Europe

Consumer Discretionary

Stellantis’ latest results reinforce concerns that its finance arm is masking weakness in the core car business. While the market is focused on the potential for a recovery in earnings, the report argues that rapid growth in leased vehicles and heavy use of off-balance-sheet JVs is helping support sales and industrial free cash flow. With credit ratings now close to junk, higher funding costs could undermine this support and create further pressure.

Industrials

Epiroc remains a strong BUY despite lagging sector peer Sandvik’s recent surge. Since its 2018 spin-off from Atlas Copco, Epiroc has delivered consistently high returns, averaging 24% ROCE, well above its cost of capital. Its strength lies in a service-led business model: recurring services generate most revenue, while mining contributes 80% of sales. Global operations and extensive service networks create barriers to entry against rivals such as XCMG and Sany. Demand is supported by strong copper and gold markets, electrification trends, and growth in underground mining. With strong Q1 2026 orders, low debt, and expanding high-margin aftermarket services, AlphaValue sees around 30% upside and continued long-term growth potential.

Industrials

Strabag is a leading infrastructure player in Germany and Austria, where urgent reconstruction needs across bridges, railways and waterways support long-term demand. Renewables is another key growth driver, now representing 18% of sales after doubling over the past two years. European data centre activity is also being supported by the EU Chips Act and Horizon Europe, while the EU Green Deal should drive longer-term decarbonisation and building energy upgrades. With momentum across infrastructure, renewables, water, energy, mining and mobility in markets including Germany, Poland, Czech Republic, the UK, Canada and Australia, the source sees Strabag’s 5.5% 2026 EBIT margin guidance as beatable.

Industrials

Alstom shares fell 27% on 17 April and 36% since being added to Alumbra’s high conviction Active List in January, after the company issued a profit warning and disappointing FY27 free cash flow and EBIT margin guidance. In its 16 January initiation report, Alumbra had flagged that a significant year-on-year increase in unbilled receivables across H1 2026 and H2 2025 could indicate project cost overruns, weighing on future margins and cash generation. This was supported by its review of local subsidiary filings. Alumbra had also questioned consensus expectations for €700m of FY27 FCF, given recent cash flow benefited from €639m of unsustainable items.

Technology

Capgemini’s investment in the OpenAI Deployment Company reflects growing demand for enterprise AI deployment services, as organisations look to scale adoption through consulting, engineering and transformation support. Rather than posing a threat to firms such as Capgemini, Accenture and Infosys, the initiative highlights OpenAI’s reliance on consulting partners for sector expertise and large-scale implementation. This should create further opportunities for AI-enabled transformation services as enterprises move from experimentation to deployment.

Technology

Infineon Technologies AG was presented by a PM at a Revelare event as a long idea with ~50% upside to a €75 price target. The stock trades at ~16x 2027 EPS and ~12x 2028 EPS, below its 10-year median multiple of ~19x. The thesis rests on two tailwinds: analog recovery and AI datacenter demand. Infineon’s industrial and automotive businesses are rebounding, while €800–900M of annual underutilization charges should normalize, driving ~600bps gross margin expansion. Simultaneously, denser AI server racks require advanced power semiconductors, where Infineon leads across silicon, GaN, and silicon carbide. AI revenue is expected to grow from €700M last year to €1.5B this year, with additional upside potential. Gross margins could rise from ~17% to ~25% over 2–3 years, supported by higher-margin AI products and cyclical recovery.

Technology

When presenting FY25 results, TKH Group warned of a weak start to the year, making its 9.6% turnover growth in Q1 notable. The order book declined nearly 10% year-on-year but remained broadly stable versus year-end 2025, mainly due to weaker Tire Building orders within Automated Machinery. This was partly offset by 7.4% organic growth in Vision Technologies, supported by a stronger order book. Electrification and Digitalisation also performed well, benefiting from strong offshore and onshore cable demand. TKH continues progressing with its automation-focused strategy. The Idea maintain a positive long-term investment view based on growth, margins and cash flow generation.

North America

Consumer Discretionary

Despite near-term margin pressure, DFH trades at only 7.5x 2026 earnings and 1.1x book value, well below peer averages. Analysts maintain a fair value estimate of $25 per share, implying significant upside potential. They have the second highest ROE in the sector out of the 17 builders Housing Research Center follows. The stock is trading at $13.02 and peaked at $43 two years ago. They have grown nearly 5x in the past 6 years more than any other builder and recently made a bid to acquire Beazer homes (BZH) at 0.5x book value. That would allow them to grow another 50% in 2027. They should make EPS of $2.00 in 2026 and $3.00 in 2027.

Consumer Discretionary

Zach Shannon initiates a Short recommendation on Shoe Carnival which experienced a rapid deterioration in same store sales in Q4 FY25, with declines across all three of its store banners. This caused the company to walk away from its plan to rebanner more than 100 Shoe Carnival locations as Shoe Station (its higher-priced storefront) as converted stores significantly underperformed expectations. As a result, the company's CEO left abruptly (resigned or terminated) in February, with the company pulling its prior CEO out of retirement to serve on an interim basis. With inventory at a 10+ year high (inventory was up 14% last year on a 6% sales decline), the company faces pressure to rightsize the business and turn its stores around. However, guidance for FY26 is backend weighted, while FY27 consensus estimates appear aggressive. As a result, Corto believes SCVL shares have material downside risk (-20% to -50%).

Consumer Discretionary

Lululemon shares are trading at both 52-week and five-year lows after a difficult period marked by product challenges and pressure on the brand’s core offering. The source notes that the company had strayed too far from its brand DNA, with limited colour in parts of the range and the departure of its senior merchant. However, early signs of improvement are emerging, including a tighter product offering, more colour and the appointment of a former Nike executive as CEO. While a full turnaround is likely to take time, The Retail Tracker sees potential for the stock to reach $175 over the next 12 months.

New Street Launches Space Economy Coverage

Communications

Very exciting launch as New Street Research starts covering the Space Economy focused on satellites, components, connectivity services and datacentres. Initial coverage is SpaceX, Rocket Lab, Planet Labs, Viasat, Telesat, Iridium, SES, Eutelsat, EchoStar, AST SpaceMobile and Space 42. The team is led by David Barden, Pierre Ferragu and James Ratzer.

Consumer Staples

Sprouts Farmers Market reported encouraging 1Q26 results, reinforcing QuoVadis Research’s bullish stance. Revenue, same-store sales, margins, and EPS all modestly exceeded company guidance and Street expectations, suggesting management has regained control after the sharp slowdown experienced in 2H25. The company also deployed all 1Q26 free cash flow toward share repurchases, buying back 1.9M shares at an average price of $73.68, with QuoVadis modeling $500M in buybacks for full-year 2026. While guidance was largely maintained, the EPS outlook was slightly raised, signaling improved visibility. At just 13x P/E and 8x EV/EBITDA on consensus 2026 estimates, the stock undervalues Sprouts’ strong ROIC-driven growth and favorable risk-reward profile.

Financials

86Research recommends investors aggressively buy Futu following its 14% post-1Q26 preview selloff, arguing the decline significantly overstates temporary market-driven weakness with a US$231 price target, implying 59% upside from current levels. Analysts believe downward earnings revisions and geopolitical tensions triggered excessive selling despite strong rebounds in global equity markets since early April. According to channel checks, Futu’s user acquisition and net asset inflows have already recovered to pre-March levels, positioning the company to achieve its 2026 target of 800,000 net new funded accounts. 86Research also highlights FUTU’s dominant Hong Kong brokerage position, Southeast Asia expansion plans, strong management team, and industry-leading margins. Trading at only 11x 2026 earnings, the stock remains deeply discounted relative to historical averages and peers.

Healthcare

MDC Financial Research’s Event-Driven Legal℠ Investment Research service is closely monitoring Sotera Health Company's (SHC) ongoing EtO litigation in California, Georgia, and New Mexico. A key Summary Judgment Hearing related to the first group of eight Bellwether Cases in California is currently scheduled to be held May 27 - 28, 2026. A favorable Ruling could relieve Sotera from this initial set of Cases and strengthen its position against the 114 total plaintiffs (as of April 1, 2026) alleging harm from Sotera's L.A. area EtO facilities. MDC will attend this Hearing and provide timely insights.

Industrials

Another very successful Short idea from the Alumbra team as Primoris declined 50% on earnings last week after reporting disappointing Q1’26 results and significantly reducing FY’26 guidance due to cost overruns on renewables projects and lower-than-expected renewables revenue. Alumbra still have high conviction that the stock will decline further due to continued cost overruns on renewables projects and difficult revenue comps.

Real Estate

Ben Jones remains bullish on M/I Homrs as volumes remain solid despite higher mortgage rates, signalling ongoing demand. Despite the US housing market showing some weaknes, increased incentives, higher LTVs, lower interest rates ahead should continue to provide support. Current operating margins of 9.3% are below recent highs but only slightly under historical averages, with long-run margins around 11%. The company’s strong balance sheet position allows them to withstand downturns and capitalise on land opportunities. Ben favours their disciplined capital allocation, balancing cash reserves and share buybacks. A persistent US housing shortage should continue supporting home prices over the long term.

Technology

JNK Research showed ROHM and VSH entered earnings with supply tightness already visible across power and passives. Its April-May Analog Tracker flagged pricing increases across close to 95% of products, while book-to-bill improved from 1.06 to 1.10. ROHM print showed that with FY26 still under-allocated and FY27 Q1 likely to snap back double-digit QoQ on SiC mix and capacity additions. Commentary on discrete SiC mix and FY27 capacity reads across to ON Semi and WOLF. VSH print provided the cleanest US-listed read on the VICR shortage, with Q4 backlog close to 5.1 months and book-to-bill near 1.2.

Technology

Rosenblatt raises its price target on PENG to $54 from $32, a nearly 70% increase, following investor meetings with CEO Kash Shaikh and CFO Nate Olmstead that increased confidence in the company’s long-term direction. The firm highlights Penguin’s plan to leverage its 40+ years of memory-subsystems expertise and combine this with AI system/factory software and services to deliver a broader full-platform solution. Rosenblatt sees the strategy as increasingly cohesive, supported by the AI market’s rising need for optimised memory subsystems and the acceleration of corporate adoption of internal AI systems driven by agentic AI. The company also intends to use partner relationships to broaden its customer base.

Vision adds liquid, low-crowded US shorts

So far in 2Q26, Shorting Specialists Vision Research has closed shorts on Tractor Supply and Insulet (both initiated in 4Q24 at much higher levels) and has initiated 2 new US shorts. The first a consumer company that trades greater than $100mn/day, facing intense Chinese competition gaining share with both local and foreign manufacturers, customers that are losing share, announced orders that do not seem to ever fully materialise into sales, weak organic sales growth, and overly optimistic estimates for 2H26 and 2027. The other short idea is an industrial company facing demographic headwinds, potential regulatory changes, increasing input costs, negative volume trends, potentially peak margins, and bullish forward estimates. Both stocks have short interest % of free float below 8%.

Developed Markets

It’s not a new cycle

According to Michael Howell, liquidity is still slowing, but policy makers lately intervened: Fed RRP + Treasury buybacks added US$600bn to money markets since October, temporarily reflating tech and crypto. Mike says this is band-aid support, not a new cycle. ‘True’ signals are ‘Risk Off’. The yield curve flattening is a strong ‘Risk Off’ signal: 10-2-year spreads and the SOFR-2y spread both point to tighter conditions ahead. Falling term premia = de risk now. China’s PBoC also just surprised to the downside: after months of liquidity injections that drove Yuan gold prices, late-April shows a sharp slowdown. Mike sees a near-term headwind for gold and global liquidity. The ‘speculation’ phase of investment cycle delivers volatile, unreliable returns. Michael is not buying this rally.

Beware the AI bubble

Does the AI bubble exist? Yes, according to Neil Newman. On average bubbles last five years, and this one largely started with ChatGPT, so we’re three years in. A small number of companies are driving disproportionate market returns and valuations being pushed to extreme levels. Monetisation is uncertain and there is a warning signal being sent to the market to reduce exposure. Avoid software-first models, which are most vulnerable to monetisation failure. Be cautious on investing in data centres – should demand disappoint, the residual asset is a specialised facility with little other use. Focus on the supply chain: infrastructure suppliers, semiconductors, equipment, power systems, benefit regardless of which applications succeed. Many of the companies that fall in this space are Japanese, which Neil believes will offer something of a defensive play.

UK: Everybody hurts

This week’s elections worked out very much as Niall Ferguson expected, with the governing Labour Party mauled, and the populist Reform UK party surging. Nationalist parties ended up in charge of Scotland and Wales. Niall sees the change as being more profound than mere shifts in the balance of party politics, with Britain breaking up into a patchwork of electoral backgrounds in a way that bodes ill for state structure and party coherence. Niall doesn’t see Starmer resigning soon but is certain he will not fight the next election. Badenoch will lead the Tories as her strong personality is beginning to get across to the public. Yet, the country is drifting towards a deeply uncertain election result in 2028/29 where nobody wins and nobody loses. It is hard to be anything but bearish about the country’s future.

UK: The next PM

It is unlikely the factions within the Parliamentary Labour Party (PLP) will be able to vote on one candidate, so the election would be decided by the Labour Party’s electoral college (1/3rd MPs, 1/3rd Trade Unions, 1/3rd party members) between the two candidates selected by the PLP. The main candidates include Wes Streeting; Angela Rayner, the most popular of the Soft Left candidates; Ed Miliband, who is the most likely candidate should Rayner decide not to run; and Andy Burnham, who would need to be elected as an MP to be able to run. The current paralysis is bad for the Gilt market due to the likelihood that it pushes borrowing needs up over the coming months due to higher gilt yields, energy subsidies and the defence budget black hole. The potential timeline for election of a new PM is between 2 and 4 months from today.

US: The case for pricing in hikes for the Fed

It’s not just the CPI/PPI prints that point to a case for hikes for the Fed, it is also the outright resilience in growth and the labour market that builds the case, claims Manoj Pradhan. Even if the Fed does not hike, Warsh and the rest of the FOMC will find it difficult to jawbone the markets against pricing in hikes. Manoj had gone Long EUR/USD since March 30th, which worked out far better than expected. However, the resilient US growth (g) and the fact Warsh and markets have kept the interest rate (r) lower than it should be, in addition to energy dependence likely damaging euro growth more than the US and the ECB pricing in over 60bps of hikes, points to a larger widening of g-r in the US relative to the euro area. This suggests a short EUR/USD position. Manoj also recommends adding paid Z7 to long 30y bonds to create a flattener. That the 5y has gone further above 4% than the 30y has above 5% is important to note.

US: Higher oil and rates, lower equities

David Woo argues that the market has got ahead of itself in reverting the move in 2y breakevens. His short-term market bias is: higher oil - lower equities - higher rates - neutral dollar. (1) Higher oil: Whether we will see resumed fighting or not, the two sides will not reach a deal anytime soon. Iran is not about to capitulate to US demands with support from Russia and China. (2) Lower equities: As the market starts to look beyond Q1 towards Q2, the high oil price will weigh more on growth expectations. European stocks are particularly at risk given their dependence on energy imports and lack of exposure to technology. (3) Higher rates: AI is inflationary in the short-term. The war is driving up prices from energy to crops. Fixed income investors are trying to ignore the war. (4) Neutral dollar: Trump wants to hit the EU with a 25% auto tariff, which the Supreme Court may prevent.

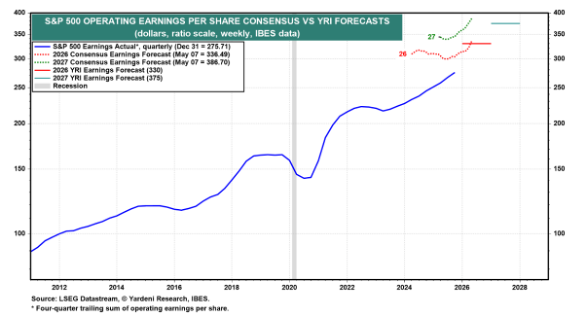

US S&P: Feeling good

Ed Yardeni is raising his year-end S&P 500 target from 7700 to 8250. He has never seen consensus earnings expectations rise so quickly for the current and coming years as they have in recent months. The result has been an earnings-led meltup in the stock market. Ed is raising his EPS estimates to $330 this year and $375 next year, while sticking with his forward P/E range of 18.0-22.0, resulting in a year-end range for the S&P 500 of 6750-8250. His key assumption is that the economy will remain resilient, and so will earnings. Ed is also raising his probability of a continuation of the Roaring 2020s to 80% from 60% simply by merging it with his meltup scenario (previously at 20%), since he believes that any meltdown will be a buying opportunity and won't trigger a recession or bear market similar to the 1999-2000 Tech Bubble and Tech Wreck.

Emerging Markets

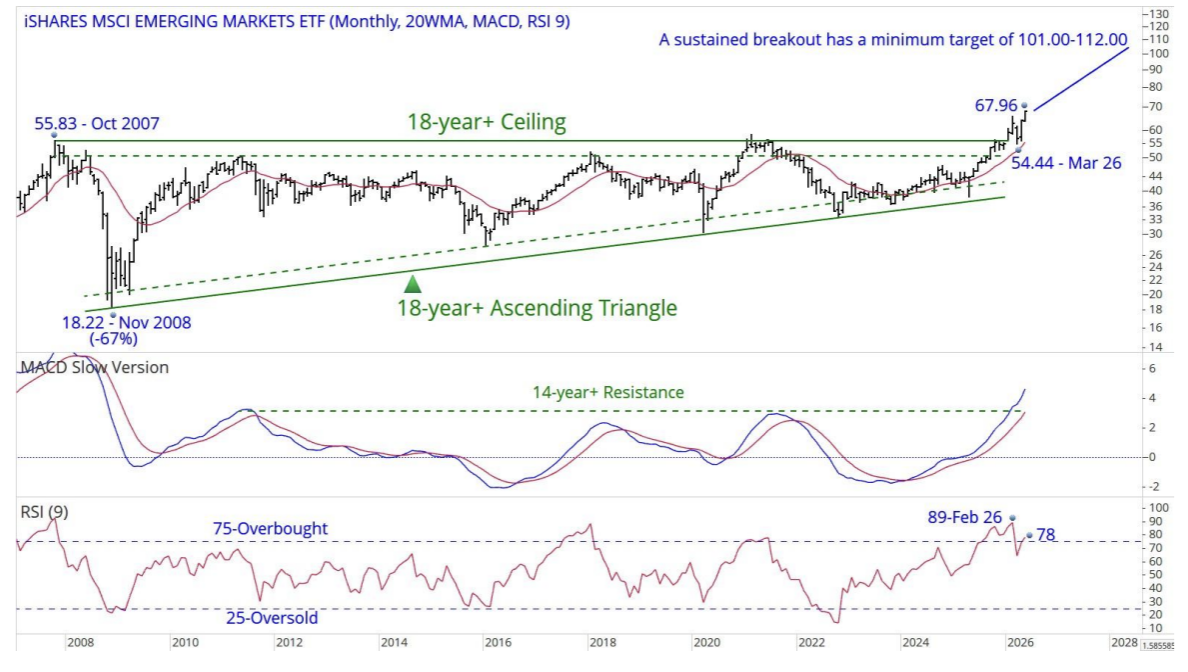

MSCI EM: The return of the Dodo

The iShares MSCI EM ETF (EEM US, last USD67.94) has successfully broken out from an eighteen-year-plus ascending triangle and is currently attempting to move beyond an eighteen-year-plus ceiling. While Chris Roberts points out that a sustained breakout above this resistance level suggests a minimum price target between USD101.00 and USD112.00, and the MACD indicates a significant improvement in momentum by clearing a fourteen-year resistance level, the nine-month RSI of 78 is approaching the very overbought threshold of 80. Consequently, it is prudent not to chase the current price; instead, the strategy is to wait for a setback toward the key support level at USD54.44 before considering a buy. Chris thinks he has found a dodo.

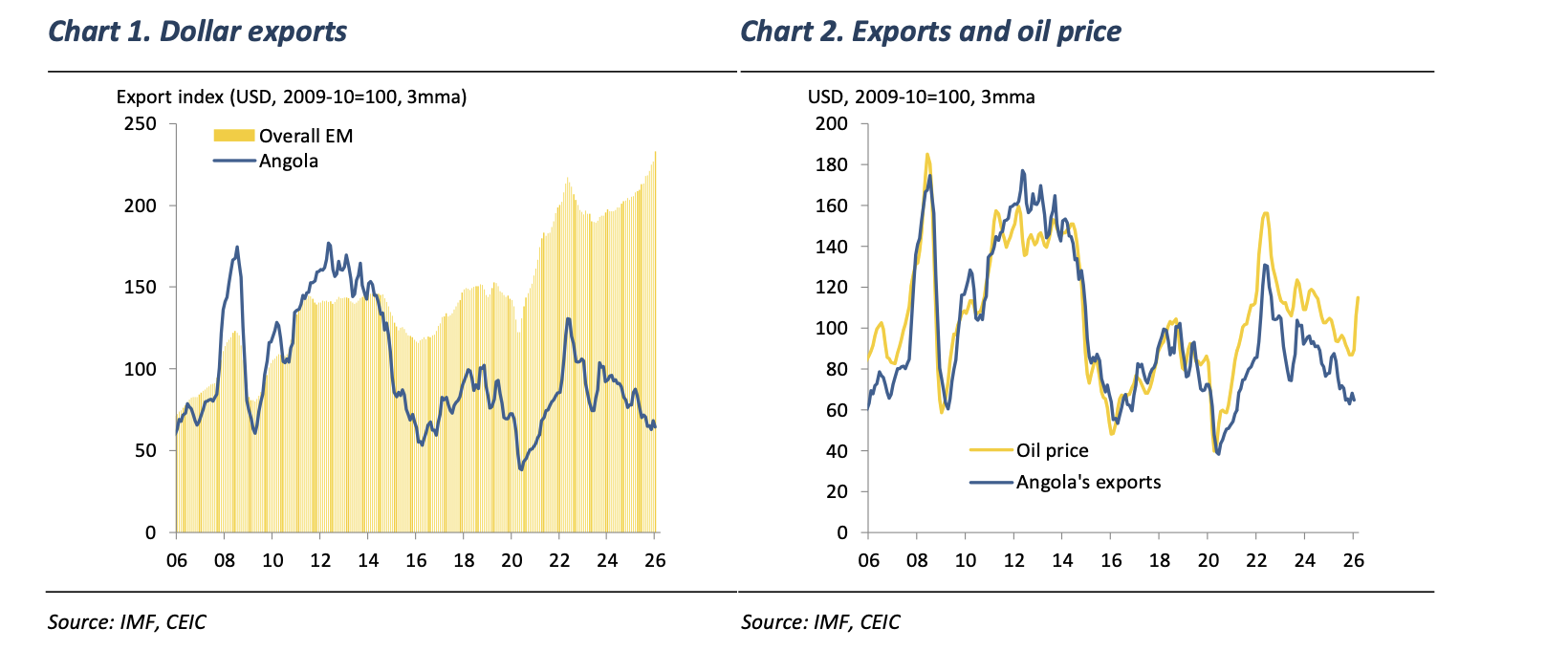

Angola could really use higher oil prices

In the first of a series of African frontier countries that Jonathan Anderson is covering in the coming weeks, he takes a look at Angola. The country did a strong job of stabilizing macro conditions in the aftermath of the late-2010s crisis, but over the past couple of years that stabilisation has been fraying, with worsening external and fiscal conditions on the back of lower crude oil prices and weak petroleum production. This leaves export earnings far below the rest of EM and well below what current oil prices would normally imply (see graph). The dismal picture may start to change soon with new energy projects that are expected to meaningfully increase oil and gas production in the near term. In the absence of this year's big oil shock Jonathan would have expected renewed FX pressures and rising spreads and yields ... and Angola's best hope is that dollar crude prices stay solidly in the triple digits.

What is driving the appreciation of the Brazilian Real?

Andrea Damico points out that the Brazilian currency’s behaviour has been noteworthy, as it has decoupled from the movement of the US dollar (DXY), as well as from other emerging market and commodity-currencies. Since the beginning of the year, the BRL had already been outperforming, but this relative strength intensified following the outbreak of the war. The Brazilian real is currently among the best-performing currencies in 2026 (around 10% appreciation), despite the country’s unresolved fiscal challenges and the presence of an important political risk event ahead (major elections), which typically increases volatility. As usual, no single factor explains this performance. Rather, it reflects a combination of elements. Andrea says high interest rate differentials, strong terms-of-trade gains, a diversified energy matrix, and relative distance from geopolitical conflicts - within a global context of portfolio diversification - have made the Brazilian currency particularly attractive.

Chile: Oil price shock and economic momentum

For now, Chile’s Central Bank appears to have opted to “look through” the shock associated with higher oil prices, given the economy’s loss of momentum, whilst delivering a clear signal that it stands ready to act should conditions warrant it. In particular, if a more persistent de-anchoring of inflation expectations were to emerge, especially towards 2027, by which point the temporary effects of higher fuel prices would largely fade and potential second round effects could begin to materialise. This was reflected in the explicit inclusion of a reference to the possibility of discussing a potential rate hike, which Enrico Vicentini and Igal Magendzo interpret more as a tactical communication tool than as a signal of an imminent tightening move. The objective appears to be reinforcing the credibility of the inflation commitment and preventing a premature deterioration in expectations.

Caution in Cote d’Ivoire

Cote d'Ivoire has done extremely well in the past couple of years on the back of explosive agricultural and metals export price gains, with an improving external and fiscal balance and falling sovereign dollar spreads. The medium-term outlook remains buoyant, with new oil and gas projects already coming online and significant further volume gains expected in the next four to five years. However, Jonathan Anderson points out that the base is still relatively low today as a share of total exports, which leaves near-term market sentiment highly geared to cocoa and gold prices. Cocoa markets have already come down hard, and while gold remains relatively buoyant Jonathan does worry about overvaluation relative to fundamentals. With high public external debt exposures compared to dollar earnings, this could be a source of volatility in the dollar sovereign market and a bit of caution is in order.

China’s asset revitalisation: An unanticipated growth boost?

In a 24-page special report, Dinny McMahon discusses the “asset revitalisation” measures that could help end the problem of local government austerity. Over the last few years, China’s local governments have significantly ramped up the amount of revenue they generate by leasing state assets and selling concessions – known as “revitalising” assets. This “asset revitalization” has become a major source of income for a handful of provinces, materially improving their fiscal conditions. Chongqing, the leader, funded 15.1% of provincial general expenditures last year from such activities, up from only 6.8% four years earlier. For China’s financially overstretched provinces, “asset revitalisation” is emerging as a much-needed new channel for expanding revenue. It stands to have a potentially transformative impact, creating an unprecedented opportunity for local authorities to repair their finances, and opening the door to an unanticipated boost in growth over the next couple of years.

Korea: The AI hardware stack

In January Niall Ferguson expressed his confidence in the momentum of Korean stocks expanding from memory makers to equipment, components and materials. Maintaining a long position in Korean firms across the AI hardware and infrastructure stack is supported by increasing demand from US hyperscalers and the ongoing structural upside of government-led capital market reforms. With the ruling Democratic Party expected to perform strongly in the upcoming June local elections, there is significant potential for renewed momentum in corporate and capital market reforms. While energy and logistics shocks remain potential tail risks, leading companies are currently buffered by robust inventory levels, significant purchasing power, and efficient recycling systems. Niall Ferguson views the easing cycle as complete and expects tightening to begin in H2/26. Still, he expects the rally to continue broadening through H2/26 and remains overweight Korean equities.

South Africa: Fiscal monitor

The fiscal year finished strong, with many of the key sources of upside and flexibility that Peter Montalto identified post-Budget materialising. Revenue was stronger despite weak growth. This left the primary surplus at 1.1% of GDP – in line with Peter’s view and above NT’s 0.9% Budget estimate. The key point is that the fiscal golden threads have been reinforced, if not strengthened, though this might well only translate into a slow ratings upgrade cycle. Peter sees the primary surplus at 1.5% of GDP in 2026/27, rising to 2.2% in the outer year. The usual caveats remain. Spending quality is still markedly lower than optimal. That the year-end fiscal strength reinforces the case for an S&P ratings upgrade later this year, in Peter’s view. NT is likely to maintain an (overly) conservative line however through the upcoming spending round to the MTBPS – focusing (perhaps too much) on geopolitical risks into the fiscus – again to be surprised to the upside later.

Thailand: A loser in the process

Six months ago, there were signs of a domestic recovery forming in Thailand as the domestic credit cycle had turned. Now, Andrew Hunt claims, the revival is doubtful with the war in the Gulf damaging Thailand’s terms of trade. Export growth has likely peaked and in the manufacturing sector there are flat output trends but rising inventories, which is never a good combination. Furthermore, the country could suffer from a decline in tourism numbers, and as fiscal policy has been expansionary, it may be difficult to provide a further stimulus following the war shock. Andrew suspects that the recent industrial survey results are likely correct regarding the outlook for economic growth, and if—and when—investor capital flows slacken, Thailand’s balance of payments will likely prove vulnerable, leaving the THB as a regional underperformer. Consequently, until such time as the tech sector bubble bursts, Thai equities will likely continue to underperform.

Commodities

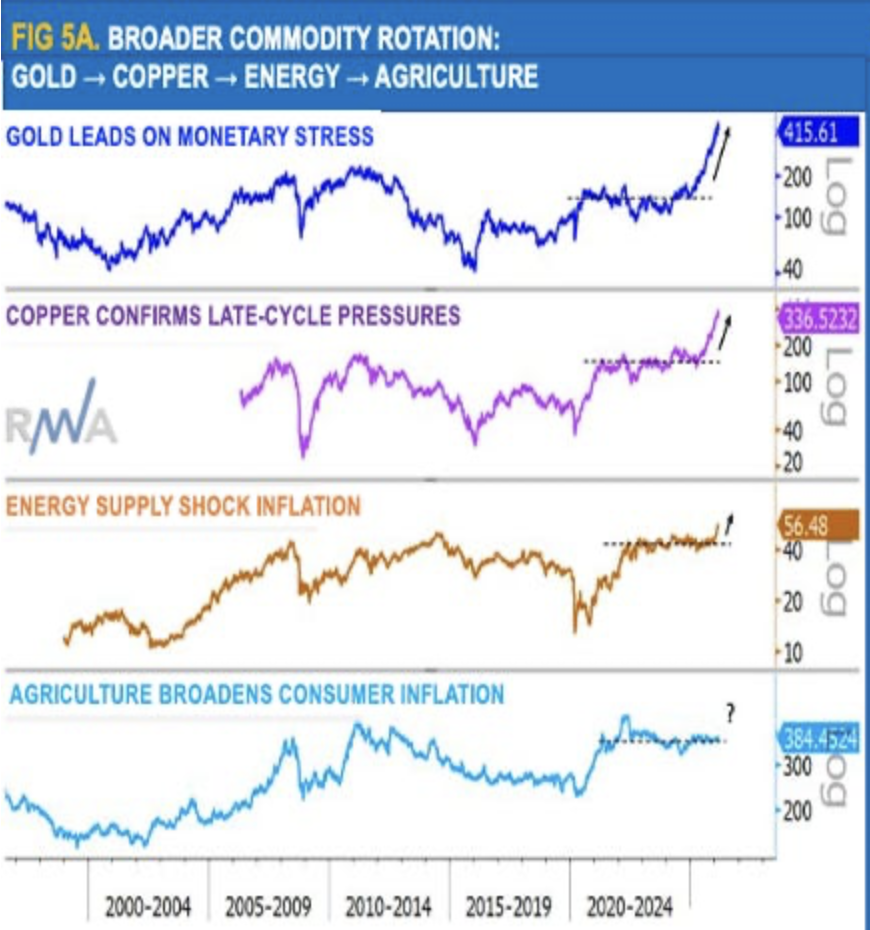

A commodity supercycle

Ron William’s latest market review continues to highlight the early stages of a developing commodity super-cycle, a theme that is already demonstrating clear outperformance fuelled by a resurgence in inflation and reinforced by second-order effects from the energy complex. What began as a concentrated move in precious metals, driven by debasement concerns, has progressively rotated into energy, reflecting supply-side constraints, and is now extending into agriculture. This broadening is significant: agriculture sits at the intersection of input costs and end-consumer prices, making it a key transmission channel for inflation, and accordingly, it remains top-ranked within Ron’s model. For the wider backdrop, Ron describes it as “shaken, but not yet stirred”: markets are absorbing a series of macro shocks – most notably inflationary pressures and the ongoing oil disruption – but these forces have not yet fully translated into a coherent, late-cycle regime.

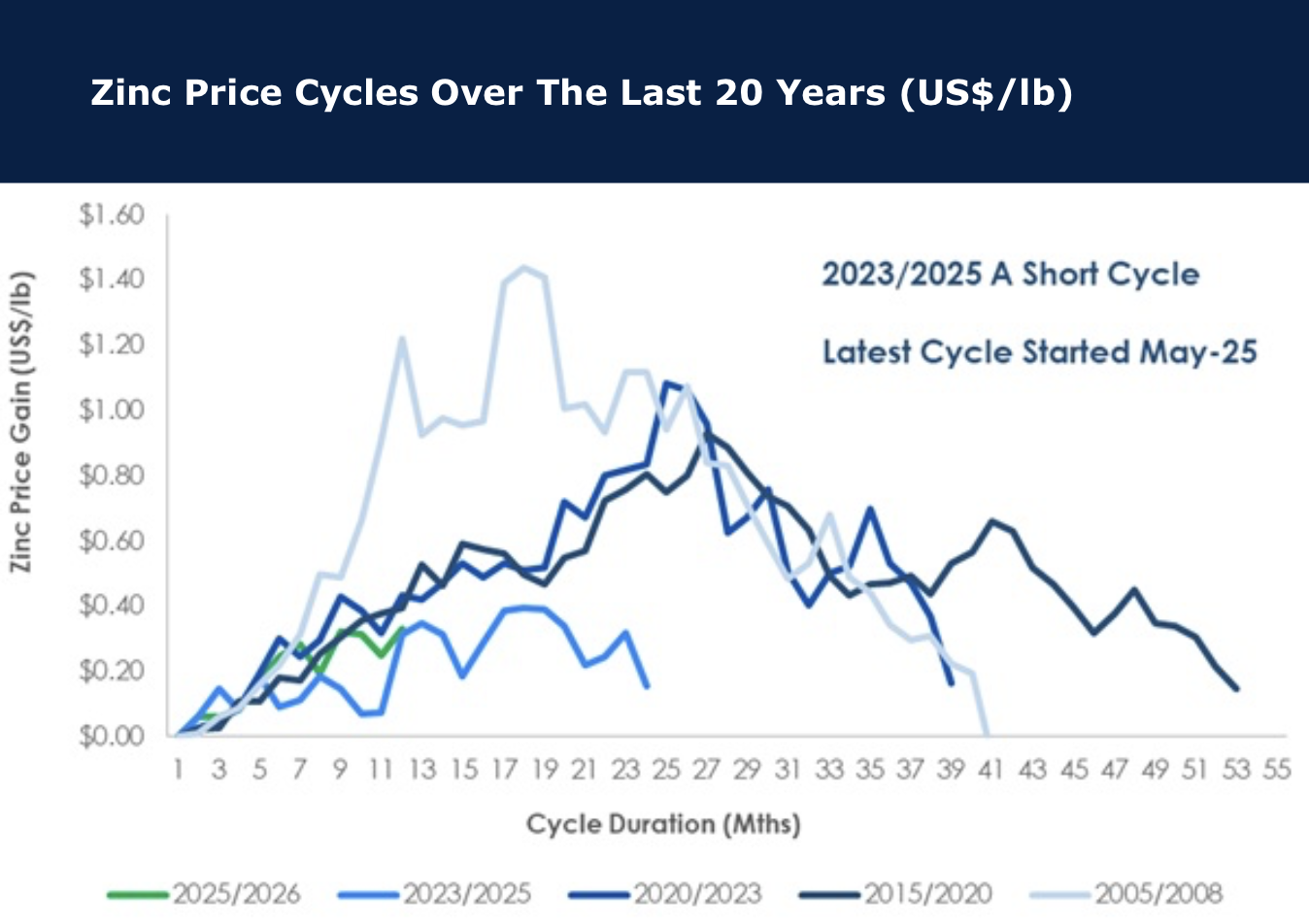

Zinc: Weak demand, weak supply

The zinc price is up ~12% in 2026 and as such has been broadly tracking the copper price momentum. However, David Radclyffe discusses some of the several recent setbacks impacting both the near- and mid-term outlook. These include recent production downgrades at both Grapenberg and Golden Grove, and the significant cost blowout / deferral of production at Hermosa. Good news has been sparse. Although global mine supply of zinc is estimated to exceed 12.5Mt in 2026, GMR’s coverage, representing a quarter of supply, is forecast to decline by ~16% this year implying downside risk to market expectations. Zinc price cycles tend to last 3-4 years with the last ending early, therefore the current cycle could extend for some time (see chart). David’s preferred choices include BOL and IVN based on value and metal exposure.

A crude awakening

Report by

BCA Research

BC

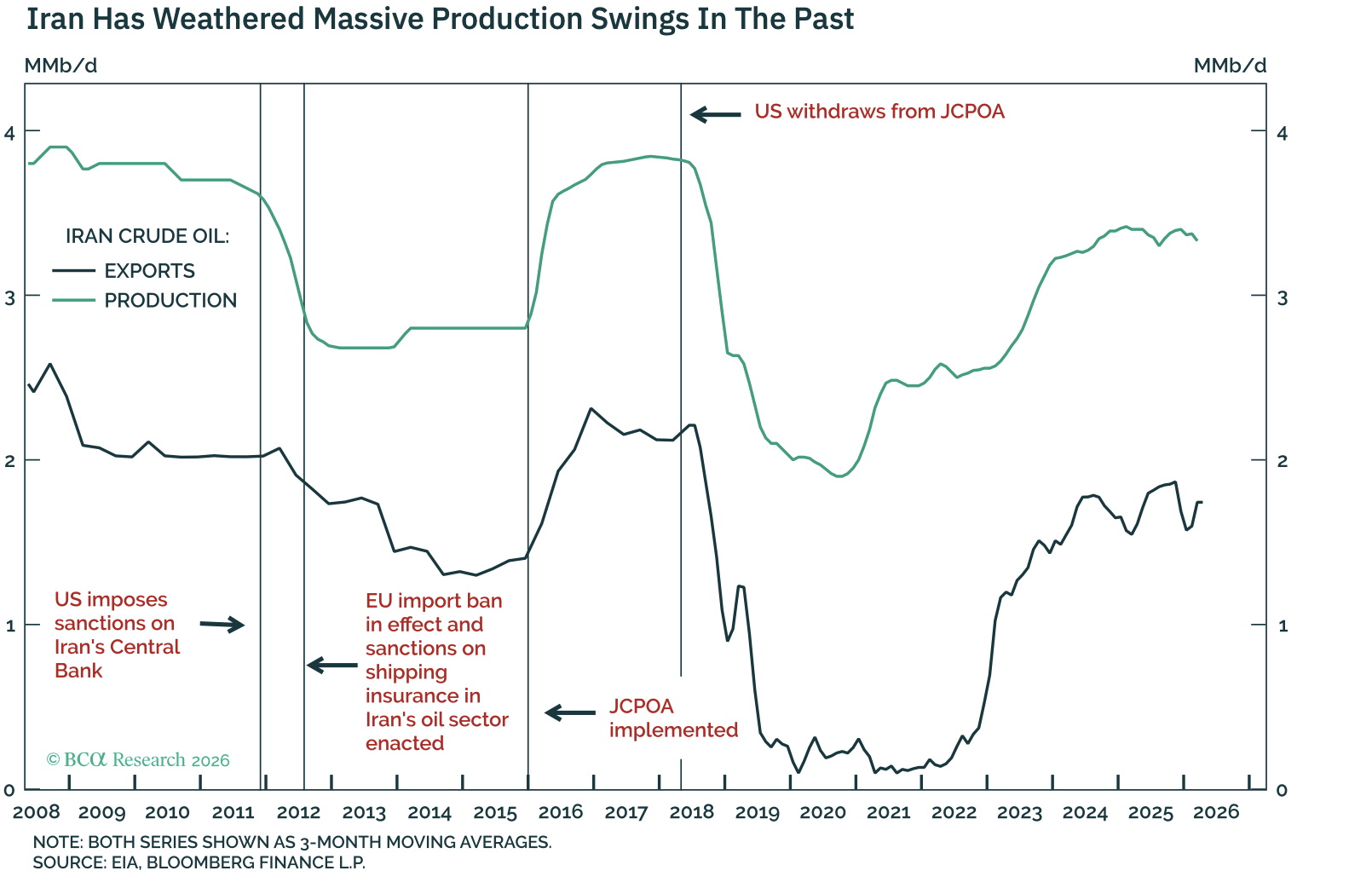

Crude oil prices are gyrating with headlines that are flip-flopping between the prospect of an imminent reopening of the Hormuz Strait and the risk of an escalation and a ceasefire breakdown. Oil markets are still trading on the hope of a deal that restores vessel traffic, and recent White House rhetoric about the US blockade pushing Iran to its pain threshold has created the false sense of a firm ceiling in crude prices. These hopes may be misplaced. Forced oil-production shut-ins would clearly damage Iran’s economy and create risks for future reservoir productivity. However, that pain alone is unlikely to compel Tehran to capitulate in negotiations with Washington. Unless the Strait reopens, the inventory buffer will weaken over time. Crucially, global observed oil inventories are on track to drop to a multi-year low by mid-year. This would likely compel crude prices to rise to new wartime highs.

Silver’s surprise breakout

In this presentation, Jeffrey Christian of CPM Group discusses the latest developments in gold, silver, platinum, and palladium markets, including renewed strength in silver prices, rising inflation pressures, and growing economic stress in India. Jeff explains why India’s government is now urging citizens to reduce gold purchases in order to protect foreign exchange reserves, and why Indian investors continue holding onto large amounts of physical gold despite the government’s concerns. The video concludes with a conversation about rising US inflation data, the Federal Reserve’s interest rate outlook, and strong silver prices. Jeff explains why precious metals may continue consolidating in the near-term while still remaining in a broader long-term bull market.

Click here to watch.