Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

Proven stock-picking outperformance

AIR’s Top 10 Best Ideas strategies continue to demonstrate exceptional consistency and alpha generation. Since inception in 2012, their European Large Cap Top 10 has delivered +526% performance vs. +142% for the STOXX Europe 600, with AIR beating the benchmark 85% of the time over 14 years. In 2025, their Large Cap portfolio gained +31%, outperforming the index by +14.4%, driven by standout performers Heidelberg Materials (+87%) and BAE Systems (+49%), with Vonovia the only negative contributor. AIR’s Mid Cap Top 10 was equally compelling, returning +36.9%, beating the STOXX Europe Mid 200 by +20.5%, with key contributions from Saab (+130%), Hensoldt (+113%) and ACS (+75%).

Ahold Delhaize (AD NA) Netherlands

Iron Blue initiates coverage on Ahold with a score of 26/60, which is top quartile and fertile grounds for shorting. They highlight FY24’s spike higher in balance sheet vendor allowance receivables, with days outstanding hitting a 10-year high. The €147m Y/Y rise was the highest in 8 years and equated to 5% of FY24 PBT adj, or 0.2% EBITA margin. Ahold has consistently stripped out of earnings one-off restructuring charges and asset impairment expenses. FY24 earnings also saw a Y/Y benefit from lower inventories write downs. They also flag €2bn of additional debt not included in Ahold’s headline net debt calculation, including €1.3bn reverse factoring.

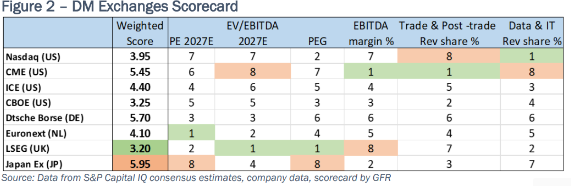

Victor Galliano names LSEG his top pick among developed-market exchanges, arguing the stock has been unfairly de-rated in 2025 on concerns that AI could disrupt its data and analytics business. This segment is protected by a defensive moat, with ~90% of data and feeds revenues covered by intellectual property rights. He also highlights the FTSE Russell index segment as a growing, structurally defensive revenue stream, benefitting from the continued rise of passive investing. LSEG ranks highest in his exchange scorecard (see above), driven by attractive valuation metrics and its good score in data revenue share. He estimates LSEG trades at a c.44% discount to Nasdaq on 2026E EV/EBITDA.

InPost (INPST NA) Netherlands

the IDEA! remains bullish on INPST following the announcement of an indicative proposal for a potential takeover. Looking at interested parties, European logistics peers risk facing antitrust hurdles, while e-commerce platforms such as Amazon or Vinted are unlikely to acquire the group outright. Private equity is viewed as the most plausible route, offering long-term capital, strategic support and operational flexibility. A consortium including PPF, Claure Group and Advent would already control ~38% of shares, with INPST CEO Rafal Brzoska’s 12.5% stake potentially tipping control. Re. valuation, the IDEA! sees EUR 16.00 (IPO price) as a floor for any deal, with their DCF analysis suggesting a potential value of EUR 18.12 per share, reflecting INPST’s substantial growth potential and European leadership in OOH deliveries.

SAP (SAP GR) Germany

Arete upgrades SAP to Buy, citing improving demand visibility as the ECC end-of-support deadline drives renewed urgency around S/4 and cloud migrations. Based on their CIO and partner checks, sentiment towards SAP has improved in 2025 vs. 2024, especially in the last few months, with more customers accelerating or restarting migration plans. While large-enterprise resistance persists, RISE adoption has shown clear signs of improvement. Arete sees limited displacement risk from GenAI, which CIOs view as years away from impacting core enterprise platforms; instead, GenAI may act as an indirect catalyst, easing migrations via automation and code clean-up. Applying a ~30x P/E multiple to their higher FY27E EPS yields a new €270 FY26 TP, implying 30% upside.

North America

The perils of premium valuations

Trivariate analysed the top 900 US equities by m/cap at each point in time to see how many stocks traded above 40x price-to-forward earnings for the first time in at least 3 years. On average this impacted 30 stocks per year. Historically, this valuation “ascension” is most common in Technology, followed by Financials, Real Estate and Consumer Discretionary, and rare in Utilities and Consumer Staples. Once stocks eclipse 40x, multiples typically contract to ~32.6x within 12 months, with 20% falling as low as 14x. Only 38% remain above 40x after one year and just 25% after two years. While the data suggests there is no need to panic sell a stock right when it first reaches a price-to-forward earnings multiple of 40x, it does appear that beginning 6- to 9-months later, the probability of outperformance begins to significantly deteriorate.

Turning 2025’s performance dispersion into alpha

Trendrating highlights that last year’s exceptionally wide performance dispersion created a powerful backdrop for active investors able to systematically capture winners and sidestep losers. Their US Large and Mega Cap model demonstrated how timely, rules-based trend signals helped clients meaningfully improve outcomes - increasing exposure to stocks in sustained uptrends while cutting risk in deteriorating names, as evidenced by their Winners & Losers track record. With 300+ institutional users, the firm positions trend capture as a repeatable source of alpha and risk control. The same disciplined approach is applied globally, with their Developed EU and Asia-Pacific models showing similarly strong performances.

Shorts continue to deliver outstanding returns

In 2025, MYST’s short ideas delivered an +11.3% average LTD alpha and 73.5% hit rate. Having reviewed all the shorts presented across their buyside events, several shorts remain compelling including:

Adobe - churn to accelerate due to new click to cancel laws + FTC scrutiny. TP $245 (30% downside).

Coca-Cola Consolidated - KO stake sale a red flag amid structural volume decline + MAHA / SNAP headwinds. This idea was highlighted at MYST’s Consumer Ideas event last month and the shares have already fallen 10%. TP $110 (25% downside).

Flutter - structural challenge from prediction markets jeopardises core online sports betting economics. TP $150 (30% downside).

Oklo - fuel supply constraints + regulatory hurdles create multi-year execution risk. TP $20 (80% downside).

Media, Internet & Information Services: 3 comeback stocks

Trade Desk fell ~70% in 2025, but Douglas Arthur sees fears around Amazon DSP competition as overdone. Forecasts for CTV and Retail Media - two critical end-markets - remain robust, while TTD remains a double-digit grower with high margins and a strong net cash position.

WPP, down 55% last year and trading at ~4x depressed EBITDA, is showing early signs of stabilisation through recent net new client wins. A new CEO from Microsoft is expected to refocus the business on a simplified, more customer-oriented model to restore revenue momentum.

Disney has been sidelined in 2025, but recent box office releases (Zootopia 2, Avatar: Fire and Ash) have been solid, while both Experiences and Streaming are contributing to bottom line growth. A decision on CEO Iger’s successor is expected in early 2026 - likely Josh D’Amaro - which Douglas believes could refocus investor attention once WBD-related noise fades.

Retail predictions for the year ahead

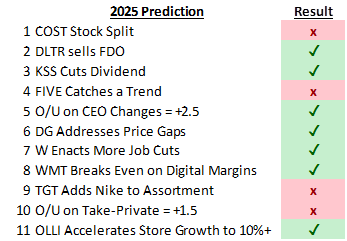

Looking back at GHRA’s 2025 Top 10 (+1) predictions, their batting average was good, hitting on 7 of 11 (see above). For the year ahead, their forecasts include: 1) Target announces an investment cycle on Mar 3rd with adjusted FY26 EBIT margin in the ~3.0%-4.0% range and a 2030 view of ~5.0%-6.0%. 2) Five Below launches Digital Loyalty Card. 3) Academy Sports adds another big brand…likely HOKA. 4) Costco unveils a special dividend and/or ramps share buybacks. 5) Ollie's embarks on large scale sales productivity effort. 6) Burlington takes a page (or two) out of the Ross Stores marketing playbook. 7) Someone gets acquired; BJ’s and Arhaus the most likely candidates. 8) Home improvement recovery gets pushed out…again.

Bank stocks face constructive 2026

The fundamental setup for US bank stocks in 2026 remains attractive, with mid-teens EPS growth driven by improving NII, benign credit costs, positive operating leverage and continued buybacks. Deregulation is a key secular tailwind, already contributing to a powerful 2025 re-rating, but valuations remain cautious at roughly 55% of the market multiple. While early-2026 performance may favour the investment banks, Charles Peabody would not be surprised if the stocks of JPMorgan Chase, Morgan Stanley and Goldman Sachs peaked in 1Q26 as he expects that to be the peak Y/Y revenue and PPNR momentum for these companies. He sees NII as a more durable revenue source throughout 2026, which favours the regional bank stocks. Charles sees the greatest relative upside in Citigroup, M&T Bank, US Bancorp and PNC Financial.

BTN sees several reasons to question how sustainable recent results really are. Standard payment terms are net 30 days for BRC, yet DSOs have climbed to 56 days and have been rising steadily for some time. In 6 of the last 8 quarters, organic growth benefitted from price increases, while underlying organic growth remains <3%. FX tailwinds have also aided recent results. Given these factors, BTN questions whether true organic growth exists at all and one thing that history has proven many times is that growth through acquisition stories often underperform when organic growth turns negative. Additional accounting red flags inflating earnings include lower bad debt reserves, reduced depreciation from aging equipment and acquisition accounting that excludes goodwill and intangibles amortisation.

Under its new CEO, CHRW has implemented a lean, AI-enabled operating model that has enabled the company to grow earnings despite struggling topline growth. Abacus expects EPS to average ~19% CAGR over the next 3 years, even without any help from a cyclical recovery, highlighting exceptional operating leverage and incremental margins of ~100%. Importantly, the demand environment is unlikely to worsen without a severe recession, hence any cyclical upside is mostly a free option. If investors gain confidence that high incremental margins are sustainable and CHRW is once again a structural share gainer, Abacus believes the stock can continue to re-rate higher.

Judy Marks is a poor fit for the CEO role. Her tenure has been marked by share-price underperformance, repeated guidance cuts, underinvestment in innovation and purging experienced internal talent to make way for inferior DEI placements. Facing a weak China market, Marks has relied on repeated restructurings that have further hurt morale and credibility. Paragon’s research draws on interviews with former senior executives from OTIS, Siemens and Dresser-Rand, revealing a sharp contrast between her stronger reputation at Siemens and overwhelmingly negative feedback from OTIS insiders. Sources cite a fear-based culture, weak grasp of the core service model and poor capital allocation. Paragon argues Marks’ leadership style is misaligned with the company's need for stability, operational discipline and reinvestment.

2025 winners & surprises; top themes & names for 2026

Last year, SPR's field-driven insights helped identify meaningful momentum in names such as Ciena, Snowflake, MongoDB, CrowdStrike and Datadog, while also flagging emerging headwinds in areas like UC/CC, vulnerability management and parts of storage. Looking ahead to 2026, their focus sharpens on where AI moves from hype to measurable ROI, how infrastructure refresh cycles finally materialise and where platform consolidation reshapes security, data and software delivery. From AI agents and identity as the new control plane to broadband acceleration and go-to-market disruption, SPR sees multiple inflection points ahead and meaningful opportunities for those tracking real-world signal over noise. Click here to access their report.

Hamed Khorsand upgrades INOD to his Top Pick, building on a bullish call first made in May 2024 at $12.30. With the stock now trading at $64, he still sees considerable upside to his $110 (12-month) target price. The 2026 outlook is anchored by multiple catalysts: accelerating demand from LLM developers, deeper monetisation of large enterprise clients and a clear inflection in US government work. With 2025 revenue growth set to be >45% and 2026 forecast at ~29%, Hamed expects to see powerful second-half operating leverage - and notes that INOD can fund growth organically, unlike AI hardware related companies.

Japan

JINUSHI (3252 JP) Japan

Yuka Marosek’s bull case on JINUSHI centres on its unique, land-only (“sokochi”) real estate model, which structurally removes building risk while delivering long-duration, stable cash flows. As the only listed specialist in this niche, JINUSHI benefits from high entry barriers, a 20+ year track record and a captive exit via its private JINUSHI REIT, whose AUM is set to reach ¥300bn by FY12/26. Her thesis highlights rising corporate demand for off-balance-sheet land ownership to improve ROE, aligning directly with TSE governance reforms. Sector growth is compelling, with Japan’s land-lease market projected to expand from ¥6tn in 2023 to ¥10tn by 2026. As recurring revenues scale, Yuka expects a rerating from cyclical developer to defensive, fee-based infrastructure play.

Emerging Markets

India: Corporate governance - clean opinions, dirty outcomes

Iii delivers a forensic take on the growing cracks in India Inc’s corporate governance, documenting multiple high-profile accounting lapses, frauds and management exits that surfaced in 2025 despite clean audit opinions. Their research sharpens the debate by introducing audit fees - and audit fee as a percentage of PBT - as practical indicators of audit independence, flagging cases where fees rose sharply even as governance issues went undetected. At a sectoral level, Iii highlights that audit fees for the BSE 500 grew at a 12% CAGR over 3 years (and 15% in 2025), with outsized increases in Power (64% CAGR), Consumer Durables, Retailing and Agri raising questions on audit depth vs. complexity. Rising audit fees should be interpreted not as a clear red flag, but as a proxy for auditor-client relationships which, in environments of weak internal controls, may delay escalation of adverse findings.

China: Muted recovery, selective alpha

86Research expects 2026 to be a year of gradual recovery for China’s internet and new economy sector. While policy support should begin to emerge in 1H26, its impact on activity and earnings is likely to be felt mainly in 2H26. They model sector earnings growth of 10%, solid but well short of a cyclical boom. Valuations remain undemanding, leaving room for further re-rating as fundamentals improve. Against this backdrop, 86Research favours selective exposure to three structural tailwinds: easier global liquidity, scaling GenAI monetisation and accelerating overseas expansion. Their 2026 top picks - Alibaba, PDD, Baidu, Trip.com and DiDi Global - each offer differentiated exposure across growth, value and AI optionality.

An excellent Q4 has effectively completed the turnaround in Samsung’s shares, shifting the debate from recovery to how long to stay invested. The company has done exactly as Richard Windsor expected - abandoning HBM3 and focusing entirely on HBM4 - and he is now virtually certain that Samsung will be announced as having qualified for Nvidia and will return to being a major supplier in 2H26. With global HBM capacity constrained through at least 2026 and likely 2027, Samsung, alongside SK Hynix and Micron, will sell everything they can produce at attractive pricing for a while yet. Richard suspects that forecasts will increase again when the company reports its results in detail later this month. While he is starting to think about exiting his position in the stock, the valuation remains fairly unchallenging compared to the peer group.

Macro Research

Developed Markets

From tightening to tailwinds

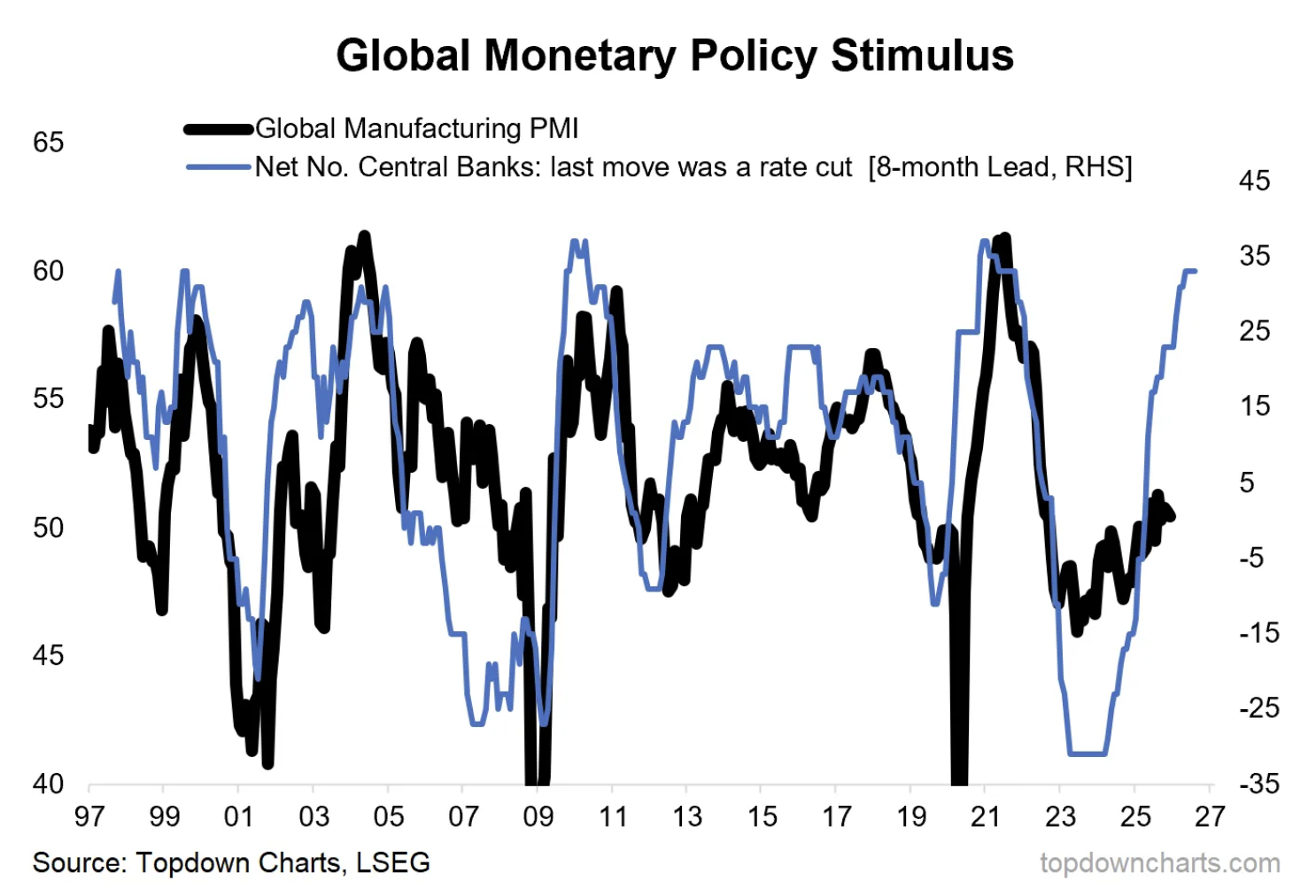

Callum Thomas says that the biggest story in macro of the 2020s will echo on into 2026, with monetary policy going from tailwind in 2020 to tightening in 2023, and back to tailwinds again now. This is coming at a time where nascent signs are showing an upturn in the macro pulse from previous stagnation (e.g. the global manufacturing PMI). Callum points out that the path laid out by the monetary policy leading indicator in the graph below is a very interesting one indeed, and it’s not the only sign. The OECD leading indicators are also pointing to a major improvement in the global economy. Aside from monetary tailwinds there are several other factors working into this thesis such as fiscal stimulus, thematic capex, inventory cycles, and so-on. But there are a couple of logical flow-on effects we need to watch should this play out as planned. One key flow-on will almost certainly involve inflation resurgence.

Roaring productivity vs the AI bubble

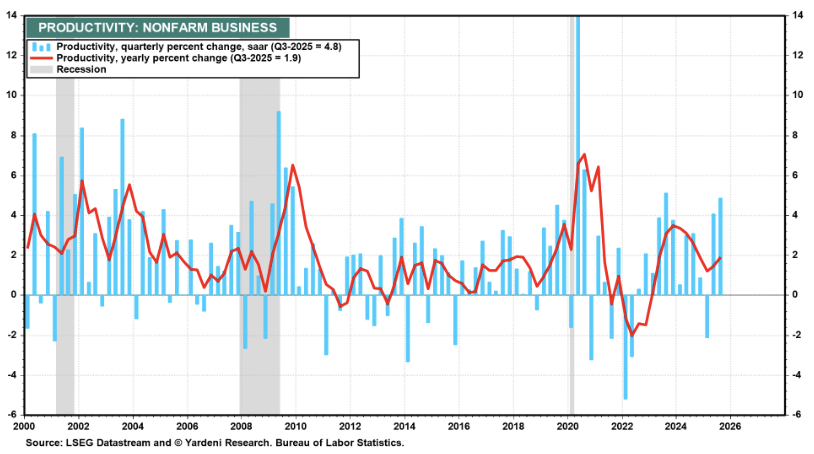

The latest Bloomberg Businessweek had the AI bubble as the cover story. Some may take this as a sign to be nervous, but from a contrarian perspective Ed Yardeni argues that it’s bullish as it signals the bubble won’t burst, if it even exists. People have AI fatigue. Ed recently recommended underweighting the Mag-7 as their AI arms race is forcing them to spend billions on infrastructure that could quickly become obsolete, and that could be unprofitable as competitors squeeze their margins. Ed believes the air can be let out of the AI capital-spending bubble over time without it bursting and causing a recession. Meanwhile, AI is starting to boost the productivity of the users of this tech, especially the S&P 500’s Impressive 493. Non-farm business sector labour productivity increased 4.9% (saar) in Q3-2025, as output increased 5.4% and hours worked increased 0.5% (see chart). Q2-2025 productivity was revised up from 3.3% to 4.1%. These are striking numbers!

Blonde Money

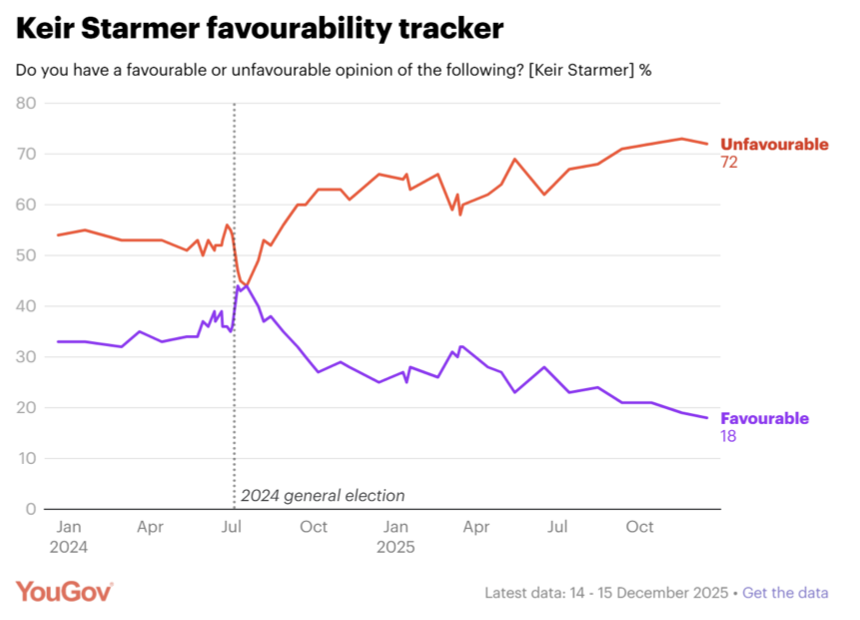

UK: The end of Starmer

Kier Starmer’s time as Prime Minister is coming to an end, predicts Helen Thomas, as it awaits only the proverbial last straw. His net favourability rating is as low as Boris’s on the day he resigned. The idea that it is difficult to remove a Labour leader is incorrect: the Part recently changed the rules so that the leader can be challenged at any time, not just at a party conference. Once the contest is announced, the battle lines will be drawn and public declarations quickly made by MPs, the contest lasting no longer than 6-7 weeks. As time passes, Starmer is posing more of an existential threat to the Party and waiting for elections will be too late; Reform are gathering more money, more ground troops and are professionalising themselves. For Labour, it’s now or never.

UK: Thoughts on monetary policy communication

In his feedback on the recent NIESR monetary policy roundtable David Owen focuses, in part, on how the BoE should better communicate policy. David is still a fan of the fan charts, first presented by the BoE when publishing Inflation Reports after the ERM debacle of the early 1990s. In contrast, he attaches little value to the narrative now provided by each MPC member after each policy decision. Far better to continue with keynote speeches, with each member providing a more detailed summary of their thinking only quarterly. David also considers that the roundtable gave too much attention to QE; the debate has moved on. Now the focus is on the BoE transitioning to a demand-led repo operating framework, as bank reserves continue to decline, on the back of QT. Debating the effectiveness of QE now seems very much like fighting the last war.

A taste of Europe

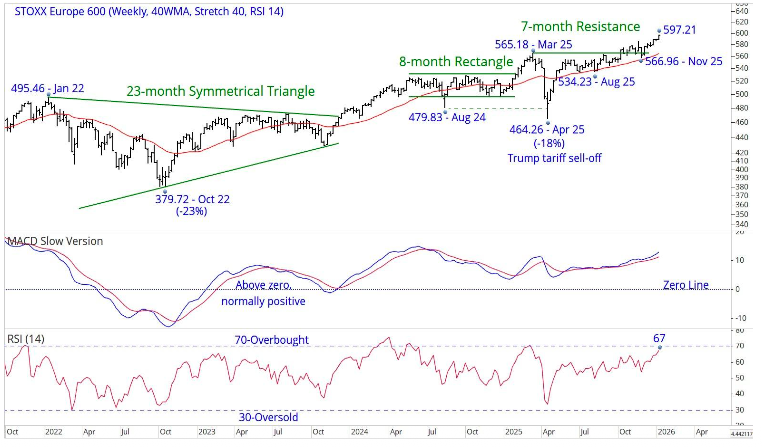

The STOXX 600 (596.14) has started 2026 with a new ATH, trading as high as 597. Next resistance is at 600, but this is not expected to be a significant obstacle. Chris Roberts’ minimum long-term target stays at 800+. That level is derived from the breakout above the 21-year ceiling around 400. The minimum expectation for a sustained breakout above a multi-year ceiling is a doubling of that ceiling. The 14-week RSI is currently at 67, just below the 70+ overbought zone. MACD has been above zero since Jan 2023. Chris remains 50% long from 576.29. The recommended stop stays at a daily close below 527.00.

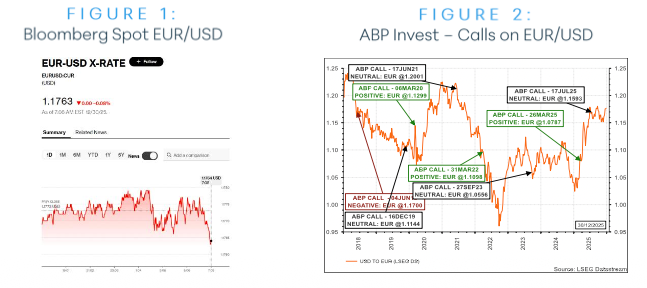

Upgrading EUR/USD to positive

ABP Invest recently upgraded EUR to positive against the USD. This goes against their intuition that the USD could be a stronger currency in 2026 on either a stronger-than-expected US economy or a deteriorating US economy that triggers the safe-haven characteristics of the greenback. However, given the second consecutive month of an improving overall score differential between the currencies, the team felt the decision-making process should not be impacted by their qualitative expectations. In March 2025 they turned positive EUR/USD at 1.0787, given their concerns on US developments driven by Trump and the surprising pick up in underlying European economic data - the decision turned out to be quite timely. Should the recent slower economic patch in the US continue and the long-awaited fiscal push take place in Europe, alongside positive momentum from Russia/Ukraine developments, there could be further upside.

US inflation still above target as job growth narrows

John Fagan notes that Tom Barkin, President of the Richmond Fed, recently delivered a cautiously optimistic speech to the Raleigh Chamber of Commerce, highlighting the need to watch both sides of the Fed’s mandate. Barkin noted that while inflation has slowed in recent months, it remains above target. Meanwhile, unemployment is relatively low at 4.6%, but it has been creeping upwards over the past few weeks. Slow job growth has contributed to the rising unemployment rate. Additionally, Barkin highlighted that roughly 90% of the 70,000 jobs added per month in 2025 were in healthcare and social work, indicating a reliance on select industries to offer new work. Looking ahead, Barkin cautioned that consumer index scores are close to bottoming out, recording their second lowest ever reading in November. However, incoming deregulatory initiatives and the delayed impact of federal rate cuts signal that consumer sentiments may rebound in early 2026.

Emerging Markets

Argentina holds the line

So far so good, claims Jonathan Anderson. Not only is the post-election government holding the line on the budget, it is also maintaining the sharp policy changes of last summer, i.e., tight quantitative monetary conditions, positive real interest rates and FX market liberalization. There’s no "landing" yet. Overall credit is still growing at a 50%-plus y/y annualized pace, with inflation also stuck in the 30%-35% y/y range on a sequential basis. And the external balance is worsening again as demand pressures continue to build. There’s still work to do after all. Even so, Jonathan is taking NDF peso exposure. The forward market is pricing a dramatic peso depreciation over the coming quarter, which seems unlikely under current macro conditions, and the team are taking a tactical position here. By contrast, Jonathan remains on the sidelines in the dollar sovereign and equity markets.

Brazil: The effects of fiscal impulse

Buysidebrazil’s latest report examines the effects of fiscal impulses on the investment decisions and capital structure of Brazilian companies listed on B3. They find that an expansionary fiscal shock of 1% of GDP is associated with: (i) a reduction of up to 4.14% in the investment rate after one quarter; (ii) a decline of up to 2.77% in leverage after six quarters; and (iii) an increase of up to 4.73% in cash liquidity after three quarters. This behaviour signals bad news for productivity and long-term development, since persistent private investment retraction compromises capital accumulation and the incorporation of new technologies, reinforcing the productive stagnation that has characterized the Brazilian economy in recent decades. As for the year ahead, the team project the exchange rate at BRL 5.50/USD, expect continued disinflation and further deceleration in economic activity, and the beginning of a monetary easing cycle.

China’s deflation: The case for a floor

China’s deflation lessened recently, and Paul Cavey says it is tough to attribute this stabilisation to an improvement in cyclical momentum; data in Q4 showed renewed property sector weakness and FAI numbers have been terrible. However, some domestic drivers are helping to address deflation, and China’s price level is also benefiting from global factors including the stability in commodity prices. There are also structural reasons to think deflation is cyclical rather than a hard-to-shake Japanese funk, such as the lack of signs of a balance sheet recession. However, Paul doesn’t see any real cyclical improvement as long the property market remains in crisis, and so does not expect CNY to move much. There is a scenario, however, in which pressure for CNY appreciation helps stabilise the domestic economy and thus becomes self-reinforcing. By intervening to slow down appreciation, the PBoC would boost domestic money supply and so try to engineer more domestic reflation.

India: Is the rupee now a problem?

The rupee has been one of the worst-performing EM currencies over the past few quarters, a big disappointment in an environment where most of the world was rallying against the dollar. Jonathan Anderson asks: is this a serious issue for the investment outlook ahead? He doesn’t think so. As always, the bad news is that India is a structural deficit economy without a buoyant export sector, which heightens currency risks in any given year, especially when domestic demand is booming. The good news, though, is that the trade balance has been distorted by huge cyclical gold imports in recent months, with little sign of aggressive inflation or monetary pressures building up in the system. As a result, Jonathan expects the FX market to calm down in the first half of 2026. Stay tuned.

Malaysia’s looking good

Sometimes small countries bring huge returns, reminds Konstantin Fominykh. South Korea has been his favourite since Oct 2024 and has since seen +104% gain. Now, Malaysia is grabbing his attention. The country is estimated to see real GDP growth of ~4.5% in 2026, outpacing many EM peers. Inflation is moderate and predictable, easing pressure on consumers and businesses. Unemployment remains low. The country’s equity market trades at attractive multiples with dividend yields above 4%, providing steady cash flow and downside protection. Konstantin also points out the nation’s central role in back-end semiconductor manufacturing and electronics, and global energy transition and data-centre initiatives are driving long-term demand for capital investment. Konstantin has had a buy on Malaysia equities since Aug 2025 and advises investors to look at the Malaysia ETF (EWM) for an extremely low-volatility instrument.

Venezuela: Fear and loathing in Caracas

After the formal inauguration of interim President Delcy Rodríguez, Venezuela is on tenterhooks, with fears of a coup d’etat. Amid the turbulence, Rodríguez has maintained open channels to the US government and its oil industry. What is more complicated for her is to ensure military support from Minister of Defense Vladimir Padrino López and Minister of the Interior Diosdado Cabello, who leads the Bolivarian colectivos and feared secret police. Cabello has a challenging relationship with Rodríguez (as well as being an enemy of Marco Rubio), making him the most unstable part of an unstable status quo. Niall Ferguson does not expect a coup attempt in the coming weeks. Meanwhile, the White House is rushing to entice American oil companies back to Venezuela, which Niall expects to be fruitless without a stable and investor-friendly government in power, although he expects Chevron to start shipping oil produced by other producers to the US. European players are complaining about past debts, but nobody is listening.

Venezuela: The knock-on effects of kicking out Maduro

According to Jose Ignacio Hernandez, Maduro’s sudden removal marks a political shock that forces Washington to rethink their oil-sanctions enforcement, OFAC licensing, recognition, and Venezuela’s long-frozen public-debt problem. Delcy Rodríguez enters office structurally weak and politically exposed, constrained by internal Chavista power balances and demands from Washington. The next 4–6 weeks will be decisive. If Rodríguez stabilizes her position, a second phase opens—bringing selective movement across oil policy, creditor engagement, asset strategy, and recognition. Aurora’s latest report lays out what is most likely to change, when, and under what constraints, including the outlook for OFAC licensing, the pending Citgo sale, creditor engagement, and US recognition policy. Jose says that contingent on Rodríguez remaining in power, gradual liberalization of sanctions—particularly in the oil sector—could become conceivable. This might include expanding Chevron’s license and granting new, limited individual licenses to select international oil companies.

ESG

South Africa: Sparking the transition

According to Peter Attard Montalto, South Africa’s climate transition is set to reach a pivotal moment of action in 2026. Peter says that carbon budgets, a tighter carbon tax and trade measures such as the Carbon Border Adjustment Mechanism move climate risk from disclosure into core business and financial decisions. At the same time, sustainability reporting will gain momentum to shift from voluntary practice to mandatory, investor-focused standards aligned with IFRS S1 and IFRS S2. However, Peter points out that most companies are not ready. Disclosures still focus on non-financial metrics and remain weakly linked to earnings, asset values and capital allocation. Data quality and systems lag, raising costs, limiting access to capital and increasing greenwashing. Clear ownership is now essential. Policy, regulation and market expectations must align. Companies and banks must embed reporting into strategy and risk management so it supports the transition to net zero rather than becoming another compliance exercise.

Commodities

Gold/Silver: No longer just a commodity

James Burdass reminds us that 2025 was the year when the gold stealth bull market turned into a mega bull market for precious metals (as his regular readers will know, this was a key call for Commodity Intelligence). Silver has seen one of the most pronounced catch up trades in its history. The 2020-2024 ratio was in the abnormal zone (80-120/1), which assisted us to make that call. At 56, the silver/gold ratio is now just below the 30-year average of about 65. James says that gold and silver have transitioned from being just a commodity to visible allocations by central banks, funds and other investors. He still thinks there is scope for more generalists to replace their exposure to US Treasuries with an allocation to precious metals, as fiscal dominance sets in.

Oil: A non-consensus forecast

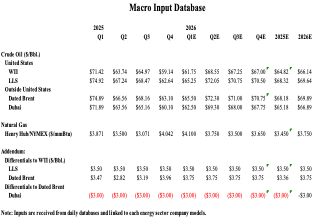

William (Buff) Brown’s preliminary take on the situation in Venezuela is that he currently sees no reason to amend his base case for 2026 either in terms of price or the physical balance, even though Venezuela’s long-term potential is obviously massive. He is retaining his hydrocarbon price estimates for 2026 (see table). William is aware that his WTI outlook appears absurdly bullish at this point. He believes crude oil prices were depressed relative to fundamentals in the fourth quarter of 2025, reflecting the overwhelming consensus view of a “mega surplus” in 2026. If his positive view is anywhere near the mark, funds should begin to buy en masse, complementing relatively constructive underlying fundamentals, helping to pull prices up contra-seasonally. For natural gas, however, he believes his outlook is less controversial and for the first quarter may even end up a bit on the high side.

What if copper reaches $7/lb?

With the metal starting 2026 with strong price momentum, David Radclyffe’s team examines the “what if” upside for the nine senior copper pure plays. In the year ahead, David estimates a 410kt copper deficit, as Grasberg and other issues feed through, and that is before production guidance downgrades are announced for some. The copper market is tight. Best leverage to higher copper prices is with First Quantum Minerals Ltd and Teck Resources Ltd, showing high EPS upside near term and with long-term upside to NPV assuming copper stays at US$7/lb indefinitely. Least upside is with Grupo México S.A.B. de C.V. and Ivanhoe Mines Ltd, albeit still good. GMR’s quality vs value screen highlights Grupo México S.A.B. de C.V. and Freeport-McMoRan Inc. as offering better value, although not with the best leverage. The chief risk is the obvious one, that copper is near-term overbought with long-term prices expected lower.

Precious metals: What happens next?

In this presentation, Jeffrey Christian of CPM Group provides a market update on gold, silver, platinum, and palladium prices as metals continue to reach record levels. He explains why political developments, both in the United States and internationally, have become one of the dominant drivers of investment demand for precious metals, moving away from traditional economic fundamentals. Jeff discusses how rising political uncertainty and strained international relationships contribute to elevated investor anxiety and renewed buying interest in gold and silver. Jeff also addresses persistent misinformation in the silver market, including claims about shrinking inventories, paper versus physical silver, and alleged shortages.

Click here here to watch