Europe

Insight’s global Infrastructure stocks offer average upside of over 80%

Robert Crimes remains bullish on the Infrastructure sector, citing strong long-term traffic growth, resilient IRRs (averaging 11.3%, +290bps above Insight’s 8.5% Ke) and deep value in listed equities trading ~40% below NAV, despite private market transactions averaging just -3% below NAV over the past decade. Towers top the table with +136% weighted average upside, with Robert favouring Cellnex over Inwit. Railroads rank second at +113% average upside, favouring Canadian National Railway over Union Pacific and Canadian Pacific Kansas City. Contractors offer +74% upside, with Ferrovial standing out vs. Eiffage and Vinci. Airports offer +42% upside but stronger opportunities are seen in Europe with ADP, Aena and FH Zurich all offering 60%+ upside. In Toll Roads, average upside is only +19% but stock selection is key, with Salik Robert’s preferred pick.

Consumer Discretionary

Revelare offers a differentiated bullish angle on DIE, which controls 50.3% of Belron, the world’s largest vehicle glass operator and owner of Safelite. The analysis argues Belron is uniquely positioned to expand gross profit dollars and EBITDA margins thanks to unmatched buying power and a higher proportion of US-manufactured glass, including close ties to Fuyao Glass’s US facility. In a tariff-driven pricing environment, Safelite can either raise prices in line with the industry while enjoying lower COGS, or raise prices less aggressively to gain market share. A further tailwind is stabilising car insurance pricing, easing claims avoidance and supporting volumes. Given recent media reports, it seems that Belron’s private equity shareholders, have waited for this to happen before considering an IPO.

Materials

GMR is sceptical on a potential tie-up between RIO and GLEN, citing material integration and execution risks. They highlight stark contrasts in management culture and business models, alongside challenges around thermal coal exposure, sovereign risk tolerance and regulatory scrutiny given combined copper output. Assuming US$1.5bn of annual synergies, GMR estimates RIO could bid up to £5.40 per GLEN share for the merger to be, on average, neutral on Earnings/share and NCFO/share out to 2028. Following GLEN’s recent rally, GMR downgrades the stock to Hold and moves RIO to Sell on deal risk. Their proprietary Acquisition Rationale score reinforces caution: GlenRio scores just 9/18, a level that historically underperforms peers over the next 24 months.

Technology

the IDEA! highlights a strong finish to 2025 for ASM, with Q4 revenue of €698m and bookings of ~€800m, both well ahead of guidance. The beat was driven by robust demand in advanced logic/foundry and solid spares & services sales, alongside a late-year rebound in China orders. Encouraged by the improved bookings trend, ASM guides for healthy revenue growth in 1Q26 vs. 4Q25. While the company’s backlog has come down from its record peak, the net sales-in-backlog ratio remains elevated at 4.2 months. the IDEA! also points to TSMC’s sharply higher capex outlook as reinforcing confidence that AI-driven investment will continue to benefit leading semiconductor equipment suppliers like ASM.

North America

Earnings season screens

Mill Street has developed an "Earnings Screen Score" ranking methodology that draws on selected inputs from their MAER (Monitor of Analysts’ Earnings Revisions) stock database to identify companies which have strong near-term fundamental momentum going into an earnings report. Mill Street’s research indicates that companies scoring highly in their ranking have a much higher chance of near-term improvements in analyst expectations than those that score poorly. Stocks most likely to produce positive near-term analyst estimate activity in the next couple of weeks include Lam Research, Regeneron Pharmaceuticals and Teradyne. Bottom ranked stocks include LyondellBasell, Eaton and Marathon Petroleum. Click here to access the full report.

Doubles & Halves Idea Forum

At MYST’s latest buyside event ideas spanned multiple sectors, with many of the long recommendations skewed towards small caps offering multi-bagger potential, driven by substantial operating leverage. These included A2Z Cust2Mate, Bed Bath & Beyond, Brookdale Senior Living, NioCorp, OptimizeRx, Vor Biopharma and Vuzix. Other notable themes included “AI Losers” such as H&R Block and Reddit; “AI Winners” including Mobileye and Spotify; lower-rate beneficiaries like Figure Technology and LendingTree; and positive management change stories such as CAE and GXO Logistics.

Consumer Discretionary

A debt-free company with robust cash flows, CHWY boasts a dominant and growing market share in an industry that is not only adding customers each year but also seeing rising spend per customer. KCR - former bears now turned bullish - highlights CHWY’s resilient, subscription-heavy model, with 84% of revenues recurring, strong demographic tailwinds and a fully built, highly automated fulfilment network that drives meaningful operating leverage as volumes scale. Despite offering better growth prospects and carrying lower risk, CHWY trades at ~21x forward P/E, a ~10% discount to the S&P 500 and at <19x EV/adjusted EBITDA vs. ~25x for the index. With margins at ~5.4% and a credible path towards 10%+, each 100bp margin gain could add ~$6 per share, supporting a compelling re-rating case.

Consumer Discretionary

FY26 marks an inflection point as US comps benefit from secular demand tailwinds and expenses tied to re-accelerating store growth reach equilibrium. SVV IPO’d in 2023 and the shares have de-rated on Canadian inconsistency and near-term margin pressure, yet the underlying economics remain compelling: ~14% EBITDA margins, strong FCF (>EPS), inventory turns >20x and estimated lease-adjusted ROIC in the low 20s with cash-on-cash returns >50%. In the US, affordability pressures and sustainability-driven thrifting are driving momentum, with 4QFY25 comps up 8.8%. Furthermore, recently re-ramped new store openings will start entering the comp basis and could contribute 2-3% annually to comps. Trading at just ~8x EV/EBITDA, John Zolidis sees ~40% upside at 10x his FY27 forecasts, with significant optionality from multiple expansion.

Canadian MICs: The bloom is off the rose

Financials

After several years of rapid growth, Canada’s Mortgage Investment Corporation sector is entering a more challenging phase. Canadian home prices have declined ~20% from the 2022 peak, refinancing rates remain elevated and liquidity pressures are becoming more visible across the private lending market. Over the past two years, these pressures have surfaced through gated redemptions, fund wind-downs, secondary offerings to meet investor liquidity demands and even regulatory interventions, including OSC cease-trade orders. In this report, Veritas reviews 30+ public and private MICs. They exhibit a wide dispersion in underwriting discipline, liquidity management and portfolio risk, which will undoubtedly leave some lenders significantly more exposed as housing markets soften and refinancing pressures build and consequently make them vulnerable to distribution cuts and/or constraints on investor redemptions.

US Healthcare + Merger / Arb Catalysts: What’s next from DC

Healthcare

2026 is shaping up to be an active year for US healthcare policy, with President Trump's focus on affordability impacting Congressional and Administration priorities. Near term, Congress is considering spending legislation impacting clinical labs (Quest Diagnostics, Labcorp), diagnostics (Natera) and life science tools (Danaher, Thermo Fisher). Investors are also awaiting clarity on MFN deals and their impact on companies that have not yet signed agreements with the Administration. Beyond HC, Aldis also leverages their connectivity to provide timely insights and updates around M&A with regulatory catalysts, including Nexstar-Tegna and Union Pacific-Norfolk Southern. Contact us below for further information on events hosted by Aldis and access to their content library.

Healthcare

While Q4 revenue modestly beat consensus, growth slowed to the lowest level in five years and 2026 guidance points to further deceleration, limited operating leverage and weak FCF. Bulls were clearly disappointed as the stock traded down >20% on the day. In OWS's last update, they wrote that ATEC would struggle to deliver on profitability and cash flow targets without negatively impacting revenue growth, which they expected would decelerate substantially going forward. Moreover, they noted that ATEC’s FCF benefitted from unsustainably low investment in inventory and capex, setting bulls up for disappointment in the coming quarters. Their thesis appears to be playing out. A recent share bounce on takeout speculation following Boston Scientific’s acquisition of Penumbra is seen as misplaced, with large players exiting the spine market in recent years and ATEC is not cheap at ~3.5x EV/S. TP $10.50 (40% downside).

Healthcare

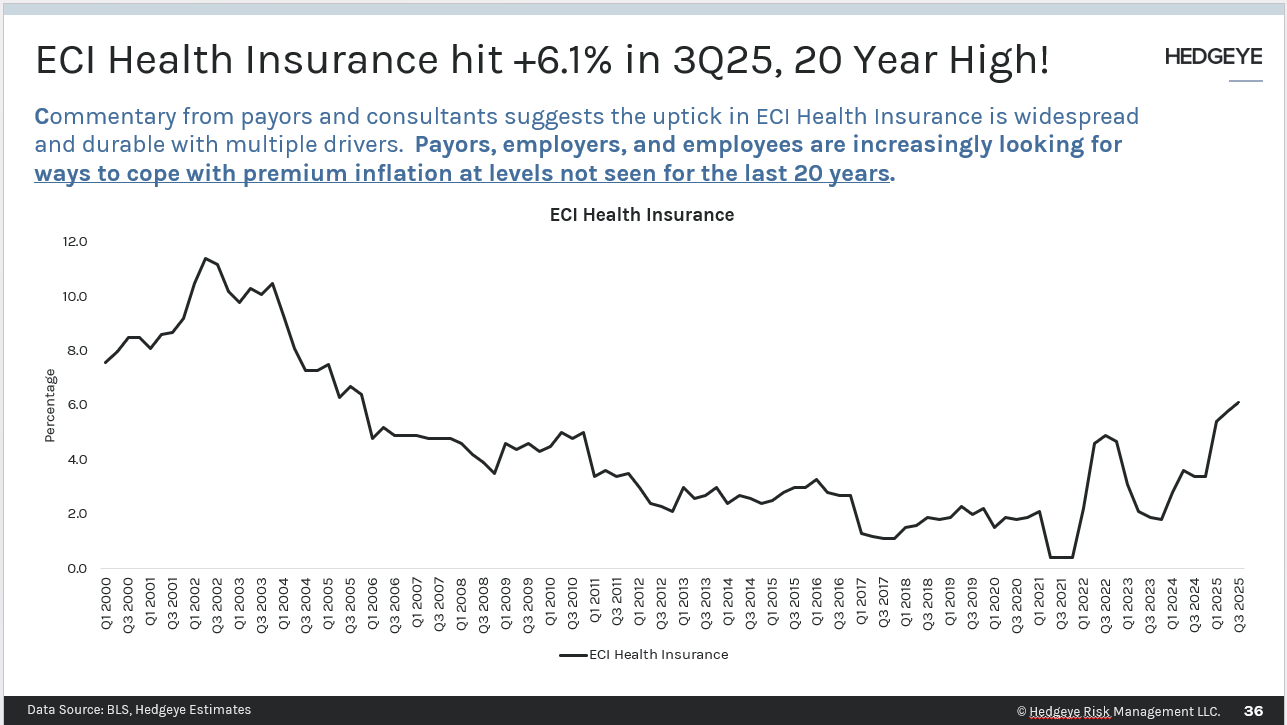

2025 mirage sets up 2026 disaster - slowing volume trends, accelerating labour costs and mounting policy headwinds are converging into a “perfect storm”. While 4Q25 may appear resilient due to pull-forward utilisation ahead of Jan 1st plan resets, Hedgeye expects brutal comps in 1Q26. They contend that Medicaid supplemental payments and unusually low uninsured volumes (due to immigration enforcement) flattered 2025 margins - tailwinds that are likely to reverse in 2026. With employer premium inflation at a 20-year high (+6.1% in Q3), insured lives are set to shrink just as labour costs accelerate amid unsustainably low SG&A ratios, driving significant margin pressure. Additional policy headwinds under the Trump Administration are working to shrink the population of insured medical consumers, amplifying the pressure already seen.

The global memory-chip shortage will cost us all

Technology

This article in the Wall Street Journal features insights from Counterpoint Research highlighting the severity of the global memory-chip shortage driven by AI demand. According to Counterpoint, prices for memory chips surged ~50% in late 2025 and are projected to rise another 40-50% by early 2026, as data-centre builders aggressively secure supply. MS Hwang, Counterpoint’s Research Director, warns that manufacturers are already selling capacity not just for 2026, but through 2028, leaving non-AI buyers increasingly squeezed. With new capacity unlikely to meaningfully arrive before 2027-28, memory is becoming one of the most expensive components in electronics, potentially rising to ~30% of device costs. Counterpoint’s analysis underscores that AI-driven demand is structurally reshaping global semiconductor supply as well as pricing power.

Technology

BTN highlights a growing set of earnings-quality red flags at AVGO, arguing recent beats are increasingly supported by accounting and working-capital levers. Software contract assets doubled in 2025 to ~$8.9bn, driving implied DSOs from ~45 days to ~120 days since 2023. With one day of software sales worth ~$78m of quarterly revenue, this dynamic helps explain the company's $100-$500m revenue beats. Upfront license revenue rose to ~29% of software sales from 14% in 2023, contributing an estimated ~$0.59 of EPS in 2025 vs. only $0.21 of cumulative EPS beats. Additional supports include falling deferred revenue (down ~50% in 2 years), rising receivables, historically low distributor reserves, elevated non-GAAP add-backs, flat cash R&D spending and aging assets - levers BTN sees as difficult to sustain.

Technology

CAMT is showing signs of late-cycle digestion beneath the bullish AI narrative. Revenue growth has decelerated sharply, slowing from ~40% y/y in Q3 '24 to 12% in Q3 '25, with Q4 guidance implying just ~8% growth. HPC, expected to be the primary growth driver, is up only 2% YTD and management has guided for a slower start to 2026. Meanwhile, inventory and receivables continue to build, pushing DSI and DSO to multi-year highs. As a result, Corto believes that valuation has become disconnected from fundamentals, with shares trading at peak multiples despite the massive deceleration in growth and inventory overhang.

Technology

QUBT has legitimate quantum assets across photonics, compute, security and sensing, alongside burgeoning thin-film lithium niobate (TFLN) fabs that could supply both internal and industry demand for integrated quantum photonics, nonlinear optics and optical waveguides. The company is also acquiring fabs (LSI) from Luminar for <5x revenue, improving P&L optics and diversifying into another key laser market. With $1.6bn of cash and no debt, QUBT’s interest income currently exceeds operating expenses. Rosenblatt likes the risk-reward, citing exposure to quantum computing, fab-driven product integration, customer acquisition in fast-growing optical communications, optionality around photonic gate-based quantum computing and the potential to embed quantum security into consumer edge devices. They initiate coverage with a Buy rating and TP of $22 (80% upside).

Emerging Markets

TikTok’s LatAm move has global reverberations

Report by

Blue Lotus Research Institute

Blue Lotus argues that TikTok Shop (TTS)’s entry into Latin America is the largest e-commerce opportunity in developing countries for 2026. Video and live commerce penetration in LatAm remains <5% of GMV vs. 20-25% in SE Asia, despite larger GMV and strong TikTok engagement - creating a wide opening for disruption. TTS’s traffic advantage is expected to pressure incumbent margins, particularly MercadoLibre and Sea, while driving logistics upgrades. J&T Express emerges as a key beneficiary, with LatAm filling a growth gap as China and SE Asia slow. Blue Lotus also sees strategic upside for Kuaishou, partnership optionality for Grab and longer-term opportunities for Alibaba to reposition internationally.

Communications

Lucror initiates coverage with a Buy recommendation, favouring the new TECOAR ’36s following the successful issuance of USD 600m 8.5% senior unsecured amortising notes due 2036, priced at 99.2 to yield 8.63%, inside initial guidance. They view the transaction constructively, as it is leverage neutral and will result in the extension of the company's maturity profile. Rated B2 by Moody’s, the bonds price in line with Lucror’s fair value and offer attractive relative value, delivering a ~90bp pick-up over higher-rated VISTAA ’35s and priced ~75 bps above the longer and lower-rated PAMPAR ’37s. With fundamentals improving and Argentina macro risk no longer a key factor, Lucror sees the entire TECOAR curve as compelling.

Materials

Prajogo Pangestu (Chairman since Jan 1993) bought 3m shares at IDR 2,830 per share, spending US$502,000. This is 3x the price of his last purchase 11 months ago. While small relative to his 71% ownership of the company, the purchase is in line with his prior purchases. He has also been timely on most of those prior purchases with an 18% average 6-month return. This is an interesting purchase as the stock has fallen from an all-time high in October. Smart Insider are ranking the stock +1 (highest rating).

Developed Markets

AI: Hammer to fall

Richard Windsor observes that OpenAI’s own data confirms that the cost to build a data centre or GW of compute is rising rapidly, yet the revenue that one can generate from it is static. The business case for offering compute for sale is worsening at an increasingly rapid pace. Consequently, either the cost to build a GW of compute needs to fall (as opposed to rise), or the revenue that a GW of compute can generate needs to rise. Failure to find a credible way to monetise the 700m+ users who do not pay the AI companies anything but cost a fortune in free compute could cause IPOs to be pulled, bringing forth a loss in confidence in the business model for AI. As many of the AI companies are now interconnected, this could easily set off a domino effect where the valuations of all concerned take a big hit, with acquisitions and bankruptcies becoming a clear sight.

Baby boomers and their wallets

Paul Hodges points out that 2026 is the year Baby Boomers join the Perennials 55+ generation. The largest and wealthiest generation in history, their spending helped to build budget surpluses and offset recessions – between 1983 and 2000, the US only had 8 months in recession, and that was largely a consequence of the 1990-91 Gulf War. The perennials are now the main source of G10 and global population growth for the first time in history. Unfortunately, mainstream economics is yet to recognise this trend and have yet to adjust their models to account for the fact consumer spending is age-related. G10 countries (ex-India) now face a major growth challenge due to the failure to increase pension age in line with life expectancy. Reserves such as Social Security and Medicare are running out; look forward to either higher taxes, a larger deficit, or Boomers being forced to spend less if reserves run out.

UK: The Shadow battle

Helen Thomas says we will be seeing a lot less of Keir Starmer as this year progresses. The shadow battle for his replacement is already well underway. His replacement will at least be afforded a honeymoon boost. The party will have to fall into line behind the new leader, reducing the backbiting and in-fighting, for a while at least. Yet Helen claims it won't last long term as the Labour Party remains irrevocably split over how to match its fundamental ideals with the fiscal constraints of 100% debt-to-GDP. This will ultimately lead to government collapse as Labour MPs defect or sit as independents, ushering in an election sooner than 2029. That contest will ultimately be Reform v The Greens as the electorate continues to tire of legacy parties and seeks to roll the dice with more extreme forces.

UK: Weak employment trumps noisy inflation

Report by

BCA Research

BC

Year-end employment data was weak, confirming the recent labour market slowdown, with the payroll fall of 53k exacerbating the 33k decline in November. December CPI data was mixed but on the cool side. Headline inflation printed hotter than expected at 3.4% y/y, but core inflation held steady at 3.2% when economists expected it to accelerate. Tight financial conditions will cap growth upside and further dampen inflation, while recent strength in hard activity data partly reflects pent-up industrial activity rather than broad-based momentum. BCA’s UK growth diffusion index appears to have bottomed, but at a very low level. More BoE cuts will be required, with barely two 25 bps cuts priced by year-end. Further weak data could bring an April cut into focus. BCA’s Global Fixed Income strategists’ highest-conviction view for 2026 remains an overweight in UK gilts, alongside GBP 2-year/10-year steepeners. Sterling remains mispriced versus the USD: UK equities have priced in weakness, but the currency has not, and BCA remain underweight GBP on a 12-month horizon.

The Arctic of the Deal

President Trump has announced plans to impose 10% tariffs on goods from eight European countries until a deal is reached over Greenland. Niall Ferguson remains sceptical that the new tariffs will be sustained, if imposed. If they are, Brussels will likely launch an investigation to activate the EU’s “trade bazooka” Anti-Coercion Instrument (ACI). Niall’s view remains unchanged: a US acquisition of Greenland via a compact of free association (COFA) or US military action to annex Greenland are highly unlikely. By far the most plausible off-ramp is for Trump to argue he has “won” some form of enhanced access to Greenland that in reality falls short of the type of acquisition he originally envisioned. Should the crisis drag on, expect the UK to retaliate against the US in politically painful sectors.

Questions on the USD

US economic growth is re-accelerating following the authorities’ shift back towards easier fiscal & monetary policies. Andrew Hunt continues to have doubts around the accuracy of the US profit data. For him the key question for 2026 is a simple one: will domestic and foreign investors continue to regard the USD as a safe store of value, or will the demand for money (USD) decline? If the latter, then US assets will be de-rated, likely starting with UST (if there is no YCC) or the USD if YCC is deployed in earnest. In 2007Q2, a “surprise” rise in UST yields acted as the catalyst for what became the GFC. Andrew would be extremely cautious if UST continue to trade poorly this year in response to external factors. However, if faith in the USD is sustained, the current liquidity-driven inflation of asset prices will continue until such time as its inflationary consequences for the real economy can no longer be ignored.

Australia: Rates down under

Markets still only peg 2 hikes from the RBA this year, whereas Craig Ferguson reckons we could see 3-4 hikes. That said, market reactions were swift to respond to the jobs data this week, with AU bond yields rising and the AUD continuing its ascent and starting Thursday morning near .6840 with the breakout new confirmed and truly underway. Craig comments that the most powerful AUD bull markets are always eventuated due to a rate cut cycle end when commodity CBs like the RBA lead the charge, and when a commodity supercycle unfolds as it is now. The RBA will lead the pack of growth sensitive commodity based central banks out of the cutting cycle. Expect outperformance of small- and mid-cap value and cyclical (resource) stocks, while large cap tech and financial growth equities suffer. As for AU 10yr yields, highs above 5% are in prospect, so stay underweight bond duration.

Big in Japan

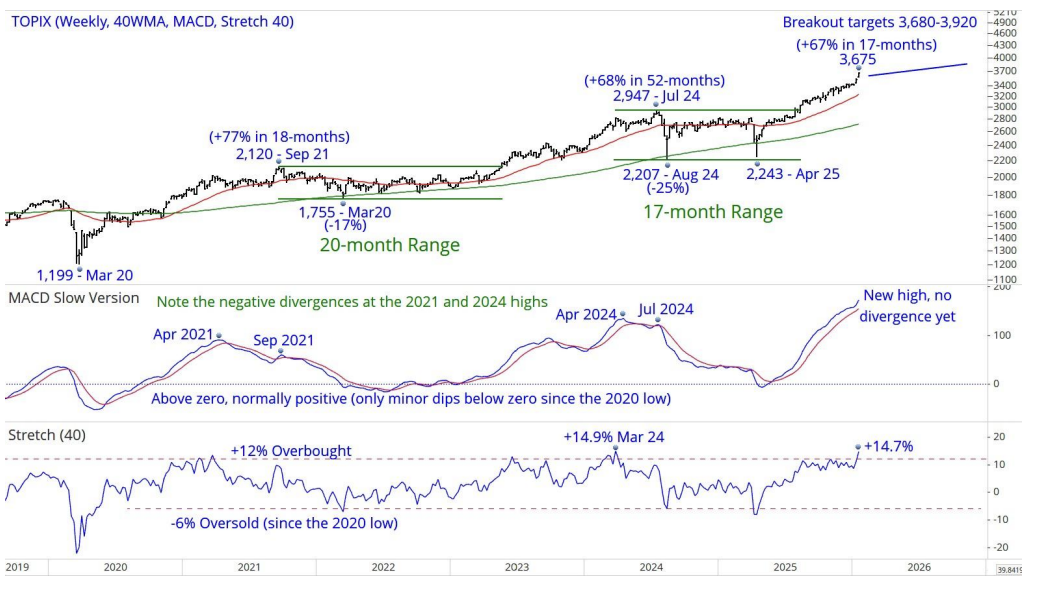

The Topix’s (3,659) breakout from the 2,207-2,947, 17-month range targets an advance to 3,680-3,920. Last week’s new ATH of 3,675, essentially puts the index into the target zone. The break above the 1,700-1,825, 28-year ceiling in 2021, targeted a minimum of 3,400-3,650+, now marginally exceeded. The prior behaviour of the MACD indicator (peaking before price) leads Chris Roberts to expect further net gains before a large correction, as seen in 2021-22 and 2024, occurs. He is 65% long from 2,925. Sell 5% at 3,658, 5% at 3,678 and 5% at 3,698 to take partial profits. The stop for all longs moves up to a daily close below 3,194 from 2,780.

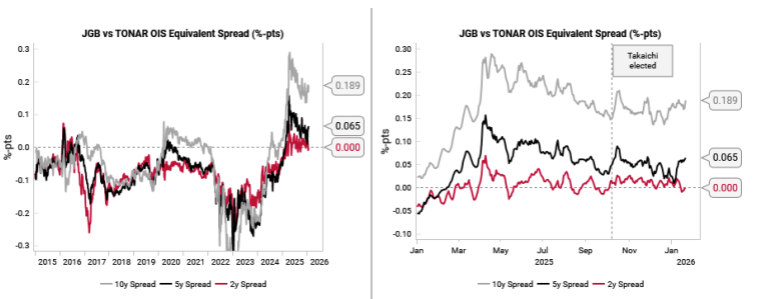

Japan’s impossible trinity mechanism

The country’s “doom loop” narrative has built momentum over the past six months as the yen and JGB selloff has become disorderly, driven by the slow pace of rate hikes, higher expected issuance of JGBs and lower domestic demand for long-term JGBs. Although the Variant Perception team see some validity to the doom loop story, the underlying mechanism is that policymakers are being pushed back into Japan’s impossible trinity problem; the country cannot have both exchange rate stability and such a slow pace of monetary policy normalisation. Expect USD/JPY to go higher first before policymakers are forced to take action to exit the impossible trinity later this year. There are three key indicators to watch for when to fade the yen selloff: a convergence in 2y yield vs the 5y5y OIS spread; convergence in JGB vs OIS spreads across tenors (see chart), and the monthly JGB purchase data show a pick-up in demand from foreigners and pension funds.

Emerging Markets

The emerging new world order

Now it is becoming clearer that the era of the USD being the dominant reserve currency in the world is coming to an end. As investors diversify away from the US, a weaker USD will shine the light on certain asset classes, with emerging markets a case in point. Much of EM debt is denominated in USD and will therefore benefit from a weaker greenback, improving emerging economies across the globe. The iShares EM MSCI ETF (EEM) appears to be finally breaking above its 2007 peak after, on this count, completing a triangle in 2020. The end of wave D may be a tad above wave B, breaking an Elliott rule, but this was so brief and small. EEM’s relative strength has pivoted from 2020 with the downtrend line now acting as support, a clue that sentiment is changing. In the years ahead, don’t be surprised if EM significantly outperforms.

Switching from Asian bonds

Since Warut Promboon’s Asian Bond Monitor (ABM) in September, Indian USD high-yield bonds in his sample have outperformed on an improving operating environment in India. The Fed has cut rates twice since then, as Warut expected, and he sees a further US rate cut as probable but not guaranteed. His base case scenario calls for a stabilised rate environment in 2026 which makes fixed rate bonds fully-valued. Asian corporate bonds have rallied 300 bps in the past 2 years. Given the stable rate environment, he believes it is time to pare down Asian bond exposure and switch to Asian equities for growth and low inflation stories. Warut argues for a reduction in Asian bond exposure, and not a total abandonment. He forecasts an improving operating environment in India and Indonesia which could lead to more fixed income inflow into both countries. As the USD softens, expect more foreign direct investment and portfolio investment into emerging Asia.

China: Pick up in nominal GDP data

Paul Cavey observes that China’s Q4 GDP data showed a pick-up in the deflator and nominal GDP, which external trends suggest can run further. In terms of the details, the data show two big discrepancies: collapsing FAI v industrial stability and falling retail sales v rising consumption share of GDP. According to the official data, GDP grew by 5% in 2025, which, perhaps unsurprisingly, was exactly in line with the government's approximate target. Real growth in Q4 slowed to 4.5% YoY, with a bigger boost from net exports being offset by slower growth in consumption and investment. However, nominal GDP growth ticked up. That nominal growth would be better in Q4 had already been flagged by the firming of the monthly PPI and CPI data. With equity prices up too, that helped produce an improvement in all-economy inflation through the end of 2025. The weak point remains property prices, which other data shows continued to fall in Q4.

Hungary: Upcoming elections could see the end of Orban

According to Teneo, the upcoming April election in Hungary will be perhaps the most watched one in CEE this year, holding implications not only for Hungary’s domestic outlook, but also for the broader appeal of Orban’s “illiberal” governance model. While reliable polling is scarce, the opposition Respect and Freedom Party (TISZA) appears to hold a lead over Orban’s Fidesz. Given an electoral system tilted in Fidesz’s favour, TISZA would need a clear margin of victory to secure a parliamentary majority. The main downside risk stems from Fidesz’s potential attempts to manipulate the outcome or bend constitutional rules to remain in power. One victory will bring policy continuity at the risk of further authoritarian drift; the other victory will end Orban’s 16-year rule and align Hungary’s domestic and foreign policies more closely with the EU mainstream. Such a shift would likely strengthen EU unity on Ukraine and could unlock Hungary’s access to suspended EU funds.

Iran: Markets have little margin for complacency

John Fagan points out that the markets are treating Iran less as a headline risk and more as a background constraint. The unrest has reinforced a floor under oil prices and sustained demand for hedges, but it has not forced a repricing of global growth or US monetary policy expectations. John says two uncertainties remain central. The first is economic durability. Continued currency weakness and inflation raise the probability of renewed unrest or policy error, increasing the risk of spillovers into energy logistics or regional trade. The second is transmission risk. While escalation remains contained, even marginal disruption in Hormuz would have outsized effects on US gasoline prices, freight costs, and inflation psychology - even more important factors during the late stage of the US disinflation cycle. Until financial stress translates into physical disruption, markets are likely to remain anchored to fundamentals, pricing Iran as a persistent risk premium rather than a catalyst.

Syria: House of cards

Stability remains fragile. Kurds are open to discussions, but deep tensions continue to bubble over border control, education, security, energy issues and women’s rights. The French Development Agency may have carried out a discreet engagement, but the same country’s intelligence agency views engagement with scepticism. The US sees medium term stability diverging either way. The new leader is adept at balancing power among factions and maintains a degree of control over independent players, but the GlobalStrat team expect major sectarian violence to erupt among independent “liberator” factions, triggering massive confrontations. They place only a 35% chance on the status quo being maintained with all players involved, including Israel and Turkey, eager to avoid a civil war at all costs.

Thailand: Is this weird?

The economy is still stagnant. Thailand is still flattish externally and depressed at home, with exports and tourism lagging the rest of EM and weak domestic activity indicators. So, why then have imports exploded in recent months, sending the external balance into sharp deficit? Jonathan Anderson’s best answer is that this appears to be tied to "round-tripping" goods flows from China - but he will be watching the data carefully in the first half of 2026 for clarification. In the meantime, all the more reason to be cautious on Thai assets. There's no earnings growth in the equity market, local yield and carry are extremely low ... and the external swing could mean heightened risks on the baht going forward.

Commodities

Don’t chase the bubble

With everyone and his brother long the stock market bubble, gold and silver assets have been pulled into the speculation. It seems that Michael Belkin is a rare voice who was wildly bullish on precious metals last year but is now sceptical about the prospect for continued gains. So, what should investors look at? Michael recommends two market-neutral rotation trades which are already up +6% so far in 2026; the two spreads are value growth (IWD/IDF) and S&P493 minus MAG7 (XMAG/MAGS). Both have an intermediate-term (3 month) and long-term (12 month) upward model forecast, implying a high probability of a continued rotation trade out of large-cap tech sectors. Get out of MAG7 and shift into value, consumer staples, energy, industrials, materials, financials, utilities and REITs.

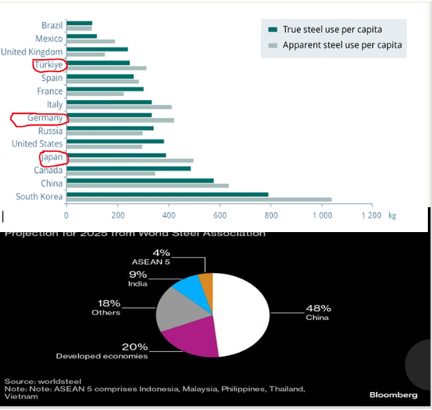

Iron ore: China’s urbanisation supercycle is over

James Burdass notes that China’s National Bureau of Statistics has reported a production of 960.81 million tonnes of steel last year, 4.4% less than in 2024. This may not appear significant, but is in fact an important data point that every commodities investor needs to be aware of. In his presentation a year ago "The New World Order and Commodities", James showed just how far China's apparent steel use per capita could fall. He suggested at the time a fall of at least 200 million tonnes from the peak – the trend is definitely on the way towards that. Falling materially below 1 billion tonnes for the first time since 2018 is the official obituary for the "Urbanisation Supercycle." It signals to every Iron Ore investor (Rio Tinto, BHP, Vale) that the volume cap is in place. This has the potential to be a headwind for the global steel sector for years to come.

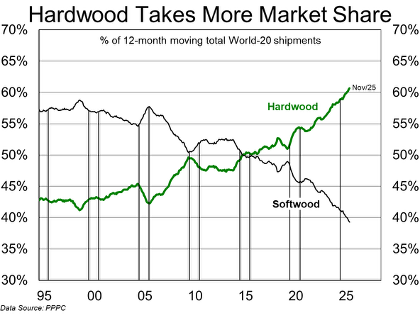

Hardwood gains more market share

The hardwood share of global pulp shipments reached an all-time high in 2025. As global hardwood pulp capacity has grown at a faster rate than softwood and given production costs are ~$300/mt lower, the potential rate of substitution of hardwood into established softwood markets has been a key variable in determining the demand growth rate of each grade. Hardwood pulp producers will clearly benefit, although they have challenges, including exposure to China’s rapid build-out of integrated domestic pulp capacity and the burden of recent huge greenfield mill capex. There’s also the threat that upcoming BHK capacity additions will simply step into expanded hardwood market opportunities. The ERA team see upside in Suzano SA but highlight that R$ swings may require nimble repositioning. They remain cautious on NBSK near pure-play Mercer International Inc given a very stretched balance sheet and little room to manoeuvre. Without more shuts, NBSK prices have little near-term upside.

How silver markets really work

In this presentation, Jeffrey Christian of CPM Group explains what is really driving the latest surge in silver prices, and why so many popular explanations circulating online don’t hold up when you look at how the market actually works. Jeff starts with a market update of where gold, silver, platinum, and palladium are trading, then focuses on the silver market, including why large moves often come with sharp pullbacks as short-term investors take profits. He explains how today’s market is being influenced by momentum traders, and why those same buyers can quickly become sellers once prices spike. He also addresses several misconceptions, including the “paper vs. physical” narrative, claims of backwardation based on mismatched price references, and the confusion created by comparing different products and markets. Jeff also looks at what higher prices tend to mean in real world conditions: more scrap coming to market, more supply development, and more substitution by manufacturers.

Click here to watch.