Europe

EU Tech Sovereignty: Risk for European OEMs

Richard Windsor sees the EU’s technology sovereignty push as another example of regulation that could hurt the companies it is intended to protect. While restrictions on non-European technology providers appear supportive for local champions such as SAP, Siemens, Nebius and Mistral, he warns that limiting access to superior US technology risks making European products less competitive. Autos are the clearest pressure point: European OEMs already struggle with in-car digital user experience, while Apple CarPlay and Android Auto remain popular with consumers, and US-linked chip platforms from Nvidia, Qualcomm and Mobileye have won key infotainment and ADAS sockets on product merit. Given the pushback from industry, Richard expects that these proposals will never come into force and so if the EU can move quickly to fix the AI Act, there is still time for Europe to become relevant in AI.

Consumer Staples

Three Non-Executive Directors recently purchased a combined £646,000 of shares at an equivalent price of c.£42 per share, with some transactions conducted through ADRs. Notably, each purchase was their first. Ruby Lu, a Non-Executive since Nov 2021, acquired £374,392 of shares, despite never having bought shares at Yum China, where she has served as a Non-Executive Director since 2016. Judith McKenna, a Non-Executive since Mar 2024, purchased £186,000, having made no purchases while an executive at Walmart or since joining Delta Air Lines as a Non-Executive in 2025. Benoit Potier, a Non-Executive since Jan 2025, acquired £87,000. Smart Insider views the cluster of buys as bullish and ranks the stock +1, their highest rating.

Financials

AIR argues CMBN’s improving efficiency profile is underappreciated, with AI integration expected to accelerate cost reduction and drive the cost/income ratio below 40% in 2026 and 35% in 2027. With no further Swiss rate cuts expected this year and loss provisions forecast to remain <1%, CMBN is probably the most efficient bank in Europe on a risk/reward adjusted basis. The group’s 100% Swiss exposure, no controlling shareholder and attractive risk profile also make it an ideal target for foreign financial institutions seeking CHF and Swiss consumer market exposure. TP CHF130 (35% upside).

Utilities

Iron Blue initiates coverage with a score of 31/60, which is top decile and fertile grounds for shorting. Key factors include the company’s Asset Rotation Plan and other Construction percentage-of-completion and off balance sheet SPV accounting, expansion of balance sheet contract assets, gap between PPE capex and the depreciation charge, aged debtor book, elevated gross cash position, and associates related party transactions. Governance red flags include the non-independent chair, internal appointees to CEO/CFO roles, unusual incentive arrangements and elevated non-audit fees. They also note the 2027 regulatory risk to MTLN’s important Gazprom relationship.

North America

3 (non-AI) trillion-dollar trends

As we hit the near term financial and physical limits on AI spend, Erik@YWR shifts his focus to 3 non-AI themes with trillion-dollar potential. First, a prolonged state of insecurity in the Persian Gulf could force a structural re-architecture of global energy supply, benefiting alternative routes, LNG, refining, chemicals and infrastructure plays outside the Middle East (e.g. Turkey, Nigeria, US). Second, higher inflation and interest rates could extend the outperformance of DM banks, which remain cheap, under-owned and increasingly important in funding data-centre capex and new energy infrastructure. Third, China, which nobody owns and is at an earnings inflection point. Erik also wonders if Chinese construction companies could benefit from the rearchitecting of the world energy supply or Hong Kong as a financing hub for new infrastructure.

Bear’s Den Idea Forum

Despite the market hitting all-time highs amid rapid sector rotation and narrow breadth, Bear’s Den remains one of MYST’s best-performing Forums - their previous event (March) produced an impressive ~83% positive hit rate with a record average alpha of ~19%. Stocks featured at their June Forum included:

CoreWeave (CRWV US) - Vendor-financed neo-cloud faces real bankruptcy risk. TP $50 (50% downside).

Ingredion (INGR US) - Secular short with high leverage + negative volume trends. TP $65 (35% downside).

Logitech (LOGI US) - AI-driven headcount cuts to negatively impact demand for core Peripherals business. TP $75 (25% downside).

McDonald’s (MCD US) - Convenience moat deteriorating as drive-thru share collapses. TP $199 (25% downside).

US Cable / Telcos (incl. AT&T, T-Mobile, Verizon) - Fibre to flip from asset to liability as Starlink + Amazon satellite buildout expands.

Communications

Fox's $22bn acquisition of Roku represents a profound structural shift in the US television market. While investors view this as a content synergy play, Fox is actually constructing a vertically integrated "walled garden". The severely underappreciated angle is the impending disintermediation of independent ad-tech. By locking down Roku’s proprietary Automatic Content Recognition (ACR) data, Fox will trigger a supply path squeeze that devastates exposed SSPs like Magnite. Simultaneously, to defend Roku's OS market share against Google and Amazon, Fox will be forced to aggressively inflate OS pre-installation subsidies. This creates an "Allied Industrial Tax" where the true, hidden beneficiaries of this transaction are Asian OEM hardware manufacturers like TCL and Hisense.

Consumer Discretionary

BROS has assembled a C-suite with the functional depth required for its next phase of growth. CEO Christine Barone has built a leadership bench well matched to the current mandate, combining expertise in capital allocation, site development, retail technology, digital marketing and operational execution to support 185+ annual store openings, improve throughput and scale the brand nationally. The principal risk is cultural rather than operational, with a faster shift towards a more process-driven organisation potentially weakening the founder-led “Dutch Luv” culture that differentiates the brand. Nevertheless, Paragon believes this risk is manageable if management can preserve the customer-facing culture while building a more disciplined, scalable operating model capable of supporting stronger unit economics and a more durable growth algorithm. Their analysis includes diligence memos / interviews on Barone, CFO Guenser, CMO Davilla, CDO Cahoe, CT&IO Krishnababu and CSO Somers.

TJX: The competitive landscape for HomeGoods in BTC

Consumer Discretionary

Competition in the back-to-college market is broad and intensifying, with Target the most aggressive omnichannel player, Bed Bath & Beyond potentially making a big comeback through The Container Store (Scott Mushkin has already visited the new stores) and Williams Sonoma expanding online via Dormify. Against this backdrop, Scott thinks TJX is right to avoid college-focused bricks-and-mortar formats and instead focus on generating interesting design ideas and leveraging social media influencers. HomeGoods appears best used as a “first stop” for unique or deeply discounted branded items before consumers round out their BTC basket at other retailers. Even outside BTC, Scott’s research suggests HomeGoods’ high-brand-quality-at-low-price proposition remains an attractive derivative play on a housing recovery.

Consumer Staples

Strong Q4 results validate Kathleen Wong's positive thesis, with a record US fuel margin and improving merchandise trends reinforcing two key points: fuel margin strength is more structural than cyclical and the company’s supply-chain playbook is starting to translate into C-store performance. ATD reported a US fuel margin of 52.44cpg, well above the industry average of 35.6cpg and Casey's latest 46.9cpg. An integrated fuel supply chain, logistics reach, sourcing optionality and market positioning enable the company to capture margin opportunities when oil markets are volatile or constrained, consistent with the framework Kathleen previously highlighted, in which she argued that concerns re. higher oil prices compressing ATD's fuel margins were overstated. Merchandise also improved, with US SSS up 3.4%, marking the fourth consecutive quarter of positive SSS and the best result in three years. Foodservice SSS grew >5% and US merchandise gross margin increased 50bps to 34.4%.

Financials

AMP is one of the leading players in global wealth management, an industry with underlying growth characteristics rivalling the fastest-growing segments of the tech sector. Household wealth has quadrupled over the past 35 years and investable assets have increased 1,600%, while an ongoing evolution in investing customers’ tastes and preferences continues to tilt the financial services industry landscape in favour of wealth management vs. asset management entities. AMP’s wealth management revenues and adjusted operating profits have grown at LDD annual rates in recent years, with margins holding around 30%. EPS has also compounded strongly, helped by buybacks that have reduced shares outstanding by 23% since 2020. Despite this, the stock trades on just 10.1x 2026E EPS, below both its own history and peers.

Financials

Although further declines in crypto trading activity have weighed on estimates and the valuation, Rosenblatt increasingly sees the malaise as a buying opportunity. In just the last 6 months, COIN has launched 18 new products and features that have the potential to transform the company from a pure-play crypto platform to a powerful financial services "super app". While the market remains sceptical given the multiple challenges associated with this ambitious diversification strategy, Rosenblatt views the near-immediate success of its prediction markets launch as a very encouraging sign. With an increasingly diversified revenue base and rising ARPU, they believe COIN has the potential to trade more like Robinhood as the market gains confidence in the new trajectory. TP $240 (65% upside).

Healthcare

Tom Tobin sees THC as exposed to a broader consumption cliff across US healthcare, as one of the most generous periods for medical demand gives way to one of the worst. Higher costs are pressuring payors, providers, employers and consumers at the same time, with employers likely to shift more costs to employees and payors protecting MLRs through network pressure and utilisation management. Trends across the healthcare industry continue to decelerate visible across acute care, physician offices, diagnostic imaging, physical therapy and ASCs, all key contributors to THC. Policy headwinds under the Trump Administration could further reduce the insured population, with Treasury outlays suggesting ACA enrolment may be down >50% in May 26, significantly worse than expectations. While THC looks optically cheap at 6.5x EV/EBITDA, Tom sees risk of another leg down on a Q2 miss and lower FY26 guidance.

Industrials

Arete initiates coverage with a Buy rating and DCF-based $401 2027E price target, reflecting the scale of opportunities in Space, Connectivity and AI. Starship’s path to full reusability could reduce launch costs to below $100/kg, while cooling and power appear resolved for Orbital Data Centres, with cost parity vs. terrestrial expected in the early 2030s. SSO launch cadence is likely the key scaling challenge. In Connectivity, Starlink has reached 12m customers and is adding c.800k/month, with Arete expecting a 2026E exit run-rate of c.$20bn revenue and c.$13bn EBITDA, helped by V3 satellites opening a larger suburban broadband opportunity. Mobile looks like a multi-billion-dollar long-term opportunity, but its inferior link budget and limited spectrum leave little room to disrupt terrestrial wireless. In AI, Anthropic and Google add $26bn p.a. in run-rate terrestrial AI infrastructure sales, while Orbital Compute could reach 29GW by 2035E and generate >$1trn of sales by 2037E.

Technology

BTN remains sceptical re. the sustainability of NTAP’s margin improvements and believes the credit risk associated with the company’s receivables portfolio is greater than many investors appreciate. DSOs have exceeded 60 days in 3 of the past 5 quarters, among the highest levels in recent years. Arrow Electronics and TD SYNNEX together account for c.25-40% of receivables, with both having stretched working capital positions, and their payables and debt obligations significantly exceed expected collections. Margin expansion has been supported by fully depreciated equipment, which BTN estimates contributes c.350bps to margins and c.$1.25 of annual adjusted EPS. Lower R&D and S&M spend also helped the Q4 beat, but these savings may be difficult to sustain as NTAP pursues AI-related customers. Deferred revenue continues to decline as a percentage of sales and the company has discontinued warranty disclosures in its latest 10-K.

Asia

Is Starlink a threat to telcos in Japan, Korea & Singapore?

Communications

Physical and commercial constraints mean Starlink is unlikely to be more than a niche operator across Developed Asia for the foreseeable future. Low proportion of profit from Broadband also limits any likely impact on the relevant telcos P&L. Rather than seeing the Developed Asian telcos as likely to suffer from a “second wave” of Starlink-related selling, New Street thinks they are more likely to benefit from internal switching within global telcos as investors figure out how much better placed they are than telcos in the US or Europe. Ultimately telcos work when dividends are rising and New Street sees dividend growth across the board for this group, coupled with ongoing share buybacks. Top picks: Singtel, KT and SoftBank Corp.

Financials

ADCB is AlphaMena’s top pick in UAE banks, supported by superior asset quality, best-in-class efficiency and a more domestic balance sheet, which provides a natural hedge against the FX and rate volatility affecting more internationally exposed peers such as Emirates NBD and QNB (Turkey). Compared with First Abu Dhabi Bank, ADCB has less reliance on market-related revenues, supporting better earnings visibility, while its exposure to stressed sectors is significantly lower than Dubai Islamic Bank, particularly in aviation. 2Q26 results are the key near-term catalyst, with potential upside from a strong quarter and a NIM guidance upgrade in a higher-for-longer rate environment. AlphaMena sees attractive risk/reward, with geopolitical risk largely priced in and de-escalation a potential re-rating trigger.

AIDC liquid cooling enters a scaling cycle

Industrials

Liquid cooling is moving from an efficiency upgrade to a functional requirement for high-power AI data-centre racks. The cleaner domestic China exposure is not necessarily the system-level liquid-cooling vendors, many of which have limited direct exposure to NVIDIA's core ecosystem. Instead, Horizon Insights sees more visible order conversion in the precision-machining equipment used to produce liquid-cooling quick-disconnect connectors. UQD/QD connector expansion is driving demand for Swiss-type lathes, where Tsugami China appears to have c.60% share in China’s connector-processing equipment market. Channel checks also point to >2,700 liquid-cooling-related orders in Jan-May 26 and potential 2026 shipments of c.6,000 units, implying c.RMB2.7bn of potential revenue at c.RMB450k per machine.

Industrials

An under-covered Japanese small-cap (Asymmetric has been the only one highlighting this stock over the last few years) benefiting from ageing domestic industrial assets, decarbonisation investment, renewed focus on energy security and a shrinking pool of nationwide plant engineering providers (according to management, only Raiznext and Sankyu now have nationwide petrochemical coverage, together controlling c.50-60% of the market). The company has beaten its initial operating profit guidance for each of the past five years, including FY25 OP of ¥14.7bn, 36% above its initial target. Although FY26 guidance implies a 12% decline to ¥13bn, Asymmetric sees this as conservative given management tends to forecast only on projects already in hand. The shares trade on c.13x P/E with a 5.2% yield, while ENEOS’s 28.7% stake creates potential corporate-action optionality.

Materials

Lucror sees the proposed CopperTech Metals IPO as credit positive and another step towards improving VRL’s portfolio transparency, liquidity and funding flexibility. The proceeds will mainly be used for growth capex at Konkola Copper Mines and to reduce pressure on VRL holdco liquidity. VRL is also undertaking a broader refinancing, which should extend maturities, lower funding costs and strengthen liquidity; S&P has affirmed VRL at BB and assigned BB- to the proposed senior notes (Lucror generally agrees, except for the notching down of the senior unsecured rating). Lucror also views Twin Star’s recent 1.7% VEDL block sale as modestly credit positive. Their credit bias remains Positive, supported by projected record earnings. They recommend buying the VEDLN 9.85% ’33s at 109.5/8.0%/4.9Y, while holding the rest of the curve.

Developed Markets

The AI infrastructure boom is no bubble

Report by

Musha Research

MU

As massive AI infrastructure investments accelerate, Ryoji Musha examines whether the current stock market boom represents a dangerous bubble or a historic structural revolution. Capital expenditures by GAFAM are nearly doubling to $703-735 billion in 2026, boosting US GDP growth by 0.5-1% within a 2.0% expansion track. Ryoji notes that this epoch resembles 1995-96 rather than the dot-com crash, with valuations supported by high profitability and a Mag7 P/E ratio under 26x. Technological progress and cost reductions driven by AI scaling laws are pacing significantly ahead of Moore's Law, triggering a price revolution that isolates the traditional economy from the hyper-productive AI sphere. With the Trump administration deploying deregulation and expansionary fiscal policies to channel global capital into infrastructure assets, Ryoji believes equity gains can endure for years. Institutional participants should position for this structural divergence as elevated short-term interest rates persist and the government yield curve continues flattening.

The Great British Peso

Now that U.K. Prime Minister Keir Starmer has said he will resign, it paves the way for, in all likelihood, Andy Burnham to become the next PM. Murray Gunn points out that in the nineteen years leading up to 2016, the U.K. had three PMs. In the ten years since 2016 there will now have been six PMs. What happened in 2016? Oh yes, that was when Britain became the only country in history to impose economic sanctions on itself by voting to leave the European Union, the planet’s largest economic trading bloc. Since then, social mood has continued to trend negatively, economic growth has been anaemic and the far-right has risen in the political zeitgeist. Sterling still looks like it is appreciating versus the US dollar, but the chart of EUR-GBP shows that it could be set for years of depreciation after completing a triangle from 2008 to 2024. Do not be surprised if developments on these islands become even more dramatic over the next decade.

UK: Hello Mr Burnham

Andrew Hunt notes that the likely new UK Prime Minister has little actual experience in government. Mr Burnham may be in a rush to introduce change, and this urgency is not always optimal… Andrew says that the key objectives for a Burnham government must be to lift productivity growth and a new “policy paper” suggests that his government will attempt to achieve this via heavier levels of public investment and nationalisation. However, the anticipated supply of Gilts to the non-bank sector was expected to be the equivalent of around 8% of GDP, or more. Andrew Hunt doubts that Camp Burnham’s assumption that subsidising living costs as a way of controlling inflation will prove popular in the debt markets. If global bond market sentiment is buoyant, then the Burnham Regime may avoid a Gilt / GBP crisis, but if global markets are in an unfriendly mood, then Andrew Hunt expects lower bond prices and a notably weaker GBP over the medium term (and higher actual inflation).

UK: Brexit, 10 years on

In an extensive report examining the paradox of Brexit a decade on, Niall Ferguson observes that leaving the European Union has fallen short of revitalising the economy or curbing immigration. Non-EU trade agreements fail to offset the single market exit, which permanently lowered trade volumes and left business investment significantly depressed. However, Niall believes that Britain's primary drags remain homegrown, driven by an inefficient NHS, rigid planning laws, and severe energy grid fragility exposed by recent shocks. While the likely next Prime Minister Andy Burnham targets incremental alignment on agri-trade and emissions, Brussels will demand politically costly concessions. Consequently, structural domestic blockages and demographic change will continue to impede fiscal consolidation. With public finances failing to recover from the pandemic, persistent energy-induced inflation risks and deep political uncertainty mean the structural rise in borrowing costs is unlikely to reverse, maintaining long-term upward pressure on 30Y Gilt yields.

Canada inflation spike provides no cause for hikes

According to data in Screenshot 2026-06-25 at 12.47.26.png, Carl Weinberg observes that headline CPI-based inflation metrics printed higher than expected, if only by a squinch. Technically, headline CPI at 3.2% is pretty far above the 2% midpoint of the inflation target range. However, traditional core CPI was just 1.6% higher than last year, while the Bank’s preferred measures of core inflation, CPI-median and CPI-trim, averaged just 2.05% between them. Sticking to his guns, Carl notes that the BoC did not raise rates at its last meeting because it didn’t have to. Petrol prices were behind the acceleration of headline CPI, but there is little sign those cost increases are bleeding through into core prices. The economy has plenty of slack to absorb the energy price increases, unlike the US where output is camped at the edge of the production possibility frontier. This result gives the BoC no cause to contemplate rate hikes now.

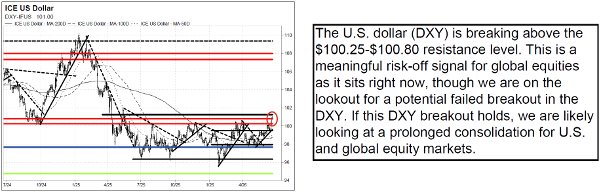

US DXY breakout: A cause for concern?

Ross LaDuke remains bullish on the S&P 500 (SPX), Nasdaq 100 (QQQ), and Russell 2000 (IWM). The IWM has begun to lead, hitting new all-time highs on 22nd June, while SPX and QQQ consolidate below their early-June highs. This continues to suggest to Ross that the rally is broadening out. A new wrinkle is that the USD is showing signs of breaking out. The DXY is marginally above $100.25-$100.80 resistance on concerns that the Warsh-led Fed's first move could be to raise rates, and Ross believes a DXY breakout would be a significant risk-off signal for global equities. With that said, he does not yet see it as a decisive breakout with acceptance above $100.80, and he is on the lookout for a failed breakout. Still, as long as SPX support at 7259-7294, IWM support at $270.50-$271, and QQQ support at $695 and $681-$686 continue to hold, Ross views pullbacks as buying opportunities.

US: Record high spread between inventory holding costs and levels

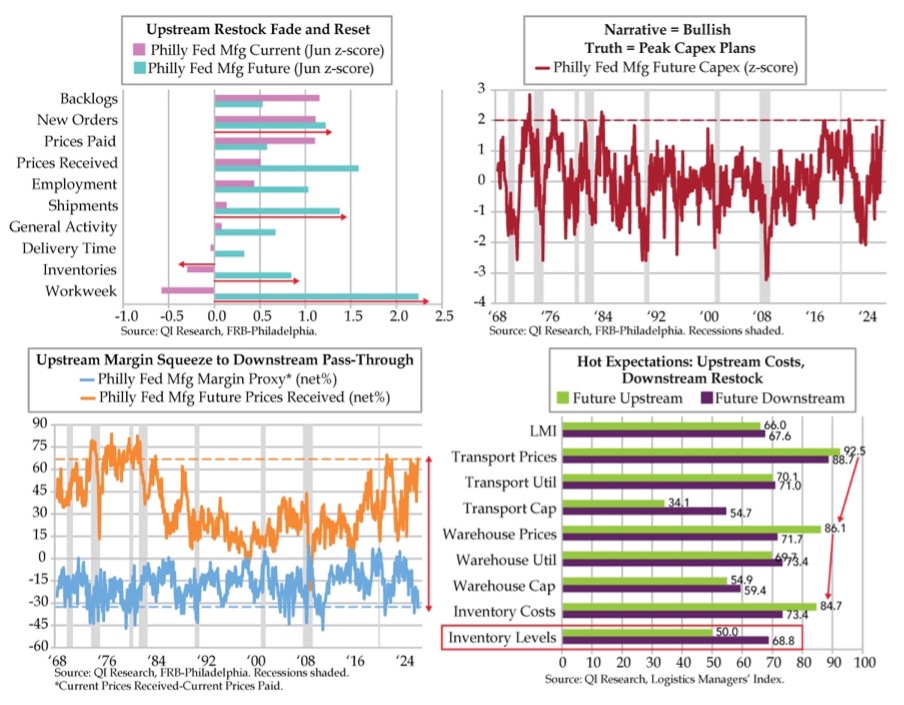

The Philly Fed flagged a continuation in high input costs that has factory players in the Chemicals hub keen to pass through higher prices. Danielle DiMartino Booth points out that the red flag raised, however, is that historical spikes of this week’s magnitude have been followed by nasty bouts of payback. Indeed, a margin squeeze proxy has sunk so deep into negativity, it sits in the 93rd percentile of history to 1968. The latest Logistics Managers Index corroborates the unsustainability of the current environment as aggregate logistics costs have risen to the highest since March 2022. Upstream firms plan to ratchet back inventories, which are sporting prohibitively high holding costs, in the hopes that Downstream sees demand rise sufficiently to restock and absorb the higher prices they’ve had to bear. While the transportation sector will continue to benefit, the risks of a pullback grow with every margin point that’s bled from US firms’ bottom lines.

US S&P futures funding squeeze opens arbitrage plays

James Aitken points out that the volatility of the implied cost of financing a long S&P futures position has started to spike. The demand to finance long equity futures positions is intense across market participants, with asset managers’ net-long futures positions extremely high while hedge funds and systematic strategies are also heavily exposed. This year’s stock rally mechanically increased how much financing is needed for exposure, compounded by leveraged ETFs using synthetic exposure through futures, swaps, options or other derivatives. While a squeeze like this creates headaches for money managers that need leverage, James notes it offers an opportunity for investors sitting on cash piles. Higher equity-funding costs effectively boost the returns available to those willing to lend balance sheet to the market. A typical cash-and-carry trade strategy involves purchasing stocks in the S&P 500 and selling futures against them to pocket the financing spread, which is exactly what some of his largest clients are doing.

US: Why the Fed will cut

The MOU signed by Iran and the US triggered massive selling in oil, but David Woo disagrees that this means the agreement will prove durable. Iran thinks it can push Trump to make more concessions and is seeking to apply pressure by claiming Israel is breaking the ceasefire. David believes the IRGC is directing Hezbollah to violate the ceasefire to provoke Israel. Aragchi suggested progress on Lebanon has been made, but the IRGC will seek to maintain pressure as it chases tolls on Hormuz, causing more volatility. The most immediate consequence is likely a short squeeze in oil as technical support at the 200d meets traders deciding not to hold risk over the summer. This will also pressure the AI trade, where the underperformance of companies providing capex in the US and China suggests a significant repricing is near, forcing the Fed to cut.

Emerging Markets

Asia FX correlation breaks down completely

Jon Turek examines the historic breakdown in correlation across Asia FX, where major regional currencies are trading independently due to idiosyncratic variables. While USDJPY prints fresh highs above 161, USDCNH continues making new lows as the PBOC allows the currency to reflect China's massive trade surplus and expands its internationalisation via a new RMB Repo Facility for FIMA. Meanwhile, Korea's currency remains remarkably weak in real effective exchange rate terms despite a current account surplus near 10% of GDP and a stock market up over 100% year-to-date. Jon notes that Korean policymakers are earnestly trying to reverse this weakness through exporter conversion discussions and an impending Bank of Korea tightening cycle under Governor Hyun Song Shin. Because Japan's authorities only seek to cap yen weakness, Jon exploits this asymmetry by adding a short JPY basket against CNH and KRW at 23.80 CNHJPY and 9.52 JPYKRW.

How big is China’s financial system?

In a series of reports, Jonathan Anderson explores the true size of China’s financial economy. The Chinese financial system set a new all-time high in 2025, with gross assets reaching 554% of GDP. Unlike in 2024, the main marginal driver was the banking system rather than non-bank financial institutions (NBFIs). China's "big six" banks accounted for the largest single share of the increase, despite a contraction in outstanding household loans. Concurrently, NBFI growth slowed noticeably from 2024's surge, narrowing to just the insurance and trust segments. Securities, fund management, and finance companies all went into reverse. Furthermore, the trust sector's marked deceleration suggests the shift toward passive, fee-light structures may be plateauing. Deposit formation recovered slightly but stayed well below the 2022–23 pace. Paired with sustained loan growth, the system loan-to-deposit ratio held steady, signalling a slower, grinding tightening of funding constraints rather than an abrupt deleveraging shock.

Colombia: Ambitious promises face governing realities

Right-wing populist Abelardo de la Espriella won the presidential run-off, defeating Ivan Cepeda, the candidate of the governing left-wing Historic Pact (PH) coalition. In the face of a potentially obstructionist opposition, a key question will be how De la Espriella builds and maintains governability. He spurned traditional parties during the campaign and will need to negotiate with transactional parties in Congress. This could prove challenging for a politically inexperienced president, who promised transformative “miracle” solutions. If the courts or other oversight bodies frustrate De la Espriella’s ambitions, frictions with institutional checks and balances could emerge. On the policy front, a sharp change of direction is likely once De la Espriella takes office on 7 August. His immediate economic priority will be to restore fiscal credibility. A similarly abrupt shift is likely in security policy: De la Espriella will abandon Petro's "Total Peace" strategy in favour of a more coercive approach designed to recover state authority.

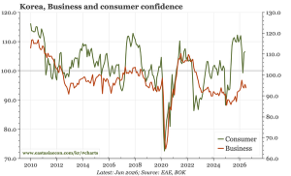

Korea: Not quite K-shaped

Paul Cavey points out that June business confidence was weaker than expected, with the July exporter outlook score ticking down and showing no real strength in the electronics sector. While sentiment among big companies looks bullish and exporter sentiment remains comfortably above the long-term average, domestic sentiment continues to stagnate due to construction drags and depressed small firms. Growth is undeniably uneven, but consumer confidence remains strong, reflecting strong asset markets, an equity price surge, and corporate profitability boosting worker bonuses. Paul notes that while the Bank of Korea is sensitive to disparities across sectors, bank officials state this is not an issue for monetary policy. Governor Shin argued that developments in growth, inflation, and financial stability point relatively clearly in one direction. With the energy shock receding quickly following a sharp decline in global oil prices, softening input and output prices mean the bank will become more optimistic about growth.

Mexico: Breaking free

The iShares MSCI Mexico ETF (EWW US, USD77.33) traded at a new ATH of USD81.65 in Feb, up 76% from the Dec 2024 low. At 81.65, the ETF was 6.3% above the now 19-year Ceiling, that extends from 65.00-76.80. A sustained breakout above the Multi-Year Ceiling would have a minimum target of USD130.00+ (a doubling of the low end of the Resistance Zone). In recent weeks, the EWW has retreated somewhat from Feb’s peak (long battles at Multi-Year Ceilings are common). The weekly chart is forming a potential 5-month Ascending Triangle pattern and Chris Roberts would follow a breakout from that pattern.

South Africa: Structural reform faces capital shortfalls

The Macro Advisors team outline how South Africa’s productivity problem has deepened alongside a long erosion in capital formation. While recent total factor productivity gains are welcome, they look more like windfall gains from a dire operating base than evidence of a sustained productivity cycle. Structural reform across logistics, electricity, and ports can lift productivity by restoring the operating base, but this constraint-relief channel is being deployed on a weak capital base. Net investment is just above depreciation, meaning the economy is barely replacing and repairing existing assets rather than expanding the productive frontier. The team struggle to pencil the required 4-5% real gross fixed capital formation growth into their forecasts over the next three years. Without stronger investment crowding into productivity-enhancing assets, potential growth remains stuck at a maximum 2% in the medium run, raising serious challenges for business positivity.

Venezuela debt restructuring flags severe bondholder haircuts

Niall Ferguson points out that Venezuela’s US-backed fiscal receivership was more likely to entrench Chavismo in power rather than deliver democratic reform, and bonds face significant restructuring risk. Although sovereign bonds have continued to appreciate as the Delcy Rodríguez government formally launched a debt restructuring process, the market has read this as bullish. This restructuring is proceeding without a multilateral anchor, and total external obligations are roughly $190BN against an IMF GDP estimate of $111.3BN, implying a debt-to-GDP ratio of ~170%. Trump’s executive order shields Venezuela’s oil revenue from creditor attachment, and no US or Venezuelan policy action thus far prioritises bondholder recovery. The most likely deal structure is a greater than 60% haircut, consistent with a medium-to-low debt-carrying capacity under IMF frameworks. Niall maintains his view that existing financial creditors are not first in line; the bonds are currently overpriced for the restructuring realities.

Commodities

Bitcoin: The upcoming sixth cycle

Markus Thielen points out that there has been a recurring pattern to Bitcoin cycles: each cycle was defined by a distinct dominant narrative, which in turn demanded a different kind of promoter and attracted an entirely new class of believers. Bitcoin has now completed five bull markets and is navigating its fifth bear market. If a sixth cycle is coming, which Markus believes it is, what drives it, and who is the marginal buyer? He says that the sixth may look less like a reinvention and more like a continuation, driven by the same forces and the same buyers that defined the fifth. What gives him confidence in a sixth cycle is that the primary drivers of the fifth, money printing, dollar debasement, and the search for hard assets outside the traditional system, have not disappeared. If anything, they are compounding and accelerating. Markus believes that the next sovereign debt crisis, whenever it arrives, will not find Bitcoin without an audience.

Gold and Silver: New risks are building fast

Jeffrey Christian gives a precious metals analysis covering the gold price outlook, silver market update, platinum and palladium weakness, and the growing risks affecting financial markets. He explains why gold is testing $4,100, why a break lower could point toward $3,800, and why silver is testing support near the low $60s. He also discusses why any sharp spike lower in gold or silver may be short lived. Jeff also discusses new risks being added to the existing economic, political, social, and financial issues that have supported gold and silver prices over the past several years. He reviews the new Federal Reserve chairman, the Fed’s shift toward less transparency, and why reduced information from central banks may increase uncertainty for consumers and investors and make good decision making more difficult. The presentation also covers additional topics such as AI, private equity and shrinking public markets, which may be negative for the broader economy but supportive for gold and silver over time.

Click here to watch.

Are you ready for a super El Nino?

Report by

BCA Research

BC

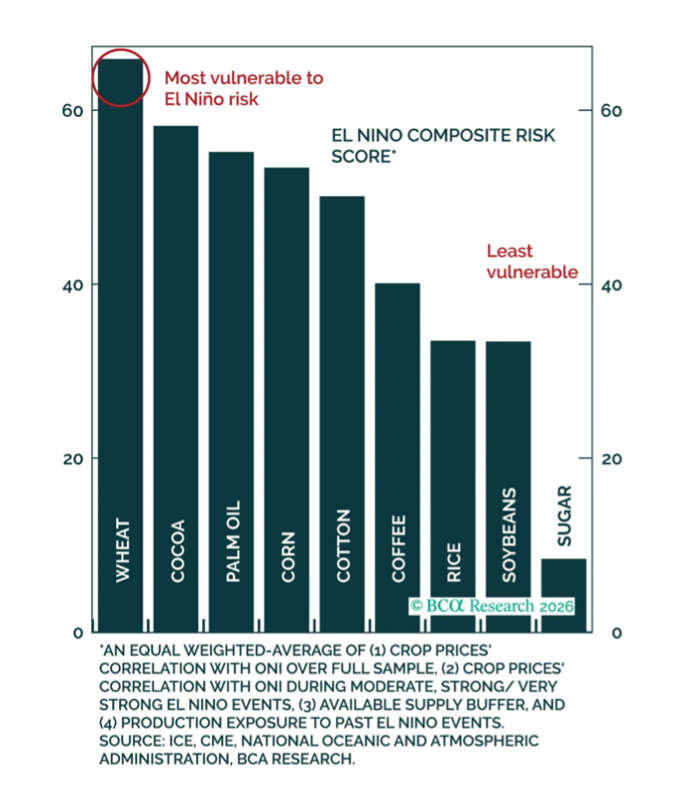

According to Ashwin Shyam and Marko Papic, a potential Super El Niño poses a meaningful upside threat to agricultural prices. Investors should also monitor the political and fiscal risks that higher food prices could create in vulnerable emerging and frontier markets. Major price swings in agricultural commodities are often driven by weather-related supply shocks rather than by demand fluctuations. El Niño risks are rising, with several forecasting agencies expecting sea-surface temperature anomalies to intensify over the coming months. Historically, El Niño episodes have often led to higher global food prices. However, the impact has varied meaningfully depending on crop-specific supply dynamics, macro conditions, and the US dollar. Based on their crop vulnerability scorecard, investors should favour a selective long exposure to a basket of wheat and cocoa versus sugar. Expecting bond price declines across non-oil-exporting MENA economies is a way to hedge for the Super El Niño in a non-commodity manner.

Finding value in junior miners

The large cap copper miners are expensive, trading as much as 3.4x NPV10 on David Radclyffe’s base case assumptions and as much as 2.3x on spot copper prices. Better value can be found in the smaller to mid-cap miners, which often offer attractive growth paths and M&A upside. Risks are sometimes higher in the smaller copper companies. with share liquidity another trade off. Of the five stocks covered in David’s latest report, the best financial leverage to higher copper prices are Taseko Mines Ltd and Atalaya Mining Copper SA, while the lowest leverage is with Sandfire Resources Ltd having strong margins. However, Capstone Copper Corp has the best four-year growth outlook assuming Santo Domingo delivery. The implied copper price (10% nominal discount rate) shows most stocks are near the spot price levels. Out of the group, David prefers Taseko Mines Ltd which offers value, FCF yield, leverage and growth, with Atalaya Mining Copper SA herein upgraded to BUY.