Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Overlooked opportunities in YWR’s QARV rankings

Why do China, shipping, iron ore, hardware, Brazil… all stand out if you screen high ROE’s with low valuation? Erik@YWR sees it as scepticism about global growth on which he is taking a contrarian view. Following this month’s review of YWR’s QARV rankings key themes include: 1) A massive China bull market has only just begun. 2) Opportunities in iron ore, where Fortescue, Rio Tinto and Kumba are delivering ~20% ROEs at <12x P/E despite China’s property crash. 3) The Taiwanese semiconductor supply chain stands out as highly profitable and undervalued. Everyone focuses on Nvidia and the datacentre buildout but misses the whole Taiwanese supply chain behind this. Tokyo Electron and ASML also screen well. 4) Brazil is overlooked, with names like Itau, Vale, Ambev and B3 all screening well. 5) Container shipping - supply-chain diversification could sustain tighter freight rates than investors expect.

Edition: 220

- 19 September, 2025

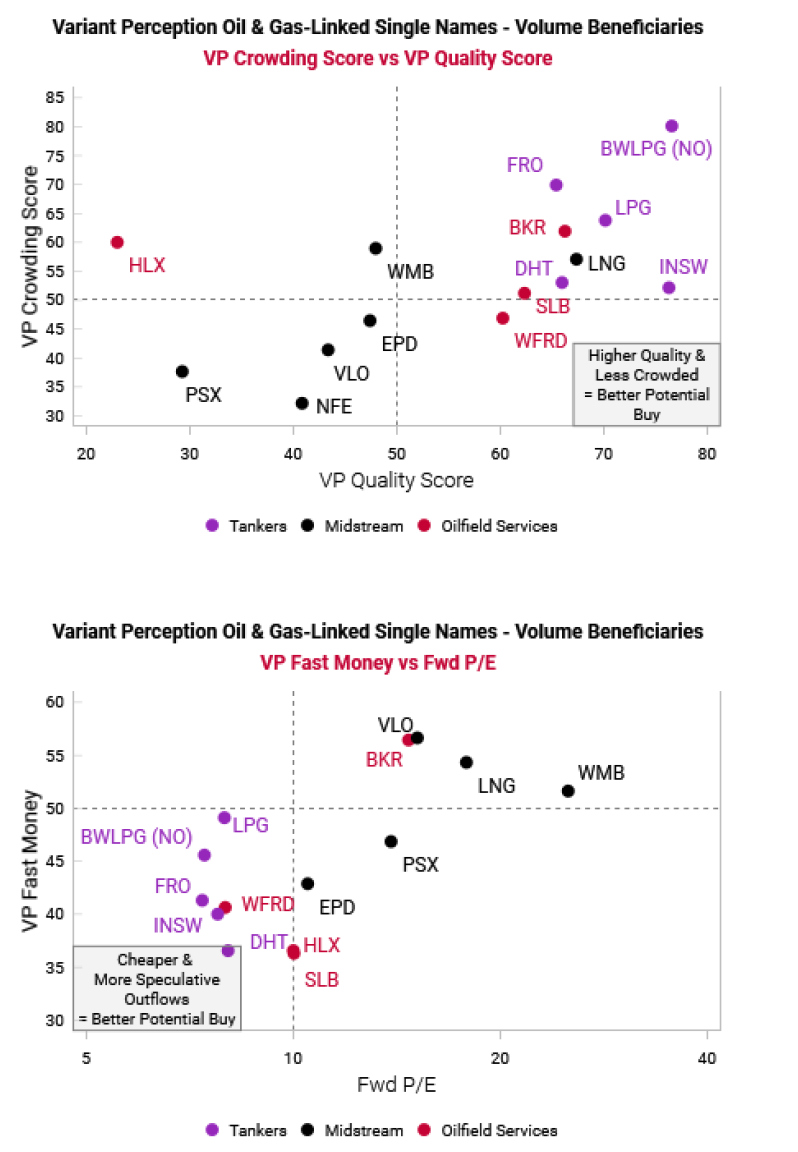

Pockets of value emerging in energy-linked single stocks

Variant Perception’s team suggest that underperformance in the energy market may continue, but they still see an opportunity for select single names if/when their tactical models turn bullish. They examine the market for single stocks that have favourable business models that benefit from higher volumes for oil and gas, and that screen well on VP metrics like capital cycle, crowding, and quality. Oilfield services, midstream and tankers are well suited, US-listed oilfield services are not. Despite appealing valuations, some midstream names still offer reasonable upside and volatility. However, among tankers, the team are highly cautious on LNG and product tankers as these have a glut of new builds coming online in the next few years relative to the existing fleets. Potential plays include Schlumberger, Baker Hughes, Enterprise Products Partners, Frontline and DHT.

Edition: 216

- 25 July, 2025

Vista Energy (VISTAA MM) Mexico

Energy

EM Spreads recommends buying Vista’s new 2033 bonds, citing an attractive 8.5% yield and shorter duration relative to the 7.625% 2035 notes (yielding 8.3%). The bonds offer a more compelling return within Vista’s debt capital structure and screen wide relative to the broader EM BB and LatAm BB curves. Strong execution on well tie-ins and midstream expansion supports the group's ambitious EBITDA and production targets. EM Spreads views Vista as a top credit pick for exposure to Argentina’s energy sector, with relative insulation from sovereign risk. They believe operational momentum and an improving macro backdrop, including easing capital controls, could drive bond outperformance over the next 9-12 months.

Edition: 213

- 13 June, 2025

Large cap growth screen

The point of Willis Welby’s Japan screen is not just to find stocks with growth that will compound value, but to find them at reasonable prices. They begin the process with 175 stocks with market caps north of USD 5bn. 71 have consensus Y3 revenue growth in excess of 5%. And of those, 46 pass Willis’ financial productivity and sector parameters. When they add the parameters of reasonable financial productivity and an implied to Y3 EBITM ratio of less than 110, they end up with 23 names. Focus stocks this month include Ebara, M3 and Hoshizaki.

Edition: 197

- 18 October, 2024

Technology

DGII has hit a wall in its attempts to transition from a product-reliant company to a subscription-based one. Revenue has started to decline, even with evidence of aggressive revenue recognition (surge in DSO, excess inventory at customer locations) and potentially aggressive accounting (inventory transferred to PP&E, recent SEC comment letters). While the shares screen as cheap, Corto believes there is 50%+ downside here with peers trading at revenue multiples closer to 1.0x vs. the company's current 2.8x multiple. The shares have rallied 30% over the last three months, in spite of horrible guidance revisions.

Edition: 197

- 18 October, 2024

InterContinental Hotels Group (IHG LN) UK

Consumer Discretionary

Willis Welby remains of the view that the UK has plenty of interesting and growing businesses. IHG features in their latest large cap growth screen - it has great financial productivity and is clearly winning market share. Dollar weakness does not help but the implied to Y3 EBITM ratio is just 84. It is too low. Hilton and Marriott are on 135 and 114, respectively. IHG would make sense GBP20 higher than it is now. Other stocks highlighted include QinetiQ (there is a good fundamental story here alongside some very cautious expectations. Despite a Q2 rerating, the implied to Y3 EBITM ratio is still only 65) and GlobalData (the disposal of part of the Health franchise may prove seminal. Management is talking organic growth >10%, margins drifting higher and accretive roll-ups).

Edition: 194

- 06 September, 2024

Universal Scientific Industrial (601231 CH)

Technology

Within Creative Portfolio’s extensive global equity universe, they screen for the best combined ranked stocks focusing on Valuation, Profitability, Piotroski and Accruals. Paul Hollingworth thinks Universal Scientific Industrial offers a compelling technical-fundamental opportunity. The current valuation only points to a modest pick up in EBIT margin and ROE which he feels is too pessimistic. Furthermore, the company's balance sheet is rock solid and its FCF Yield looks attractive. Using a discounted cash flow model, Paul sees fair value at CNY40.45 (60%+ upside).

Edition: 194

- 06 September, 2024

UK: Plenty of interest

The Willis Welby team revisits their review of UK growth names they put in place at the start of 2023. They have 104 stocks in their UK coverage with market caps north of USD 2.5bn. Nineteen of them make their screen of consensus Y3 revenue growth in excess of 6%, reasonable financial productivity, and an implied Y3 EBITM ratio of less than 110. The performance of this approach has been okay since May 20, with the mean move of the 18 names at -0.8%, which is ahead of the -2.1% return from the FTSE 350. The team remains of the view that the UK has plenty of interesting and growing businesses. And enough of those names are still available at attractive prices, including the likes of Sage, Convatec and IHG.

Edition: 189

- 28 June, 2024

China Banks: Deep value despite the NPL challenge

Financials

Galliano's Financials Research

In Victor Galliano’s China banks screen, he focuses on the credit quality headwinds going forward, as well as the returns trends that can absorb potentially worsening cost of risk charges. While China bank shares continue to be poor performers, Victor sees selective contrarian buy opportunities for those banks with deeply discounted valuations and strong balance sheets including credit quality metrics. He upgrades Ping An Bank to Buy and continues to favour Industrial Bank and CCB, although Minsheng remains a Sell.

Edition: 171

- 13 October, 2023

Screening UK Stocks: Combining quality, momentum and expectations indicators

Methodology - the initial universe are stocks with $2bn+ M/Cap. After that Willis Welby starts with a quality cut off based on their measure of Intrinsic Return on Capital Employed. They then narrow down using a combination of share price momentum and EBIT revisions before incorporating their expectations analysis via their measure of the implied to Y3 EBITM ratio. This has been another month of low turnover for the UK screen and it is notable that stocks coming in are exclusively in Consumer Services with the return of three retailers (B&M, Pets at Home, WH Smith) and Flutter. The four stocks leaving are Burberry, IAG, Hikma and Serco.

Edition: 166

- 04 August, 2023

Technology

Amir Anvarzadeh has been bullish the stock for much of the past 3 years and the share price is up 38% since he added SCREEN back to his buy list in early Nov 22. Despite this strong performance Amir still thinks it looks very undervalued, especially given the firm's high exposure to EUV and logic chips and its low exposure to memory which has insulated the name from weak order trends seen by its bigger peers, namely Aysmmetric's two short sell picks, TEL and Lasertec. Trading at a significant discount to its front-end equipment peers, at around 10x P/E and 4.6x EV/EBITDA, Amir thinks SCREEN should be trading closer to ¥20K (75% upside).

Edition: 160

- 12 May, 2023

Materials

ROCGA’s proprietary Cash Flow Returns On Investments based platform helps identify and value companies. WOR appears on an enhanced US GARP screen. The company has been modelled, valuation back tested, and projected forward using expected earnings, and is looking undervalued. A total of 57 companies appear on this screen and warrant further investigation. The screen can be adjusted to target US large or small, UK large, or small, & Europe. Once identified, ROCGA’s Cash Flow Returns On Investments based systematic DCF models will help determine valuation. Click here for further details. A free trial is available on request.

Edition: 160

- 12 May, 2023

Umicore (UMI BB) Belgium

Materials

ROCGA’s proprietary Cash Flow Returns On Investments based platform helps identify and value companies. UMI has been identified on an enhanced GARP screen. The company has been modelled, valuation back tested, and projected forward using expected earnings. It looks undervalued using the systematic DCF analysis, as well as historic valuation ratios. A total of 123 companies appear on this screen and warrant further investigation. ROCGA currently covers c.2000 companies across Europe and the US. More details on ROCGA’s systematic and interactive valuation tools can be found here. A free trial is available on request.

Edition: 159

- 28 April, 2023

Does gold M&A create value? A rational screen offers clues

The recent proposed offer by Newmont to acquire Newcrest demonstrates that corporate M&A is alive and well in the gold sector, but it also raises the question as to whether it creates value. David Radclyffe’s latest report analyses major mergers over the past five years in the gold sector, concluding that most deals do not create lasting value – less than one-third show positive returns a year after the deal. Global Mining Research have developed a screen to explain why some deals generate a positive initial market reaction and others do not, providing investors with a ready tool.

Edition: 154

- 17 February, 2023

Screening UK & Europe: Combining quality, momentum and expectations indicators

Methodology - the initial universes are stocks with $2bn+ M/Cap in the UK and $5.5bn+ across Europe. After that Willis Welby starts with a quality cut off based on their measure of Intrinsic Return on Capital Employed. They then narrow down using a combination of share price momentum and EBIT revisions before incorporating their expectations analysis via their measure of the implied to Y3 EBITM ratio. This month sees 6 stocks enter the UK screen (including Rio Tinto, Flutter, Renishaw) and 17 names added to the European version (including Nestle, Hapag-Lloyd, Roche, Vestas, Aker).

Edition: 140

- 22 July, 2022

Buy Chinese equities, short Chinese government bonds

Deep Macro’s Turning Points Trade Tool superimposes phase angles of market conditions on top of the macroeconomic state in order to effectively screen for high conviction macroeconomic transitions and trades. Their latest recommendation is to go LONG China equity via the Shanghai SE Composite Index, since cyclical trends and inevitable policy measures will bring about a market rally, and to short China’s govt bonds. To play it right, investors should offset with short NZDUSD and short UK equity which are not normally pro-cyclical trades.

Edition: 118

- 03 September, 2021