Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

Deutsche Boerse integrates social media intelligence in market surveillance software

While Deutsche Boerse has been an early adopter of social media monitoring for years, they have now taken the critical step of integrating Stockpulse's social analytics directly into their core Scila surveillance system. This integration provides comprehensive monitoring of 70,000+ global equities and cryptocurrencies with real-time social sentiment analysis, buzz metrics and seamless workflow integration within their mission-critical market oversight platform. This signals a broader trend toward holistic market surveillance encompassing trading data, news feeds and social sentiment. As social media increasingly shapes market dynamics, similar integrations are likely to follow globally. For investors, Stockpulse's insights into social sentiment, help spot emerging risks and opportunities before they hit the market. Contact us for a free trial / demo.

Robert Crimes views CLNX’s sharp de-rating since 2022 as highly unjustified. Prop. EBITDaL has grown 36%, from €1.8bn in 2022 to €2.4bn in 2025E, yet the share price has declined 26%, massively underperforming the Eurofirst 300. The stock trades on 2025E EV/EBITDaL of 16.7x, a 29% discount to the 22.9x average of its recent disposals. Robert believes CLNX could attract a buyout from a large consortium, such as American Tower, as it offers a non-replicable pan-European network, ranking first or second in eight of the ten countries it operates in. His TP of €69, implies ~135% upside, with CLNX ranking 3rd of 23 on Insight’s Stock Ranking System.

Arete’s report titled "The Capex Conundrum" focuses on: 1) The broader growth backdrop for leading-edge semi demand and the disconnect in ASML and wider WFE estimates into 2026/27. 2) Capex for key customers which should see significant upside over this cycle, boosting EUV demand and delivering above consensus revenues and EPS through 2027E. 3) The ongoing China capex contraction which is now captured in consensus numbers and stock sentiment. 4) Why there has been a disconnect between N2 capacity growth and EUV unit shipments. 5) Risks around the EUV roadmap and the possible move to 3D DRAM and how that might impact unit demand. 6) Valuation risk/reward, especially against the backdrop of recent sell-side downgrades and negative broader investor sentiment towards WFE, looks attractive.

Paragon’s Executive Diligence Memos highlight a bearish view of DSY’s Chairman Bernard Charles and CEO Pascal Daloz. While Charles’ visionary approach was instrumental in building the company, his controlling management style will hinder the necessary commercial agility and cultural change, making his continued deep involvement the primary obstacle to DSY’s future performance. Meanwhile, Daloz's plan involves methodical, incremental process improvements and evangelising a long-term AI vision, but his non-confrontational style is ill-suited for driving the disruptive change that is urgently needed. Since Daloz took over, deal slippage has doubled, forcing the company to offer more favourable payment terms to secure deals. This culminated in management cutting the FY25 OCF outlook, a move that has shaken investor confidence.

North America

Actionable Alpha: +59% in Q3, defensive rotation in Q4

Michael Belkin’s proprietary time-series model delivered another standout quarter, with his alpha capture portfolio up 59%, eight times the S&P 500’s return. His portfolio had no MAG7 exposure and all 50 final stocks had positive alpha. Michael expects Q4 will see a major change in sector rotation. In a speculative bubble nobody cares about utilities, energy, healthcare, consumer staples and REITs - but when the tide turns those sectors are where the risk-off money scrambles into. Utilities turned around last week and other defensive sectors are likely not far behind. Gold and silver mining stocks are also expected to continue to outperform. On the other hand, several software, semis, social media, asset manager, regional banks, retailers and construction stocks feature on his model’s underperform/short list. Stock specific ideas are available on request.

Special Sits Idea Forum

The majority of ideas presented at MYST's latest buyside event were industrial-related, with themes including potential takeouts, SOTP simplification stories and power-related names. Stocks highlighted include:

Aptiv (APTV) - “GoodCo vs. BadCo” split to unlock hidden value of Connection Systems business. TP $125 (45% upside).

Bed Bath & Beyond (BBBY) - unappreciated assets create “zero enterprise value” amid positive FCF inflection. TP $28 (180% upside).

DuPont de Nemours (DD) - re-rating tailwinds fuelled by fundamental and technical catalysts. TP $115 (45% upside).

Idaho Strategic Resources (IDR) - enormous upside from potential US government partnership / investment.

Peloton (PTON) - new product launches + subscription price increase to accelerate turnaround.

Ralliant (RAL) - ignored "broken spin” poised for positive revision cycle. TP $60 (35% upside).

Retail Cross Currents: 4 key themes & top stock ideas

GHRA highlights an unusually volatile retail backdrop through late 2025 and early 2026, noting multiple “cross currents” affecting both consumers and retailers. Recent rating changes include downgrades for Dollar Tree (Reduce) and BJ's Wholesale Club (Hold), while upgrades cover Williams-Sonoma (Buy), Wayfair (Accumulate), Kohl's (Accumulate) and Dick's Sporting Goods (Hold). GHRA’s key investment themes emphasise: 1) stocks offering both EPS upside and multiple expansion (Five Below, Ross Stores, Burlington); 2) underappreciated turnaround stories (Kohl's, Dollar General); 3) selective “rate-trade” exposure favouring home furnishings over home improvement (Williams-Sonoma, Wayfair, Tractor Supply); and 4) secular winners / “Coffee Can” stocks (Walmart, Costco, TJX, Ollie's Bargain Outlet, Casey's).

Hesham Shaaban expects DKNG’s Q3 results to miss consensus, with Periphery’s revenue trackers showing mixed y/y growth in Jul and Aug and their new NFL Upset Tracker pointing to a weak Sep (total upsets down ~33%). He had planned to increase his short into Q4 to capture the downward revision cycle but notes the buyside has already sniffed out the early fallout from the NFL season. Looking ahead, he anticipates management will cut FY25 guidance while going big with their initial 2026 guide to backstop the stock - a pattern seen in both 2024 and 2025. With history likely to repeat, Hesham may still add into the revision cycle but could reduce exposure ahead of the Q3 print.

John Zolidis turns bearish on SBUX heading into Q4. He views domestic store closings and a potential China exit as signs that SBUX is no longer a growth business and valuation should contract to reflect this. Furthermore, traffic remains negative and estimates are too high more than one year after Brian Niccol started as CEO. Last quarter was good for Quo Vadis’ calls with their average Long idea falling 1% compared to an average decline in their Short ideas of 15%. Their (Retail & Restaurants) universe fell 9%, reinforcing that Quo Vadis' approach is identifying winners and losers and creating alpha. Q3 was the fourth consecutive quarter with longs outpacing short ideas.

Bios scores big on 89bio, rotates to new opportunities

Bios Research’s long call on 89bio has paid off handsomely: since turning bullish in Apr 25, the shares have climbed ~120%, culminating in Roche’s announced takeover at $14.50/share plus a $6 CVR. With conviction now removed, Bios suggests rotating into SMID-cap biotech to capture what they see as the early stages of a new bull cycle. On the short side, the team has just launched a new idea with 30-50% expected downside over the next 6 months. Their track record is strong: 15 of 22 shorts over the past 18 months have generated absolute returns (~72% alpha-adjusted hit rate), with notable successful conviction removals including Apellis, Butterfly Network, Geron and Inspire Medical.

GH has two new liquid biopsy products that are ramping quickly and are well positioned. There is a massive TAM to go after: $100bn vs. current industry revenues of ~$3-5bn. Abacus believes Shield, one of the new products, could transform GH, with revenues growing from $60m this year to $700m in 2028, with further upside if Shield evolves into a multi-cancer screening platform. GH’s first-mover advantage is significant, provided the company demonstrates strong commercial execution. Abacus does not anticipate the need for additional capital, though a modest equity raise in 2026/27 to support growth would not be surprising. They target ~150% upside over the next 3-4 years.

Further misery for beleaguered Canadian lumber producers

ERA continues to urge caution on all lumber-leveraged names and sees risk as downside-weighted in the near-term from sluggish demand. While the timber REITs are better positioned over the long-term, weak wood products markets will be a headwind for them too. Q3 earnings will be terrible and with an incremental 10% tariff being introduced shortly, prospects for Q4 remain extremely bleak. Lumber names are generally beaten up and there will be plenty of upside runway for survivors when markets eventually begin their next upcycle. However, ERA recommends waiting a quarter or two before building long positions.

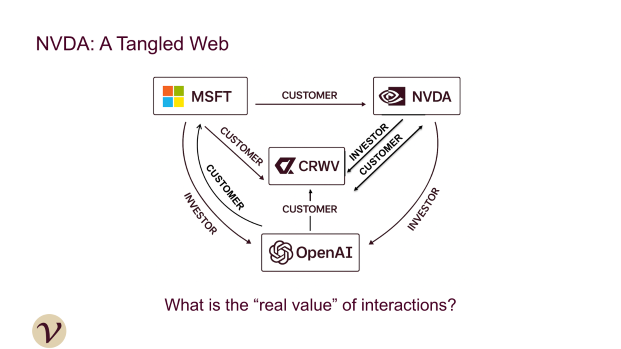

Nvidia's circular financing

Veritas has been flagging NVDA’s customer financing activities well before they hit the headlines: in 2023, they first highlighted the issue in “Nvidia & The Tech Sector's Circular Cash Flows” and reiterated their concerns earlier this year in “Nvidia’s CoreWeave - A Familiar Story”. Following the Oracle/OpenAI deal, the sell side is now echoing Veritas’ warnings, drawing parallels to the dotcom bubble, when Nortel, Lucent and Cisco extended credit to customers to enable their internet infrastructure buildout. Veritas does not expect this risk to be priced into NVDA's stock until revenue growth slows. If investors doubt customers can generate returns on their chip investments, these large negative cash flow purchases will not be well received.

PAR has repositioned itself as a pure-play technology company following the divestiture of its government business, while expanding its TAM through the acquisitions of Stuzo and TASK, which extended its cloud-based unified commerce platform into convenience stores, fuel retailers and new international markets. Although management flagged some caution on ARR growth in 2025, Sidoti expects the company to achieve its 20% growth target in 2026, supported by recent contract wins and a ~$100m pipeline (excluding two large deals, one potentially closing by year-end). The recent share price sell-off is unwarranted, as PAR is well-positioned to win larger customers with more potential for upselling and margin expansion. An improved balance sheet also allows for increased flexibility around further M&A opportunities. TP $97 (150% upside).

AI is fuelling accelerating demand for high-performance compute (HPC) and Bitcoin miners-turned HPC hosting providers have been huge beneficiaries. While the stocks have rallied significantly as multi-billion-dollar contracts become more frequent, Rosenblatt sees a valuation disconnect at WULF due to its perceived smaller power pipeline. They view this as more of a disclosure issue than anything fundamental and expect the power experts at WULF to proactively add new capacity ahead of current market expectations. As such, Rosenblatt reiterates their Buy rating and raises their TP to $14.50, based on 16x their 2027 Adjusted EBITDA estimate.

Japan

Under new leadership, Kyodo is accelerating its pivot from the declining paper-printing business towards higher-margin niches such as high-performance packaging materials, flexible packaging and tube products. Margin gains in recent years already reflect this shift and the company’s 10-year plan aims to scale these efforts further. The key question for investors: with DNP and Toppan well ahead in diversification, can Kyodo leverage its niche strengths to establish itself as a viable third player in a consolidating industry. Yuka Marosek argues it can. While Kyodo’s OP recovery appears partially priced in (13.9x P/E vs. DNP at 14x and Toppan at 18.4x), a 4.8% dividend yield should appeal to income investors and with FY26 OP projected +20% y/y and ROE rising to 6.1%, further upside remains possible.

Emerging Markets

Can a demand sanction on Chinese biotech help US companies?

Blue Lotus examines the early-stage pipelines of 25 Chinese biotech companies (CBT), covering 177 drugs and 278 rival drugs worldwide across 80 biotargets. CBT claims 5 dominant leads, 8 competitive leads and 8 co-leads. Of the remaining 59 biotargets, US biotech companies (USBT) hold leads in 43, of which 31 face "me-better" Chinese competition and 12 "me-too". CBT has been winning by quantity and now increasingly by quality. This raises a dilemma: US demand sanctions could ease competitive pressure for ~49 USBTs (~14% of sector m/cap) but it might also restrict patient access to innovative therapies. Innovent, BeOne, Duality, Junshi and Akeso are highlighted as top early-stage innovators, while 3SBio and SinoBio appear undervalued.

At first glance, Delhivery’s FY25 results - its first net profit and positive EBITDA margins - suggest the company has finally scaled and matured. However, Iii argues the turnaround is more cosmetic than fundamental. Favourable revenue recognition policies (contract assets equal to ~30 days of sales vs. a 13-day transit cycle), depreciation changes and halved ESOP charges materially flattered reported profits. Capital allocation remains troubling, with Spoton Logistics revenues collapsing >70% since its INR 16bn acquisition, yet losses effectively buried via amalgamation. Rising impairments, questionable subsidiary accounting and elevated executive compensation add to concerns.

It has been three years since the last insider activity in this stock occurred. In Jun 22, the selling was from Finance Director Junqiang Guo and Deputy GM Chan Zhang around CNY 200 per share. The stock rose for a few months but then fell sharply in 2023. Recently, Guo, Zhang and Deputy GM Hefeng Lu made large sales at less than half that price: Guo sold US$862k at CNY 85, Zhang US$515k at CNY 85.06 and Lu US$350k at CNY 87, reducing their holdings by 30%, 30% and 23%, respectively. The stock has nearly doubled from its Apr 25 low but remains flat over the past 12 months and below 2023 levels. Smart Insider are ranking the stock -1 (lowest rating).

Buy the VEDLN 9.85% '33s at 101/9.6%/4.9Y; Hold the rest of the curve - Vedanta priced its USD 500m 144A/RegS 7NC2 notes at 9.125%, down from IPT of 9.5%. The lower-than-expected yield signals strong demand and investors’ growing confidence for the credit. Lucror’s Credit Bias on VRL remains "Stable", as the company's low-cost positions and robust balance sheet should help it weather commodity price volatility amid global trade tensions. The 9.85% '33s have the longest duration and would hence have the most upside if the credit spread tightens, which Lucror expects to occur following the successful issuance of new 7NC2 notes.

Macro Research

Developed Markets

AI: Scepticism’s turn

The last week has seen AI sceptics jumping up and down about a coming crash, but Richard Windsor sees them citing data that is misleading. One reason was the MIT study, which claimed that 95% of AI projects failed to yield benefits, but the report also said that great benefits can come when such projects are implemented correctly. So, the sceptics may be wrong, but not nearly as wrong as those who believe superintelligent machines are soon to be among us. Richard sees the idea of $200bn/yr in revenue for OpenAI by 2030 as preposterous, and sees a correction coming, but it won’t be a crash on the scale as the AI sceptics claim. Hyper valued companies burning through money will get into real trouble, but the picks and shovels like Nvidia, Nebius, Micron, SK Hynix, Samsung and Qualcomm and so on are likely to continue to do well. Richard continues to hold the latter two.

UK: A governing party in denial

Helen Thomas sums up the Labour Party Conference with one word: denial. Denial about the scale of the economic challenge, the breadth of discontent within the party and the country, and what must be done to resolve the situation. The message of the conference was that we are in "a fight for the soul of our country", with Starmer pitching himself against Farage. Despite Andy Burnham rowing back on his ambitious coup attempt, everyone is discussing who the replacement for Starmer will be. Meanwhile, Chancellor Reeves is fighting the Gilt market daily for her political life, but she is in denial about what is required. Helen says that we remain in a hiatus ahead of the budget, where even the Chancellor doesn't know yet what will be in it on 26th November, in part because she does not yet know how the Office of Budget Responsibility (OBR) will model her choices.

Germany: Angela Merz

Four months in and Chancellor Merz’s government has a mixed record, and Niall Ferguson says that doubts over the coalition lasting until 2029 are justified. However, media forecasts for a near term breakdown are unlikely to be founded, and Niall expects the coalition to survive beyond November of next year. Even if the AfD secures victories in state-level elections, Merz and Vice-Chancellor Klingbeil will be able to use the argument that time must be given for economic recovery before the electorate rushes to the polls for another party. Russia’s antics in testing NATO should bolster the coalition’s cohesion. Niall is positive on German equities and continues to be constructive on German growth, which will in turn boost Europe as a whole.

US: Drift risk rising

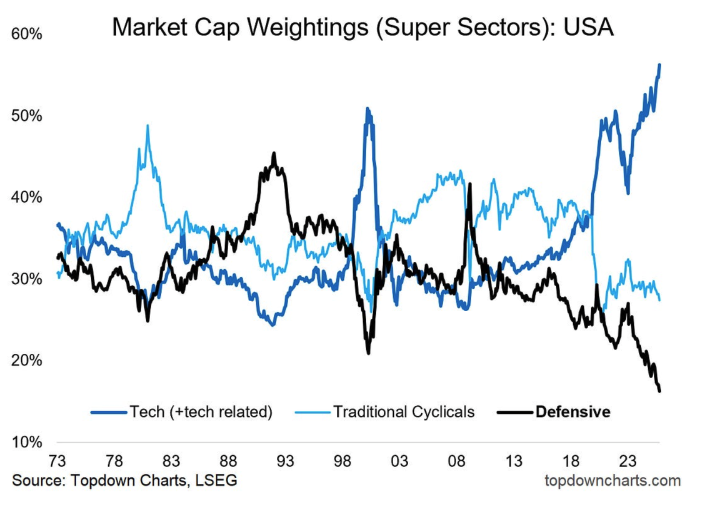

The good thing about cap-weighted index investing is that over time it automatically allocates more money to the best stocks and takes from the bad ones. The bad thing about it is that… over time it automatically allocates more money to the best stocks and takes from the bad ones. Callum Thomas’ chart shows both of these aspects in action, with tech dominating the scene and record lows for defensives. In times like these where there is a very sector driven bull/boom/bubble underway, such strategies can become very undiversified and lop-sided very quickly. Options for investors include switching to equal-weighted indexes, active allocation, tactically making sector tilts when major extremes are reached, or correct it at the portfolio level by including uncorrelated/defensive assets.

US: Payroll data points to further cuts

According to ADP, payroll employment fell in September, and the figure for August was revised lower. Carl Weinberg takes the view that whether this is an accurate statistic or not, people in the markets believe that it signals something! The signal from today’s headline will not be a good one. Remember, perceptions are more important than realities in the financial markets. The ADP private sector payrolls estimate was -32K in September after -3K in August. The August estimate was revised sharply lower to 54K. According to ADP’s estimates, private sector payrolls averaged 22K in Q2 compared to 139K in Q1. Goods-producing payrolls were -3K. Service-producing payrolls were -28K. If supported by the upcoming monthly non-farm payrolls data, Carl says these ADP numbers are likely to increase market participants' expectations for additional Fed rate cuts this year, which should, in turn, weaken the dollar and flatten the yield curve.

US: Favour the bears for short-run USD risks

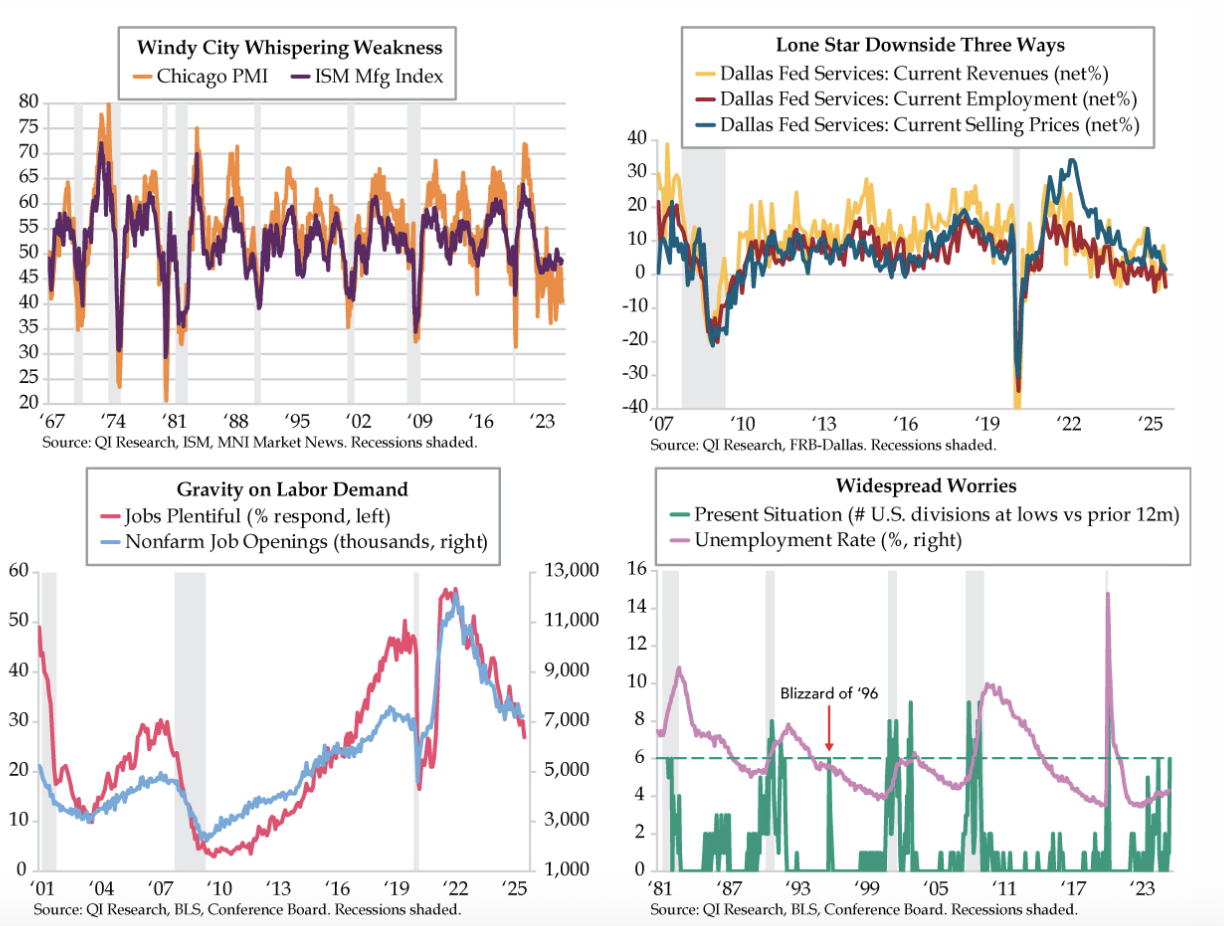

The Chicago manufacturing PMI fell from 41.5 to 40.6 in September, marking 22nd straight months of contraction. It’s streak in the red (below the 50-breakeven) has now extended to seven months. Whilst JOLTS nonfarm job openings surprised to the upside by rising 19,000 to 7.227m, only 9 of 18 industries increased. The Conference Board’s Jobs Plentiful gauge fell to a cycle low of 26.9%, calling into question job openings’ staying power. The forecasting community may have been too sanguine on September’s unemployment rate, after all. Should downside risks of growth, labour and inflation come to fruition, they would bolster the case for Fed easing in both October and December and could push the USD to new lows for the year.

US: Why the Fed’s rate cuts will be fruitless

The gist of Fed doctrine is that rate cuts boost economic growth and inflation, but this inverse relationship has not been observable for many a decade. David Ranson’s latest paper covers three areas in which the role played by the Fed is not what many would expect. First is the way that movements in the short rate relate to those in the long (30-year) rates; second is the way that interest rate movements relate to the economy’s performance, with the correlation between current real GDP growth and short-term rate movements being strong and positive; and third is the way that interest rate movements relate to inflation, with inflation driving the Fed rather than the other way round. Many decades of evidence show that it is ultimately the long rate around which the short rate fluctuates. Control of the economy from the short end of the yield curve is a myth.

Japan: Give me capex

The quality of Japan’s growth is outstanding, Manoj Pradhan comments on how capex is the dominant trend alongside base pay growth. Additionally, the composition of inflation is not convincing, with goods and rice prices forming the biggest component. Thankfully, the combination of labour shortages and services producer price inflation suggests that capex may be playing a critical role. Pulled together, these point to productivity creating the virtuous cycle of income-spending, a more sustainable likelihood of the wage-services price drift that the BoJ desires, and an economy that can handle any rate rises as the underlying rate of return in the economy is rising. The productivity dynamic points to equity upside not just today but for the next 2-3 years. Balassa-Samuelson should mean medium-term Yen upside, with Manoj claiming EUR/JPY as the better choice for Yen bulls whilst USD improves.

Emerging Markets

Remain overweight Taiwan, China and Korea

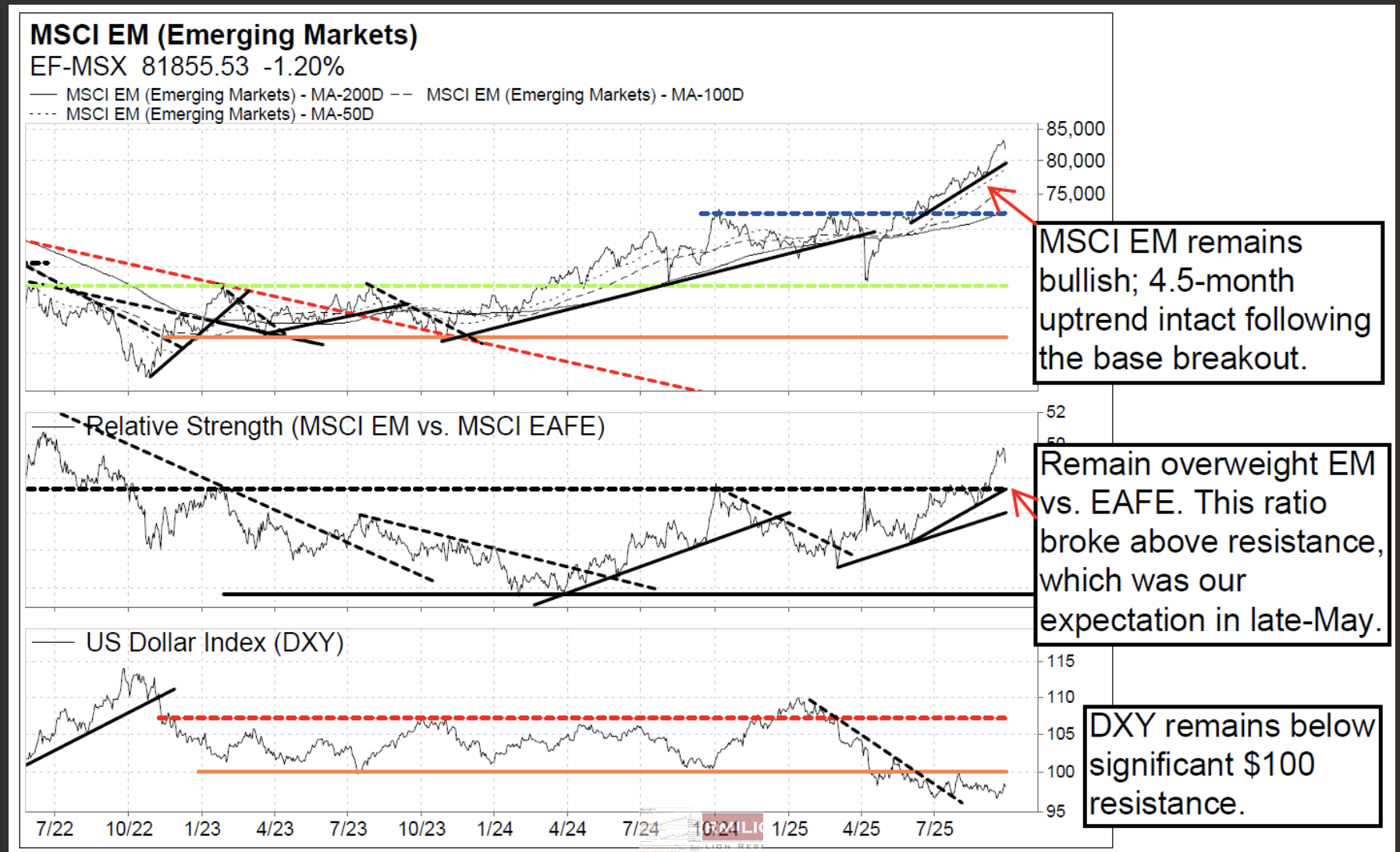

According to David Nicoski, the MSCI Emerging Markets index (local currency) and EEM-US (USD) are both trading within 4.5-month uptrends, and he remains bullish. David expects support at the uptrend, which also coincides with the 50-day MA and $50.65 horizontal support on EEM-US. He would view any pullback to $48 support on EEM-US as a buying opportunity. For EM countries, while price remains attractive, he is downgrading Greece to market weight due to RS deterioration. EM countries where he remains overweight include Taiwan, China, and South Korea. Additional leadership countries include Vietnam, Romania, and Pakistan. For EM sectors, defensive EM sectors (staples and utilities) continue to underperform and are at YTD RS lows; underperformance has continued, as expected -- avoid. Meanwhile, attractive EM sectors where David expects outperformance include: MSCI EM technology, consumer discretionary, materials, and communications. He is also monitoring for a RS bottom on EM health care.

Argentina tries… orthodoxy

From a muddle-through approach fraught with renewed peso and inflation risk, to more classically orthodox measures, Jonathan remarks just how much the policy stance has changed in the past three months. This is the best chance of getting money growth and inflation back down into low double and ideally single digits, at the cost of keeping the economy in recession. In the face of the country’s anaemic export economy, the only hope for external stabilisation is to keep overall demand and import spending weak. Even if Argentina holds course, it doesn’t guarantee a stable peso, and the needs to give up the USDARS 1,500 "ceiling" and let the exchange rate find its level without endless borrowing support. The recent backup in dollar yields has opened tactical value, but not necessarily a structural buying opportunity; there's a big difference between successfully stabilizing the macro position and finding an exit strategy for external indebtedness.

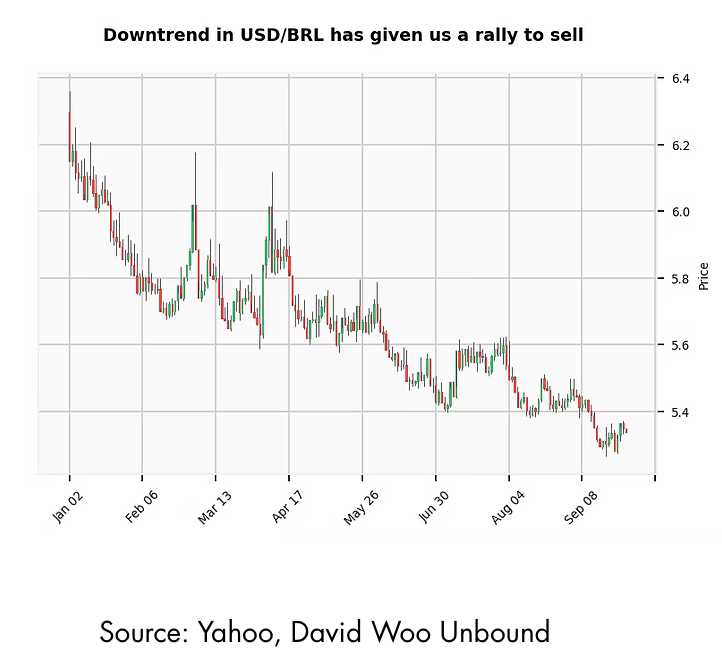

Brazil: Benefitting from uncertainty

The short-term trend in the dollar switched to a bull trend against most currencies as rates reversed higher last week. This wasn't the case for MXN and BRL however, where David Woo points out that the correction to the trend wasn't sufficient to reverse it. BRL in particular failed to get above pivotal resistance at 5.40. Brazil has been a beneficiary of the trade war between US and China, with China choosing to purchase soybeans from Brazil. Uncertainty about the future of the government in Argentina has also been a tailwind for BRL. A shutdown in the US should be beneficial for carry trades as markets will have little guidance from data to change macro views. David bought the November BRL future at 0.18625. He’ll take profit on a move to 0.1930 and stop out at 0.1820.

China: Holding against resistance

Chris Roberts comments on the Shanghai Composite (3,828), which has been ranging above 10-year resistance at 3,500–3,732 for five weeks. Daily chart indicators have now unwound very overbought readings (14-day RSI reached 88, just below extremely overbought 90), and the area of the rising 40-day WMA has been acting as support since May. The ranging above major resistance is seen as a sign of strength, and there is a low-risk entry here that allows Chris to try an initial long position. Go 50% long at market. His initial stop is a daily close below 3,695.

How will China monetise AI differently?

China will be a close and capable AI follower, focusing on downstream implementation as the US focuses on upstream. This means the two will not run head-to-head encounters right away, and China can lead in the application of AGI in manufacturing and logistics. Its monetisation path will be more complex but can exist. However, as it stands, China is under-monetising AI vs the US. The Blue Lotus team estimate that consumer (2C) AI applications generated $2.0–3.5bn in the US and $0.3–0.5bn in China (excluding AI-enabled advertising and much of video AI). The US monetises AI globally, with global 2C revenues bringing in ~12x that of China. However, the gap will shorten significantly by 2030, in part by taking a lead on robotics+AGI. The team reiterate their top picks of Alibaba, Hesai, CATL and Kuaishou. Baidu stays as a sell.

Should investors re-enter India?

Jonathan Anderson’s growth proxy index has rebounded to around 5% y/y in the past few months, with a renewed pickup in credit activity and earnings. It may be below the official 8% real GDP growth rate, but is a very respectable pace nonetheless. The external balance is back in surplus on the back of weak imports and low oil prices, inflation continues to fall, the fiscal balance is "just enough" to avoid serious trouble, and the RBI still has room to cut rates at the margin. Jonathan sold his Indian equity position a year ago, and the index has underperformed since then. This is still an expensive market on any valuation metric - but if he really sees the cycle stabilizing and growth maintaining at 5% or more, he is certainly considering a re-entry. Stay tuned.

Commodities

From precious to soft

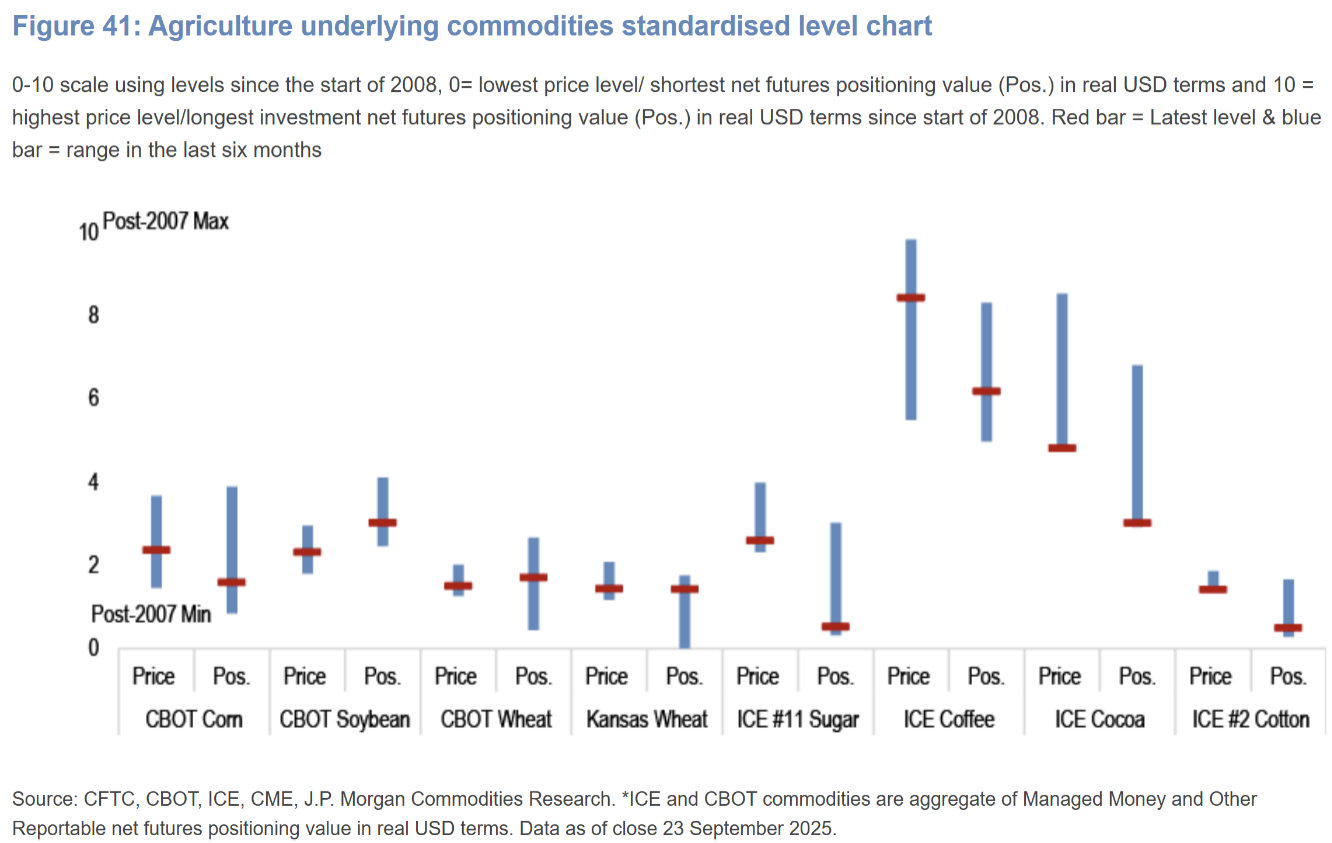

Craig Ferguson has come full circle in recent weeks in his thinking about the beneficiaries of US inflation. For the last few years, he’s been playing gold & silver longs, seeing them as good hedges against a weaker US economy, falling Fed Funds, the USD, and inflation. The story has worked out pretty well for Craig, but now he sees both precious metals as heavily overbought and has now exited his longs. His attention has now shifted to ags, grains, softs and energy commodities, with sugar, wheat and natural gas added to his portfolio to the tune of ~5% exposure. Over the coming weeks, Craig is considering adding corn and cotton and possibly WTI oil to the mix, with the diverse commodities basket potentially reaching 10% of his Growth SMA portfolio.

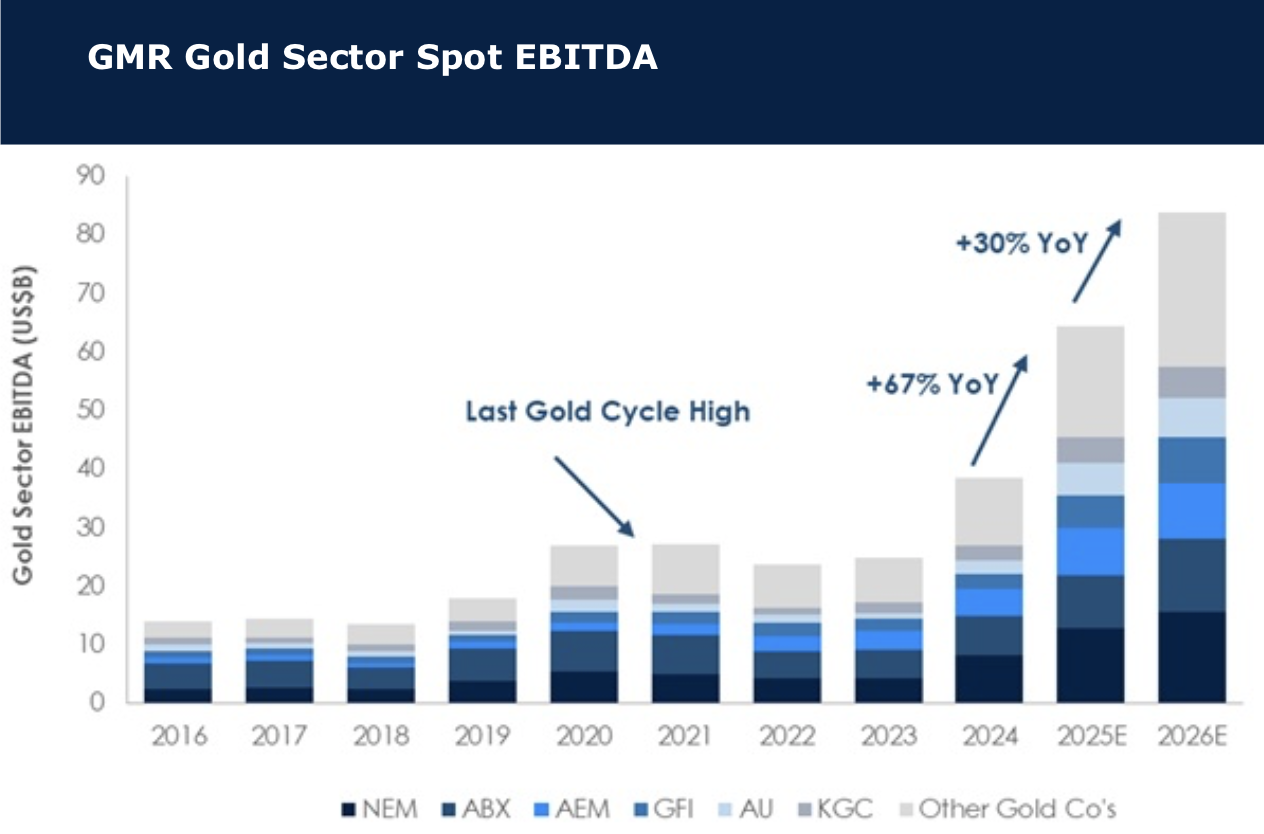

All that glitters is gold

Gold has been setting new highs through 2025 as the best performing major commodity. The music will come to an end, but David Radcliffe says that until that happens, a spot gold price over US$3,800/oz will generate some extraordinary returns. He examines the impact that spot prices could make to a sector that has already benefited from a robust 18 months. The 2026 consensus gold price is ~US$470/oz below spot, implying further upside if prices are maintained. On David’s expectations, spot prices into 2026 could lift sector EBITDA another 30% after an expected 67% lift in 2025. His covered gold stocks trade at a discount with spot P/NPV5 of 0.87x, or an implied gold price of ~US$3,330/oz, a 13% discount. There remains a value argument for gold miners, plus earnings momentum. David’s preferred exposures remain Agnico Eagle, Kinross and Northern Star of the seniors, and IAMGOLD, Equinox and Alamos of the more leveraged intermediates.

Oil: Building up

The US continues to export its surplus to the rest of the world, and inventory builds are underway. A combination of higher floating storage and Chinese inventories is offsetting lower US inventories. In Q3 inventories usually fall on strong demand, but OPEC upping its production has prevented this from occurring, with supply outpacing the seasonal increase in demand. Visible inventories, which Kathleen Kelley tracks, are now above 2022, 2023 and 2024 after a sharp move higher this month, but are still below the five-year average. Given the move higher in inventories, and the anticipated continuation of this trend into Q4, bearishness continues to be near record extremes. Kathleen forecasts a large build in Q4 this year, continuing in 2026 and H1/2027. There are risks to supply that are not priced in that could result in much lower inventories, and a decline in Iranian oil exports would balance the market.