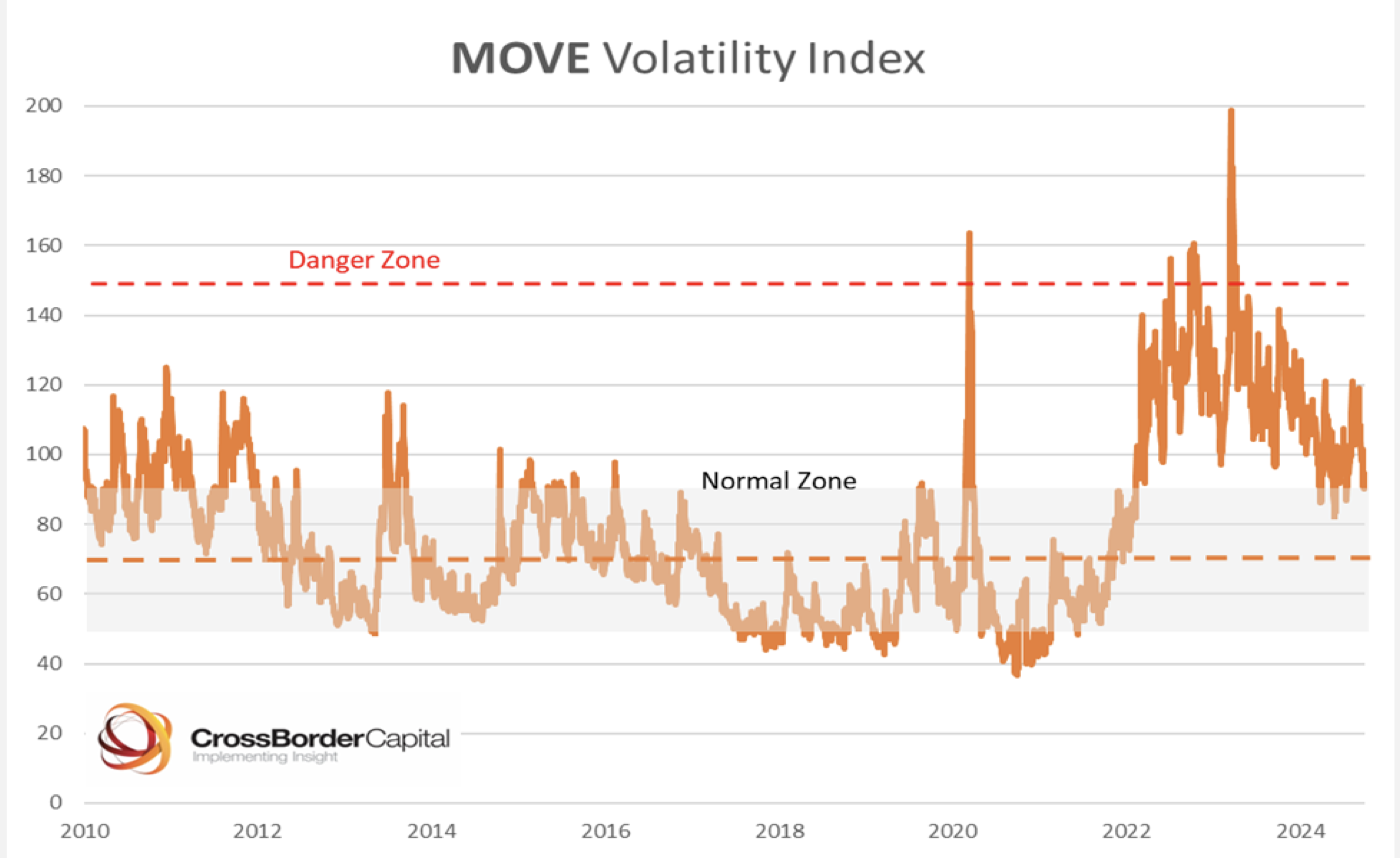

The hidden driver of global liquidity

Michael Howell’s latest report examines another important source of Global Liquidity, where an increasing multiplier pushes up an expanding collateral pool. He argues that the size of this multiplier is closely tied to falling bond market volatility. Thus, more Global Liquidity drives down the MOVE index of bond volatility, which in turn generates more Global Liquidity in a self-reinforcing loop. Maybe the MOVE index is more important to investors in risk assets than the more popular VIX index?

UK: A rudderless government

To burn all of your political capital within two months of winning the largest majority since Blair’s 1997 victory requires special talent, but Starmer’s government appears to have done it. James Aitken comments that, as a result, hopes for some sort of post-election, end-of-shambolic-Tories re-rating of sterling assets have been dashed. In terms of what this failure means for markets, James tells investors to consider the confusion over the coming UK budget: there have been an equal number of recent briefings on cutting investment versus changing the UK’s fiscal rules. The dysfunction has a whiff of Truss to it. James doesn’t see LDI 2.0 as pending and sees little risk of that, but there’s still a reason why gilts have underperformed since the election. The renewed risk premium on sterling assets is justified; and Bailey’s interview should continue to undermine sterling. Avoid.

Europe: Budget crunch in Berlin and Paris

In France as well as Germany, upcoming budget negotiations could fracture fragile governments. France’s sovereign risk premium could rise further if Marine Le Pen, the leader of the far-right Rassemblement National (RN), decides to censure Prime Minister Michel Barnier in December. In Berlin, Niall Ferguson expects the Free Democrats (FDP) to exit the three-way coalition of Chancellor Olaf Scholz over budget negotiations this autumn. German snap elections in February or March 2025 would be market-positive. The center-right Christian Democrats (CDU) would most likely emerge victorious and open the door to a slight softening of the debt brake to allow for higher defence spending. In France, however, the risks are to the downside as Barnier braces himself for an exceptionally short term as president.

Austria: Kickl’s sweet & sour victory

The far-right FPÖ won the Austrian elections with a solid 28.8%, even more than the polls predicted. In coalition talks, the ÖVP will be the kingmaker: they can choose between a coalition with the far-right or the centre-left. Wolfgang Münchau discusses two likely coalition options: one with the FPÖ, with a prime minister other than Kickl, and a classic grand coalition with the SPÖ and perhaps the Neos. There is also an option of a minority government with a confidence-and-supply agreement in the assembly. For the FPÖ and Kickl, the crucial question could thus turn into a choice between power and principle. If they insist on their Fortress Austria programme with its radical proposals and Kickl as the next prime minister, they won’t get into government. If they open up to compromise, they may lose votes. Power comes with strings attached. The far-right is no exception to this rule.

US: Accept lower rate expectations “promise” at your own risk

A record rise in lower rate expectations has created a burst of euphoria for U.S. households’ short-run economic outlook. However, Danielle DiMartino Booth points out that when a critical mass has formed for future rate cuts, it has historically heralded higher equity volatility, higher unemployment and excess supply conditions, not the other way around. In the University of Michigan’s September data, 55% of consumers expected interest rates to fall in the coming year, a record in data back to 1960, with higher tallies for upper-income and degree holders; notably, five other months have had prints north of 50%, four of which occurred in recession. Prior upswings in UMich lower rate expectations have presaged increases in the VIX, something which has yet to happen in the current cycle; similarly, lower rate expectations cleared 40% in the last three downturns before the unemployment rate began to rise sharply.

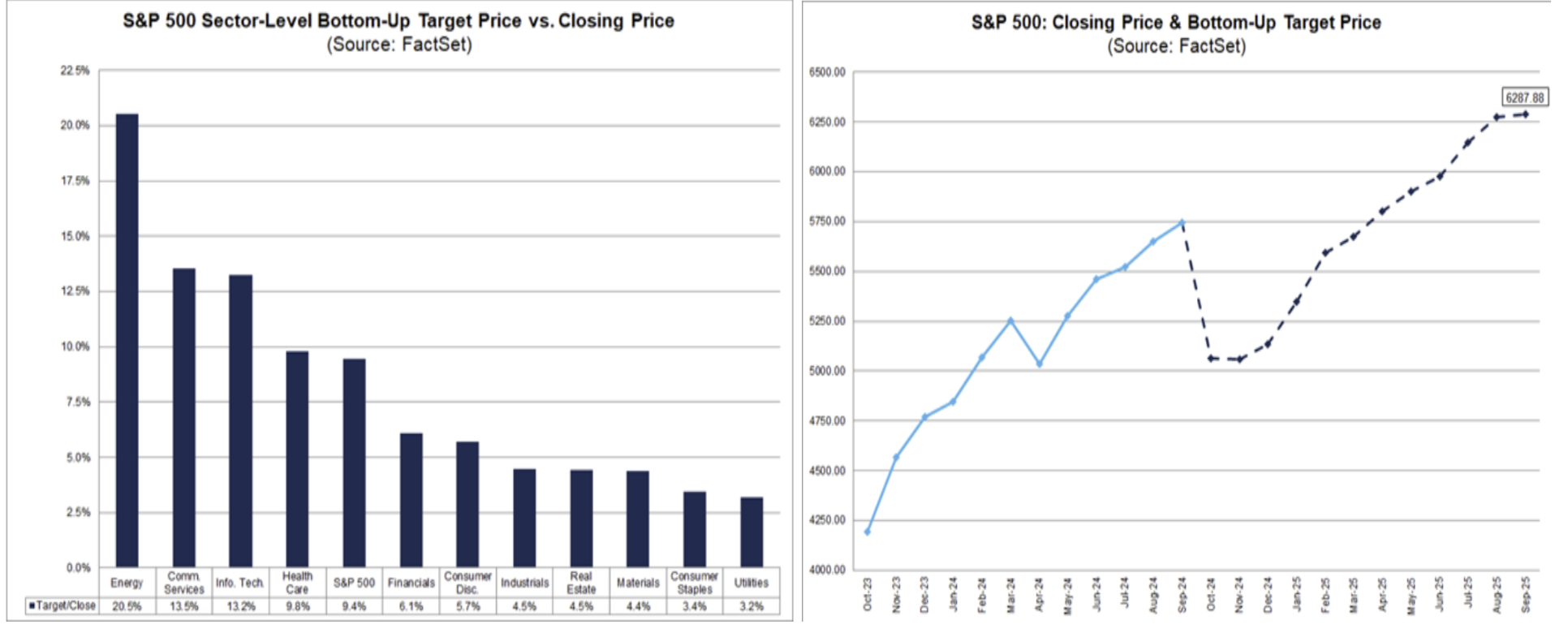

US: Bullish at the wrong time?

Craig Ferguson’s charts highlight the extent of analyst earnings optimism. Chart 1 indicates that analysts expect a 9.4% rise in S&P EPS in the next 12mths, with every sector contributing but energy sector EPS leading the charge rising by over 20%. Is it really possible to see the entire US energy sector record a 20% profit increase in the next 12mths? Global growth has not stopped slowing and downside will only intensify. Furthermore, after holding a 5000 average price target for October 2024, analysts have now jumped well ahead of the S&P’s current level to hold an October 2025 6287 Index target (chart 2). Arguably, right at the wrong time as global growth downside risks accelerate, analysts have increased their bullishness on the S&P to well above current levels. Are they going all in on the soft landing? It certainly looks like it, probably at or near the high.