Europe

Balance sheet stresses threaten earnings recovery

‘Walking a Tightrope’ - this 30-page white paper examines the hidden data, revealed by StockViews’ proprietary Dragonfly red flag analysis of over 1300 European companies. Areas of focus include how companies have extended payables to unsustainably high levels (31% of companies display a DPO red flag); the fact that companies are drowning in inventory and only a rapid recovery can save them; receivables write-offs (ageing of receivables and rising DSO). Travel, Autos and Consumer products are the sectors that produce some of the worst offenders.

Next (NXT LN) UK

Consumer Discretionary

Report by

Holland Advisors

HO

Holland Advisors discuss the transition of the company into a logistics powerhouse providing the Total Platform that brands require to solve their fulfilment/delivery/logistics problems. Holland's conviction re. why Amazon should purchase NXT continues to grow - it has the perfect cultural and customer brand offering for AMZN and while AMZN may have formidable skills and scale, it does not have the supplier trust and buying wisdom in the world of fashion apparel that NXT possesses…over to you now, Jeff.

Inditex (ITX SM) Spain

Consumer Discretionary

Zara is looking better than ever; top European comeback play - Stacey Widlitz explains why she believes the Spring/Summer collection is perhaps the best of any brand right now (incorporating mom jeans colour, prints and the Pucci look). Its product is now appealing to a wider age group (teen to late 40s) and accessories are finally hitting their stride and still offer loads of potential. Stacey also reported that Zara has been one of the clear winners as the UK eased lockdown restrictions recently.

Roche (ROG SW) Switzerland

Healthcare

Intron downgrades the stock to Sell - based on ROG's increasingly gloomy biosimilar outlook, high likelihood of EBIT downgrades next year, collapse of its pipeline and absence of any emerging blockbusters. TP CHF280 - implies ROG trades on 14.3x in 2022 - a 7% discount to the sector. This is more than justified given its 0% EPS growth this year and just 2% next year. It is the slowest growing Pharma name (ex-GlaxoSmithKline) on a 5-year view.

North America

JetTrack: Real Time Insight into Corporate Strategy

Paragon Intel’s JetTrack is an analytics and data platform that enables investors to track the private jet activity of ~3,500 companies (5 Min Demo Here). JetTrack has been very successful in helping investors get ahead on many deals through the tools built into the platform (Raytheon/United Technologies, Occidental/Anadarko, Gilead/Immunomedics, ICE/Ellie Mae to name a few). Recently, they have flagged outlier flights of Simmons First National Corp. visiting Regions Financial Corp. twice after not travelling near their headquarters for over 5+ years.

Boyar Research significantly outperforms the S&P 500…again

In April of last year Boyar Research released a special report detailing 19 companies they believed would do well amidst the market sell-off. One year later, the ideas profiled have advanced 77.7% on average, outperforming the S&P 500 by ~27%. This is especially noteworthy (as well as a testament to their stock picking ability) due to the lack of high-flying technology names featured. Companies highlighted include Dollar Tree, Hanesbrands, Laboratory Corp., Mohawk Industries, Howard Hughes Corp. and Watsco.

Frontier Communications (FYBR US) US

Communications

New management, new strategy - FYBR to transform itself from broken ILEC into a fiber-based infrastructure asset, resulting in a return to growing revenues, expanding margins and a higher multiple. New Street see the opportunity for a four-fold increase in the equity organically, with potential for a ten-fold increase with M&A over time.

Coursera (COUR US) US

Consumer Discretionary

Obex’s short thesis focuses on the intense competition faced by this online education platform and its lack of leverage with content suppliers. COUR’s growth trajectory is being mismodeled based on 2020’s surge in signups. Downside risks around regulation and incursion by tech platforms paired with an obscene valuation make a compelling short case. Bear Case Valuation $20 (55% downside).

Tesla (TSLA US) US

Consumer Discretionary

Report by

Silk Road Research

TSLA China analysis - will the recent product quality issues escalate to a level of a long-lasting scandal? Following a barrage of negative headlines at the same time as the Shanghai Auto Show was taking place (one of the most important marketing events for OEMs) the short term outlook is a concern and domestic brands look well placed to benefit. SRR will be closely monitoring the situation; conducting their own channel checks to gauge any material shifts in consumer perceptions over the coming months.

Tractor Supply (TSCO US) US

Consumer Discretionary

1Q earnings smash expectations; the longer-term outlook continues to strengthen - R5 highlight the company's ability to create a unique rural superstore format. Store-based enhancements are synergistic with TSCO’s efforts around Omnichannel, product line extensions and customer loyalty. Expects upside to comp sales in 2022 and beyond, which should yield stronger than expected EPS growth.

Anyone care for a Beverage?

Consumer Staples

Beverages are starting to pop as the rotational rebound for defensive sectors is underway. Nautilus view the confluence of the recent breakout (SP500 Beverage Index just registered a one-year high for the first time in six months), the bullish seasonal window, the fact that the Beverages/SP500 long-term cycle is bottoming (anticipating outperformance over the next 18 months), coupled with compressed relative valuations, to indicate a very attractive entry point for investors.

Blinded by the Light: Highlighting Solar Non-GAAP Risks

Energy

Veritas’ analysis reveals common non-GAAP metrics used by US solar leasing companies, such as Gross Earning Assets, Net Earning Assets and Net Present Value, could be overstated by as much as 70%. They challenge key assumptions that underpin these complex calculations, such as renewal rates, default rates and discount rates. Their study focuses on three industry leaders - Sunrun, Sunnova Energy and SunPower and they believe that unless legislation impairs the economics of competing energy sources, all 3 companies remain significantly overvalued despite recent 30-40% corrections.

Tronox (TROX US) US

Materials

Markets are massively underestimating the positive impact of price rises in TROX’s key products (TiO2, pig iron and zircon). TiO2 price hikes alone could boost EBITDA by $582m YoY in 2021. Favourable supply/demand fundamentals mean that these higher prices are sustainable. Alembic raise their 2021 EPS forecast to $2.20 (from $1.70) and 2022 estimate to $3.05 (from $2.30). 12-month TP $29 (35% upside).

Equifax (EFX US) US

Technology

Craig Huber initiates coverage on this high quality, fast growing information services company. He believes that EFX’s differentiated offering sets it apart from its peers. Highlights its unique datasets, cloud transformation and increased focus on fintech. US Information Solutions pipelines are at the highest level since 2017. New product innovation revenue growth to accelerate to up 75% this year. TransUnion’s entrance into the income and employment verification market will not negatively impact the business. Craig’s earnings model and 10-year DCF analysis are also included in the report.

Nvidia (NVDA US) US

Technology

Report by

Blueshift Research

BL

Blueshift Research examine whether dramatic developmental changes in chip technology are putting increased pressure on NVDA to close its deal to buy Arm - smart everything means that the standard edge-to-the-data center model is going to break; a new kind of edge-based compute fabric centred around Arm’s tiny chip designs will rapidly emerge - an area that NVDA does not have a strong foothold. They also consider opposition to the deal to be short-sighted especially since Softbank cannot fund the innovation necessary for Arm to continue to evolve chip architecture.

Emerging Markets

Kuaishou (1024 HK) vs. TikTok

Communications

With short video platforms becoming the centrepiece of mobile entertainment more and more companies are trying to toss their hats in the ring, however, the two companies in the spotlight in China's domestic market are Kuaishou and TikTok. Horizon Insights' in-depth report examines the relative strengths and weaknesses of the two companies with direct comparisons of the in-traffic flow and duration, monetisation methods, and growth strategies of each platform.

China Handset Semi Checks

Technology

Westlake's report includes detailed analysis and data on semi shortages, handsets and components inventory and lead times - Qualcomm, MediaTek, Skyworks, Qorvo and Broadcom saw very strong pricing and better-than-guided 1Q demand at Chinese OEMs. Their OEM contacts also observed lower phone inventory in 1Q vs. 4Q, with some indicating 6-7% inventory-to-sales ratio (normal level is 10-12%). Based on fab wafer sizes and technology nodes, the most severe shortages were seen in basebands / SoCs, MCUs, CIS sensors, display ICs and PMICs.

Bilibili (BILI US) US

Technology

Report by

RedTech Advisors

‘Too Niche or not to Niche’ - BILI’s evolution from niche purveyor of ACG (Anime, Comics and Gaming) content to entertainment giant continues apace and with management’s target of 400m MAUs by 2023, the bar is high. The problem is that while trying to appeal to a wider audience BILI risks losing the very thing that made it special - a dedicated community of ACG lovers. This begs the question: would BILI be better off doubling down on its existing strengths instead?

Zenith Bank (ZENITHBA NL) NL

Financials

Zenith offers the best combination of value, safety, profitability and yield among the Nigerian banks. It posts 20%+ ROEs while maintaining a 38% ratio of tangible equity to loans. With such a high TCE/loans ratio, even if 7.5% of the loans went bad that would only reduce capital by 20%, which the bank would make back via operations in a one-year time frame. Forward dividend yield of 17%, rising to 23% in 2023. TP increased to 59.01 NGN/share (168% upside).

Saudi Arabia: Scaling New Heights

Fund Analysis

Global EM active fund allocations to Saudi Arabia have hit record levels led by increased investment in stocks including National Commercial Bank and United Electronics. Yet, on average, managers are still underweight by -2.49% (2nd largest underweight behind China & HK). Of the 241 funds in Copley’s analysis, only 51 currently have exposure. 40 out of the remaining 190 have previously held positions in Saudi Arabia, but are currently on the sidelines. Given that the country has started to generate some serious outperformance (YTD +26.9% vs. MSCI EM Index) this may not last for long.

Developed Markets

How to invest if inflation breaks out

Gerard Minack looks at the investments that could survive a breakout of inflation. He mentions commodities as the stand-out inflation hedge amongst conventional assets, with trends strategies having generated positive real returns in previous inflationary bouts. Debt and equity do badly, though energy stocks gain. 10-year treasuries have also in the past lost less money than US equities in inflationary periods, a likely result of rallies around anticipation of a cycle downswing at moments of peak inflation.

UK: Kompromat, but not enough to topple PM?

Boris Johnson’s previous chief advisor clearly has kompromat on his former boss, which could escalate into something far more serious for the PM. Niall Ferguson doesn’t believe so. The information Cummings has is insufficient to indict and topple Johnson, either in the eyes of voters, who are busy enjoying newly reopened pub gardens, or with the Tory party, who will see good results in the upcoming local elections.

Brexit – a blessing in disguise

Despite one of the strictest lockdowns in the world, the UK is having its forecasts revised upwards. How come? Helen Thomas explains we are adapting to the new virtual world, with the UK uniquely positioned with its long and stringent lockdowns. As supply chains around the world get redrawn, Brexit has also afforded the UK the flexibility it needs to bolster trade flows. The short-term pain the UK has endured will be a blessing in disguise.

When Irish eyes are smiling

What’s going on in Ireland? Marc Rubenstein claims a fresh chapter is being written. In the past couple of weeks two banks have announced their departure from the market, and Ireland is rapidly converging on a duopoly. Interest rates and regulation determine bank profits in all markets, but market structure comes out on top. The duopoly will provide a path for the banks to overcome challenges they face, in particular the low level of interest rates. This duopoly is worth watching.

Sweden: Riksbank cautiously optimistic

The bank’s latest report indicates the world is becoming a brighter place, but with a long list of caveats. The bank will continue to purchase assets (SEK ~700bn) and hold the repo rate at 0%. It plans to keep total securities holdings at SEK ~900bn, holding at this level until 2022’s end by reinvesting around any redemptions. The pace of recovery is slightly stronger than expected and the GDP forecast has once again been upgraded to 3.7%.

Eurozone inflation – the forgotten one

Andrew Hunt believes there is an increasing threat of inflation in the German economy, with core CPI rates reaching >2% and stymying the country’s competitiveness. The high level of demand pressure will simmer in a year or two when citizens are forced to save more to fend off a looming pension funding crisis. The rest of the EZ will not see similar inflation, with current upward pressure originating from import prices, a situation which will be deflationary for incomes and pose a headwind to recovery over the medium-term.

US: It’s never different this time

Even with various reforms in Biden’s plans, investors in the private sector will be the losers. Barry Knapp’s analysis of historical capital gains rates and the S&P 500 earnings yield points to a valuation hit of one PE multiple point, which would be much higher but for the government's inability to collect taxes. He claims the MMT experiment will not end anytime soon. The spending portion of Biden’s agenda will regain momentum, with the real rate curve steepening eventually, although progressive wealth transfer plans will be trimmed considerably. Consequently, the reflation theme remains Barry’s highest conviction view.

The Canada conundrum

If you think the US is doing MMT, wait until you see Canada. Jared Dillian explains that this presents a conundrum: how do you price USD/CAD? Jared doesn’t have an answer for CAD’s strength, but on the other hand he mentions that BoC governor Macklem is making noises about tapering asset purchases – what will happen to Canadian bond yields? They have to go a lot higher till they become attractive and - with no reserve currency - if the BoC steps back things in the bond market could get ugly.

Emerging Markets

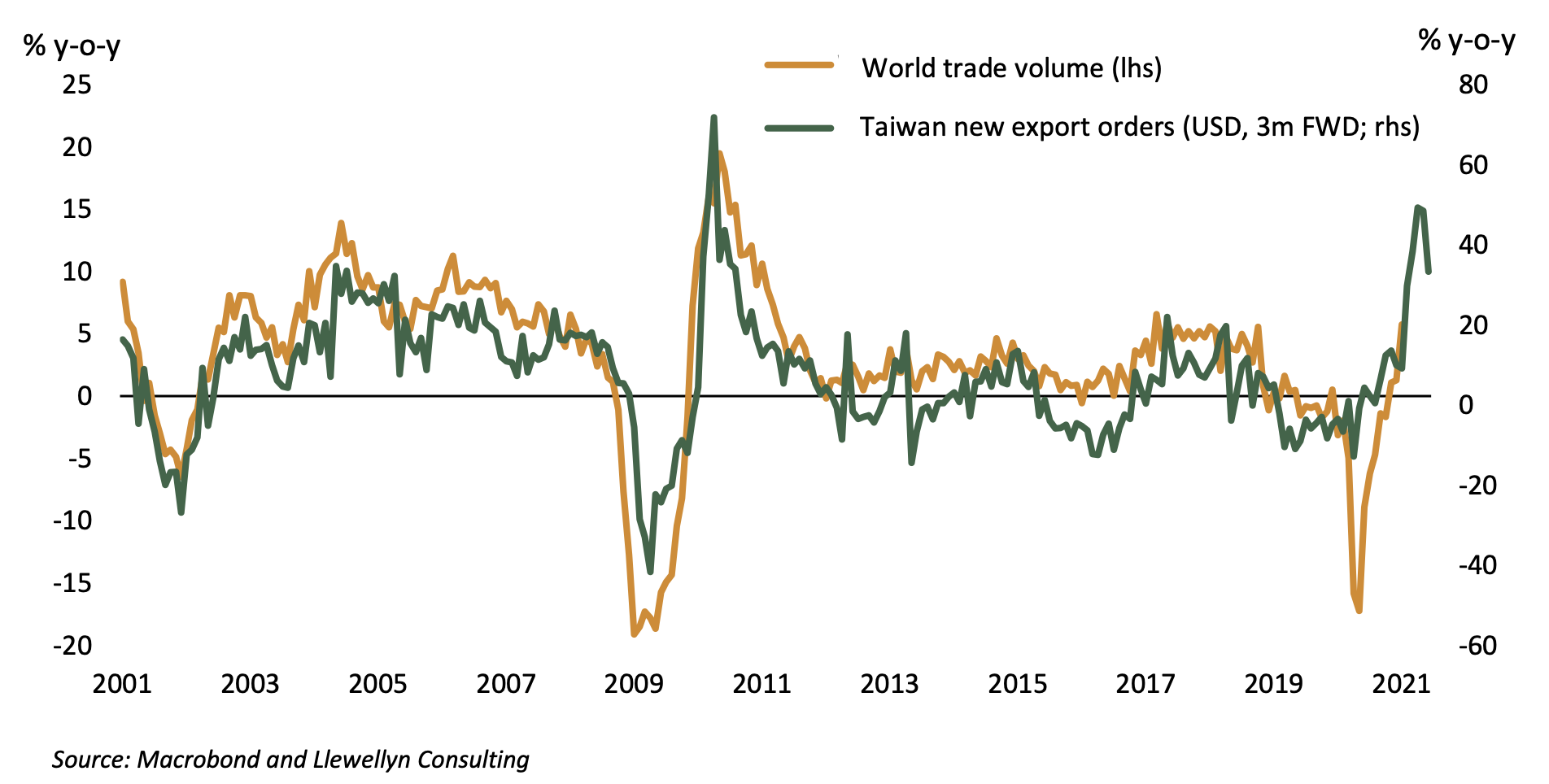

Chart of the fortnight: Taiwan export orders point to strong world trade growth ahead

Report by

Llewellyn Consulting

LL

Q1 export orders are up on average by 44% on the year, compared with 25% for Q4 last year.

Semiconductors: The new oil; East Asia to benefit the most

Rory Green explores the mounting importance of semiconductors. Over the next three years the winners will be the ones that have a physical integrated circuit trade surplus and/or a technical one; East Asia has both, and the US possesses the former. China is a semiconductor twin-deficit country with insufficient domestic production and a dearth of advanced IP, and leading-edge production will remain out of their hands for the future despite Beijing’s efforts. Investors should take a “buy on dips” approach for leading semiconductor capital providers and firms with monopolies (TSMC, ASML, etc.). Consider Chinese national champions, for they are too big to fail from a political and national security perspective. For short-term trading ideas, early signs of Dutch disease point to a strong secular tailwind to TWD and KRW, both tied increasingly to semiconductor cycles - the FX weakness provides an entry point for long KRW and TWD positions against EUR.

EM’s to continue relative underperformance in higher rates environment

EM currencies (MXEF0CX0) have started their correction with bearish elements confirmed – further drop towards 1660 or even 1627 are forecast. EM stocks (EEM US) are undergoing a correction, with a further drop anticipated towards 46.30 (~16% downside) and also expects EM local currency bonds (LEMB US) will see an additional 10% drop.

No evidence of Chinese monetary policy tightening

Warnings about China’s monetary tightening threat are not backed up by evidence, of which there is none. Although open-market operations have recently stalled, liquidity levels seem adequate; investors have read too much into the weak stock market and distorted official liquidity data. Despite perceptions of instability, China is remarkably stable, and, unlike its increasingly vulnerable Western counterparts, it is considerably less likely to experience its own Lehman-moment.

China: Shifting official views on demographics

China’s demographic profile is deteriorating faster than official data indicates and population will peak sooner than expected. To prop up potential growth, investments in supply side productivity and redistributive policies are necessary to improve the breadth and composition of household demand. China’s capital accumulation phase is far from over and investments in innovation and supply chain capacity, as well as infrastructure spending, will continue to drive growth.

Flooding pounds China’s Three Gorges Dam again

Water inflows to the world’s largest dam are expected to reach record levels. Whilst disaster pundits span stories over a dam collapse, the real story is the washout of 40% of China’s usable arable land. Mark Latham explains that it serves as a stark reminder of the fact 50% of the population is reliant on 15% of the water resource (85% of China's rainfall is south of the Yangzte river, but most of the population and industrial base is to the north). There is also another serious issue that is being ignored, that of water pollution; the invisible danger could mark an impending catastrophe.

Mexico President’s disconnect with Biden becomes clear

President Lopez Obrador has said that the country will continue to exploit its oil reserves for domestic use. The ironic comments came during his speech at the Climate virtual conference; the President’s failure to commit to any new targets in the face of Biden’s call for world leaders to commit more to climate change shows that Lopez Obrador is out of step with the US administration and is risking producing serious bilateral frictions.