Europe

Time to buy Greece

Greece is healing - after a brutal 15-year wait, the country has finally regained its BBB investment-grade rating from Fitch. Despite chronic under-investment in infrastructure, Greek corporates have expanded at home and abroad and now boast strong balance sheets, often with net cash - a rarity in Europe. Ultra-low labour costs and the highest workload in the EU have boosted competitiveness, while political stability since 2019 has restored investor confidence. Yet Greek equities still trade at half their 2008 market capitalisation, leaving substantial upside for companies that are leaner, stronger and more agile than their European peers. AIR’s Buy-rated ideas include Athens International Airport, Motor Oil, National Bank of Greece and Sarantis, each offering 40-100%+ upside.

Communications

The Chair, CEO, CFO and 2 other executives bought a total of €1.3m of stock at ~€3.70 following share price weakness after the earnings release and a dividend cut. Marc Thomas Murtra (Chairman since Jan 25) bought €500k of stock in his first purchase since joining TEF, Emilio Rodríguez (COO since Mar 25, joined 2018) bought €500k worth of stock in his first purchase since he became declarable in 2025 and Laura Abasolo Garcia De Baquedano (CFO since 2017) bought €91k of stock in her first clean purchase. Pablo Antonio De Carvajal Gonzalez (Divisional Director) bought €126k of stock in his largest purchase and his first since 2019. Juan Azcue Vich (CSO since Jan 25) bought €74k of stock in his first purchase since joining. Whilst a likely co-ordinated response to disappointing news, the magnitude of the purchases is notable.

Healthcare

EKTAB delivered a Q2 profitability beat despite tariffs and FX headwinds, while sales were only slightly soft, helping spark a sharp rebound in the shares. Adjusted EBIT came in 6.5% above expectations and margins rose to 10.1%, supported by mix and pricing. Although China and the US weighed on revenue, order intake grew and China’s book-to-bill ratio exceeded 1.3x suggesting a potential recovery ahead. H2 should be stronger, with improving China trends and US approval of Elekta Evo expected. The new CEO’s restructuring plan - cutting ~450 jobs (10%), simplifying the organisation and cancelling low-quality orders - targets SEK500m+ annual savings. With a robust SEK34bn backlog and solid uptake of new products, AlphaValue maintains a positive view as the turnaround gains traction.

Materials

Ben Jones reiterates his bullish view with the stock up ~200% since initiation in July 23. AAZ is set to enjoy a dramatic increase in net income as well as FCF which is expected to swing from -$2m (2024) to c.$126m (2026) - a 45% FCF yield on today’s m/cap. He expects AAZ to develop 3 new mines (without raising equity) over the next 5 years which will boost copper production from 2.1kt in 2023 to around 40kt per year from 2028. Ben increases his base case price target from £3.70 to £5.59 (150% upside), assuming long-term copper prices at $4.50/lb, but with optionality to £8.00+ if long-run copper averages $5.50/lb, as forecast by Citi and BAML. Since publication of Ben’s report, AAZ has disclosed it is in preliminary takeover talks - unsurprising given his view that the market continues to undervalue the company’s asset base and growth profile.

North America

Identifying stock swaps within your portfolio

Mill Street’s Swap Shop report responds to strong demand from equity portfolio managers seeking to use their MAER model (the Monitor of Analysts’ Earnings Revisions) to identify problematic low-ranked holdings and find high-ranked substitutes that preserve overall portfolio allocations. By leveraging MAER’s powerful intra-sector and intra-industry ranking performance, Mill Street highlights potential swaps within the same benchmark universe and industry, helping managers avoid “portfolio inertia” while keeping sector and style exposures consistent. This month’s screens include global large-cap Value stocks amid the recent rotation from Growth to Value, US Financials and Health Care following Mill Street’s sector allocation changes, and additional screens across the S&P 500 and their European equity universe. Click here to access the report.

Consumer Discretionary

Paragon Intel is bearish on HOG’s new CEO, Artie Starrs, arguing that while he may mend dealer relations and bring an outsiders’ perspective to the company, he is not equipped to deliver the deep brand turnaround required after two prior CEOs already failed to halt the brand’s decade-long decline. Paragon’s analysis includes interviews with Starrs' former colleagues from Yum! Brands and Topgolf. They found mixed and often critical feedback: he is seen as polarising leader, valued by some sources as a strategic thinker with strong financial acumen, boardroom presence and the ability to drive large-scale initiatives, yet criticised by others as overly numbers-driven, aloof and weak at culture-building.

Financials

Abacus revisits BN after a 70%+ rise since their Jan 24 write-up, arguing the fundamentals remain as compelling as ever. They still see a 22% IRR over the next 2 years - even assuming a persistent ~30% SOTP discount. BN’s thesis is simple despite its perceived complexity: a longstanding focus on infrastructure positions it as a major beneficiary of US on-shoring and increased infrastructure spending, while structural growth tailwinds support its insurance and wealth platforms (Brookfield Wealth Solutions is highly attractive at ~1x book, given 15% ROE). Although BN is improving its communication, Abacus argues few investors appreciate the value, leaving ~35% upside to their TP of $63.

Healthcare

Tom Tobin thinks there are several secular trends, including AI tailwinds, which makes RDNT a compelling idea even after its share price has rebounded in recent months. Core to Tom’s thesis is his ability to track Diagnostic Radiology staffing at RDNT, monitor turnover, and forecast volume and revenue per clinician. While the current valuation against consensus estimates appears stretched, he can model upside well into 2027 with a number of simultaneous secular tailwinds that justify the premium: 1) continued inpatient-to-outpatient imaging migration; 2) mix shift towards high-margin advanced imaging where demand is being driven by Alzheimer's, Oncology and Cardiology; and 3) AI tailwinds driving incremental revenue and operating leverage.

Emerging leaders in data & AI

Technology

Channel sentiment this quarter shows mixed momentum across data platforms. Elastic saw fewer partners meeting targets amid rising competition and questions about AI-driven sustainability. MongoDB continues to receive more positive views, benefitting from diversified modernisation wins and strong Atlas demand, setting up for a strong Q4. Snowflake is also receiving strong views as they evolve their partner model with new incentives, expand their work with System Integrators and accelerate AI-driven use cases. Box is sharpening its focus on high-value partners and operational AI workflows. Channels see Box benefitting as end users work to manage unstructured data for AI use cases. Click here to access the report.

Apple: HBM reallocation adds $4bn to iPhone memory bill

Technology

JNK Supply Chain Research reveals AAPL's iPhone memory costs have doubled as a share of BOM - from 5% to 10% - driven by structural HBM reallocation, not cyclical shortage. iPhone 17 Pro Max memory runs $41-$43 per unit vs. $22 in iPhone 15 Pro Max. Across 225m annual shipments, that is $4bn in incremental cost AAPL absorbs through margin compression, not price increases. HBM production for AI accelerators consumes 3x normal wafer capacity. SK Hynix and Samsung control 95% of DRAM supply with all capacity sold through 2026. AAPL negotiates from a position of weakness and there will no relief until late 2027 when new NAND lines come online. For timing of the resulting GM impact, contact us below. AAPL and other smartphone makers are covered in JNK's Consumer Tracker.

Palantir CEO’s defensiveness raises some red flags

Technology

MYST highlights a worrying behavioural shift after analysing CEO Alex Karp’s recent media appearances. Following the stock’s sharp pullback, he has adopted what behavioural economists call “defensive attribution” - a psychological bias where people facing harsh criticism attribute negative outcomes to external factors rather than accepting personal responsibility. Karp’s responses increasingly dismiss critics, question motives and escalate into personal attacks. While MYST are not insinuating PLTR is a fraud or a bad business, his rhetoric mirrors CEOs from some of the biggest corporate scandals.

Technology

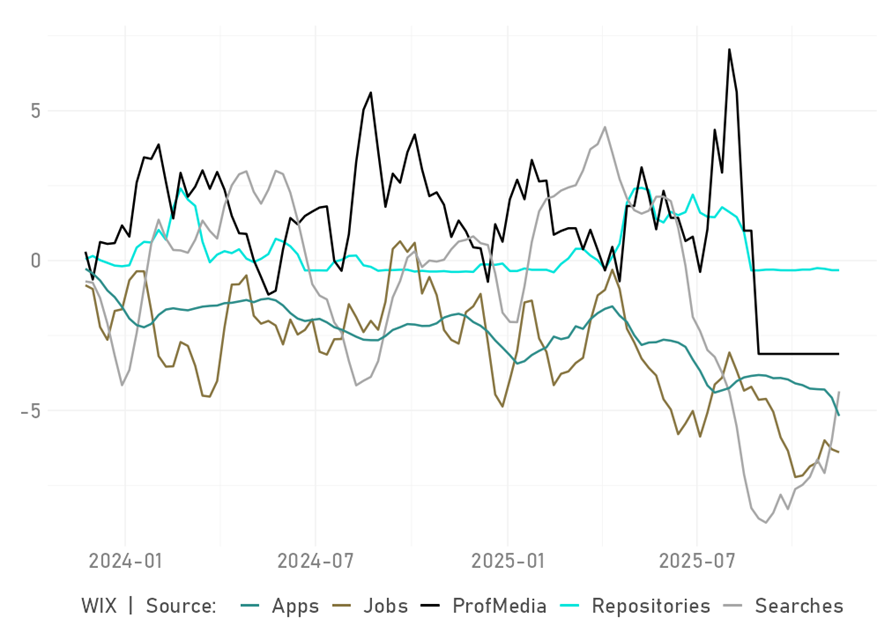

AnteData flags a sharp deterioration in developer engagement around WIX in 2025, with a TrendRank of just 0.02 - near the bottom of their software universe. GitHub pushes and Stack Overflow discussions are especially weak, signalling that fewer developers are building WIX-related code repositories and that community interest is fading. In contrast, website-building tools Vercel and Webflow show rising coding activity, which indicates a shift in website architecture. WIX holds only ~5% of a market dominated by WordPress (~40%) and Shopify, and AI tools plus social platforms are eroding demand for traditional no-code site builders. The stock has fallen 50% YTD, bringing its Price/Sales ratio down to a moderate 3x. However, the Street still expects DD sales growth. And the stock is not yet priced like low-growth comparables such as GoDaddy or Dropbox, suggesting further downside potential.

Technology

ZM delivered a "clean sweep" Q3 that should silence the sceptics. This was not just a beat-and-raise quarter; it was a validation of the company’s structural pivot from a meeting app to an AI-first work platform. With revenue and EPS ahead of forecasts, a raise in FY26 guide and a fresh $1bn buyback authorisation, management is demonstrating immense confidence in the company's capital allocation and operational execution. The real story for investors, however, is the tangible monetisation of AI: usage is up 4x Y/Y and paid AI features are now anchoring 9 out of 10 large CX deals. With the core business stabilising and the AI/CX growth engines firing on all cylinders, ZM offers a rare combination of deep value (trading at ~3.2x EV/Sales vs. peers at 3.7x) and highly profitable growth.

Developed Markets

UK Budget is negative for economic growth

Mark Bathgate's initial thoughts on the overall shape of the UK Budget is welfare spending and taxes up a lot, borrowing up in the first two years of the budget period, with most tax hikes coming years 4 and 5. He points out that the Budget looks to be negative for growth – primarily via the further decline in household real after tax income, and likely impacts on confidence from the messy process of recent weeks and prospects of many years of rising taxes. Moreover, three key expenditure areas have not been addressed which questions the sustainability of the current budget:

* defence spending (no funding for NATO commitments entered into at June summit);

* Ukraine 2026 & 2027 budget which UK is publicly committing to contribute significantly to;

* local government financing crisis.

Overall, Mark says this looks to maintain the trend we’ve seen over the last 15 months: higher borrowing; lower economic growth; steeper gilt yield curve/higher long gilt yields; and more speculation about next round of tax hikes. However, Mark also says that one positive is that there are less inflationary risks relative to the previous budget.

US Tariffs – Trump’s IEEPA alternatives

Although the timing of the Supreme Court’s ruling on the legality of President Trump’s use of the International Emergency Economic Powers Act (IEEPA) to impose tariffs is uncertain, the Trump administration's stance remains one of confidence, despite the perception after the hearing that it is likely to face at least some restrictions. However, if the duties were to be struck down, there are other authorities that the White House might rely on to impose tariffs, with Sections 232, 301, 338, and 122 being possible alternatives. Of these, Section 338 imposes the fewest restrictions on Trump, with the only meaningful restriction being that the tariffs it authorizes are limited to 50 percent, which is higher than any current reciprocal tariff level. The most significant risk of using this authority, though, is that it has no history of use since its creation in the Smoot-Hawley Tariff Act of 1930. This lack of precedent means the president’s efforts to use this authority for tariffs could face legal challenges.

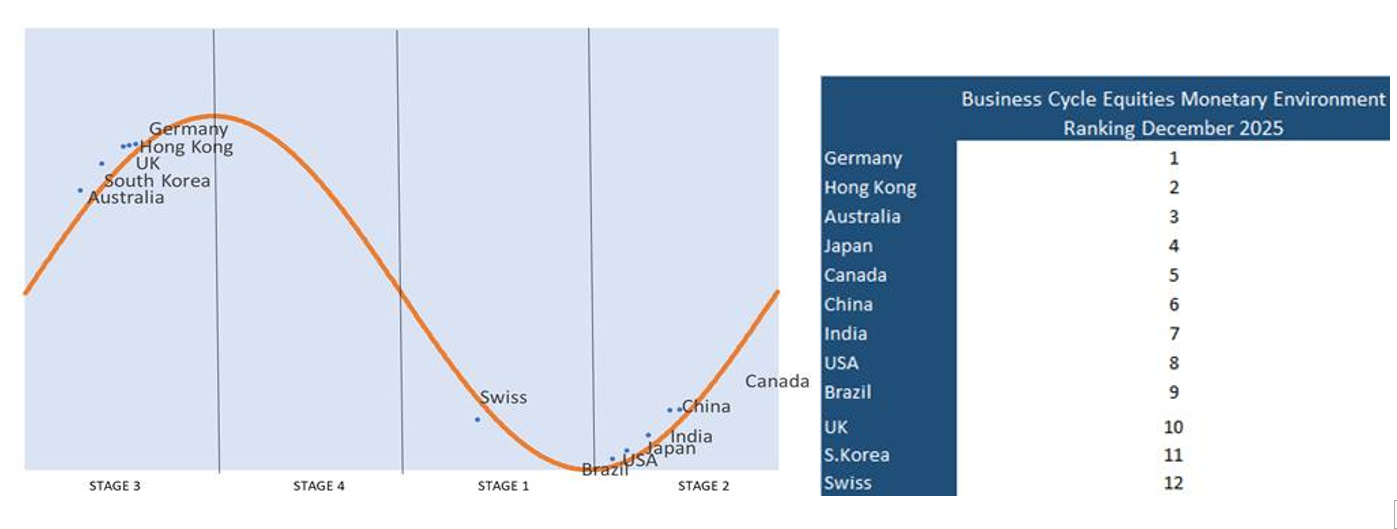

Global Equities Tactical Asset Allocation – Germany moves into late-cycle Stage 3

In this report Frank Shostak describes his highly dynamic equities tactical asset allocation framework which delivers specific country capital allocations down to the sector level. In the latest monthly report, Germany rotates into the late cyclical Stage 3 of the business cycle, joining the US, Eurozone, UK, Canada, Australia, Brazil, India, China & South Korea in exhibiting monetary tailwinds. In contrast Switzerland alone continues to exhibiting monetary headwinds ahead. According to the AASE analysis, the cycle itself is a function and product of fluctuations in the rate of growth of money supply, which provide a very reliable leading indicator of business activity, and Stages 2 and 3 correspond to periods of expansion in (lagged) money supply. The chart above shows a visual illustration of where each country will be in the business cycle for the upcoming month. By combining the business cycle staging with Frank’s Liquidity measure AASE derive a country rank, the current state of which is shown in the table above. Sector allocation in each country is determined as per AASE’s sector allocation framework, whereby different sectors of the stock market perform better in some stages of the business cycle than do other sectors.

September US retail sales up modestly but Q3 still strong

John Ryding points out that while the increase in retail sales was modest in September, for the quarter as a whole, sales were relatively solid with the control group measure of retail sales rising at the fastest rate (6.3%) since the first quarter of 2023. Core producer price inflation held steady in September at 2.9% but the increase over the last three months was a more rapid 4.7%. Jumping ahead to November, however, consumer confidence fell more sharply than expected as the median one-year inflation rate edged up to 4.8% from 4.7%, households’ perceptions of the labor market declined, and plans to buy autos and cars fell. John doesn’t see this report materially shifting the debate at the FOMC meeting on December 9-10 with the cut camp finding comfort in the inflation readings holding steady and the hold camp seeing potential faster price pressures in input costs and higher frequency inflation rates as well as the strength in retail sales for the quarter as a whole.

US consumer confidence fell 1% in October

Carl Weinberg notes US consumer confidence was down again in October, with the Conference Board’s headline index continuing its jagged course toward the southeast corner of the chart. Expectations declined, too, and so did the index of current conditions. These confidence indices are very low, well below levels seen just before the Covid lockdowns. Carl says consumers are rattled. The survey indicates that the labour market is tight but jobs have become harder to find in recent months. The inflation expectations index for one year rose, seems to have steadied, but is still extraordinarily high! Carl believes consumer confidence this low will add to the arguments in favour of a rate cut at the FOMC… not a lot, but they do imply a slowdown of consumer spending. Whether or not that might not be a good thing—since the economy is at full employment anyway and cannot produce much more goods or services near term—is a question the FOMC should be debating.

European budget deficits are overshooting

Wolfgang Munchau points out that Finland, traditionally a fiscal hawk, has entered the excessive deficit procedure. Wolfgang says that this is a canary in the coal mine of what is yet to come. He sees overshooting budgets everywhere in Europe - a result of structural shifts in the global economy, and fiscal overcommitment since the pandemic. These shifts are also reflected by persistently over-optimistic fiscal forecasts. European governments have yet to come to terms with the fact that debt and deficit levels are incompatible with their commitments. They cannot simultaneously spend more for defence and the support of Ukraine when their economies are not growing, and maintain their tax policies, public spending commitments and deficit targets. Social welfare systems also cannot afford to stay as they are as working age populations are shrinking now that the baby-boomers are retiring. These are structural shifts Europeans are trying to band aid over with quick fixes.

Watching The Tides – The ECB’s search for a new normal: QE, QT, QN

Although the process of monetary policy normalisation in the euro area is well under way, expressed as a share of GDP, total Eurosystem assets are still double what they were a decade ago. The ECB recently laid out its vision of what the journey from QE to QT to QN is likely to involve: the banks and the sovereign bond markets now need to adjust. In this article, Marcel Alexandrovich focuses on the Eurosystem (which is made of the ECB and the 20, soon to be 21, National Central Banks). The first point Marcel makes is that just as the aggregate banking data often disguises what’s actually going on at the country level across the euro area, the same is true when analysing the aggregate Eurosystem balance sheet. Repayment of the Longer-Term Refinancing Operations (LTROs) and QT are reducing the size of the ECB’s balance sheet. One thing which is not clear, however, is who in the future will end up holding the large volume of European sovereign debt that currently sits on the balance sheet of the European banking system.

Emerging Markets

Argentina – Economy grew 5.0% year-on-year in September

The Argentine economy expanded 0.5% month-on-month in September, much better than Jorge Morgenstern’s expectations, according to the GDP proxy EMAE. Activity grew 5.0% year-over-year. There were significant upward revisions of previous data, with August now 0.9% higher than previous data release and monthly expansions since July. While the economy expanded 5.2% yoy in January-September (5.4% using the seasonally adjusted series), activity in September was 0.2% above February’s peak. As a result, GDP expanded at a seasonally adjusted annual rate of 1.9% in 3Q-2025 following a 0.2% contraction in 2Q-2025, dodging a technical recession.

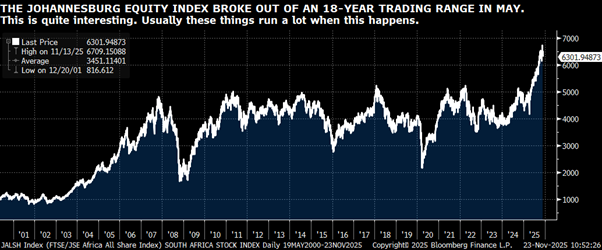

South Africa: Johannesburg equity index breaks out

Mike Churchill says that the African countries that are realistically investable (critical mass of stocks + decent macro) are South Africa, Mauritius, Tanzania and Kenya. Two “maybes” are Egypt and Nigeria (lots of stocks but bad macro track records). He says African banking is a good business – but insurance is not. For South Africa, Mike observes that the country is run as a partnership between elite capital and the populist ANC. The official rhetoric is populist but illegal immigration is rampant and the capital gains rate is 18%. So companies do well. As the chart above shows, Johannesburg stocks are breaking out of an 18-year trading range in USD terms -- and there are a lot of stocks to choose from.

China’s slump deepens

China’s domestic economy is deteriorating. Andrew Hunt asks if this could lead to a degree of angst within the population? Domestic policy conditions look to have tightened: fiscal policy is notably less expansionary, and liquidity growth has cooled as a result. Equities appear less well bid and the rally may have stalled. Andrew also points out that the corporate sector’s weak financial situation has led to a reduction in China’s once aggressive rate of exportation of private sector capital. China is now a deflationary force within the global economy. The PBoC has acted to suppress the rise in the CNY via hefty FX intervention. Presumably, the weakness in the domestic economy will lead to another round of easing within China’s fiscal policy at some point, although concerns over fiscal sustainability could delay this action. Andrew says global investors should pay close attention to China’s fiscal stance and the nature & quantum of its capital outflows. These may yet hold the key to determining “the top” in global risk markets.

Brazil Central Bank waiting for clear signal on inflation

The BCB Director of Monetary Policy and Deputy Governor, Nilton David, opened his remarks at the Brazil Treasury Summit by highlighting that the rate-hiking cycle is over and that raising the Selic is not part of the baseline scenario. He stated that the priority now is understanding when the cutting process may begin, something fully conditioned on data convergence. He stressed that the Central Bank is waiting for clear signs of inflation and expectations easing before moving forward, and that forward guidance is not appropriate in a highly uncertain environment. According to Andrea Damico, David’s remarks reinforced the sense of a technical Central Bank highly focused on keeping expectations anchored, aligned with recent speeches by President Gabriel Galípolo. The communication emphasized the priority of preserving credibility, avoiding unnecessary volatility, and consolidating the disinflation process. The messages indicate confidence in the effectiveness of monetary policy, while acknowledging that full convergence still depends on a lower-uncertainty environment and disciplined communication. Overall, the tone reinforces prudence, mandate focus, and continuity in strategy.

Chile – Market signals scope for further interest rate cuts

In terms of interest rates, declines continued, albeit modestly, in line with the recent trend. In particular, nominal swap rates fell by an average of 3 basis points since the previous report, although this time Igal Magendzo observed some shifts in trend compared with recent weeks. Igal notes that the market continues to assign a high probability to a reduction of the Monetary Policy Rate (MPR) to 4.5% at the December Monetary Policy Meeting (MPM), consistent with his base case. It also now prices in a second additional 25bp cut during the first half of 2026. However, it still does not fully incorporate the idea of a 4% terminal rate, which the Central Bank has been signalling for quite some time. Regarding Igal’s base case, the latest macroeconomic data continue to indicate that the economy is operating close to equilibrium, and therefore near the neutral rate. As such, it would take evidence of a meaningful weakening in activity or more persistent downward pressure on inflation to justify taking the TPM below 4.5%.

The Philippines – Protests will not confront Marcos, but the president remains at risk

Major anti-corruption rallies are scheduled throughout the country for 30 November. Civil society groups primarily associated with the middle class — such as the Catholic Church, private universities, professional groups and the business community — are taking the lead. The loose coalition leading this weekend’s protest is critical to political stability, given its prominent role in shaping the broader media narrative and eventually mobilizing the broader population. The consensus view in Manila is that while the broader coalition is calling for accountability and reform, it is still not yet aiming to target President Ferdinand Marcos Jr. directly. Instead, protesters are expected to apply indirect pressure by calling for the president to allow for investigations to continue unimpeded and for the prosecution of high-ranking lower house, senate and executive officials. One key reason for the coalition’s less confrontational stance toward Marcos is that they are less certain that the president himself participated. Driving this consideration is the coalition’s deep unease over the prospect of Vice President Sara Duterte succeeding to the presidency.

Commodities

Back into gold

Charles Ekins wrote on 9th October that gold was extremely vulnerable because it had the reached the second most overbought level in 45 years at over 3 standard deviations (in terms of deviation of its price from its trend). In the EG Chartbook in early November, he reported that their model had by that stage significantly reduced the gold allocation in their multi-asset model portfolio. That model has now moved back into gold. Although gold did fall back from its peak of just over $4,350 on 20th October to below $4,000, given the level of extreme overbought, that correction in gold could well have been more extreme – so caution was warranted. However, gold has in fact stabilised and is now pushing on upwards again. The overbought "steam" has subsided somewhat - it is still vulnerable but less so. The renewed momentum has triggered a move back into gold by their model for the time being.

Lumber price decline continues

Lumber price declines continued unabated in S-P-F last week, with 2x4s off by a further $15 at just $395. More S-P-F supply is coming out of the market this quarter, but with little excitement about H1/26 demand prospects, buyers appear to have shrugged off recent mill curtailment announcements and remain happy to operate on a hand-to-mouth basis. In SYP, 2x4 prices were flat at $326 as upcoming holidays (and disruptions to production schedules) had very little impact on trading. ERA expect that prices across North America will be flat-to-down through year-end, and Q1/26 pricing will be driven by changes to supply—clearly, more sawmill downtime is needed.

Gold and silver to remain volatile with underlying strength

Jeffrey Christian of CPM Group discusses the increasingly unstable economic and political environment and what it means for gold, silver, and broader precious metals markets. He compares today’s conditions with the late 1970s, noting both the similarities and critical differences to that period, and what those differences may mean for gold and silver prices. Jeff looks at the volatility across gold, silver, platinum, and palladium, explaining the factors influencing investor anxieties. He also discusses economic shifts, including weakening U.S. influence on the global stage. The video concludes with a look at inflation data, consumer behavior, policy risks, and why CPM Group expects a recession within the next 12–24 months.

Click here here to watch

Fears of lower oil prices may be too pessimistic

While market participants await to see what, if any, peace accord emerges from the current Russia-Ukraine talks, William Brown notes that Wall Street analysts appear to be leapfrogging over one another in terms of how bad the global oil “surplus’ will be next year and beyond, and in turn how low oil prices could go. Once again, as William has discussed over the years, analysts always qualify their either extreme bullish or bearish price forecasts with “could” and not “will”. Be that as it may, he notes that one bank he has now heard from is JP Morgan, who suggests that Brent, again “could”, plummet into the $30s due to an “overwhelming” market oversupply. Meanwhile Goldman Sachs are reiterating their bearish view, estimating an average 2.0 MMB/D surplus in 2026, leading to a Brent average of $53.00 per barrel. In contrast, William’s view is the opposite, given what he estimates to be the substantial net short position investors and funds have already amassed.