Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

German FTTH deep-dive

While German broadband volume growth is slowing, New Street argues this is outweighed by a more rational market structure taking shape. Fibre overbuild looks set to remain far lower than in most other markets, supporting sustainable pricing and derisking the payback on high levels of FTTH capex per premise. Their report highlights the growing number of wholesale deals emerging; how the MDU market structure is likely to play out given the new draft law amendment; and evolving thoughts on the SDU fibre overbuilder market where they have more visibility on the longer-term wholesale dynamics. New Street also examines the implications for key players including Deutsche Telekom, Tele Columbus and Deutsche Glasfaser.

Consumer stocks poised for a recovery

AIR expects a wave of upward revisions from European corporations in the coming months as tariff clouds thin, China stabilises, infrastructure spend ramps up and European rates remain low. The missing piece is consumer confidence, which should rebound quickly if geopolitical tensions ease. Consumer names like Inditex, Stellantis, LVMH, Diageo, Kering, Adidas, Nestle and Unilever look compelling after steep share price declines, with valuations back to decade-lows. Many of these firms are pursuing clear turnaround strategies focused on FCF generation, deep efficiency gains (utilising AI) and renewed focus on core businesses - supported by a trend toward insider CEO appointments, after a decade of appointing outsiders.

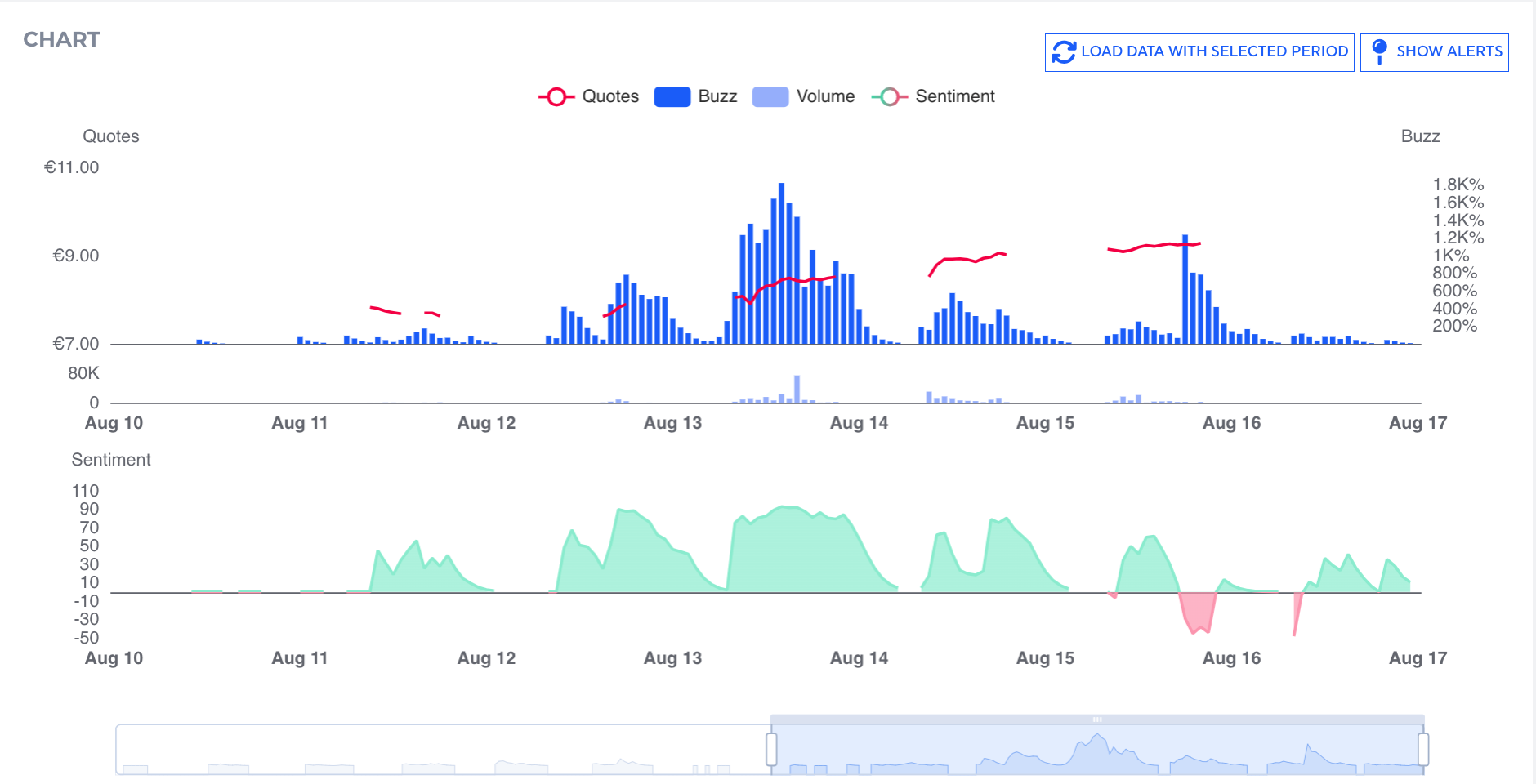

Stockpulse, whose platform provides real-time insights into social media sentiment, highlights a wave of positive attention around TUI. This was particularly apparent on 12th Aug, when the company reported a buzz score of 443% and a sentiment score of 86. This surge in communication and positive mood could be attributed to the company's recent earnings guidance update. Given the significant increase in market sentiment and buzz ahead of the earnings announcement, along with the positive stock price movement and exceeded earnings expectations, TUI's short-term outlook appears bullish. However, the market will need to assess whether this momentum can be sustained in the coming days and weeks.

SBM Offshore (SBMO NA) Netherlands

SBMO delivered another impressive performance in H1 and raised FY25 guidance. The Fast4Ward model is proving highly effective: in the past 7 months, 3 FPSOs with a combined 650kbpd capacity have achieved first oil, with unprecedented time-to-market that sets SBMO apart. While net debt of $5.6bn is still a concern for some investors and came in above consensus, it largely reflects new FPSO construction financing and the IDEA! expects deleveraging to progress as planned. This underpins its $1.7bn dividend / buyback commitment through 2030, with further upside from new orders and two unallocated hulls. Given SBMO’s continued strong performance, the IDEA! reiterates their positive stance.

Fraport (FRA GR) Germany

The shares have risen ~30% YTD (+75% 1Y), reaching Insight’s €75 SOTP-based TP. While recent tariff increases and the successful execution of a major capex programme have supported sentiment, the stock now trades at 8.2x 2026E EV/EBITDA (vs. 7.6x LT avg.) and looks overvalued vs. peers. Structural constraints persist, with Frankfurt’s majority state ownership, unionised workforce and insourced ground handling keeping EBITDA margins low. Aviation returns are weak, with NOPAT/RAB averaging just 3.2% in 2010-19 and only 5.4% by 2040E, still 120bps below Insight’s 6.6% WACC. Tariffs are expected to average just +2.0% p.a. through 2050E, despite high Aviation capex (€390m p.a.). With DPS resuming at only €1.0 in 2025E (1.3% yield), Insight has a Sell rating on the stock, preferring ADP (+70% upside), Aena (+55%) and FH Zurich (+55%).

North America

High-conviction short ideas

Dick’s Sporting Goods (DKS) - the Foot Locker acquisition will go down as one of the most value-destructive deals in retail history. The first time DKS misses a quarter because of perennial weakness at FL, this newco will trade at 3-4x EBITDA.

Best Buy (BBY) - 100% of EBIT comes from extended warranties, credit and membership - all of which are facing cyclical and secular pressure. Tariffs could take margins to zero, spurring a massive round of store closures.

Lam Research (LRCX) - the most complacent name in semicaps with 2026 WFE expectations set too high especially in DRAM. P/E now 4.5x turns above 3-yr average despite little growth in 2026. Domestic competition in China intensifying longer-term.

AI driven 10Q / 10K filings analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) Advanced Micro Devices - struck previous wording around the need to discount products, suggesting more confidence in pricing power. 2) Bright Horizons Family Solutions - no longer anticipating expanding operating cash flows. 3) GoDaddy - takeover target? Plus, further colour on international expansion plans. 4) Gilead Sciences - more competitive market for Bulevirtide. 5) Installed Building Products - new change in control agreement prompted by external takeover interest? 6) New York Times - increasing concerns re. competitors gaining market share at its expense.

Assessing the risk of a crash in the Canadian housing market

Veritas’ latest Housing Riskometer update highlights continued stress in the Greater Toronto Area (GTA) and Greater Vancouver Area (GVA) housing markets. Current months-of-inventory levels suggest detached and condo prices in both regions could fall ~10% Y/Y, or at least another 5% from Jun 25 levels. While prices have declined in recent months, a meaningful correction has yet to occur. To contextualise risks, Veritas reviews prior housing busts - GVA in 1981 and GTA in 1989 - where prices dropped more than 25% peak-to-trough, to understand the current resilience better. Specifically, they examine the labour market conditions during the two historical market downturns.

How to play America’s atomic acceleration

The US nuclear sector is at an inflection point. The Department of Energy has launched a program to fast-track the approval of 11 new reactor designs, with first units targeted for approval by 2026, as part of broader plans to quadruple capacity by 2050. Momentum is spilling into capital markets, with developers seeking more than $500m via SPACs and IPO pipelines building. A major step last week saw ASP Isotopes and subsidiary QLE sign an MOU with Fermi America to develop new enrichment capacity at the planned 11 GW HyperGrid campus in Texas. Yet while demand is surging, uranium supply growth remains constrained - leaving the fuel chain as the sector’s hard limit, and where high-conviction opportunities are emerging.

The Genius Act has changed America’s relationship with crypto, making it the most attractive country in the world for stablecoins. Abacus’ latest report notes that while the pace of adoption is still unclear, long-term disruption of financial incumbents appears inevitable. CRCL’s model is attractive if USDC can scale, though Abacus estimates ~10x growth is needed to deliver a reasonable IRR - a challenging hurdle. Blockchains are expected to replace legacy infrastructure, with SWIFT the first casualty. Visa and Mastercard face limited near-term risk, but crypto is the primary long-term threat to their duopoly. Stablecoins have the potential to reach >$2trn m/cap in the next few years vs. $260bn today. Abacus sees CRCL as a compelling risk/reward play, with upside potential of 195% outweighing downside risk of 50%.

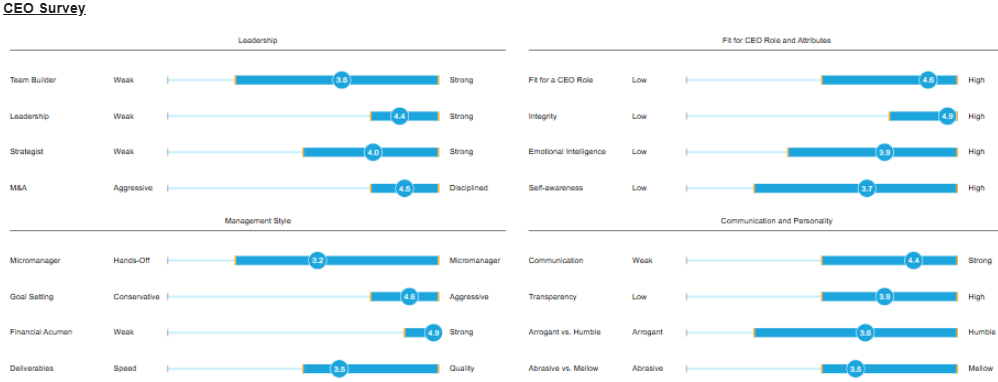

Paragon interviewed 7 former senior executives at ATS who worked with BAX's new CEO, Andrew Hider, for more than 36 years combined. Feedback was universally positive. Hider is a disciplined, process-driven leader who blends Danaher-style operational rigour with strong communication and an ability to scale businesses via organic growth and M&A. At ATS, he drove cultural transformation via the ATS Business Model, delivering margin expansion and shareholder returns, though his intense stretch targets and competitive nature created a high-pressure environment that could limit collaboration and agility. His success at BAX will hinge on whether he can balance his relentless operational focus with greater strategic flexibility and adaptability to the slower-moving, more regulated dynamics of the pharmaceutical industry.

KCR slashes tech exposure

KCR’s evidence-based stock selection process has swung from unambiguously bullish tech to record levels of bearishness. Their report (click here to access) shows long exposure in the technology sector across all of KCR's Large Cap model portfolios was >50% between 2014-2019 but has since collapsed to a far more modest 32%. Contrarily, 59% of their short model portfolios are now made up of tech stocks. The impact is even more dramatic in KCR's Small & Mid Cap portfolios - only 5% of their long book is in tech, while 58% of their SMID short model portfolios are IT names. KCR’s report also includes their Top 10 Ranked Long and Bottom 10 Ranked Short ideas.

While CDNS appears to be handily beating both sales and earnings estimates, BTN’s analysis shows it is being driven by increasingly aggressive revenue recognition. Recurring revenue growth slowed to 6.5% Y/Y in 2Q25 (vs. mid-teens previously), while upfront revenue has surged >100% Y/Y in the last 3 quarters. BTN cautions comps will toughen significantly in Q4 and even modest declines in upfront revenue would see CDNS lose its EPS beats. Unbilled receivables have doubled in the last 8 quarters and long-term receivables doubled in Q2. Deferred revenue days of sales has also dropped Y/Y for 4 consecutive quarters. Additional red flags include lower bad-debt reserves and an EPS boost from higher stock comp. At >50x forward adjusted EPS, there is little margin for error before the stock price could face pressure.

Boyar argues investor fears around the stock are overblown. While the loss of a respected CEO, macro uncertainty and competitive pressures in the Merchant business have weighed on sentiment, Boyar sees the past year’s share price swing as a textbook case of exuberance turning into excessive pessimism. The company retains leading market positions, a strong operating track record and a mid-teens earnings growth outlook, yet trades at just ~12x forward P/E - its cheapest valuation in over a decade. Wall Street’s intense focus on Clover's short-term performance overlooks the company's host of other valuable business lines, which together contribute ~83% of revenue. Applying a 19x multiple to 2027E EPS of $13.33, Boyar values the stock at $253, implying ~80% upside.

Richard Windsor argues SoftBank’s $2bn investment in INTC, alongside a potential 10% US government stake, may keep the company alive but does little to resolve its strategic paralysis. INTC faces a stark choice: either invest heavily to catch up with TSMC or break up the business - yet under new CEO Mr. Tan, neither path is clear. The board abandoned Pat Gelsinger’s catch-up strategy due to mounting costs, leaving INTC exposed to further share losses in PCs (to AMD and Qualcomm) and in data centres (to Nvidia and AMD). Richard warns that without decisive strategy, customer confidence will erode, competitors will gain share with ease and capital injections alone cannot avert decline. He sees no attractive entry point in INTC shares.

According to Systems Integrators who work with SNOW, they saw strong 2Q25 momentum driven by rapid partner expansion and AI innovation. The company now has over 10,000 partners worldwide reflecting heavy investment in programs that broaden global reach. New AI-driven tools, including Cortex AI, Iceberg tables, and adaptive compute capabilities, enable enterprises to interact with data in natural language and automate pipelines, and are driving revenue. Strategic acquisitions, such as Crunchy Data, further enhance Postgres capabilities and enterprise appeal. To sustain momentum, SNOW is leaning heavily on system integrators, hyperscalers and resellers to drive adoption of next-gen AI offerings.

Japan

Japan’s space capabilities are rapidly expanding

Investor enthusiasm in the country’s space sector is accelerating, underpinned by several IPOs expected in the next couple of years. At SPEXA 2025, this enthusiasm was on full display, led by Toyota’s backing of Interstellar Technologies, which plans a listing and aims to capture the growing low-Earth-orbit launch market. Japan is also positioning itself at the forefront of space-debris removal working with Astroscale and JSAT, targeting an international regulatory framework by 2026. Meanwhile, government ambitions include doubling the space industry to ¥8trn, achieving 30 annual rocket launches by the early 2030s and deepening NASA collaboration, including a Toyota-built lunar rover. Neil Newman sees Japan’s space industry as an increasingly attractive investment theme.

Emerging Markets

China's biotech rally has only just begun

Horizon Insights argues investors continue to underestimate the sector’s progress as global pharma validation accelerates. Over the past year, BMS, Merck and others have paid billions in upfront licensing fees for Chinese-developed assets. China now leads globally in ADCs and bispecifics, representing 40-50% of pipelines. YTD, MNC-led upfront BD payments total $9.1bn, on pace to double last year’s figure. Horizon Insights sees a structural repricing underway, driven by patent cliffs in big pharma, globally competitive pipelines, deep policy support and rising clinical credibility. If 2018 marked the breakout for China EVs, 2025 could do the same for innovative drugs. Top picks include Innovent Bio, Keymed Biosciences and Akeso.

Lucror maintains a “Buy” on Greentown China’s 8.45% ’28s (102.8/7.1%/2.2Y), citing attractive carry and manageable credit risks. The 1H25 profit warning reflects delivery timing and non-cash impairments rather than underlying liquidity stress. Credit quality is supported by a strengthened capital structure, with short-term debt reduced to <20% of total debt and Cash/ST Debt at a record 2.5x. Access to financing remains solid, backed by parent China Communications Construction Group, demonstrated by successful bond issuances and continued land-banking activities in Tier 1-2 cities. Despite earnings volatility from the absence of recurring income and sector ASP pressure, Lucror’s “Stable” credit bias reflects expectations of continued resilience and relative outperformance.

AceCamp analyses first half results for these two leading robotaxi companies, focusing on revenue structure, burn rate, strategic focus and commercialisation outlook. They believe WeRide's early-mover advantage in globalisation and Pony.ai's capability for technological mass production represent two divergent industry paths. In the short term, Pony.ai's diversified revenue structure offers greater resilience; in the long run, WeRide's high-growth overseas markets may unlock larger opportunities, though local operational costs remain a challenge.

Macro Research

Developed Markets

UK: Under the weather

Mark Bathgate’s exceptional level of dialogue and understanding of Westminster/Gilt markets has allowed him to accurately call changes over the past few tumultuous months. Mark warned clients through May and June that Labour MPs were unwilling to accept any curbs on welfare spending, and hence a much larger deficit, gilt funding needs and tax cuts would be the main political and market talking points for the second half of the year. He sees the upcoming Autumn budget being dominated by an internal debate within Labour over which taxes to hike, which will play out via media leaks until a last-minute resolution. There is little reason to expect a change from the story of excess inflation, overshoots in borrowing needs, higher taxes and weak household real income growth and spending. Hence, the market trend to higher long term gilt yields and underperformance of other DM sovereign bond markets is well founded, and investors should expect no reason for change.

ECB: Expect the circumspect

In line with Dimitris Valatsas’s expectations, the European consumer is showing signs of life: June retail sales came in at 3.1% y-o-y. But across the EU, growth remains slow and non-mortgage lending subdued. Demand for mortgages and consumer credit fell in Q2 and credit to EA companies stays very low. Spain remains Europe’s economic steamroller—2Q25 consumption grew by 3.5% y-o-y, while GFCF grew by 5.6% y-o-y. Dimitris views the trade truce with the US as a derisking factor—though he expects some of the deflationary effects of the global trade war to remain. Dimitris says the ECB has settled here; policymakers are too scared to get ahead of the economy, so he now expects them to hold for at least the next two meetings. 2Q26 forward rate expectations still seem too hawkish. The French and Spanish governments are increasingly fragile, though only the French situation presents a major threat to policy continuity.

USD: A race to the bottom?

According to Charles Hess, the US strategy is to lower the value of the dollar - without affecting its status as the world’s reserve currency - and encourage domestic manufacturing by increasing the price of imports and lowering the price of exports. Trade will shrink among some trading partners and increase between others (i.e., India and Russian oil), as they rearrange their economic relationships. As the US pulls away from the alliances and allies that have granted it primacy as a global superpower and as the provider of the world’s reserve currency, China is attempting to make available a substitute for the dollar-centred international economy via Beijing-centred international organizations and alliances. These Beijing-centred coalitions increasingly trade in their own currencies. Gold, silver and other hard assets will hold their value and increase in price as the dollar declines.

US: Bull in an American shop

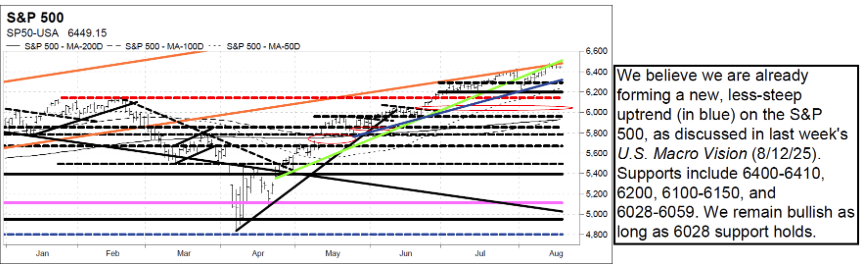

The Vermilion team have discussed since late-July how the S&P500 had not closed below its 20-day MA for three months, but even when it does, all they would expect is for a new, less-steep uptrend to form. Their prediction came true on August 1st, with the index returning to all-time highs after finally losing its 20-day MA. Therefore, the team remain both near- and intermediate-term bullish, and will maintain this view as long as market dynamics remain healthy and the SPX remains above 6028-6059. It’s also worth looking at Bitcoin mining names such as Hut 8, Iris Energy and TeraWulf – if such names continue leading, it suggests risk appetites remain strong and that the bull market is in full swing.

US dollar index shifts bearish and commodities diverge

Keith McCullough observed that the US Dollar Index had shifted from Neutral TRADE to Bearish TRADE, while remaining Bearish TREND — confirming the broader dollar devaluation move as both CPI and PPI reinforced Hedgeye’s call for sustained inflation reacceleration into November. This setup is a tailwind for his global equity longs (KBA, EWG, EWK) and other non-dollar exposures, with the immediate-term Hedgeye Risk Range™ for USD at 97.50–99.00. Keith keeps pressing into assets that benefit from dollar weakness and asset inflation. Meanwhile, commodities diverged last week— Oil broke to Bearish TREND while Gold and Silver stayed Bullish TREND, both setting up fresh buy signals at the low end of their Risk Ranges. Bitcoin hit new ATHs and Ethereum (ETHA ETF) led all ETFs in performance, digesting gains without breaking trend. Keith will keep pressing longs in precious metals and crypto, using pullbacks toward LRRs (low end of Risk Range) to add exposure.

US: Any easing rally may be short lived

The ongoing wave of T bill issuance looks to be crowding out private sector borrowers in the US credit markets. It’s early days, but Andrew Hunt points out that the data seems to be leaning that way. The US economy is slowing, with little going on outside of the AI boom, and nominal growth currently seems to have a high price / low real growth composition. The crowding out phenomenon will bring about a bear steepening effect in the near term, supporting the USD, although Andrew expects the Fed to respond aggressively. He sees markets being strong and USD weak in 2025/Q4 as a Pavlovian response to rate cuts, and that the new easing will cast the economy’s inflation expectations adrift, leading to nominal growth accelerating for the wrong reasons (i.e. prices not volumes). At some point in the coming year, markets will have to worry about an FOMC tightening and/or entrenched inflation.

Australia: The consumer shines bright

Craig Ferguson says that better confidence in Australia should mean relatively higher AU yields and Aud FX rates, and even stronger AU corporate earnings outlooks. Craig’s chart of the day focuses on the relative outperformance of the AU macro economy, a theme he first noted around 4-8 weeks ago and one which has firmed up with the data inflow over that period. On the one hand, markets still expect a further 2 rate cuts from the RBA in this cycle, but on the other Craig has been arguing that the rebound in AU PMI, NAB, Ai Group, jobs, building approval and even the latest consumer confidence survey all suggest that the country’s economy is in a re-acceleration phase as the RBA’s slow motion 3 rate cut cycle so far starts to have an impact.

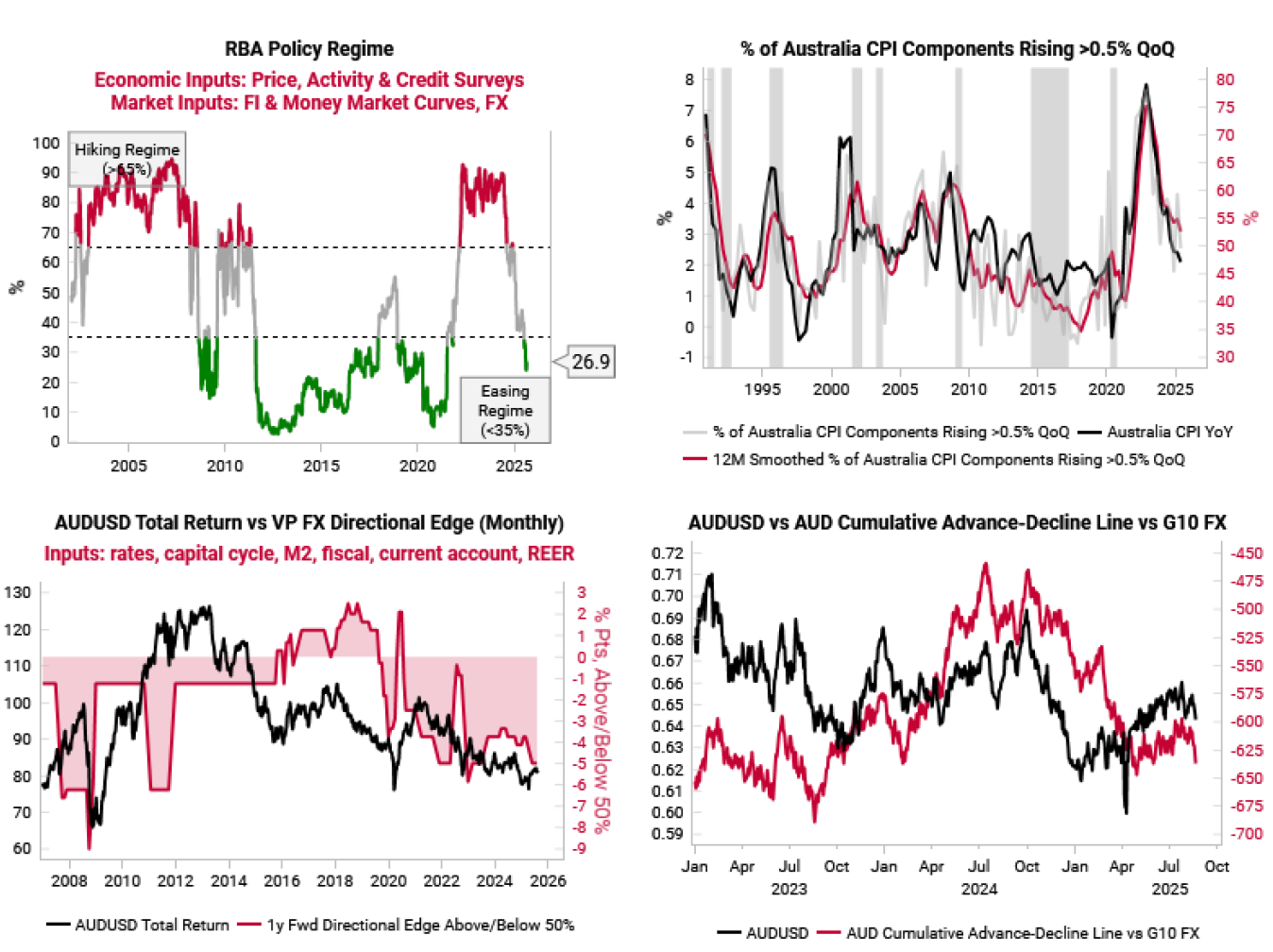

Australia: Feeling eas-y

Variant Perception’s Policy Regime model shows the RBA as the latest central bank to be in an easing regime (top left chart). This is consistent with signs that inflation will fall further towards the bottom of the RBA’s 2-3% CPI target range. The team’s inflation LEI is also edging lower, and inflation breadth continues to decline (top right). Meanwhile, their fundamentals-based FX Edge model fell further last month, pointing to negative 1-year forward returns for AUD/USD (bottom right). Tactical models also point to short-term pressure for AUD, and AUD’s breath relative to G10 currencies has been recently weak (bottom right). The team add short AUD exposure to their short EUR exposure to play a tactical rebound in the USD.

Emerging Markets

Emerging market equities are picking up steam

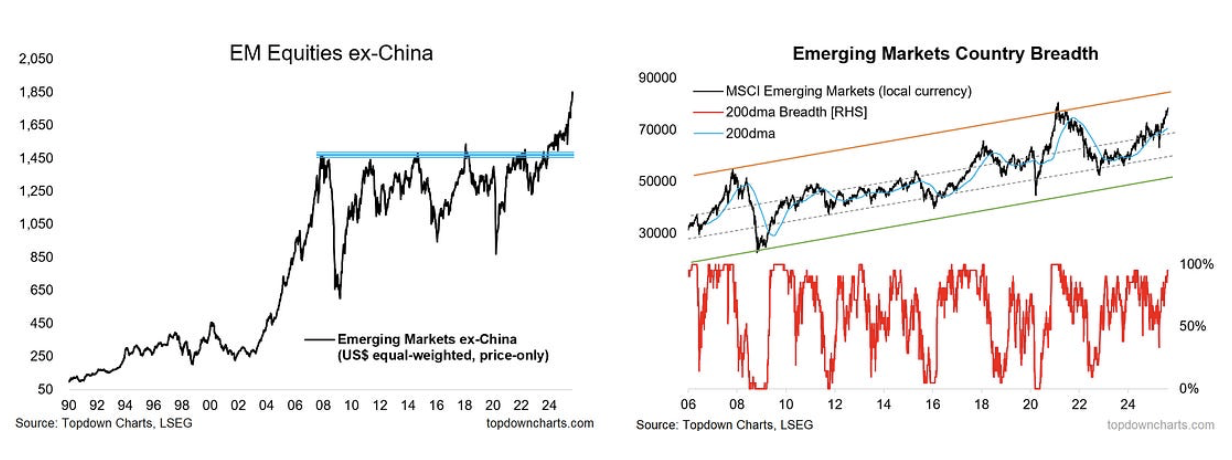

Callum Thomas maintains a bullish view of emerging market equities, noting that equities are accelerating post-breakout. He sees this in both the local currency and US$ indexes. Moreover, market breadth is expanding, indicating broadening strength. Chinese stocks in particular are also finally seeing significant improvement. The picture is very bullish. His charts illustrate how EM equities are picking up steam; the US$ equal-weighted EM ex-China index is accelerating following its breakout and initial consolidation, while the MSCI EM local currency index is also accelerating following the earlier failed break below its 200-day moving average and is doing so with expanding market breadth. He also notes very bullish price action in China, with A-shares breaking out vs the key overhead support level after a year-long period of consolidation. This is a clear sign of bullish strength and looks more like the booming early-2000's than the stagnant 2010's.

Bolivia’s long goodbye to Evo

After two decades of leftist rule, Bolivians rejected the socialist candidate backed by former president Evo Morales’ party. The two remaining candidates are both eager to introduce fiscal discipline and pro-market policies. Markets have rallied since April on expectations of this pro-market shift, but Niall Ferguson points out that the market is shallow. The country’s weak macroeconomic fundamentals call for painful austerity and structural reforms. Should the election winner quickly commit to fiscal austerity, abandon the peg, and implement reforms, Bolivian assets could see upside. However, investors should expect things to get worse before they get better.

China: Tailwinds in equities

William Hess is fully aware that geopolitics may fill the policy void in China, but last week saw a continuation of positive signals behind equity markets. Most important are volume-based measures for the CSI300 that point to strengthening support – William notes that price-volume indicators are pointing to position accumulation rather than intraday trading. Other constructive factors are also worth noting, including falling risk-free and interbank rates, elevated systemic liquidity levels and regulatory mandates for onshore institutional investors to increase equity allocations (which was responded to positively). Another tailwind comes in the form of repatriation of Chinese institutional capital in the face of Trump risks in the US. Sure, the property sector is still in the tank, but this just encourages more asset rotation into equities. The direction of the tide is clear; it’s time to buy the CSI300.

China’s inflationary waves

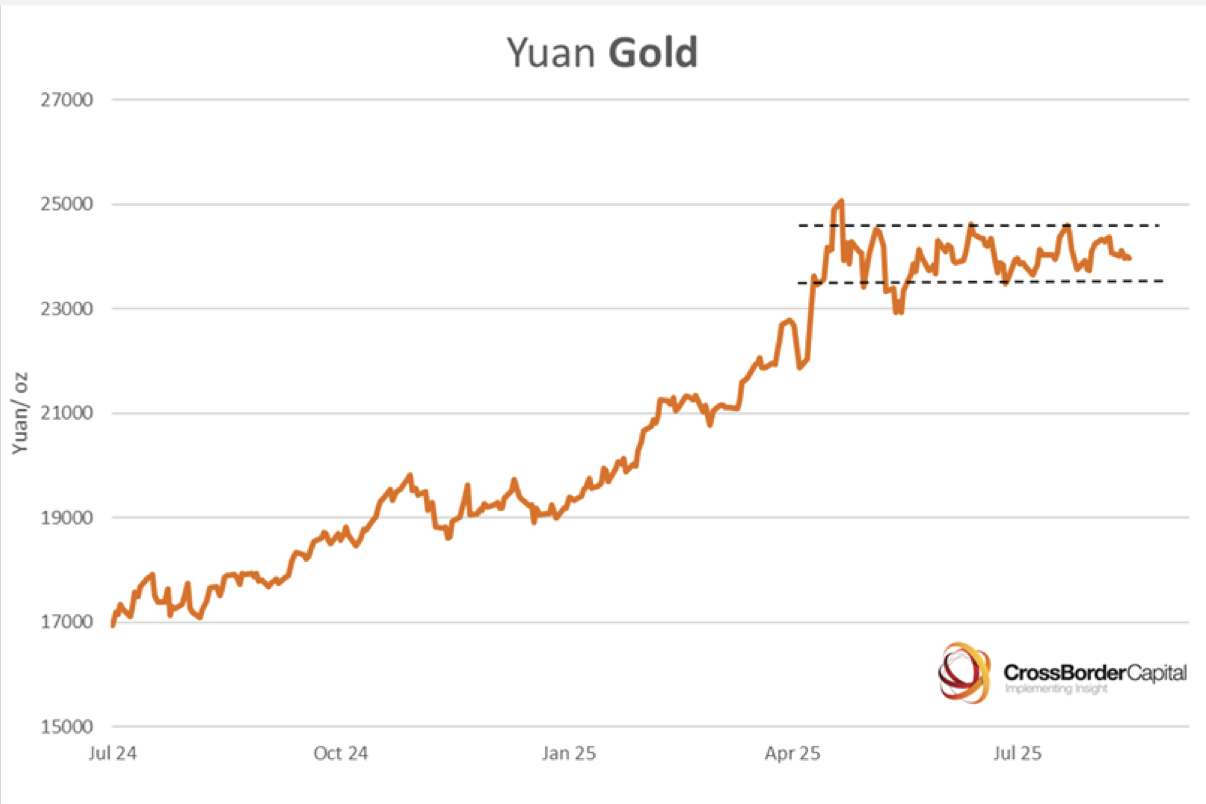

Michael Howell points out that Chinese deflation is a persistent issue driven by an excessive debt overhang. Debt deflation requires a domestic monetary solution. The PBoC must dramatically expand its balance sheet to drive an acceleration in liquidity growth sufficient to devalue the real burden of debt; Michael claims that to get back to former trends, liquidity would have to expand by some 50%! This escape from debt deflation does not necessarily require a weaker Yuan against the US dollar but instead will be signalled by stronger Yuan gold, which is now a crucial test for Chinese policymakers. The resulting monetary inflation, evident in rising asset prices and a recovery in commodity demand, is poised to become a significant inflationary force worldwide, transmitting higher prices to the rest of the world through surging gold and commodity markets. Expect a breakout in the Yuan gold price above RMB 24,000/oz.

Chile: Running on autopilot

Enrico Vicentini and Igal Magendzo note that the market has continued to display a rather anaemic dynamic, with only marginal movements. This may appear reasonable given the level of global uncertainty and the fact that Chile is near the neutral rate. Yet, with the Fed on the verge of resuming rate cuts, other central banks will be incentivised to adopt a more dovish stance and push rates down further. Enrico and Igal argue that the Central Bank is effectively on autopilot at around 4.5% (the upper bound of the neutral range). From here onwards, additional dovish signals will be required to give the Board the confidence to bring the policy rate closer to 4.0%. As for market opportunities, they continue to see value in holding a long position in the 9m9m BEI (or alternatively, in the UF forward Feb-27/May-26 spread), which has already moved up by 14bp since they initiated coverage.

Tanzania: Liabilities higher than Kilimanjaro

According to Mandy Ong, Tanzania's structural problems are rooted in its abysmally low export earnings capacity, but regional goods and services exports have boomed over the past 18 months. However, this is not a game changer for a country plagued by a sky-high stock of external liabilities and twin macro deficits. The jump in external earnings has helped reduce debt service ratios, but Tanzania still runs wide current deficits and remains heavily dependent on the IMF, China and other foreign creditors. It will take a few years of booming exports to meaningfully change the macro maths. On the bright side, the Tanzania shilling has been relatively stable and with oil prices low and the export outlook improving Mandy sees no immediate threat to the currency. Meanwhile, domestic demand has slowed on the back of government austerity measures and she sees no compelling reason to focus on this small equity space.

ESG

Hot picks for the heat economy

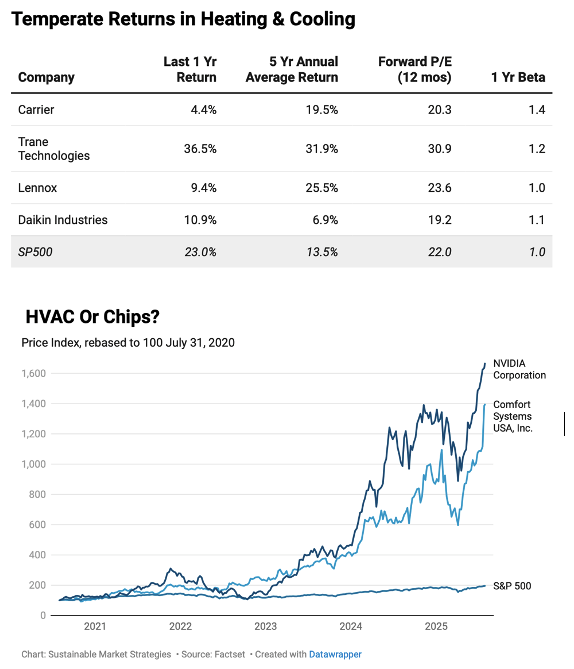

Heat pumps are the go-to solution for building space cooling (and heating), and the Sustainable Market Strategies team expect the bull market in HVAC companies to continue even in the face of subsidy removals. The IEA expects 1.5bn more air conditioners in operation in 2025 than today, driving the need for energy efficient solutions. Heat pump improvements aren’t just good for reducing emissions, they’ve been good for portfolio returns; just take a look at Comfort Systems, which some could mistake for super star Nvidia (see chart). Sure, this performance does stand out among HVAC players, but others have also done well (see table). The tech will become only more important in use cases like food refrigeration and data centre cooling, so demand will see sufficient growth. When it comes to cooling solutions for the data centre boom, look to US companies to fill this gap.

Commodities

Speech is silver, silence is gold

David Woo believes that Trump has reneged on a deal to take a hard line on Putin in exchange for a more favourable tariff arrangement. David expects a showdown, with geopolitical risk set to ramp up. After CPI, the curve resumed its steeping trend, suggesting that gold may break higher from its range. The tight range for gold in April means that a large move in a short period of time may be possible; the only reason it stayed in range last week was due to the decline in geopolitical risk premium. David bought the December gold future at 3382.40, and will take profit on a move to 3550 and stop out at 3300.

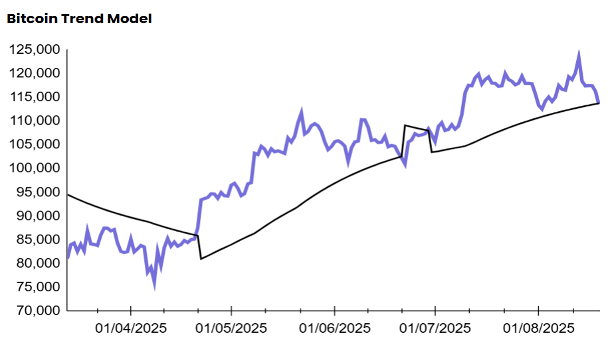

Crypto: Take it easy

While Markus Thielen had hoped Bitcoin might attempt a sustainable rally last week, he treated $117,000 as a clear stop-loss level for long positions. Since then, several key trend shifts have emerged—Bitcoin (BTC), Ripple (XRP), and Sui (SUI) have all turned lower and entered bearish trends. Markus notes that short signals in this bull market have been challenging, but the current environment calls for greater caution, especially in managing the more volatile parts of a portfolio. Bitcoin has already corrected swiftly from its recent all-time high, with the new stop-loss for the downtrend now set near $123,900—coincidentally close to that high—and ratcheting lower each day. Markus’s preference remains to align with the bullish trend when it reasserts itself or to buy at deeper pullbacks. Still, for now, he says a neutral stance and trimming portfolio volatility is the prudent approach.

Brother, may I have some oats?

Chris Roberts comments that looking at the quarterly chart for spot oats shows a 57-year up-channel, and this chart’s MACD gave a buy signal from below the Zero Line in May; since May 1985, 5 of the 6 prior signals like that have been followed by a strong cyclical advance. Recently, spot oats have been rangebound for 11-months, following a 64% fall in 2022-24, and Chris sees that an 11-month rectangle has formed following a double bottom in 2023-24 at the USc290.00 level (see chart). A breakout from the rectangle would signal a new cyclical advance. Go 25% long at market and 25% long at USc3.31. Chris’s recommended stop is a daily close below USc308.00.

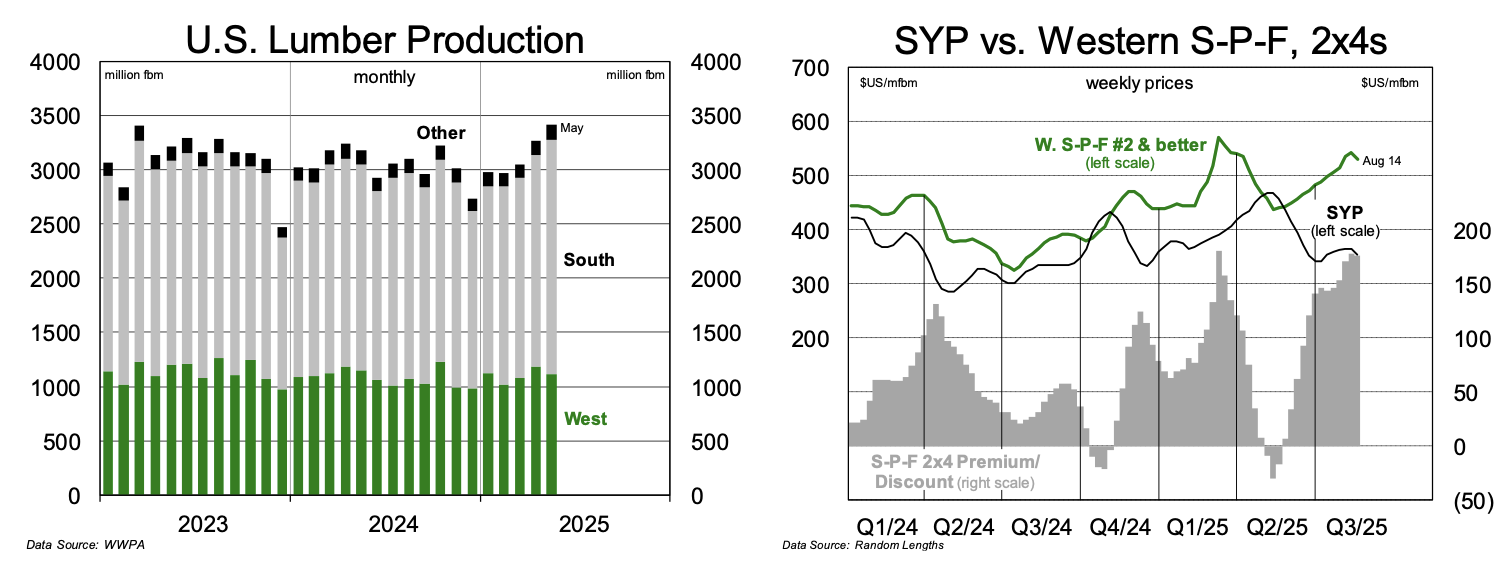

Lumber: Falling demand, rising production

Total US lumber production has risen steadily this year, reaching a higher level in May than any point in 2024 (left chart). All the production was in the South (US). The steady increase comes even as US single family housing starts declined 6% through May, with Southern starts down 10%. It is hard to say who wins from a weak US housing and lumber market, and with lumber demand expected to remain subdued until year-end and throughout 2026, SYP mill capacity reductions will be needed before a sustained lift in SYP prices occurs. Sawmills in the US West appear to be best positioned to benefit from declining Canadian S-P-F supply as lumber buyers appear to view species like Douglas Fir and Hem Fir as closer substitutes for S-P-F. The sustained price increase in lumber will happen, but the mill closures in South US and Canada will be painful. For now, investors should wait.