Europe

Consumer Discretionary

Forensic Alpha increases their risk rating on AUTO1 to 7/10 following the release of the company's H1 results, which revealed another jump up in DSO, driven by an increase in both their installment purchase programme and merchant financing programme. DSI also saw a large increase. The aggressive deployment of their balance sheet is causing cash flow to lag significantly behind earnings.

Consumer Discretionary

ResearchGreece is keen to see the contribution from the new IKEA stores in Patra and Crete; the roll-out of Foot Locker stores; and the recovery from the recent cyber-attack. In short, evidence that the business plan is working. Management guides for €600m in retail sales and €38m in cash EBITDA in 2025, vs Q1 sales of €118m and EBITDA loss of €1.1m. Upcoming Q2 results will be key in assessing if the implied 2025-2027 CAGR +12% sales and +24% EBITDA are on track. ResearchGreece rates Fourlis as OI (Own it).

Consumer Discretionary

Odigeo delivered a strong Q1 FY25/26, with year-on-year gains in revenue, earnings and profitability, though cash flow weakened on working-capital outflows and higher cash interest and taxes. Reported net leverage was broadly flat quarter-on-quarter and liquidity remains comfortable. The company reaffirmed full-year targets for adding 1 million Prime subscribers and cash EBITDA of €215–220 million, while trimming FCF (ex-non-Prime working capital) to €103–108 million. Lucror still expect a robust FY25/26 underpinned by sustained Prime subscriber growth, with profitability set to strengthen over the coming quarters as newer Prime cohorts enter their second year.

Industrials

Kloeckner looks to be turning a corner. The low-margin Distribution segment now accounts for less than 20% of sales with a 5% target, while North America—benefitting from US industrial reshoring and auto activity in Mexico—has been the main growth engine and now contributes about 60% of revenue. Price normalisation in Q3 is pressuring EBITDA margins near term, but Germany is poised to become the key driver as new defence and infrastructure plans gather momentum, even if current operations are loss-making at roughly 60% capacity utilisation. US customers have shifted to a wait-and-see stance amid policy uncertainty, yet the stock’s valuation—around 0.36x price/book—remains strikingly cheap, suggesting the worst may be largely behind the company.

Industrials

Sofia Frandberg (Non-Executive since Apr 23) bought 4,000 shares at SEK 474.96, spending €173,000 and doubling her holdings. This is her first purchase since joining the board in Dec 23. Smart Insider ranked this stock +N on Sep 1st based on a €110,000 purchase from Bo Selling (Chairman, joined 2020) at SEK 481. It was a 50% increase in his holdings and his second purchase. His first was in Aug 23 at SEK 448, was part of a +N rank at that time, and proved timely. Now with two interesting purchases, Smart Insider are upgrading the stock further, from +N to +1 (highest rating).

North America

How do you Identify Compounders?

In a market where investors increasingly seek long-term “compounders” to ride out volatility, Trivariate’s research shows that out of the four factors tested (revenue, gross margin, net margin, and price momentum), consistent gross margin expansion has been the most reliable signal of future stock outperformance. This is a rare but powerful cohort with only 39 companies having expanded gross margins for 12 consecutive quarters; 22 are expected to continue doing so next quarter. Actionable names include AMZN, T, ETN, APH, and TDG, among others.

Consumer Discretionary

Amazon ran steep tool discounts over the holiday, highlighting Lowe’s pricing disadvantage. Across 25 items from brands like Bosch and Dewalt, Lowe’s averaged 27.5% higher prices; 15 items were cheaper on Amazon with average discounts of 34.6%, while only one was cheaper at Lowe’s. This follows R5's year-long observation that Lowe’s prices exceed Walmart’s on common goods. The wide gap raises concerns about Lowe’s gross margins and potential sales/earnings headwinds, even if housing improves. Meanwhile, Amazon’s aggressive pricing supports volume growth and advertising profits—a positive for AMZN but a structural challenge for broader retail.

Healthcare

A solvency risk, BKD operates senior and dementia-care communities. Sales grew 4.6% last quarter after stagnation, with modest margin gains and controlled SG&A. However, leverage is extreme at 11.8x EBITDA, with heavy maturities in 2026 and beyond. Free cash flow has flattened, estimates continue to weaken, and sales are forecast to slow (+2.7% in 2025, -2.4% in 2026). Despite missing recent earnings and facing refinancing risks, shares are up 53% YTD, trading at 15.7x 2025 EBITDA. Investors face a mix of modest operational improvement but significant balance sheet strain and declining growth expectations.

Healthcare

Dexcom, with ~30% global share, is a leader in the fast-growing continuous glucose monitoring (CGM) market, operating in a near-duopoly with Abbott. Renowned among specialists and type 1 diabetes patients, Dexcom benefits from expanding adoption and broader reimbursement, including recent U.S. approval for basal insulin users and high hypoglycemia risk patients. Future coverage is expected to extend to all type 2 diabetes patients. With formulary inclusion at the three largest U.S. PBMs, Dexcom is positioned for ~13% annual revenue growth and margin expansion from longer-wear sensors and manufacturing efficiencies, driving 21% EPS CAGR and mid-teen total shareholder returns.

US Healthcare + Merger Arbitrage Catalysts

Healthcare

With President Trump signing the OBBB into law, Washington will now turn to other regulatory priorities and states will begin work on implementing the Medicaid reforms. Aldis Institutional's policy-focused events provide investors with timely and actionable insights into the DC landscape. This differentiated platform combines small group conversations with key stakeholders and policymakers, with real-time market commentary from Aldis' senior team. Recent and upcoming event topics include the outlook for ACA tax credits in Congress, Medicaid Reform Implementation - Including Work Requirements and Provider Tax Changes and the Outlook for Home Health and DME/CGMs after CMS's recent proposed rule.

Industrials

Aptiv reshapes its future, planning to split into two independent companies: one focused on software and safety technologies, the other on electrical distribution systems. The separation is designed to sharpen strategy, optimise capital allocation, and unlock value, as markets typically award higher multiples to software-driven businesses versus traditional auto suppliers. Stronger-than-expected automotive demand has boosted near-term fundamentals, with analysts raising earnings forecasts for 2025 and 2026. The breakup could attract new investor interest, offering both a stable cash-flow business and a higher-growth tech play. For investors, Aptiv’s restructuring presents potential upside and a classic spinoff opportunity worth close monitoring.

Technology

Jamf’s stock may appear attractive, trading at just 10x forward earnings, but Q2 results reveal several red flags. While adjusted operating earnings beat by $3.5M and Q3 guidance was set $8.5M above Q2, management only raised full-year 2025 income guidance by the same $8.5M, implying limited momentum. The timing coincides with a 6.4% workforce reduction in July, suggesting improved outlook stems from cost cuts rather than stronger demand. Financial statements also highlight warning signs of muted growth ahead. Despite its low valuation, these issues leave us cautious on Jamf’s near-term prospects and sceptical of sustained upside.

Technology

Nvidia’s coding momentum is weakening, raising concerns about its AI dominance. Once a leader in developer mindshare across GitHub, StackOverflow, searches, and job postings, its trends have declined sharply in 2025, ranking near the bottom of 150 stocks. This signals a potential headwind for sales, though hyperscaler-driven revenues limit direct correlation. More importantly, the trend reveals structural risks: developers are shifting from Nvidia’s proprietary CUDA toward hardware-agnostic frameworks like PyTorch, TensorFlow, and JAX, which run across AMD, Google TPUs, and others. With optimised kernels reducing Nvidia’s software edge, the erosion of developer focus may undermine long-term competitive strength.

Technology

Seeing strong growth from expanded product line and improved supply availability. Recent new product launches have boosted revenue and earnings, giving the company flexibility to allocate free cash flow beyond debt reduction. In Q4 results, Ubiquiti increased its dividend and announced a $500 million stock repurchase program. Investment in innovation and a broader portfolio opens opportunities for recurring subscription revenue, strengthening long-term growth prospects. With greater earnings power and shareholder-focused capital allocation BWS raise target price from $440 to $600.

Emerging Markets

Industrials

Insight lifts its target price for Salik to AED11 on expectations of new toll gates and the rollout of variable pricing. The Dubai concessionaire continues to deliver strong cash generation and dividend growth, while its unique rights to future gates underline long-term potential. Sensitivity to bond yields and inflation remains a key watchpoint.

Technology

86Research attended Kuaishou’s Investor Day in Chengdu, where management highlighted how AI is boosting engagement and monetisation across its core community while scaling Kling AI. OneRec has already lifted time spent and GMV, with full rollout and ecommerce upgrades ahead. Management frames Kling as a sustainable long-term business in a US$140bn video market, though further proof points are still needed.

Technology

While China’s e-commerce sector is mired in subsidy fuelled competition, Arete argues this is outweighed by strength in gaming and online entertainment. Record approvals and blockbuster titles underpin upgrades for Tencent and NetEase, while Alibaba shows early signs of a turnaround in quick commerce and cloud. The report also examines mounting cost pressures at Meituan, the lack of near term catalysts at Xiaomi and SEA, and the structural headwinds still facing JD and Baidu.

Technology

Vision Research sources DM and EM short ideas and has closed 2 of its Asian shorts in 3Q25. WPG Holdings (3702 TT) and Powertech (6239 TT) were initiated in 2024 and generated alpha of approximately 58% and 43%, respectively, vs the TWSE. At the time of initiation, both traded about $20mn/day and had SI% of < 2%. Other Asian shorts closed in 1H25 include Shimano (7309 JP) and Ricoh (7752 JP). Vision’s active coverage includes 9 Asian shorts, 13 European, and 17 US.

India China Ties Warm Boosting Chinese Firms

India and China are witnessing their most significant thaw in relations since 2020, with border trade, flights and visas reopening. Yet India’s dependence on Chinese imports, especially in pharmaceuticals and electronics, leaves its deficit at record highs. The revived engagement appears to offer greater benefits to Chinese companies for now, with names like Xiaomi, Alibaba, BYD and Tencent best positioned, while Indian groups such as Cipla, Dixon and Adani seek to leverage selective partnerships.

Developed Markets

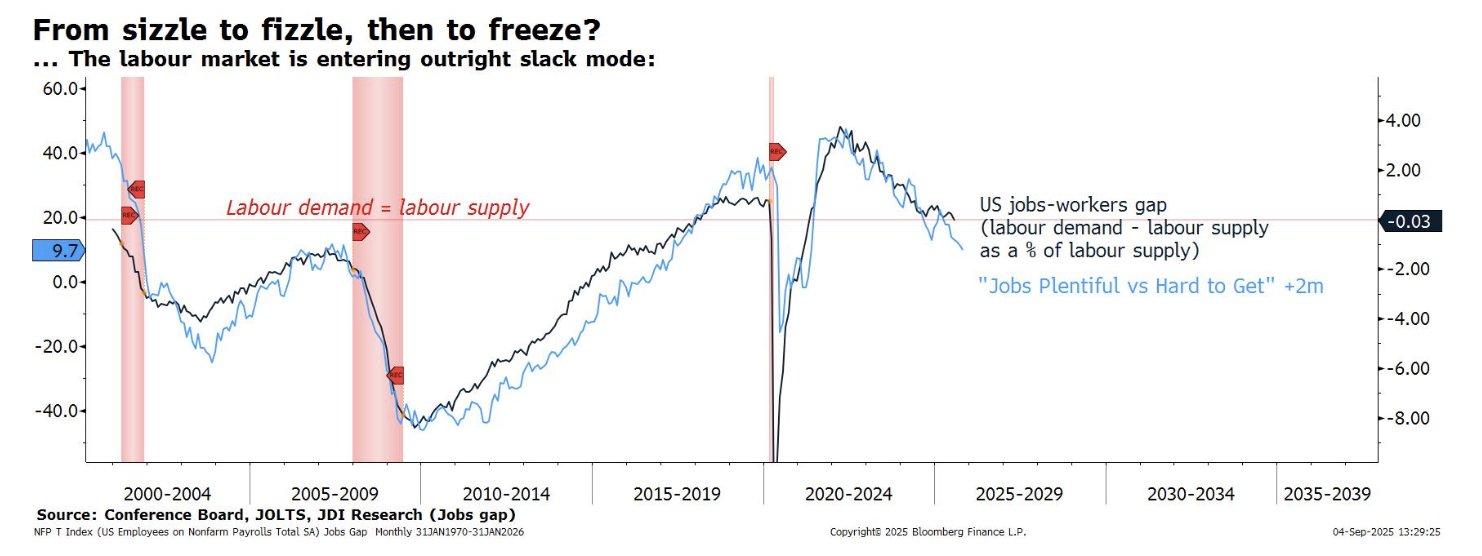

AI and the upcoming labour bloodbath

Markets are celebrating low unemployment and incoming Fed cuts, but Juliette Declercq worryingly claims that the reality is far darker; AI is dismantling the low-skill labour force and quietly erasing opportunities for young workers. This isn’t the story on the main street, but is the kind of contrarian roadmap hedge funds rely on to position ahead of consensus throughout the year. Even if the NFP is calmer than expected, the real damage will show up elsewhere – stagnant wages, falling income expectations, and a generation watching its prospects vanish. Juliette’s latest report examines who the winners will be and how to play the upcoming market upheaval.

Living on borrowed time>

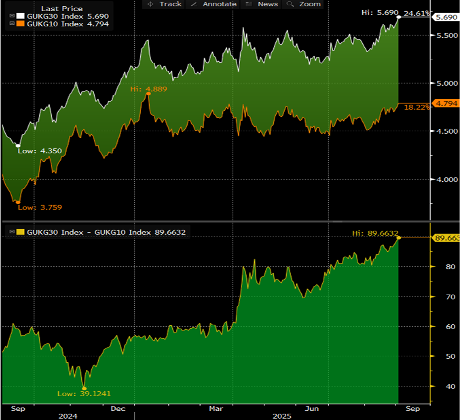

Stephen Jen points out that the 30Y sovereign bond yields in several countries in the developed West rose further on 2nd September and contributed to a further steepening in the 10Y-30Y yield curve. The two charts are for the UK, but the US and France look quite similar. These movements in the bond markets also hurt the equity markets. Stephen thinks the high long-term borrowing costs, which are refusing to come down, may reflect investors’ angst about fiscal sustainability. For the UK and France, the story is clear: there is so far no political commitment to contain spending. The US falls into the same camp, though there were some (but insufficient) efforts to cut spending. 2025 is the year when fiscal dominance starts to erode the power and influence of central banks. The pandemic, the hyperactive policy reactions, the changed social opinions about welfare are all coming together to alter the dynamics of the bond market.

France: Instability ahead

The country is entering another period of political turbulence over next year’s budget. Niall Ferguson sees Beyrou’s days as prime minister as numbered, expecting him to lose the confidence vote on September 8th. This will put President Macron back into the driver’s seat, and Niall expects him to nominate another minority government that can secure a 2026 budget with PS cooperation. Yet such a budget would reduce the deficit only marginally. The other scenario is parliamentary snap elections in autumn, which would raise the risk of a victory for RN. In any case, Niall expects the risk premium on French sovereign bonds to rise in the coming weeks, with Frech political instability a major European theme for 2H/2025.

Portugal: Breakout for the Lisbon PSI

Chris Roberts reports that the Euronext Lisbon PSI (7,768) exceeded the 7,860-7,900 target range, for the 12-month rectangle breakout, reaching 8,032 in August. The 32.4% gain from the April low is in line with other advancing phases since the 2020 low. Longer-term, major resistance extends from 13,000-15,000. Chris would be interested in buying into a double-digit percentage correction. Prior falls have varied from 12% to 18%. He is now 25% long from 6,536, having sold 25% at an average of 7,918 (see P.20). His stop stays at a daily close below 6,495.

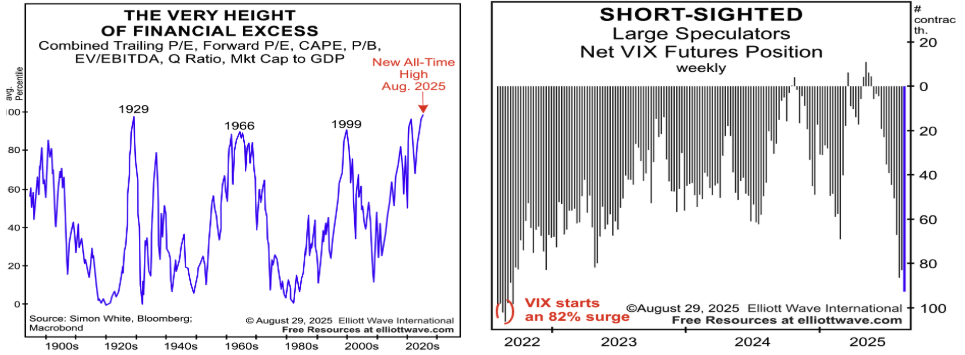

US stocks the most overvalued in 130 years

There is no escaping overvaluation if you are a multi-decade investor. The seven typical valuation measures that Craig Ferguson monitors are now at such an extreme that at nearly a 99th percentile rating the level of US equity market overvaluation is now the highest level seen since 1980 when records pretty much began. The signal is clear: long-term investors should be markedly UW stocks and largely out of US equity markets. This may be against consensus as the globe remains OW equities, but this is at a time when old sage Buffett is raising cash to $35 or more of his portfolio just as he did in the two most recent major overvaluation episodes in 1999 and 1966. Chart 2 shows that large global hedge funds are now nearly as short S&P VIX futures (or volatility) as they were in late 2021, just before the Nasdaq plunged by -38%. This won’t end well for equity markets.

US: Hammer Dollar to fall

James Aitken says that there is no denying the US labour market is weakening. If the participation rate had remained stable, the US unemployment rate would now be 4.9%. In his Jackson Hole speech, Fed Chairman Powell put a rate cut on the table. It is certainly a gamble, given inflation has been above the Fed’s target for fifty-four months in a row, but that’s why Powell was careful not to suggest a whole bunch of cuts are coming. Whilst we can all imagine the Pavlovian response to a Fed cut or two later this year (‘let’s buy more stocks!’) what’s more interesting to James is that Fed cuts make it mechanically cheaper to sell dollars outright. Short the dollar becomes less of a negative carry trade, less of a drag from an overlay perspective and therefore global capital may choose to hedge (sell) more dollars outright… especially if it helps them sleep better on their otherwise fully invested US asset overweight. If the dollar is going to fall further, now is the time.

US: Risk will become visible

Valerie Gastaldy cannot remember such a quiet market for such a long period. Bonds, commodities, and the dollar are in narrow ranges, and they are remarkably stable in those. It is always tempting to think that the longer the wait, the faster the speed, after the breakout. This is not what she has noticed. In those markets that are heavily traded by algorithms, speed is fast when reversals occur fast, but after ranges, false signals occur and speed starts slowly, to increase with time. The MSCI World, and foremost US equities, are still indifferent to the questions that other assets underline. Valerie thinks risk will become visible if and when the dollar resumes its fall together with US equities. For many weeks now, US equities have been rising as the dollar was falling, or flat. A change in this correlation may underline a change in risk attitudes.

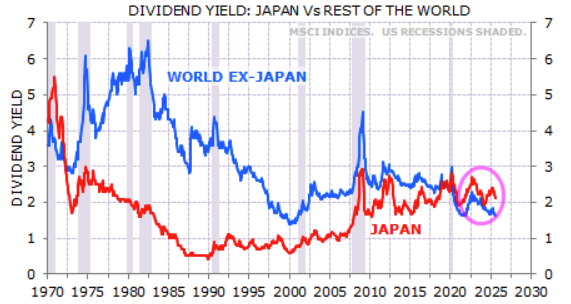

Japan: Adjusting to the end of stagnation

Escaping secular stagnation points to higher rates in Japan. Gerard Minack points out that false dawns have occurred below, so policy makers are willing to stay behind the curve. Changes in the economy are occurring: the equity-bond correlation flipping positive indicates a return to macro normality; stronger nominal growth is a tailwind for corporate sales and credit growth; the stock of credit is now rising at a solid pace; corporates have improved their allocation of capital; EPS over the past decade has matched the rest of the world; and the country now offers a higher dividend yield than its peers for the first time in fifty years. There’s a lot of changes, but they’ve yet to be rewarded, and Japanese equities now trade at a big discount.

Emerging Markets

Argentina: Brace for volatility

As the country enters its midterm electoral season soon and more important national midterms in October, Niall Ferguson comments on how erratic monetary policy, fuelling FX instability and very damaging moves in local rates, undermines the credibility of Milei’s economic team. Data suggests that economic activity has weakened. Niall expects Milei to win the midterms, with citizens endorsing his disinflationary success whilst the opposition remains headless. Yet the likelihood of defeat in the Peronist-leading Buenos Aires province has grown. The September outcome will be crucial to avert further volatility in rates and FX, and Niall believes that the popularity of Milei’s stabilisation plan will give him an opportunity to consolidate public support and steady markets, but do not lose sight of the key fact that October is what matters most.

China: The balance is shifting

For much of this year William Hess has been following the theme of relative macro stability against a backdrop of micro (sector/corporate) weakness. With some exceptions, this balance is shifting. Most important is that last week saw a massive rerating of forward earnings growth and cash flow per share expectations for the CSI300. Predictably, this follows a bottom for M1 (the old definition) to GDP on a rolling 12m basis and signs of modest but systemic injections of cash. The market view appears to be shifting whereby micro performance is now dominant as macro performance softens. On the macro data, predictable softness to the FAI data, for example, has the important exception that everything tech and IT is booming as energy investment and even manufacturing capex growth slows. This dynamic has worked well for equity market performance in the US and may be gaining momentum in China.

China’s saving glut and the A share boom

The country’s unprecedented savings glut, standing at a staggering trillion dollars’ worth of extra liquidity flooding into the financial system each year, has nowhere to go and has depressed interest rates and yields to rock-bottom levels. Attempts by Beijing to revive the property market and push a consumption boom have been met with failure. Sure, the growth environment is weak and corporate earnings flat, but Jonathan Anderson points out that the local equity market has never been particularly correlated with growth, in part because of the overwhelming role of liquidity in pushing valuations around. With the combination of record-high excess liquidity and low multiples in the domestic market today, Jonathan sees a very big potential powder keg, which is one of the key reasons why he currently holds the A share index in his portfolio.

DR Congo: Murmurs in the military

The military prosecutor indicated that the state has sought prison sentences ranging from three to 15 years for 40 military officers accused of plotting a coup. The military officers were arrested in April, after being filmed at a hotel declaring an end to President Felix Tshisekedi’s governance and stating that they would seize power. The development comes on the back of scores of arrests of military officers in recent months for various alleged infractions. While the risk of a coup in the near term is considered low, the risk will escalate to moderate over the longer term, particularly as the 2028 elections approach. If Tshisekedi fails to resolve the M23 conflict, it will likely worsen lingering public grievances with the statesman. This could undermine Tshisekedi’s position within the ruling Sacred Union coalition and the military, and may even lead to elections being cancelled.

Peak Tunisia?

Mandy Ong notes that Tunisian sovereign dollar debt has rallied dramatically over the past two years, in part due to initial macro adjustment at home and in part given the broader rally in other EM high-stress economies. To a large degree the repricing was warranted, as she stressed in earlier research - but now, with export and tourism earnings stalled, the current account worsening again at the margin, fiscal deficits still wide and high public debt indebtedness, Mandy fears that headwinds are again starting to build gradually. As a result, she sees 2025 as the end of the bond rally and suspect this is a good juncture to take profits.

Commodities

Iron ore is too big to ignore, but headwinds prevail

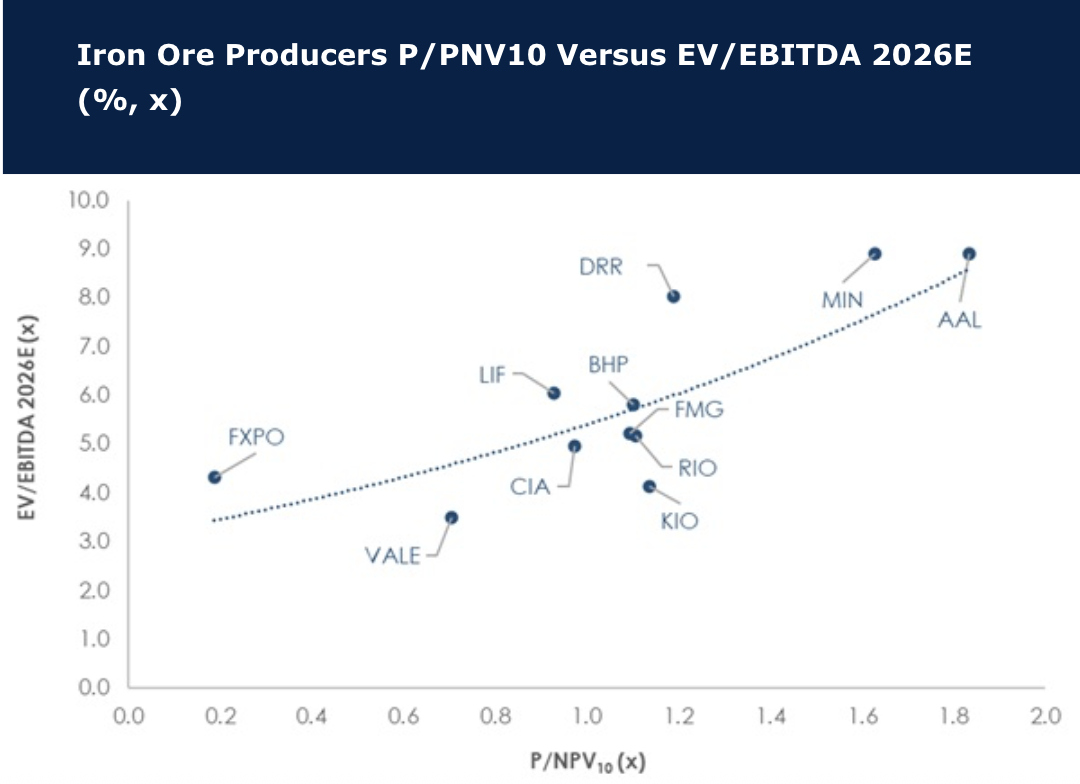

Iron ore seaborne supply is increasing at a time when steel demand is ailing, and David Radclyffe points out that this rightly makes investors nervous. However, the spot iron ore price has proven to be quite resilient this year at ~US$100/t. The headwinds may have dissuaded some investors, but at $378bn the iron ore market is simply too big to ignore in mining. As demand rolls the cost curve is key to sustaining volumes, and David assesses the LT price at US$95/t (US$101/t). Iron ore pure plays and diversified miners trade at 1.1x P/NPV10, and a prospective next two years average EV/EBITDA of ~5.8x and dividend yield of ~4.4%. Relative to other sectors this is reasonable, but high compared to historic levels. In the diversified iron ore-rich miners David prefers buy-rated BHP, then Vale, while in the pure plays it is Labrador Iron Ore Royalty. Overall, he remains underweight iron ore, with sells on key pure plays. Herein, Champion Iron is upgraded from sell to hold.

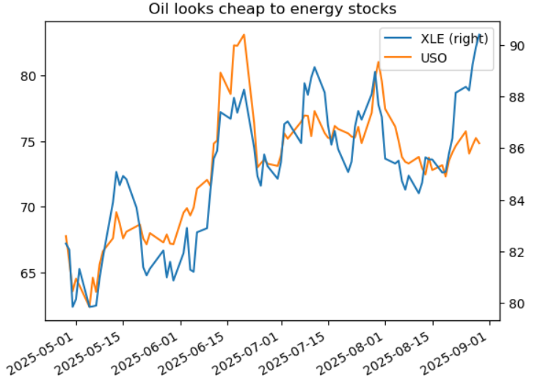

China’s oil appetite

Last week David Woo bought oil on the view that China’s decision to go its own way on AI means increased energy usage from less efficient chips. Positioning remains extremely short, and Chinese AI stocks charging higher along with increasing geopolitical risk from Europe’s snapback sanctions on Iran bolster David’s view. Oil may not have had a substantial move last week, but energy stocks did, increasing his conviction that oil has some catching up to do. We may soon see the short squeeze David is waiting for, and Trump may also be feeling the pressure from Europe to hold Putin’s feet to the fire. He bought the December WTI future at 62.99 and will take profit on a move to 68 and stop out at 60.

Copper: Gold to the rescue

China, the largest copper market, shows no signs of improvement. Meanwhile, the global copper market recorded a 251k-ton surplus in the first half of the year, and some studies are projecting further surpluses for FY2026. Broader commodity signals reinforce this outlook, particularly the sustained weakness in iron ore prices. Expect a 5-10% decline in copper prices by year-end. Interestingly, in Veritas Research’s sample of nine copper producers, costs decreased by an average 16% and 21% in the last two quarters, driven by higher gold prices for which the precious metal is a by-product. Hudbay as a result takes the crown as the lowest cost producer, with strong growth potential and the lowest valuation in their sample. Teck Resources and Lundin Mining are fighting for the dubious honour of being the highest cost producer.

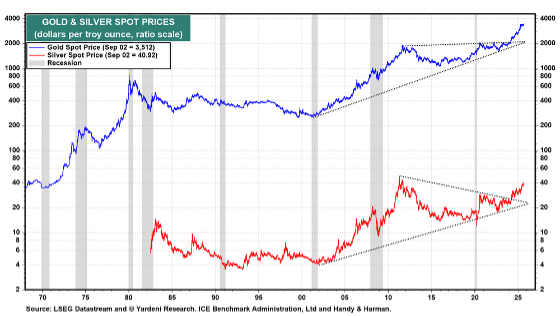

Gold: Brighter than ever

Ed Yardeni turned bullish on gold last year when the spot price of the shiny metal decisively rose above $2,000 per ounce (chart). He attributed this new bull market in gold to Russia's invasion of Ukraine in February 2022. In response, the United States and its allies froze the international reserves of Russia's central bank. That convinced the central banks of countries with autocratic governments, which are naturally hostile to the US, to increase their gold purchases. Earlier this year, when the price of gold was slightly below $3,000, Ed projected that it might remain in the rising channel that started in late 2023, reaching $4,000 by the end of this year and $5,000 by the end of 2026 (see chart below). So far, so good. Today, the spot price of gold broke out of a recent consolidation pattern to a new record high of over $3,500. The nearby futures contract just hit $3,600.

What silver’s critical metal label will really mean for prices

Since 1980 Jeffrey Christian’s buy/sell recommendations since 1980 have significantly outperformed simple buy-and-hold strategies in both gold and silver. In his latest presentation he continues the discussion about silver’s new designation in the USGS draft list of critical metals, pointing out that this label has been misinterpreted by many. Investors should take heed to note the difference between critical and strategic metals. Since WW2, metal has been essential to US defence stockpiles, but investors still need to separate hype from fact and ignore misleading speculative claims about government stockpiling or military consumption. Jeff also addresses the role of silver in soler panels, EVs and new battery technologies, and the path for demand ahead.

Click here to watch.