Europe

Defence Supply Chains: Hidden chokepoints, mispriced risk

The Iran conflict is not a regional event - it is a structural accelerant for the global Defence-Industrial Base. OMNISIGHT maps three converging chokepoints: China's gallium export controls (directly threatening F-35 radar integration timelines), Hormuz-driven sulphur disruptions cascading into propellant supply chains, and Qatar helium export risk affecting precision electronics. Combined, these create a butterfly chain that materially compresses production cadences for Tier-1 contractors in H2 2026 - a risk the market is currently underpricing. OMNISIGHT's institutional divergence analysis yields explicit ratings: Accumulate Lockheed Martin and BAE Systems; Hold RTX and Northrop Grumman; Reduce Rheinmetall, where a P/E of 90-100x leaves zero margin for delivery disappointment.

Investor Idea Event highlights several compelling Shorts

Revelare hosted a Buyside Event in London where short theses were shared for companies including: 1) Associated British Foods - Primark is caught in a competitive “no man’s land” and is being squeezed by Shein, Vinted and LEFTIES. 2) CSG - trades at peak earnings, driven by unsustainable, high-margin spot-market ammunition sales to Ukraine and its true revenue visibility is much lower than its headline backlog suggests. 3) IWG - the presenter questioned the company’s highly touted transition to a capital-light management / franchise model; sees the business as plagued by poor disclosure and aggressive accounting. 4) Vestas Wind Systems - utilities moving services in-house puts margins at risk and Chinese competition challenges a peak multiple.

Greek Equities: Adopting a more cautious stance

ResearchGreece revisits their stock picks and assesses the political outlook ahead of the next parliamentary elections. Macro conditions remain solid, with Q1 real GDP up 2.0% Y/Y, although inflation accelerated to 5.2% Y/Y in May (+0.0% M/M). With the Athens Index up +11% YTD, valuation multiples of non-banks in their universe have expanded to 13.2x P/E and 8.0x EV/EBITDA 2027, leaving more limited upside. Combined with polls pointing to a hung parliament, ResearchGreece is turning more cautious on Greek equities. Banks remain their preferred exposure (solid outlook - volume, rates, asset quality) as a leveraged Greek macro play. They prefer National Bank of Greece, Bank of Cyprus, Piraeus and Optima. Outside banks, they favour selective infrastructure, industrial and defensive names such as OTE, Titan, PPC and Piraeus Port over consumer stocks and cyclicals.

Communications

New Street remains cautious on the stock, arguing that Italy is not large enough to offset the group’s Swiss pressures or justify its 80% FY26 EV/FCF premium to the sector. Switzerland still accounts for 73% of value and faces multiple headwinds, including Salt’s share gains, weak service revenue growth, reliance on sub-brand pricing to defend KPIs and ongoing fibre-driven capex. While Italy is now nearly 30% of value, New Street does not expect a major pricing recovery, as Iliad Italy is already on track to earn a viable c.8% FCF ROIC without raising prices. Even lifting Italy 2030 OpFCF by 20% would only raise SCMN's 2025-2030 OpFCF CAGR from 4.5% to 6.0%, leaving the stock looking expensive in terms of value to growth.

Technology

TEMN’s acquisition of Additiv strengthens its position in wealth management, particularly in the fast-growing mass affluent segment, while adding a cloud-native orchestration platform that accelerates implementation times, enhances customer journey management and supports the company’s AI strategy. Additiv brings attractive growth characteristics, including strong DD ARR growth, 138% NRR and a blue-chip customer base. The acquisition also expands TEMN’s reach across Europe, the Middle East and Asia-Pacific, with opportunities to scale through its global channels. While the price has not been disclosed, GR20’s analysis suggests the deal is unlikely to be expensive, potentially valuing Additiv at c.4-5x revenue. TEMN plans a gradual integration approach, reflecting lessons learned from previous acquisitions and aiming to maximise long-term cross-selling and synergy opportunities while limiting execution risk.

North America

Stock Picking: #1 ranking for 60 straight months

New Constructs highlights a milestone 60 consecutive months of #1 rankings across multiple SumZero categories, underlining the consistency of their stock selection record. They are currently top in Consumer Discretionary and Industrials, alongside strong showings in Value, Large Cap, Micro Cap and Healthcare. New Constructs attributes this track record to their proprietary Robo-Analyst AI, which analyses financial statement footnotes and MD&A disclosures to calculate Core Earnings, a proven superior measure of earnings. Their performance evidence also extends beyond the rankings: since Jan 2021, New Constructs’ Focus List Long portfolio has outperformed the S&P 500 by 20%, while their Short portfolio has outperformed shorting the index by 60%. The three indices that they have developed with Bloomberg’s Index Licensing Group have also all outperformed the S&P 500 over the past five years.

Consumer Discretionary

Alex Barron believes the acquisition is an important signal for the US homebuilder sector, supporting his view that the bottom of the cycle is here and now is an opportune time to buy into the sector at great valuations. The deal values TMHC at 1.24x 2Q26 book value, 1.17x Alex’s 2026E book value and 12.9x 2026E EPS. His fair value estimate was $72/share. While Berkshire is unlikely to pursue an immediate acquisition spree, the deal opens the door for TMHC to become a larger consolidator over time. Alex also notes rising sector M&A, including Dream Finders attempted hostile bid for Beazer Homes, which he thinks would likely need to move closer to 0.8-0.9x book value to succeed.

Consumer Discretionary

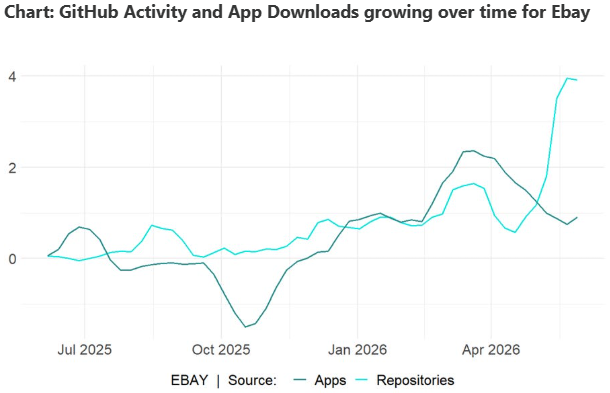

The company ranks in the top 20% of AnteData’s universe, reflecting a strong improvement in coding momentum during 2026. The signal is primarily being driven by rising App activity and exceptionally strong GitHub interest where developers are building pricing tools, arbitrage engines and inventory automations using EBAY as a pricing and transaction platform. AnteData sees the group’s focus on passion-driven goods, including auto parts, collectibles and luxury items, as increasingly important, with these categories now representing >30% of value traded. They believe EBAY can sustain c.8% annual revenue growth over the next 5 years, lifting sales from $11.5bn to $16bn and nearly doubling income to c.$4bn.

Alpha generating Healthcare Shorts

Healthcare

Bios Research publishes a new short idea that they believe is materially overvalued, with a m/cap in the $7-10bn range, significant ADV and ~50% downside potential. They also highlight additional Q2 and Q3 shorts (m/caps >$10bn) across biotech, healthcare services and medtech, alongside several M&A candidates and stocks that are attractive as a basket for investors looking to add exposure in what they believe is a new biotech bull cycle. So far in 2026, they have closed a long idea in Crinetics Pharmaceuticals for a ~59% gain and several shorts: ARS Pharmaceuticals (+46%), AbCellera Biologics (+43%), Summit Therapeutics (+42%), Butterfly Network (+34%) and TransMedics (+22%). Since inception in Feb 2012, Bios has published 194 short ideas with a c.70% absolute hit rate.

Industrials

ABM’s 2Q EPS beat was driven by stronger-than-expected revenue growth, with sales up 8.4% Y/Y and gains across all five segments for the fifth consecutive quarter. Technical Solutions, Aviation and Manufacturing & Distribution each grew by more than 15%, supported by organic gains and acquisitions. Sidoti’s FY26/FY27 EPS estimates of $4.03/$4.55 imply annual growth of 17.0% and 13.0%, respectively, while their FCF per share estimates of $4.25/$4.42 imply FCF yields of 10.0%/10.4%. ABM’s shares have traded at an average premium of 5% over the last 20 years to the S&P Small Cap 600 Index on a forward P/E basis but currently trade at a 34% discount. Sidoti maintains their Buy rating and $68 target, implying c.50% upside.

Industrials

MYST highlights a short thesis on ANDG, whose shares have risen from a $16 IPO price in Dec 25 to c.$37. The near-term catalyst is a major lockup expiry on 15th Jun, when c.99m shares become available vs. current outstanding shares of c.13m, creating a potential “meaningful amount of supply” as 300+ US partners look to monetise up to $4bn of stock. Fundamentally, ANDG relied heavily on price increases heading into the IPO, but customers already appear to be pushing back. AI is also seen eroding pricing power, as Big Four firms automate workflows and move down-market while AI-native start-ups compete at lower price points. Tax Receivable Agreements that distort reported cash flow are another underappreciated element of the short thesis. TP $25 (30% downside).

Industrials

EFN’s ~25% share price pullback over the past six months reflects concerns around lagging services revenue, moderating originations and potential AI disruption, but Veritas argues the fundamental impact is being overstated. Services revenue should recover as growth in Vehicles Under Management drives demand with a 12-15 month lag, while softer origination volumes have been offset by higher net financing revenue yields and growth in serviced-only VUMs. AI risk appears manageable, with the most exposed services representing only ~20% of annual delivery, while higher-touch offerings remain more defensible. Despite EFN’s stronger ROE profile, the stock trades below its five-year average P/E of 16.5x. They expect ROE to expand into the low-20% range and believe EFN's valuation multiple should re-rate as services revenue grows to the HSD range.

Materials

Hassan Ahmed is increasingly constructive on OLN, arguing that 1Q26 marked a positive inflection across all three segments after several years of estimate cuts and share price underperformance. Chlor-alkali fundamentals are tightening, helped by the cancellation of Chemours’ planned PCC chlorine project, limited North American capacity additions and Middle East-related disruptions, with an estimated 6-9% of global capacity currently shut. ECU pricing also appears to have stabilised after the post-2022 decline. Elsewhere, Epoxy returned to profitability after six consecutive quarterly losses, while Winchester is emerging from trough conditions as commercial ammunition stabilises and higher-visibility military exposure increases. With Beyond250 cost savings ramping, Hassan sees 2026 consensus expectations as undemanding and increases his 12-month TP to $36 (50% upside).

Real Estate

Craig Huber argues that the near-50% YTD fall in CSGP’s share price has created an attractive entry point, with investor concerns around AI competition and Homes.com losses now overdone. His 2026/2027 adjusted EPS estimates are above consensus at $1.40/$2.00, with revenue forecast to rise 18.0%/15.4% to $3.833bn/$4.424bn and adjusted EBITDA to reach $833.8m/$1.142bn. The group also has $1bn remaining on its share buyback programme (representing ~7.5% of current m/cap). The stock trades at 16.8x 2027 adjusted EPS or 13.9x EBITDA. If you exclude the Homes.com losses (where there is a lot of flexibility in the expense base; sees losses dropping to ~$300m this year), CSGP is trading at only 9.4x 2027 EBITDA. Information services is a sector that historically trades around 25x EBITDA, if not higher. Craig is an “aggressive buyer” at these levels with a conservative $50 12-month price target, implying ~50% upside.

Technology

NTNX's Q3 revenue and EPS beat was aided by exceptionally conservative guidance and accounting / cost factors that may not be sustainable. Management had guided Q3 revenue to just 6-8% growth despite maintaining a higher full-year growth outlook, creating a favourable setup for a beat, similar to Q2. BTN also highlights rapid growth in contract assets, which contributed around three days of sales to revenue recognition over the past two quarters, more than enough to explain the reported beats. Meanwhile, deferred revenue has been broadly flat for two years and continues to decline on a days-of-sales basis, while deferred commissions suggest weaker new customer acquisition. Margins also appear supported by low depreciation, declining capex, and reduced cash R&D and S&M intensity.

Technology

The market has been spooked by ORCL’s AI infrastructure spending, but Richard Windsor thinks the economics may be better than feared. Q4 revenues and adjusted EPS beat expectations, but shares fell after-hours as the company guided to $70bn of investment this fiscal year. The bond market is also flashing caution, with ORCL’s CDS widening to 198bp from 43bp in Sep 25. However, Richard estimates revenue per GW at $15.8bn, based on ORCL's incremental AI/cloud capacity and cloud revenue growth, far better than OpenAI and other neo-clouds are managing to produce, implying an 18% five-year IRR on a Grace Blackwell-based build. Strong AI investment returns could drive upside to medium-term EPS estimates, while the stock's 22x FY27 and 16.5x FY28 PER look reasonable against forecast EPS growth of 18% in FY27 and 35% in FY28.

Technology

Sales Pulse has received multiple reports from channel contacts indicating that NOW has initiated a significant workforce reduction this week. While the company has not yet publicly disclosed the scope of the restructuring, employee reports and internal discussions suggest ~2,500 employees may be impacted (8% of the workforce). The cuts have impacted multiple organisations, including sales (AEs and Solution Consultants), international operations and engineering teams. The move has surprised employees and observers given recent commentary from the CEO suggesting AI-driven productivity gains and natural attrition would manage headcount. Channel feedback has been notably negative, with one contact saying the process is “creating chaos internally” and that the company has become “so top heavy” it is struggling to execute.

Asia

Hang Seng on the launchpad

Erik@YWR argues that the Hang Seng’s sluggish start to 2026 masks a much more attractive setup, with the index described as a “coiled spring” after moving sideways for 15 years in hard-currency terms. He sees 35,000 as achievable, supported by improving fundamentals: based on YWR’s approximation of 89 constituents, earnings growth is expected to accelerate from a 6% CAGR over 2015-2025 to 11% over the next 3 years. Key drivers include 17% EPS CAGRs at Tencent and Alibaba, 6% growth from the major Chinese banks, oil-price support for energy names, 26% growth from BYD and CATL, and a recovery in property stocks. With earnings revisions turning positive, Hong Kong property prices recovering (mainland China prices stabilising) and the index on <10x 2028 earnings, Erik sees meaningful upside.

Jet-fuel panic turns contrarian opportunity

In the latest edition of David Scott’s A Strategist’s Diary, he argues that the jet-fuel panic has become an “ex-crisis”, with investors too quick to extrapolate higher fuel prices into a broader inflation problem. Instead, he sees demand destruction, airline fare discounting and rising supply from the US and China as evidence that the shock is already mean reverting. The investment implication is contrarian: sectors he would normally avoid, including airlines and state-owned Chinese oil/refining names, now offer compelling valuations. David highlights PetroChina and CNOOC as surprisingly well-run and still cheap despite strong prior returns, while also finding opportunities across global airlines including Spring Airlines, Delta, Ryanair, Eva Airways, IAG and IndiGo.

India Insider Buying Index: Methodology, historical trends and key insights

The Insider Buying Index serves as a useful indicator of market sentiment, given its strong negative correlation with major market indices. Historically, elevated readings in the index have coincided with periods of market stress and attractive valuation opportunities, while lower readings have generally been associated with stronger market conditions and reduced insider buying activity. Contact us below if you wish to understand more about the index.

Technology

Limited audit coverage raises questions over the reliability of its consolidated financials, particularly given that a large share of overseas operations is either unaudited or audited by other firms just as the company reports a turnaround. Capital allocation also remains a concern, with substantial net worth tied up in weak subsidiaries, a history of goodwill impairments and profitability heavily influenced by accounting judgements. Earnings quality warrants scrutiny, as recurring impairments, aggressive receivables provisioning assumptions, inventory write-downs and impairment reversals suggest reported profits remain highly dependent on management estimates and recoverability assumptions.

Developed Markets

The AI juggernaut is accelerating

James Aitken believes that society remains in the foothills of our collective AI journey. As

powerful as it has been, as many questions as we have about return on capital employed, it seems to him that the AI juggernaut is accelerating. James isn’t trying to take advantage by catching the Dell, Micron, SK Hynix, Samsung Electronics or related AI pianos. (Although he points out that if Jensen Huang builds out his desired ecosystem, Nvidia is not that expensive). What he’d like to buy during this turbulence is more Shell, then BHP, RIO, Glencore and Tivan. In other words, more of the ‘picks and shovels’ winners of the AI boom and winners of national resilience agenda with dependable management, and excellent execution. That includes Bloom Energy, too, which James believes will soon jump from small to megacap, missing out midcap.

Deal delusion masks an enduring energy crisis

Michael Belkin points out that markets remain obsessed with a peace accord that remains tantalisingly out of reach. While Trump claims Iran is begging for a deal, the other side has no intention to surrender control of Hormuz or hand over enriched uranium. Michael believes this blockades liquefied natural gas exports to Taiwan, turning off their power and disrupting Nvidia output. This highlights the Achilles heel of the artificial intelligence boom, where agentic model costs are turning ugly. Tech and semiconductors are now following the precious metals pattern of a major spike top. Sector rotation has hit a major inflection point, driving institutional flows out of growth into value. To capture this phase shift, sell Nasdaq QQQ, the MAGS ETF, and short TBonds via TLT, whilst establishing long allocations in crude oil, the DXY dollar index, and the XLE energy sector ETF.

UK credit expansion set for summer pause

Darren Winder points out that while UK household bank deposits grew at a steady 4% over recent months, a near-term deceleration in credit expansion looms. Driven by an upward revision to market interest rate expectations, quoted mortgage rates jumped from 4% to 5% in April, signalling an abrupt tightening cycle that will soften mortgage approvals and housing transactions in the period immediately ahead. This near-term moderation is expected to pull down mortgage lending growth from its recent 3.25% pace. However, the fundamental evidence reveals significant underlying consumer resilience; household bank deposits expanded by £75 billion in the 12 months to April, propelled by a 15% annual surge in cash ISAs to £475 billion. Winder expects this mortgage slowdown to be transitory, with lending growth projected to pick up as interest rate pressures ease during the second half of the year and into 2027.

Eurozone growth risks mispriced amid hawkish consensus

The Variant Perception team examine the outlook for the Eurozone as inflation leading indicators and breadth remain elevated well above pre-Covid levels. Whilst rising service price surveys put pressure on the European Central Bank to remain hawkish to anchor inflation expectations, matching the market pricing of at least three interest rate hikes over the next year introduces substantial downside growth risks. According to the team, current market dynamics replicate the post-GFC period by overstating inflation fears and underestimating growth destruction. This structural misalignment occurs at a time when Eurozone macroeconomic breadth vs the rest of the G10 remains weak. With the trend component of the firm's tactical outlook model turning decisively negative, the underlying economic setup points toward a sharp growth capitulation rather than a sustained tightening cycle. The team express their bearish view on European growth by selling rallies in the euro.

What’s driving bonds, war or tokenmaxxing?

David believes it is a combination of both higher oil prices and the AI rally that has driven up real yields. The release of Claude Mythos reignited the AI trade, strengthening the view that AI will unleash a productivity boom in the economy, which may be one reason why long-term real yields have repriced higher. Another factor is the positive wealth effect associated with the AI rally, supposedly meaning that the Fed can focus more on the upside inflation risks posed by higher oil prices than on the downside risks to growth. However, David is sceptical of the rally continuing; frontier model capabilities are plateauing and companies are now imposing stricter budgets on AI token usage. The growth path Anthropic recently experienced could be unsustainable and the AI rally might be becoming even more narrow. It’s too early to buy bonds, but a steepener is starting to make sense again.

US Biotech capital controls face long road to enactment

The Capital Alpha team review the Biotech Investment National Security Act (BINSA) and notes that despite hawkish bipartisan appetite for Chinese outbound restrictions, the bill faces less than 20% odds of passing this session. Introduced by House Select Committee on China Chair Representative John Moolenaar, BINSA aims to expand the newly enacted COINS Act framework by subjecting American pharmaceutical licensing deals, joint ventures, and equity investments to strict Treasury review. However, institutional friction regarding unintended disruptions to pharma supply chains, drug discovery innovation, and clinical development costs will stall swift legislative traction. With insufficient congressional bandwidth prior to the midterms, the absolute policy bottleneck prevents inclusion in immediate appropriations packages. Whilst parallel momentum remains possible, a structural phase shift in biotech capital controls is unlikely to materialise until the fiscal year 2027 FDA user fee reauthorisation cycle or a delayed 2028 legislative window.

The US labour market ain’t so bad

The strength of May’s employment report surprised many, debunking the notion that the US labour market is mired in “low-hire, low-fire” stagnation. But it confirmed the views of Ed Yardeni and Elias Griepentrog. They expect demand for labour to continue to improve and supply to remain structurally constrained. This should keep unemployment low, boost productivity, and sustain wage growth. That shouldn’t cause an inflationary wage-price spiral over the long term; the AI-sparked productivity boom should keep unit labour costs in check, in line with Ed’s longer-term Roaring 2020s hypothesis. But Ed says that near-term risks remain: the AI buildout is inflationary, and higher wage growth could add price pressure before offsetting productivity gains materialise.

US: The populist backlash against AI

Report by

BCA Research

BC

Matt Gertken and Marko Papic say that the populist backlash against AI could result in bipartisan regulation in 2027, but is especially likely to prompt tax hikes from 2029. Public criticism of the new technology is growing and politicians in the US and abroad are proposing measures such as AI regulation, taxation, redistribution, and restrictions on data centres. Job displacement is the core concern, with opposition to AI strongest in service-oriented economies where workers fear automation. Americans increasingly view AI as developing too quickly, oppose data-centre construction in their backyard, and are becoming less optimistic about the benefits of technology, particularly among younger generations. The investment risk is political, not technological: a recession, AI-driven mass layoffs, inflation, or a major AI-related accident could mobilise voters and lead to aggressive regulation or higher taxes on technology firms as early as next year – and especially after the 2028 election.

US: Bond volatility matters most

Ahead of the next FOMC in mid-June, Michael Howell questions the importance of the rate-setting ritual. He argues that the bond market, not the US Fed, is the main force shaping the economy and equity markets. More specifically, what matters most is not bond yields but rather bond volatility. Investors should be watching the MOVE index and closely examine the US Treasury’s actions in the bond market, because they may now matter more than the policy rate itself. Michael argues that the Fed has been sidelined, losing much of its traditional influence over financial conditions. Still, it plays an important financial stability role in smoothing funding operations and specifically maintaining harmony in the crucial repo / collateral markets. Also, he notes that lower policy rates are not always stimulative. Because the private sector is a net creditor to the government, rate cuts can reduce interest income to bondholders and potentially dampen spending.

US: Trump tariff V2

Beacon Research points out that the Trump administration is working to rebuild its reciprocal tariff regime through Section 301, amid ongoing legal battles over refunds and its use of Section 122. As expected, when the Supreme Court ruled that President Trump’s use of the IEEPA to impose sweeping reciprocal tariffs was illegal, the White House has set about to remake the global tariffs regime. Now the project is nearing completion, with the Trump administration on track to complete its most expansive Section 301 investigation by July 24th, when the Section 122 duties will expire without congressional renewal, which is highly doubtful. These duties are expected to be supplemented by additional Section 301 duties on sixteen countries targeted in an investigation focused on excess capacity. According to Beacon Research, these measures will be on the strongest legal footing to date, with past challenges to Section 301 tariffs largely unsuccessful, giving them the best chance of surviving judicial scrutiny.

Hong Kong: Hang Seng breakout

Chris Roberts examines the HSI’s (24,962) confirmed breakout from the 27-month rectangle/base, as it targets an advance to 35,000+, a new all-time high. The weekly chart uptrend high remains at 27,382, set in Oct 25. The index has now been ranging for 8 months. A weekly close above 27,800 would be viewed as a breakout from the current range, targeting a move to around 31,000. If such a breakout occurs, Chris will likely add a long HSI position. He is still long the iShares MSCI China ETF and the Shanghai Composite Index. RSI (last 42) continues to support the uptrend view, with lows being set in the 40-50 Neutral Zone since the 2024 low.

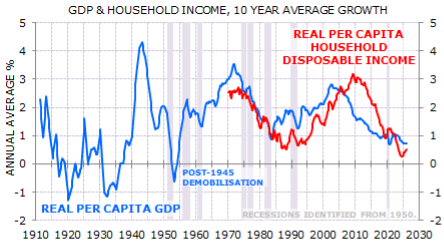

Australia heads back to the doldrums

According to Gerard Minack, Australia is growing at 2.5% – not particularly strong with working-age population rising by 1.75% – but now seems set to slow. Productivity growth remains poor, so 2.5% growth created inflation pressure that the RBA had to respond to. Gerard says the economy will head back to the doldrums of a low per capita expansion. Weaker growth is a factor behind falling EPS forecasts and the prospect of modest equity returns. Australia has had a poor decade. Average per capita GDP growth was the lowest since the 1930s (excluding the post-1945 demobilisation). What matters for consumers is disposable income, not GDP. Per capita disposable income growth was lower than GDP, payback for the mining boom boost received through the prior decade. Australia’s biggest structural economic problem is poor productivity. Poor productivity reflects low capex relative to fast-growing population, so there is little capital deepening. No capital deepening means no productivity growth.

Japan: Yen under pressure, but data is encouraging

Graham Turner says that the prospect of a rate hike at the FOMC meeting in June casts a harsh spotlight on the Bank of Japan: the BoJ will meet earlier next week, and unless it agrees to tighten policy too, the yen is likely to plumb new lows against the US$. For the Bank of Japan, there is no obvious pressure to hike, as inflation has been well-behaved. The y/y for the Nationwide CPI eased to 1.38% in April. The CPI excluding food, alcohol & energy dipped to 1.06% y/y. Real wages are rising sharply, in part, because of the drop of core inflation as well as fuel subsidies. The labour market in Japan is tight. The unemployment rate fell to 2.5% in April. Total employment jumped to 68.76m, a new high, despite a shrinking population. These are encouraging trends that bode well for Japan’s response to an ageing population, particularly against the backdrop of high government debt.

Emerging Markets

Chile: Opposing forces expected to keep policy rate steady

The macroeconomic backdrop continues to become more challenging for the Central Bank of Chile. While, on the domestic front, May’s inflation print continued to support the Board’s baseline scenario, the external backdrop has introduced a new source of uncertainty. The US economy continues to surprise with its strength and resilience, raising the possibility that the Fed may adopt a somewhat more hawkish stance than previously anticipated. Against this backdrop, Igal Magendzo’s base case (of 2026 being a transition year between economic cycles with the Monetary Policy Rate likely remaining unchanged) continues to gain credibility. He says that there are opposing forces acting on monetary policy in both directions, which should help keep the policy rate in a state of equilibrium throughout the remainder of the year.

China: Externally driven inflation

Paul Cavey says that the rise in China’s producer price index (PPI) that continued in May is of macro significance: it is pushing up industrial sector earnings, and the GDP deflator will likely turn positive in Q2. But it is difficult to find signs of domestically generated inflation that would suggest a real upturn in the economy. PPI inflation did ease MoM in May, but the headline YoY rate climbed to 3.9%, the highest since mid-2022. As would be expected, the driver continues to be upstream commodity prices. The rise in energy prices is also being reflected in CPI, with a 20% YoY rise in fuel costs pushing up the transport and communication component by 5% in May. However, headline CPI was steady at 1.2% YoY. One reason was that food prices in the CPI continued to fall last month. In addition, services inflation remains weak. That reflects the state of domestic demand, though in that regard it is perhaps notable that services inflation isn't deteriorating further.

Cuba looks down the barrel

The maximum-pressure strategy to collapse the Cuban regime has escalated into a framework to impose secondary sanctions, but the Castro regime refuses to concede to US hardline conditions. Niall Ferguson believes that the Trump administration prefers to use a maximum-pressure economic strategy to force Havana into surrender. He is starting to see more of the signals he identified in January as precursors of a military attack, such as diplomatic escalation and military build-up; military escalation has become more likely, conditional on the Cuban regime’s refusal to make timely concessions. Diplomatic efforts also ramped up as CIA Director John Ratcliffe flew openly to Havana last week to meet with Cuban intelligence and deliver an ultimatum. Niall Ferguson thinks the probability of a deal has increased from 60% to 70% as the Cuban regime stares down the barrel of the gun.

Korea: The strange case of the KRW and AI

Despite the AI boom, the KRW has been weak this year as the KIC has been funding a significant part of the US AI blowout, yet many point to foreign equities as the reason despite modest flows. Many of the issued government bonds were snapped up by foreign investors, but Andrew suspects many of these may in fact be offshore subsidiaries of Samsung et al. This would explain why, despite the boom in chip revenues, the corporate sector has not seen a significant increase in its cash holdings. With the KRW now very weak, domestic inflation rising, and sentiment towards the AI theme having “a moment”, Andrew Hunt suspects that the KIC will slow its financing activities, cutting funding to the US AI complex just as a wall of paper is scheduled to arrive.

How much of a problem is the Polish budget?

Jonathan Anderson points out that broad macro conditions are still very favourable for Poland. On the external front, Poland continues to gain European market share with outperforming exports, which in turn keeps the external economy in balance and the zloty stable. The domestic recovery is also on track, with strong credit growth, durable spending and corporate earnings momentum at home. The equity market has arguably already outrun the underlying story, but this is true for the rest of the emerging European region as well; the one imbalance that stands out in Poland is the dramatic widening of the fiscal deficit, driven by higher defence and social spending. This can't last over the long run, but with moderate overall debt levels and low external exposures there's still not a big impact on macro variables. The only market where budget imbalances are already showing up is sovereign dollar/euro bonds, where favourable yield gaps are all but disappearing.

Tanzania: Stuck on stocks, better on flows

Buoyed by higher gold export prices and tourism revenues, Tanzania has made its way to broad external balance on the "basic" BOP front, which in turn has allowed it to stabilize the shilling and lower interest rates. Jonathan Anderson points out that the main risks here are higher oil import costs and a potential reversal in metals markets, but for the time being the country is holding the line. This still leaves Tanzania with a very high stock of external sovereign liabilities relative to dollar earnings, i.e., the country is effectively "stuck" on a long-term treadmill of IMF and other multilateral refinancing support and restructuring of bilateral obligations. The only good news here is that market participation in Tanzania's dollar debt burden is close to zero, which reduces pressure on rates and funding flows during the adjustment process.

Commodities

Oil: US administration is trapped in a box canyon

With the crucial November midterm elections looming, James Burdass says the US administration is trapped in a box canyon between its non-interventionist base and a highly resilient adversary. The logistical reality is that the Strait of Hormuz remains heavily bottlenecked for unescorted commercial traffic, forcing complex rerouting and soaring insurance premiums. Compounding this immediate logistical strain is a completely stalled exit strategy. When a nuclear-capable administration faces a hard domestic deadline against a resilient adversary, the velocity of forced escalation is almost always underestimated by passive models. For sophisticated allocators, maintaining structural exposure to tactical hard-asset strategies is no longer just a standard inflation play. It has become an essential defensive volatility shield against an impending, politically driven escalation that the back end of the curve—as noted by the traders the team engaged with last week—is entirely unprepared to handle. James considers that difficulties with normalisation have moved from tail risks towards being a base case.

Ripples of risk-off

Murray Gunn wrote about the dichotomy between the fortunes of Ripple, the cryptocurrency company, and XRP, its token. He pointed out the booming company that has been securing lucrative and high-profile contracts, yet the price of XRP has been declining. Another Bitcoin bust beckons, as the iconic cryptocurrency was declining in the next wave of its ongoing bear market since its peak last year. Bitcoin also sports at least one head and shoulders top pattern which could give it even more bearish implications. Murray pondered whether the crypto slump was a subtle sign that risk appetite was waning, and it might now be finally feeding through into the stock market with the S&P 500 down over 3% last week. Don’t be surprised to hear and read about people attempting to “buy the dip.” And when the stock market struggles to recover, as he suspects, expect increasing panic to ensue.

Copper mines winners and losers

With multi-billion-dollar capex programmes failing to generate meaningful volume growth, a severe structural phase shift is unfolding across global copper mining operations. The GMR team notes that despite producers injecting an estimated $35bn of real capital into 17 legacy assets over the last five years, net output expanded by a mere 151kt, proving that nominal growth capex is behaving entirely as sustaining expenditure. Fundamental evidence shows major operational friction; Chuquicamata’s underground transition has starved its mill of feed, forcing the treatment of stockpiled ore, while Collahuasi suffers from declining sulphide head grades and metallurgical recoveries dropping from 87% to 73%. Consequently, the global supply curve remains highly dependent on a tiny cohort of recent greenfield assets like Kamoa-Kakula and Quellaveco. GMR maintains that the long-term industry thematic of capital-intensive battle to merely preserve baseline primary copper production continues completely unabated.

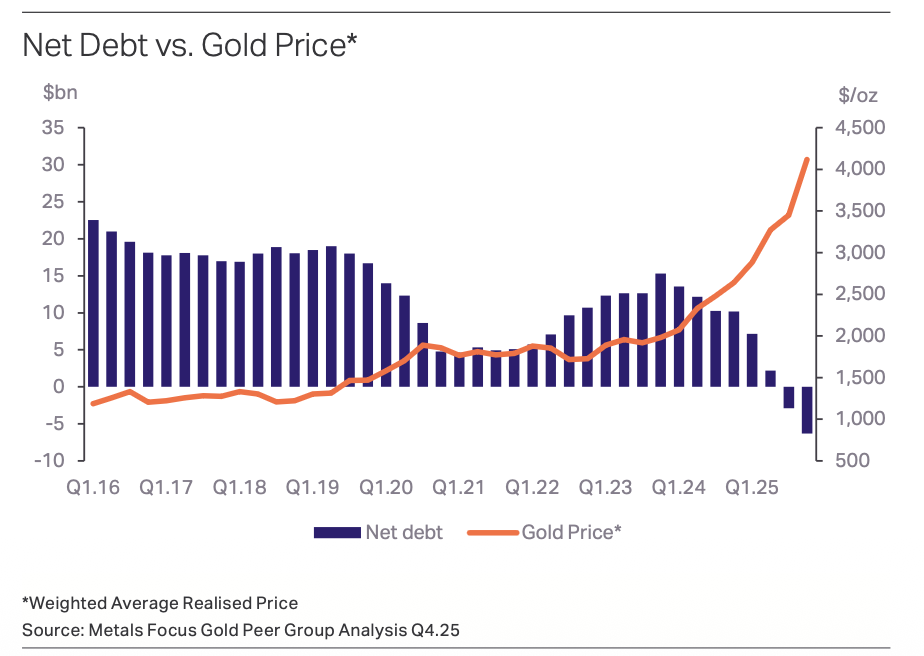

What are gold miners doing with all of their cash?

Driven by surging realised gold prices, the group of gold miners tracked by Metals Focus generated a massive $25.8bn in free cash flow in 2025. Rather than repeating the reckless expansion of past commodity cycles, management teams are demonstrating strict capital discipline. A significant portion is channelled into balance-sheet repair, transforming a $15.3bn net debt position into a $6.3bn net cash surplus. Reinvestment back into operations has driven total capital expenditure to $682/oz, alongside increased exploration spending to maintain a stable twenty-year reserve life. Host governments took a 33% effective tax rate, whilst quarterly dividends surged threefold to $3.0bn. Despite this historic financial strength, sector valuations remain subdued at a 5.4x EV/EBITDA multiple, offering a compelling opportunity for equity investors to buy these highly disciplined, cash-rich producers.