Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

Europe

Following publication of the company’s FY24 annual report, Iron Blue increases their ULVR score +3pts to 27/60 (newly top quartile / fertile grounds for shorting). This reflects 1) Increased stripped out restructuring expense (8% of PBT adj vs. 5% FY23). 2) Profit supports (swings in commodity hedges, FX and inventory impairments) that contributed half of PBT adj Y/Y growth and may prove unsustainable. 3) New disclosure of €2bn reverse factoring balance. 4) Increased goodwill impairment test assumed long term growth rate of 2.8% (FY23: 2.3%), above the 2.1% average for Iron Blue’s coverage universe. 5) KPMG’s tenure as auditor now exceeds the 10-year best practice maximum and non-audit fees contributed 33% of their FY24 payments.

Ernesto Lopez Mozo (CFO since 2009) acquired €224k of stock at €44.93 - only his second buy despite a long tenure. His first was €129k at €25.88 in Feb 20, making this latest move notable for both its larger size and higher price, after a gap of over five years. Rafael Del Pino Calvo-Sotelo (Chair since 2009) also made a rare €1.8m buy in Mar 25 at €37.17. Both are encouraging insider signals with shares near all-time highs. Meanwhile, Luke Bugeja (Divisional CEO since 2021) sold €929k worth of shares on the same day, which matches a stock award in Mar 25. This aligns with 2024, when he also sold his full award. The sale is not concerning enough to offset Smart Insider’s positive view.

At Sapphire 2025, SAP reintroduced its Business Suite as a unified, cloud-based platform integrating applications, AI (via Joule) and Business Data Cloud to drive migration from legacy systems like ECC to S/4HANA Cloud. The strategy aims to streamline operations, improve scalability and enhance decision-making through embedded AI and intelligent applications. SAP is on track to meet or exceed its 2027 financial targets, supported by strong cloud transition momentum, SaaS cross-selling and SMB customer growth. Business AI is driving efficiency by decoupling expense from revenue growth. While generative and agentic AI pose near-term challenges, SAP’s deep integration, domain leadership and resilient infrastructure position it to lead in the AI-driven enterprise software landscape.

UK Mid Cap Technical Review

Messels adds two new stocks to its FTSE 250 Momentum portfolio, which now comprises 27 companies. The portfolio continues to show a preference for Building Services (5 holdings), F&B (4), Financials (4) and Industrials & Services (4). New additions: PayPoint - reasserting price and relative bases from medium term support. Kier - renewed the uptrend and is now breaking out of 5-year price and relative ranges. Other notable charts this week: Chemring - breaks to new 1-year highs and renews outperformance. Coats - developing price and relative bases at long term support levels. AJ Bell - testing resistance at the 5-year highs and gains relative momentum. Telecom Plus - renews medium-term price and relative uptrends.

North America

The stock market scheme

While markets keep climbing, Kolytics warns that their dependence on constant inflows resembles a Ponzi scheme. Financial innovation, policy backstops and herd behaviour have pushed valuations beyond fundamentals, masking growing systemic risk. Key drivers of past bull markets - low debt, falling yields, cheap valuations, globalisation and population growth - are fading or reversing. The Make America Great Again approach is bizarre given that “American Exceptionalism” already pointed to both absolute and relative greatness, but the effects of MAGA policies and trade wars run the risk of rebalancing capital away from an overweight position to American assets - that’s less new money not more.

It’s been one heck of a 30 years in Retail

Scott Mushkin argues that the era of (over) consumerism of "stuff" is waning, with major implications for the retail sector. Spurred by political rhetoric, tariff policies and reshoring efforts, he sees the deflationary tailwind of globalisation unwinding. He also cites changing attitudes, particularly among younger shoppers, embracing second-hand goods over big-box retailers, and how uniquely American it is to have so many physical goods that 80% of all self-storage units are in the US! While this signals headwinds for the majority of retailers, Scott sees upside in the “Make America Healthy Again” movement, underpinning his bullish view on Sprouts Farmers Market, United Natural Foods and Natural Grocers.

Paragon Intel adds BBWI’s new CEO Daniel Heaf to their research pipeline. He earned his reputation as a digital builder, but his tenure at Nike was marked by inventory issues, cost cuts and a leadership shake-up that ultimately eliminated his role, while the stock underperformed the S&P 500 by ~40 percentage points. He now steps into a retailer that has cycled through 3 CEOs in 3 years and watched FY24 revenue slide 7% to $7.3bn, even as it courts a broader demographic appeal and eyes faster international growth. Paragon’s work will examine whether Heaf’s omnichannel playbook can reignite top-line momentum, widen margins and restore investor confidence, while also weighing governance stability and the risk that NKE-style missteps resurface as BBWI charts its next phase.

Despite doubling EBITDA over the past 5 years, LNR's valuation multiple has halved. The problem is that the market sees the high returns in the Industrial segment as funding the lower returns in the Mobility segment. Between 2019-2024, LNR allocated ~$950m to Industrial (mainly M&A) at an attractive ~22% incremental ROIC, while reinvesting ~$900m in Mobility (mostly organic), at a mere ~2% incremental ROIC. Veritas maintains a Buy rating on the stock, citing the company’s strong FCF, low valuation (near tangible book value) and insulation from tariff risk. To lift the conglomerate discount, Veritas suggests improved capital discipline, clearer segment disclosure and scaling buybacks.

IDEXX still commands growth-stock multiples that assume a return to vet services acceleration despite multiple quarters of negative pet visit volume. During Covid and the immediate post-pandemic surge, rising pet ownership bolstered vet visit volumes and gave clinics the pricing power to pass through list-price hikes they were getting from IDXX. Those tailwinds have been fading longer than just a tough comp should last and Hedgeye thinks the market has further to pull back. High inflation is causing pet owners to cut spending, either by reducing visit volumes or declining recommended treatments; these weaker trends are catching up with IDXX, which is losing customers and facing pricing pressure. Sees 30% downside.

BTN raises concerns about DGX's reliance on acquisitions for growth, questioning its sustainability given rising debt (3.0x EBITDA) and acquisition spending that regularly exceeds FCF post-dividends and buybacks. They also highlight earnings quality issues: over half of Q1’s EPS beat came from an unexpectedly low tax rate; receivables are rising without a corresponding increase in bad debt allowance; and more than $2.00 per share in acquisition-related expenses are not being recognised, which is over 20% of the company’s expected 2025 non-GAAP EPS forecast.

Chemicals: Is the worst behind us?

Frank Mitsch sees early signs of stabilisation in the chemicals sector, despite short interest sitting at 52-week (or longer) highs and persistent investor concerns around potential dividend cuts. While he remains cautious on Tronox and Huntsman’s payouts, he considers dividends from Dow and LyondellBasell to be safe. Roughly 60% of 1Q results landed within 4% of his expectations, with Olin, Corteva, FMC and Celanese leading on beats vs. the Street. Westlake was the notable miss, due to underperformance in its PEM segment, partly from unplanned downtime. After over two years of sector underperformance, exacerbated by the overreaction to Liberation Day, Frank believes the worst may be behind us; hence his recent upgrades (to Buy) on DOW, LYB and PPG. He has also been heartened by how the credit markets have been open to companies such as CE and OLN.

InterDigital v. Disney litigation

MDC Financial Research’s Event-Driven Legal℠ service is monitoring InterDigital, Inc. v. The Walt Disney Company (Case #25-00895, C.D. Cal), where a Hearing on Disney’s Motion for a Preliminary Injunction seeking to block the enforcement of a potential Brazilian Injunction is scheduled to be held on May 30th. The case relates to InterDigital's assertion of its video coding/processing Patents against Disney. Disney's Counterclaims will also be argued at this Hearing. MDC will attend this and future proceedings to identify legal catalysts potentially material to InterDigital’s share price. Institutional investors can contact MDC for timely insights, court coverage, and risk assessment on this and other event-driven equity opportunities.

Trivariate flags PLTR as one of the most compelling short ideas ahead of the June 2025 index rebalance. Having surged nearly 5x since mid-2024, PLTR now trades at a $291bn m/cap and an eye-watering 73x EV-to-forward sales - making it the second most expensive US non-biotech stock with over $50m in revenue. Historically, stocks trading above 30x EV/sales fall to 18x within a year and underperform the market by an average of 22.5%. With PLTR comprising over 8% of the mid-cap growth index, a shift into the large-cap universe will likely trigger major selling pressure. Unless you believe PLTR can grow faster and longer than any company has ever grown, selling now and shorting near June 30th is the logical strategy.

Abacus highlights IOT’s unique position as the only scaled, modern IoT platform with strong network effects, pricing power and consistent >30% ARR growth. With low market penetration and a vast TAM, they see years of high growth ahead. IOT’s 200-800% customer ROI and >8x LTV/CAC ratio support a compelling business model, while its AI-driven innovations, such as Samsara Assistant, deepen platform utility. Abacus sees the group as a long-term compounder, especially as regulatory shifts and global expansion drive broader adoption, while in the short-term they believe there is upside to consensus forecasts.

Australia

Robert Crimes maintains a Sell rating on ALX, citing limited upside vs. broader infrastructure peers and mixed asset quality. While ALX’s stake in APRR delivers robust FCF and steady distribution growth, its minority position and concession expiry in 2035 limit long-term value. The Chicago Skyway deal offers modest value, but DG is deeply value-destructive, with equity estimated 70% below ALX’s 2017 purchase price. ALX's infrastructure distributions are set to rise to A$920m by 2030E but collapse to A$250m in 2037E. Robert expects IFM to increase its stake, but it has had a negative impact on the share price to date and cut daily trading liquidity in half. He continues to prefer Ferrovial (+100% upside) and Getlink (+85%) in Global Toll Roads.

Japan

Yuka Marosek sees Kyokuyo as a compelling play on Japan’s tourism boom and the growing global demand for sushi. Japan’s tourism market is forecast to grow from US$49.2bn in 2025 to US$132.7bn by 2035 (10.3% CAGR), supporting demand for premium sushi experiences. While sushi chains like Kura Sushi trade at 39x PE despite slim 2.4% margins, Kyokuyo trades at a steep discount with a price-to-book of 0.81x, even as it posts 26% profit growth and a 12% ROE. Its strategic global expansion and rising overseas sales reinforce the company’s strong long-term investment potential.

Trump to give Japan’s new liquid biofuel business a boost

Neil Newman’s latest Japan Strategy note outlines how US auto tariffs may unexpectedly catalyse growth in Japan’s biofuel sector. While Japan remains firm on protecting its auto industry, it plans to appease US trade demands by boosting corn imports - not for food, but for ethanol production - aligning with its national energy goals. Japan aims to blend 10% ethanol into gasoline by 2030, rising to 20% by 2040, offering US corn exporters long-term demand stability amid uncertain markets like China. Though Japan’s biofuel sector remains small, it is poised for significant growth thanks to renewed political support, trade-driven incentives and infrastructure investment. Companies in Japan involved in liquid biofuel manufacturing include Mitsui & Co, Toyota Tsusho Corp and Idemitsu Kosan Co.

Emerging Markets

Consolidation - THE theme driving improved trends for EM Telcos

New Street expects many markets to consolidate further to just two operators, and in smaller, poorer countries, possibly a single network. Consolidation underpins much of the sector's improvement - most notably through reduced capex, as seen in Brazil, where industry capex dropped from $7bn to $4bn. Countries where further consolidation is likely include Colombia, Peru, Chile, Malaysia and many in sub-Saharan Africa. Key beneficiaries include Millicom, Airtel Africa, MTN, VEON and Entel. EM Telcos remain substantially undervalued on double digit equity FCF yields. Top regional picks include Singtel and KT (Asia), IHS Towers and Vodacom (Africa), and Liberty Latin America and TIM Brasil (LatAm).

China EV: The shakeout

Recent price cuts from BYD are accelerating a price war against a backdrop of weak domestic demand, meaning that the inevitable consolidation of Chinese car companies is coming sooner rather than later. With over 100 carmakers in China, which have ~200 vehicle brands (vs. 10-15 major companies with 26 brands for the RoW), oversupply is rampant - dealer stock has surged to 3.5m units, the highest in years. Richard Windsor sees more industry pain ahead, including overseas dumping of excess capacity and heightened pressure on global markets. While BYD is likely to emerge as a long-term winner, he thinks it is too early to re-enter the stock despite the recent sell-off.

Recombinant Collagen: China’s next Beauty growth engine

Recombinant collagen is emerging as a transformative force in China’s beauty and aesthetics sector, poised to replace traditional hyaluronic acid and animal-based collagen in both medical and skincare applications. On the clinical side, Jinbo Bio stands out as the only company with Class III approval for injectable collagen, expanding its product lineup and expected to grow revenue by over 50% in 2025. In the skincare space, Giant Biogene leads with strong brand equity and broad channel reach, using collagen innovation to power new launches and deepen consumer engagement. With rising demand for safe, science-backed ingredients, recombinant collagen is becoming a structural growth story to watch.

Macro Research

Developed Markets

Double-digit returns through precision-driven trade signals

Triple i Advisors provides algorithmically driven, risk-managed trade signals across global markets - including FX, equities and commodities - backed by models refined since 1985. What sets Triple i apart is its precision: where traditional fundamental research lacks actionable timing, Triple i delivers high-probability trade ideas with real-time execution potential. Their proprietary system distills global data into clear signals with a ~75% historical success rate - an accuracy level rarely seen in fundamental analysis. Clients, including hedge funds, investment banks and sovereigns, receive trades through a secure portal with dynamic risk oversight and CIO-level access. The result: double-digit annual returns and a differentiated edge in identifying opportunities well ahead of the consensus. Click here for further information on Triple i's methodology.

Global liquidity continues to slip lower

Digging deeper into the data, Michael Howell comments that there has been some improvement in central bank liquidity growth thanks largely to the PBoC, ebbing bond volatility, and a faltering USD. These are liquidity-positive, but ongoing QT among other major central banks – including the Fed despite this week’s better numbers and weakening bond markets are liquidity-negative. Global liquidity growth has dipped to +8.1% in 3m annualised terms. A continued slide in liquidity through the rest of Q2 will put pressure on risk assets and liquidity-sensitive cryptocurrencies in Q3. For now, risk asset markets and cryptocurrencies are being supported by the Q1 liquidity upturn, which saw global liquidity expand by over US$5trn. A typical liquidity cycle lasts 5-6 years trough-to-trough, and although Michael originally expected the current cycle to peak in Q4, the downside risks to economic growth and easing central banks will see the cycle peak in early 2026 instead.

Europe’s steady improvement

ABCG Research’s previous forecast of a range-bound movement in EUR/USD played out accurately, as the pair rebounded from the 1.11 level and currently trades around 1.135. The recent PMI data showed mixed signals, but Taha Bin Sohail points out that the manufacturing sector is on an improving trajectory and the dip in the services sector is not a cause of alarm but rather a temporary recalibration. Although trade tensions with the US have resurfaced, Taha believes Europe will not allow this to derail its progress. A diplomatic resolution on tariffs remains possible, which will see the USD gain strength and pressure the euro in the short term. If tariffs are imposed soon, the Eurozone may see a negative economic impact. In light of this, Taha has revised his long-term EUR/USD outlook, expecting the upside to be capped below 1.15.

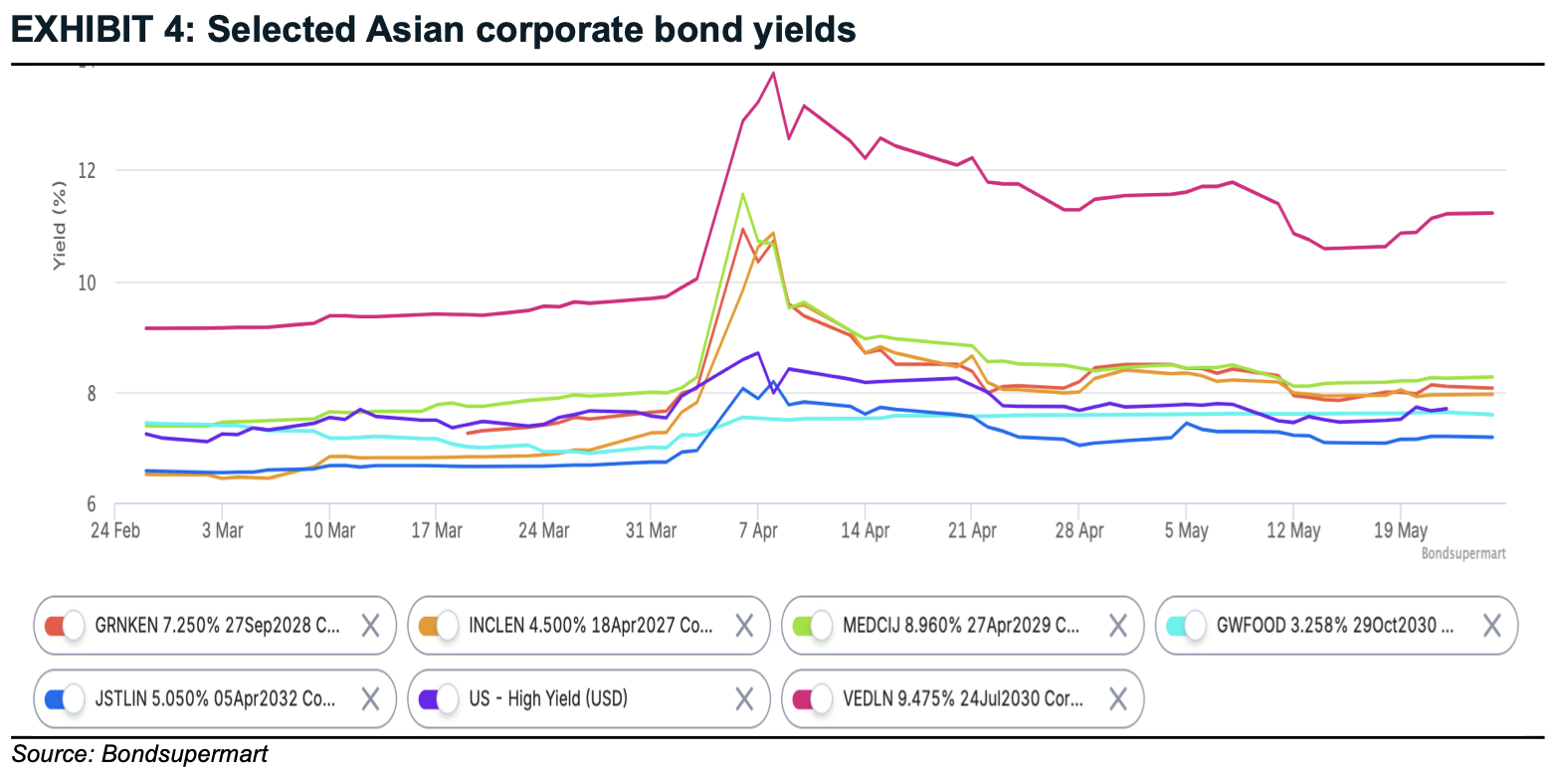

TRUMPoline projector

Warut Promboon follows up on his latest report, discussing where the US is towards the unintended recession and where in EM the Trump tariffs will impact the most. In his last report, he reiterated his recommendation to stay on short-dated bonds in addition to precious metals. Since, Moody’s, Fitch and S&P all downgraded the US, which Warut views as spread neutral, since he believes Moody’s simply took the opportunity on the tariff news to move their rating in line with other agencies. Warut sees the US in a stagflation period. Though rising rates are not friendly to fixed rate bonds, he believes Asian high-yield bonds remain a good place to park capital in the near term on their resilience and attractiveness compared to the US high-yield counterpart (see chart). Prefer short duration under 5 years to keep duration low in preparation for an upward pressure on rates in the near term.

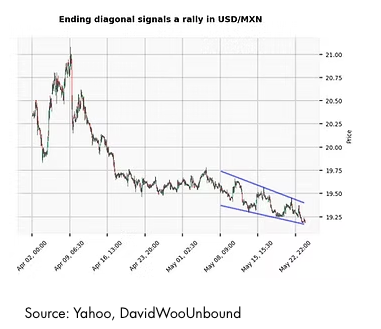

Trade of the week: USD/MXN

David Woo expects Trump to cajole countries that he thinks are being slow to negotiate deals, with Mexico expected to be the first in line, so arguably they are the slowest relative to expectations at this point. Despite this, the Peso has put in a 5-wave rally since April 2nd. Over the past couple of weeks, the 5th wave has formed an ending diagonal triangle, which signals that a corrective rally is imminent. Another source of volatility for markets are senate negotiations over the reconciliation bill. This would initially be felt in the long end of the rates curve, but David expects any dollar weakness to be countered both by a sell-off in risky assets. For their part, Mexico has reaffirmed that they will continue to ease policy regardless of what the Fed does. The local activity outlook is gloomy. Buy USD/MXN.

Japan: Land of the rising rates

Starting this year, Japanese life insurance companies have a new accounting regime requiring them to set aside more capital for any asset-liability mismatches. James Aitken points out that the problem is that the lifers prepared for this change on the assumption that the 2020-22 type JGB curve would last forever, but instead they now have little to no ability to buy the long end of the JGB curve. This may surprise many who would expect Team Japan to be a buyer if rates ever went up. If Japanese real money is selling long-dated JGBs, who is buying? James says global fund managers. The flip side of it being too expensive for Japanese investors to invest in USTs fully FX-hedged is that it must be attractive for global funds to invest in JGBs, then hedge back into dollars. The yield on the package of long 30-year JGB swapped back into dollars is ~7.25%, which is more than the US long bond at ~5.05%.

Underlying Inflation

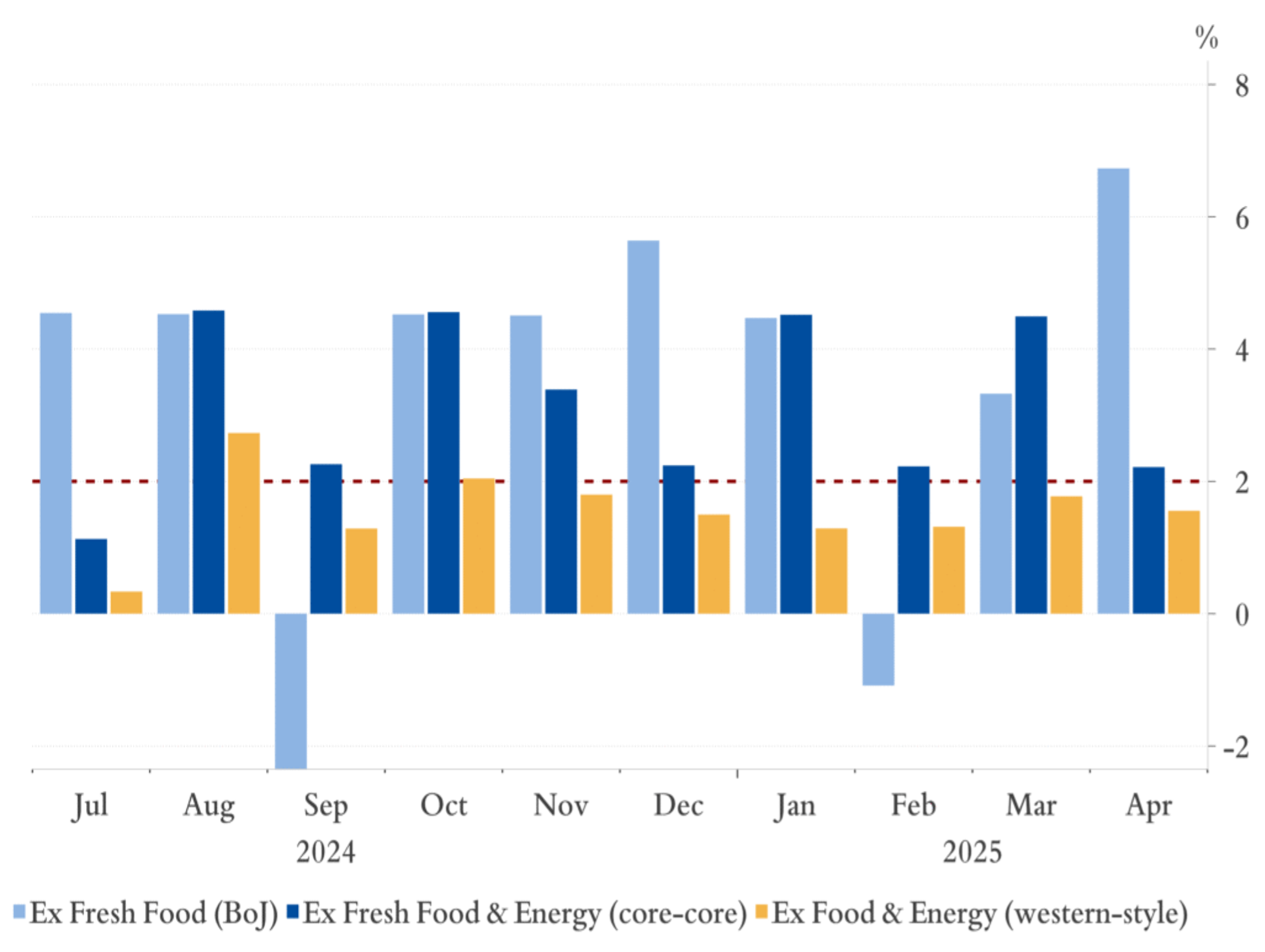

Japan: Inflationary habits

Riccardo Trezzi’s models suggest that Japan is experiencing a persistent inflationary trend, around the BoJ’s 2% target. Riccardo estimates that in April, the BoJ’s core index (excluding fresh food) rose 6.7% MoM SAAR (see chart). As for the other two core inflation measures, the index excluding fresh food and energy (core-core) increased 2.2% MoM SAAR, while the index excluding both food and energy (US-style core) rose 1.6% MoM SAAR. Given potential seasonal adjustment distortions, Riccardo continues to emphasize looking at NSA levels, which suggest that price pressures remain persistent and even higher than last year. His models remain well above the BoJ’s forecasts for core-core in FY2025 and FY2026, with the central bank’s current forecast implying an unrealistic average MoM of less than 10bps sa for core-core this year.

Emerging Markets

Why EMFX has the edge over EUR

Manoj Pradhan sees stronger fundamentals in EMFX than the Euro area. Right now, when it comes to the g – r equation, the euro area and China are the ones boosting g while their central banks are already pushing r lower – that’s the opposite of the US. By the time the US slowdown is evident, other economies are usually just about beginning to scramble and think about a response. Not this time. China’s fiscal drive since Sep ’24 and its strong bargaining position in tariff talks has underpinned EM. Mexico, Brazil, India and South Africa have all raised policy rates more than fundamentals required. South Africa, India, China and Mexico (in that order) all have a cyclical and structural alpha to offer. In FX, Manoj recommends going long MXN/CHF (carry+) and EMFX basket (MXN, INR, ZAR, BRL) vs USD. For equities, go long China, India – both flat – and MDAX.

China: Yuan breakout?

The Chinese Yuan (USD/CNY7.3040) has been in a large consolidation for 30-months. A potential Ascending Triangle is forming. The AT is a bullish pattern (bullish for the USD in this case), with flat highs and rising lows. A breakout would target USD/CNY8.10+. The potential pattern would be invalidated by a break below 6.6968. Most FX rates Chris Roberts follows show potential for further gains against the USD OR potential setups for gains against the USD; thus, the CNY is a bit of an outlier here.

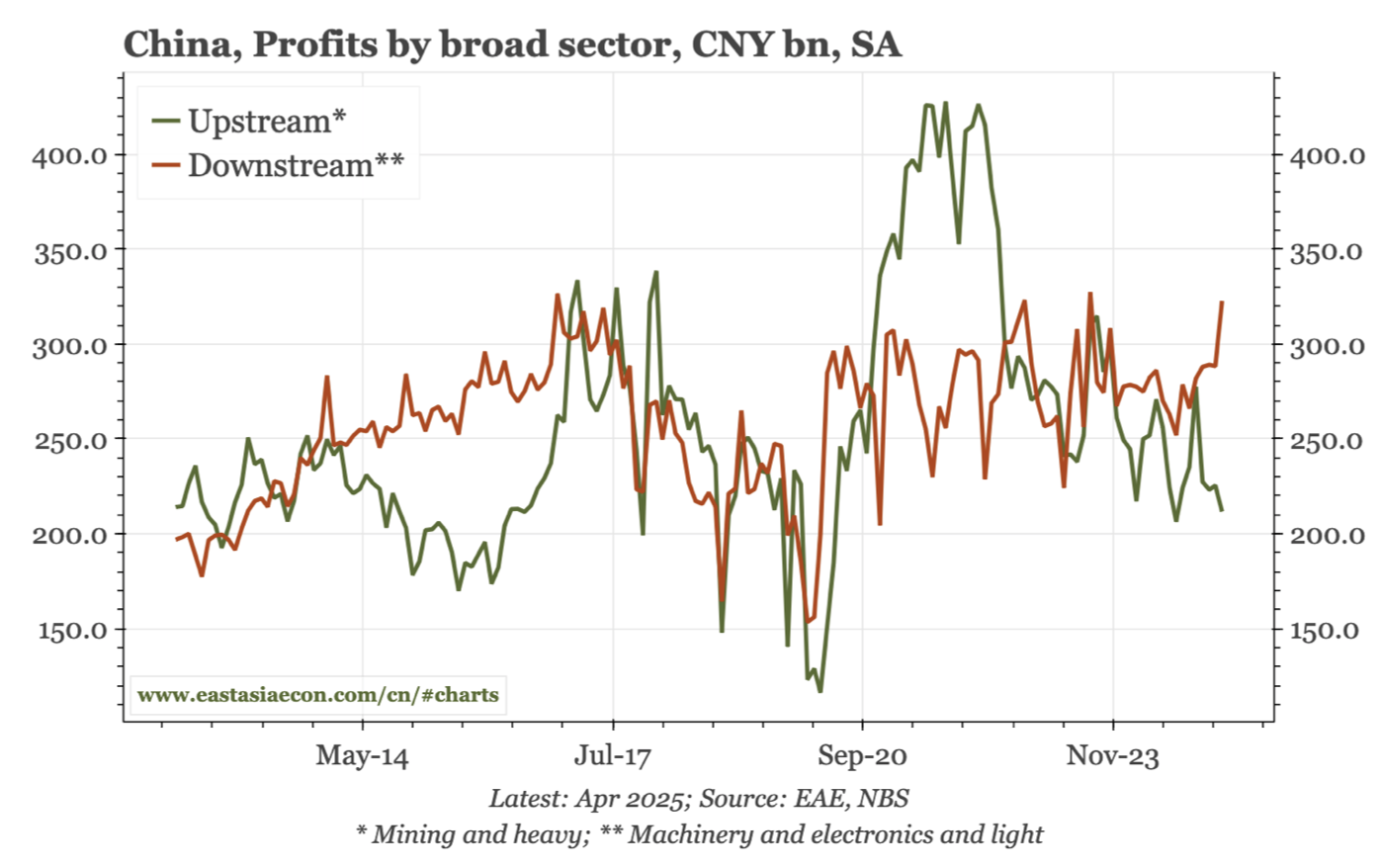

China: Heavy industry profits leading down

Chinese corporate profitability remains weak. Leading indicators for a recovery would be a rise in PPI and an improvement in business sentiment, but neither is visible yet. Indeed, the rate of PPI deflation may actually be decelerating. The weakest sectors are upstream, which Paul Cavey says is reassuring, in a sense. At an aggregate level, downstream industries are doing somewhat better, but only in a relative sense. As a trend, overall profits haven’t declined in recent years, but they haven’t risen either. April data were stronger, but without being able to identify a turn for the better in the economy to explain that rise, Paul assumes it is just simply noise.

India’s investment opportunity

For all the uncertainty about the re-orientation of international trade and supply chains, Asia remains a critical region for global capital investors across every asset class. While the focus on India in recent weeks has been geopolitical, the Verisk Maplecroft team have been keeping a close eye on local market trends. The outlook remains positive, with real GDP growth forecast at 6% y-o-y despite considerable external headwinds, and an improving fiscal image. Tax reforms remain supportive of the business environment, and although public debt remains high-ish, rating agencies are relatively sanguine on the BBB rating. The team remain positive on the country’s strategic opportunity in global sourcing, allowing it to capitalise on the current wave of global trade tensions – as Chinese exporters are priced out of the market, India presents a compelling alternative. Bottlenecks have hindered progress, but significant strides have been made at a subnational level. Investors should watch closely.

Indonesia: Back in quasi-recession

Jonathan Anderson points out that Indonesia is back in recessionary territory. Exports are ok, but nothing more, and domestic indicators have weakened again in most areas leaving his rough proxy growth index barely in positive territory. The good news is that Indonesia has relatively clean balance sheets at the macro level, with low public debt levels, no external deficits and well-behaved domestic leverage indicators. There is also more room to ease policy. Inflation is running near record-low levels, real interest rates are near record highs, and BI has been cautious on the easing cycle. With the rupiah supported in coming quarters, there is further room for policy stimulus ahead. Nonetheless, with listed earnings flat and lacklustre growth momentum, Jonathan still doesn't see Indonesia as an equity outperformer. Meanwhile, the combination of a stable rupiah, high real rates and a gradual easing cycle keeps Jonathan in IDR carry and local debt.

South Africa: One small cut, one big implicit signal

The SARB’s recent rate cut, while long anticipated, marks a shift in tone as risks are now seen as balanced and a 3% inflation target scenario was introduced, suggesting a preference for anchoring inflation at the lower end of the target range. However, Peter Montalto finds this scenario implausible, since it assumes a smooth and immediate re-anchoring of inflation with little macro cost. Despite lower CPI and growth forecasts, the baseline suggests a gradual rate path with the QPM-implied repo rate dropping to 6.93% by end-2025. A July cut is seen as 40% likely, with future moves dependent on global conditions and SARB communication. The next MPC meetings are set for July, Sept and Nov, with cuts unlikely beyond July without further data shifts. Peter sees the official target only being changed next year.

ESG

A transition tipping point

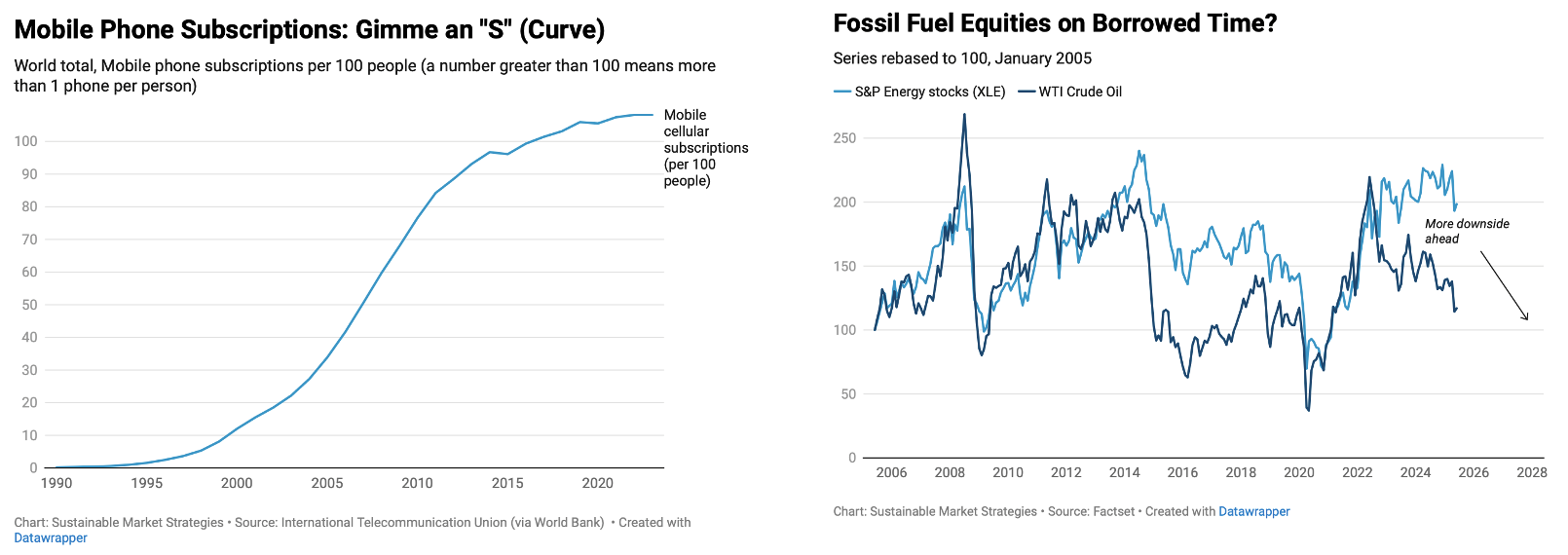

Renewable energy technologies may be entering the most exciting phase of the S-curve when it comes to aggressive gains in market share relative to incumbent fossil fuel sources. Just like mobile phone subscriptions (see chart), the S-curve demonstrates that investors must think about timing instead of assuming liner growth in order to obtain the best returns. EV sales in countries like Norway have already reached the end of their curve, and fossil fuels such as coal are seeing an inverted S-curve at play. Fossil fuel equities may be living on borrowed time (chart 2), and investors that have not yet diversified away from conventional energy assets should do so before the next wave of imminent write downs of stranded assets begins. The window is closing rapidly; act quickly.

Commodities

Bitcoin: An early warning signal

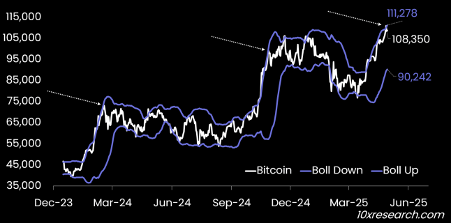

Markus Thielen points out that when Bitcoin loses momentum and falls below the upper Bollinger Band, defined as two standard deviations above the moving average, after being above it before, it often signals an early warning of impending consolidation. A close below this upper band typically reflects weakening bullish pressure and has historically preceded sideways or corrective price action periods. Bitcoin’s short-term uptrend is at risk if it fails to hold above $106,000 and $104,012, which are both key profit-taking thresholds. The rally has been steep and largely uninterrupted, driven by easing tariff-related risks, but all three daily reversal indicators have turned bearish, suggesting fading momentum and increasing the chances of a near-term correction.

2025 Silver Yearbook

Since the release of the 2024 Silver Yearbook, the silver market has seen prices rise sharply to record levels and then decline significantly, only to rise again in the first quarter of 2025, and fall again in April. CPM forecasted both the increase, decline, and further rise of silver’s price. The presentation below gives a small taste of CPM Group’s view of the opaque silver market. The 2025 Silver Yearbook is required reading for anyone hoping to get a leg up in this market, please get in touch to find out more.

Click here to watch the presentation.

Iron ore: Uncertain markets

For now, volatility in China-centric industrial metals futures will be dictated by tit-for-tat trade measures and heightened risks of a global recession. That said, Atilla Widnell explains that inflation should also serve to push marginal cost iron ore producers higher up the cost curve; raising the cost floor and support for iron ore prices. At the same time, the seasonal expansion in Australian and Brazilian iron ore shipments should also serve to create a cap on prices throughout Q2. The great unknown is whether Chinese authorities will enforce government-mandated steel capacity reductions. If global trade measures remain in-situ, Atilla believes this increases the prospect of Chinese authorities revisiting expansive fiscal & monetary stimulus to defend the domestic economy. He maintains his medium-term outlook to US$95.70–107.84/t CFR China for Q2 2025. His short-term target is updated to US$94.12-95.62/t CFR China due to a potential stronger sell-off of ferrous metals markets and expanding arrivals of iron ore cargoes in Chinese waters.

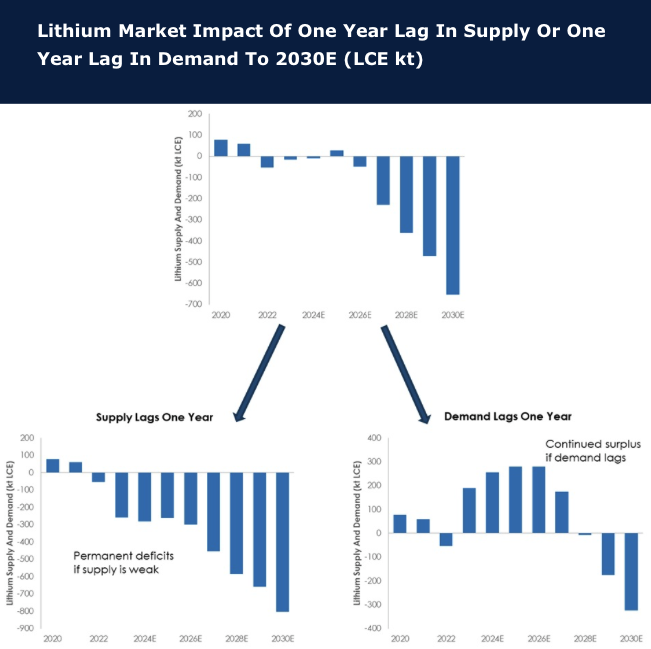

Lithium: Look to the horizon

Back in 2023, David Radclyffe notes the rapid demand growth outlook in the market and the surging supply. Such is the Law of Small Commodity Markets, leading to massive surges or declines in supply & demand, and resulting price swings that are nothing short of spectacular. In 2023 the GMR team showed that with any upset via delayed new mine starts, or of EV production being weaker than expected, the Law of Small Commodity Markets would apply – the bottom right chart created two year ago had forecasted today’s outcomes. To corroborate this, many groups are revising market expectations, with some expecting a surplus into the 2030s. Traditionally, with prices deep into the cost curve, projects would be deferred. But this is lithium! New projects are continuing with debt and equity readily available. The market remains good for lithium consumers, battery or auto makers, and bad for miners. The bumpy ride will continue, hold on tight.