Company & Sector Research

Europe

the IDEA!

Shell: To Be(P) or not to Be(P); that’s the question

Analysts at the IDEA! weigh in on media speculation about a potential Shell acquisition of BP. While Shell has the financial strength to pursue a deal, acquiring BP would involve taking on its $77bn of debt and other long-term liabilities, including those from the Deepwater Horizon spill. Although synergies are possible, integration would be costly and could disrupt Shell’s shareholder returns, which is key to closing its valuation gap with US peers. The deal would also bring in non-core assets and regions Shell has been moving away from, along with notable cultural differences. the IDEA! suggests caution and favours Shell sticking to its current strategy or exploring other deals instead.

Fighting Financials

Fighting Financials resumes coverage of AJB with a Buy rating, following a successful prior call that captured the stock’s strong rally last year. Since then, the shares have stagnated and materially underperformed the SX7P Banks Index, despite AJB continuing to gain market share and boost shareholder returns via dividends and buybacks. With ~50% ROE, no debt and positive working capital, the platform is seen as resilient - benefitting from both market volatility and higher interest rates. Long-term structural growth remains supportive, even if UK growth slows. Consensus expectations for FY25 (+10% revenue growth) appear conservative after +26% in FY23, suggesting potential for positive earnings revisions in the months ahead.

ResearchGreece

Buy Greek Banks

ResearchGreece remains bullish on Greek banks following Q1 results, citing strong economic growth, fiscal discipline and resilient asset quality that support lending, fee growth and capital generation. Higher 2026-27 RoTE estimates have led to raised price targets: NBG (€12.3), Eurobank (€3.5), Piraeus (€7.8) and Alpha (€3.1). Distribution yields range from 7.5%-10.0%, with payout ratios lifted to 70% for NBG and 60% for Eurobank. NBG, with CET1 above 19%, has the highest payout potential and deploying its €2bn in excess cash is a key catalyst. ResearchGreece favours a mix of bolt-on, fee-generating acquisitions and increased shareholder returns.

New Street Research

New Street initiates coverage with a Buy rating, citing increased prospects for French Telecom M&A as a key catalyst. They consider a Bouygues-SFR deal to be the most likely as the GUPPI is probably too high for an Iliad-SFR merger and Iliad-Bouygues is unlikely as there is no natural seller. New Street suggests an SFR-BTel deal could unlock €8–9bn+ in synergies. Regulatory remedies would likely be manageable amid current political sentiment. Drahi may now face pressure to provide lenders with an exit from SFR. New Street assigns a 56% probability of a merger in their SOTP model and sees 43% upside; they would be a Buyer ex M&A, but M&A could be a game-changer, especially as the dividend can increase by over 50% as well.

AIR Capital

AIR raises their TP to EUR 1,000 (45% upside) - 1Q25 sales hit EUR 7.7bn with gross margin improving to 54%, driven by EUV demand. Despite order normalisation from Q4 highs, Upgrades and Services reached EUR 2bn, bolstering earnings stability. ASML’s High NA EUV systems, now priced at EUR 350m, further boost profitability and widen its tech lead. Long-term, ASML expects EUR 44–60bn in annual sales by 2030. With the shares trading at a -35% discount to their 5-year average, the US semiconductor industry set to pay 100% of the extra levy charged by Mr Trump on ASML equipment shipped to the US and Chinese rivals far behind, AIR sees this as a compelling entry point into a global semiconductor monopoly.

North America

Kailash Capital Research

Venture Capital: Turning today’s dreams into tomorrow’s write-downs

KCR warns that today’s most speculative, unprofitable tech start-ups are hidden in private venture capital portfolios, not public markets. With VC valuations ballooning from $1.7trn in 2020 to $4trn today, they argue this mirrors the dot-com bubble - only this time, the risks are obscured. Many VC-backed companies can’t IPO because their valuations far exceed what the public market will bear. Worse, KCR highlights a surge in venture debt - often issued to unprofitable firms without equity backing. This debt-fueled demand props up Big Tech profits, echoing past financial manias. If failure rates hit the historical 75-90%, these holdings could implode, triggering ripple effects across tech markets. Click here to access the report.

Revelare Partners

High conviction Shorts

Revelare hosts over 40 idea events annually, sourcing 200+ original investment ideas from institutional investors. Shorts presented at a recent event included: 1) Docusign - described as a “melting ice cube” with overly bullish growth expectations for its Intelligent Agreement Management (IAM). 2) New York Times - viewed as a fully mature and fully exploited asset on a subscriber basis that likely peaked heading into the Trump vs. Harris election cycle. 3) MP Materials - a loss-making miner incorrectly perceived as a beneficiary of the trade wars, but which could actually be an existential threat for the company.

Huber Research Partners

NXST is one of only two TV broadcasters that is rated Overweight by Craig Huber. The company is generating a tremendous amount of FCF (he estimates $1.65bn after dividends over 2025 & 2026, which is more than 30% of its current m/cap). With a stronger balance sheet than peers, NXST is better insulated from a downturn in the ad market and is well-positioned for acquisitions if regulatory constraints are relaxed in the next year, as Craig expects. He sees huge pent-up demand for another wave of consolidation as well as demand for doing TV station swaps to create duopolies in markets among two top-4 rated TV stations given the cost synergies are massive.

Hedgeye

Andrew Freedman sees Google’s AI Overviews as a critical and underappreciated threat to RDDT’s business model, with RDDT content already pushed lower in search results vs. 2024. This validates his earlier view that the company’s heavy reliance on Google traffic is a key risk. Marketer feedback from 1Q25 also points to sharp declines in organic traffic, hitting both user growth and monetisation. While global user numbers may appear encouraging, they are largely driven by new translation features in international markets like India. These markets, however, monetise poorly and are unlikely to contribute meaningfully to revenue or profit growth. Looking ahead, Andrew anticipates increasingly volatile advertiser and user behaviour going into 2H25. He forecasts a faster-than-anticipated deceleration in revenue growth and a stock that is 40% lower over the next 12-months.

Veritas Investment Research

Liam Gallagher continues to have significant concerns about the sustainability of the company’s dividend. Management announced a 3-8% annual dividend growth target from FY26 through FY28 and reiterated plans to eliminate the DRIP discount by FY27. While Telus expects to support this through billions in asset sales, reduced capital intensity and EBITDA growth, Liam remains unconvinced. Even if everything unfolds as planned, Telus' FY28 payout ratio will be 104% based on Veritas’ definition of FCF and 89% using the company's. He also does not believe the company’s premium valuation at 17x FY25 P/FCF vs. BCE at 13x and Rogers at 11x is justified, especially given its higher payout ratio (~145%) and net debt/EBITDA (3.9x) relative to peers.

R5 Capital

What is Amazon doing in its grocery store business?!

Amazon Fresh stores are an embarrassment, according to Scott Mushkin - just when he thought things couldn’t get any worse, his latest store visit reveals rampant out-of-stocks, incorrect electronic tags, as well as bizarrely low prices on certain items. Indeed, there were times when the AMZN price was nearly half of what Walmart was charging. While Scott currently does not see the lack of progress in the grocery business as a problem for the equity given how well the retail business is operated overall, getting fresh foods right will make a difference regarding the ultimate TAM of the business. He has advocated the need for a different approach, including floating the idea of spinning Whole Foods back out and keeping a minority stake.

Quo Vadis Capital

John Zolidis removes DKS from his LONG list, following the group's proposed takeover of Foot Locker. He argues that the deal undermines the rationale for assigning DKS a premium multiple, which had been supported by its consistent performance and structurally superior margins. John is deeply sceptical that management can succeed where respected executive Mary Dillon failed. The acquisition threatens to create even more banner conflict, overlapping real estate, greater reliance on Nike and adds significant operational complexity. Crucially, FL lacks unit growth - the one element DKS was missing. While some cost synergies and FCF may eventually be realised, it will take a long time to recoup the $2.5bn price tag.

Periphery Research Partners

Another miss, another excuse - this is now the 4th consecutive quarter that DKNG has missed on revenue. This is also the 7th consecutive quarter where Sports Outcomes were a y/y headwind to revenue growth. As a bookmaker, DKNG’s core job is to set odds and it is become increasingly worse at doing so. Hesham Shaaban remains bearish, expecting management will have to cut 2025 guidance (again); noting it relies on the same flawed assumptions as 2024, which was revised down twice. Management also assumes 2024’s negative comps will become 2025 tailwinds, despite two consecutive quarters of poor results. Structural issues will become more evident now that DKNG is working with a slowing inorganic tailwind from new state launches.

CTFN

The leadership transition at UNH, while unexpected, underscores a commitment to continuity, according to CTFN’s sources familiar with the matter. One source noted Stephen Hemsley did not to have return as CEO, while also stressing the importance of his institutional knowledge and leadership during past crises. Sources also linked his reappointment to regulatory strategy, particularly regarding the contested Amedisys acquisition. The company’s suspension of its 2025 financial outlook, attributed to higher-than-expected costs in Medicare Advantage, is viewed as an operational issue rather than a trigger for strategic overhaul. Hemsley has pledged to implement "remedial responses" across the group focusing on pricing and operational efficiency - hallmarks of his previous tenure.

Sidoti & Company

Sidoti increases their TP to $93 (50% upside) following 1Q25 results that demonstrated that tariff and macro-related pressures are better than feared. They continue to view ROCK as a quality growth name with multiple avenues to drive earnings power, via Renewables volume acceleration, Agtech segment sales acceleration, or balance sheet deployment. During Q1, ROCK announced two tuck-in metal roofing deals for a combined $90m in cash, expanding its largest and most profitable segment (Residential). This is in addition to the previously announced Lane Supply deal (Feb 25), which expanded the Agtech segment. Even after funding these acquisitions and $62m in share repurchases, the company remained debt free. Sidoti’s TP is based on 18x their 2026 EPS estimate of $5.18.

ETR

Inside the decline: What leaders reveal about 2025 tech spend

ETR’s latest Macro Views Survey, based on responses from 1,800+ tech leaders show Y/Y growth projections for 2025 now sit at +3.4%, down from +5.3% in Jan - the steepest quarterly drop since tracking began in 2020. Midsize organisations adjusted their forecasts the most, cutting 2.3 percentage points. Small businesses still show the highest spending growth at 5.1%. Fortune 500 and Global 2000 firms now project just 2.4% and 2.2% growth, respectively. Financials / Insurance leads all industries with 4.6% projected growth, while Retail / Consumer plunged from ~4% to 1%. Regionally, APAC saw the steepest decline, while Latin America remains the most resilient. While 69% still plan modest spending growth, only 7% are planning to grow spend by bringing on new vendors. Instead, firms are focusing on vendor consolidation, staffing cuts and optimising SaaS licensing.

Japan

Astris Advisory Japan

The effect of rising food inflation

Neil Newman warns of pressure on consumer spending heading into early summer, with food price hikes expected to be particularly sharp this spring. This adds to concerns over frugality in household and beverage consumption, as falling real wages weigh on retail demand. The combination of historically high overweight positions in the Food sectors ETF relative to the index combined with 3-month reversal of flows provides the backdrop to look for structural or fundamental challenged constituents to short. Highlighted names include Kirin Holdings, Meiji Holdings and Coca-Cola Bottlers Japan Holdings.

Emerging Markets

Smart Insider

Punit Goenka (CEO since Nov 24; formerly CEO & MD 2007-2024) buys US$3.1m worth of stock in Mar at INR 96.21 and two months later, spends US$2.4m at INR 119.07. These are the first reported purchases from him and the first meaningful insider purchase from any insider since 2020. Goenka is the son of the founder Subhash Chandra. Zee Entertainment and Goenka have not been short of controversy, including an abandoned takeover bid by Sony Group for the company. That said, Smart Insider finds the CEO's recent purchases interesting and ranks the stock +1 (highest rating).

AlphaMena

AlphaMena maintains a bullish stance on ENBD, viewing the stock’s challenging start to 2025 as an overreaction to its cautious dividend policy, despite a 7% increase in 2024 net profit. The bank’s journey has also been hit by the Turkish political and social crises, fears on Cairo bank acquisition plan and global trade concerns. AlphaMena sees ~40% upside based on intrinsic valuation. Its two-year forward ROE is projected at a solid 17.6%, even amid sector-wide margin pressures and higher taxes across the GCC. They highlight ENBD’s strong retail portfolio, significant exposure to GREs and supportive UAE macro trends as key growth drivers. AlphaMena is also optimistic that Turkey’s economic recovery will support top-line growth, with still-elevated inflation helping partially offset the impact of the interest rate cut.

Galliano's Financials Research

Mexican Banks: Selective value in smaller caps

Aside from Trump’s tariff policies, Mexican banks are under pressure from the government to deliver on more competitive lending rates, with fintech challengers Nubank and MercadoLibre’s MercadoPago gaining traction. Despite these challenges, 1Q25 results were sound and the bank sector participated in the somewhat surprising Mexican bolsa rally in April. In this report, Victor Galliano applies his proprietary scorecard - which assesses valuations, balance sheet strength, returns and credit quality - that is then weighted across ten criteria to arrive at his investment picks; BanBajio, followed by BanRegio, rank as the top two. Inbursa is bottom ranked.

Macro Research

Developed Markets

Steno Research

An increasingly bullish backdrop

According to Andreas Steno, the backdrop is getting increasingly bullish as: 1) financial conditions have eased materially due to the USD debasement in March and April, 2) the Trump administration has made a double U-turn on both trade and fiscal deficits, 3) tech deals are being signed in the Middle East and 4) inflation is not going up. The only surprise for Andreas on Wednesday morning was that USD/CNH was trading higher (at about 7.21 = US$1), likely as a result of the fixing set by the PBoC. The PBoC is probably concerned that they could see a Taiwan-like appreciation of the Yuan if they allow market forces to take over. As a result, investors should expect a very managed descent in USD/CNH over the coming months.

Radio Free Mobile

AI and the Middle East

The Saudi-US Investment Forum revealed a slew of deals that look set to give the region all the resources it needs to execute its AI vision. As Richard Windsor comments, the area has the money, the space and the electricity; the summer heat is the only inconvenience. Richard expects more deals to be announced as Trump visits the UAE and Qatar. However, as they lay the groundwork to become global centres of tech and AI, what they both really need is the private sector but there are signs that this is slowly growing. The region most at risk of losing momentum to the Middle East is Europe, where AI is already languishing and where the EU is attempting to regulate an industry before it exists. Expect AI entrepreneurs to head to the Middle East instead as it flings its doors wide open.

Lazarus Economics

UK: Economy briefing

Darren Winder expects UK real GDP growth to be close to 1.5% in 2025, averaging 2% in 2026. As inflation pressures continue to subside, Darren believes that policy rates can be expected to fall well below 4% over the next 6-12 months, and inflation will fall below the 2% target in H1/2026. The budget deficit is estimated to stand at 2.25% in the 2024-25 financial year, but when the increase in National Insurance contributions kicks in (resulting in tax receipts growth of 8%), Darren forecasts the deficit to fall to 4% of GDP. Over the medium term, and based on current spending plans, his arithmetic shows the budget falling to 2% of GDP.

Grey Investment

Play it Swiss

The Swiss Franc (CHFUSD1.2040) has broken out from a 31-month Rectangle, targeting an advance to CHFUSD1.3250+. At the same time, the monthly chart has completed a bigger breakout targeting CHFUSD1.4000+ (see next page). The Swissie traded as high as 1.2438 following the breakout above the 1.1800-1.2000 resistance zone. Recent weakness is viewed as a retest of the old resistance zone, which should now be support. The 14-day RSI corrected to around 50, and if the breakout is genuine, then Neutral 40-50 should be support. Chris Roberts is 40% long from CHFUSD1.2155, and his stop stays at a daily close below CHFUSD1.0735. He will add if a confirmed daily chart breakout occurs.

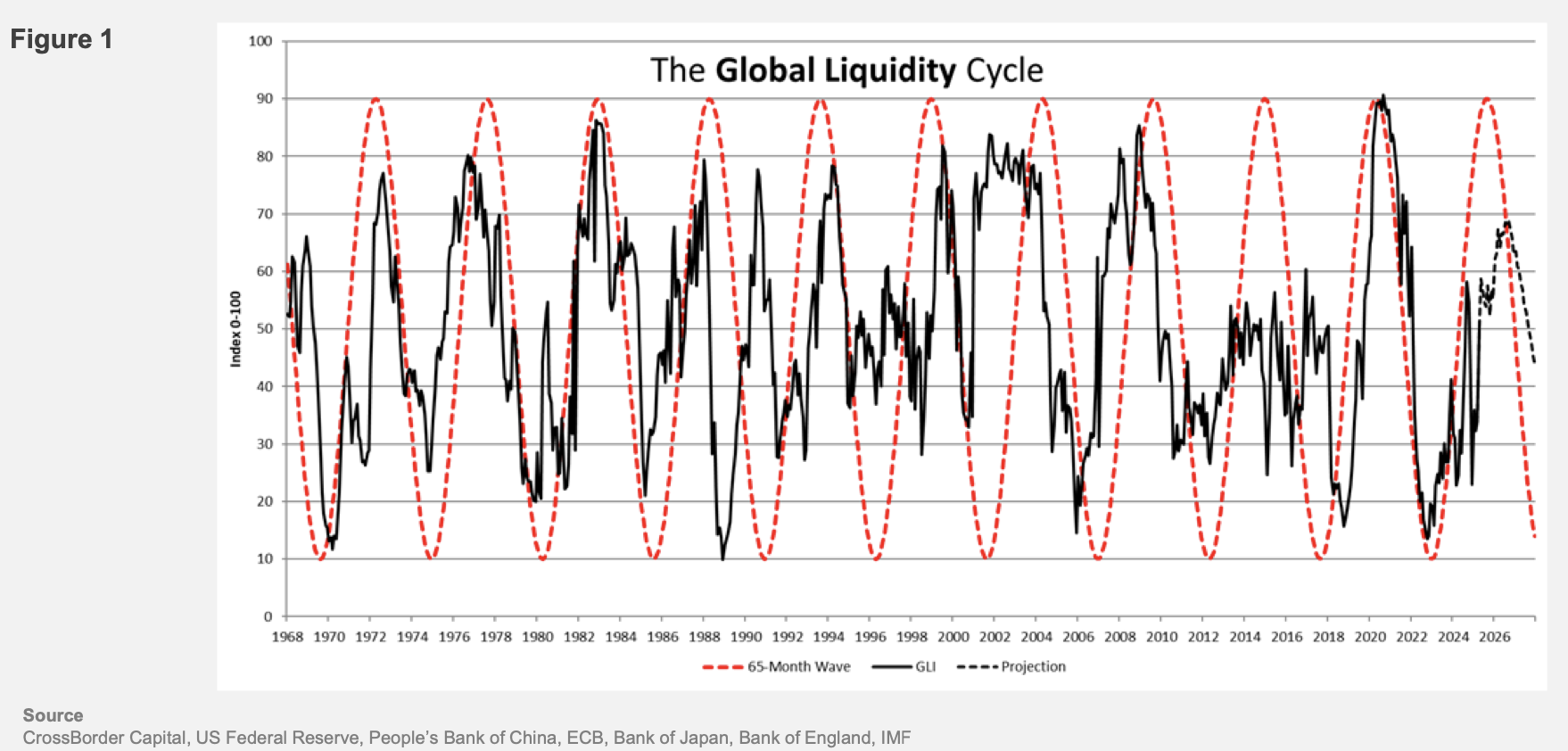

CrossBorder Capital

A looming recession

Global liquidity is edging higher, driven largely by China's aggressive monetary easing to avoid recession amid trade tensions. But, alongside, the US faces tighter future liquidity conditions due to declining private sector cash flows, shrinking bank reserves and collateral shortages exacerbated by the debt ceiling standoff. The modern financial system’s reliance on US Treasury collateral — now paradoxically in short supply — has heightened repo market stress, with key indicators like the SOFR-Fed funds spread and MOVE index flashing several warnings. Despite superficial Fed liquidity gains from TGA inflows and seasonal factors, Michael Howell comments that underlying pressures point to deflationary risks, compounded by the Fed’s reluctance to ease amid sticky inflation and political constraints. This divergence sets the stage for potential liquidity shocks, with China propping up global markets as the US grapples with a fragile debt-refinancing mechanism and the spectre of 1930s-style demand collapse. Investors are reducing risk exposure.

Macrolens

US: An incorrect interpretation

The market is off base about what happened over the last weekend, remarks Brian McCarthy, who argues that the exemptions issued on Friday are not a capitulation, nor are they indicative of a strategy in disarray. The April 11th memorandum pulls products out of the reciprocal tariff bucket into the sectoral tariff bucket and still subjects them to the fentanyl tariff. Brian also likens the wider situation to the 1992 ERM crisis or an EM currency attack and claims that the Fed’s persistent hawk-yapping can only fuel the brewing credibility crisis affecting the USD and Treasuries. Like it or not, the US is now in an economic war with China that revolves around who can inflict and withstand the most economic pain. Should the Fed make the mistake of allowing monetary policy to tighten into a supply shock, the US may well lose the economic war. Counterintuitively, a less hawkish Fed is USD bullish.

Vermilion Research

US lockout rally continues

While the Vermilion team have been short-term bullish for three weeks on the SPX, there are a few things that held them back from shifting to an intermediate-term bullish outlook – until now. The 2.5-month uptrend on high yield spreads was violated last week as the team discussed in a recent report, but now spreads are also decisively narrowing below the crucial 355bps level. Additionally, the steep 3.5-month RS uptrends on defensive Sectors Staples (XLP) and Utilities (XLU) are officially breaking. When combined with the other ingredients for a major bottom, this all suggests a bullish longer-term outlook is appropriate. The team are monitoring for potential resistance at 5860-5910 on the SPX as a spot where it could pull back, which would present buying opportunities.

Emerging Markets

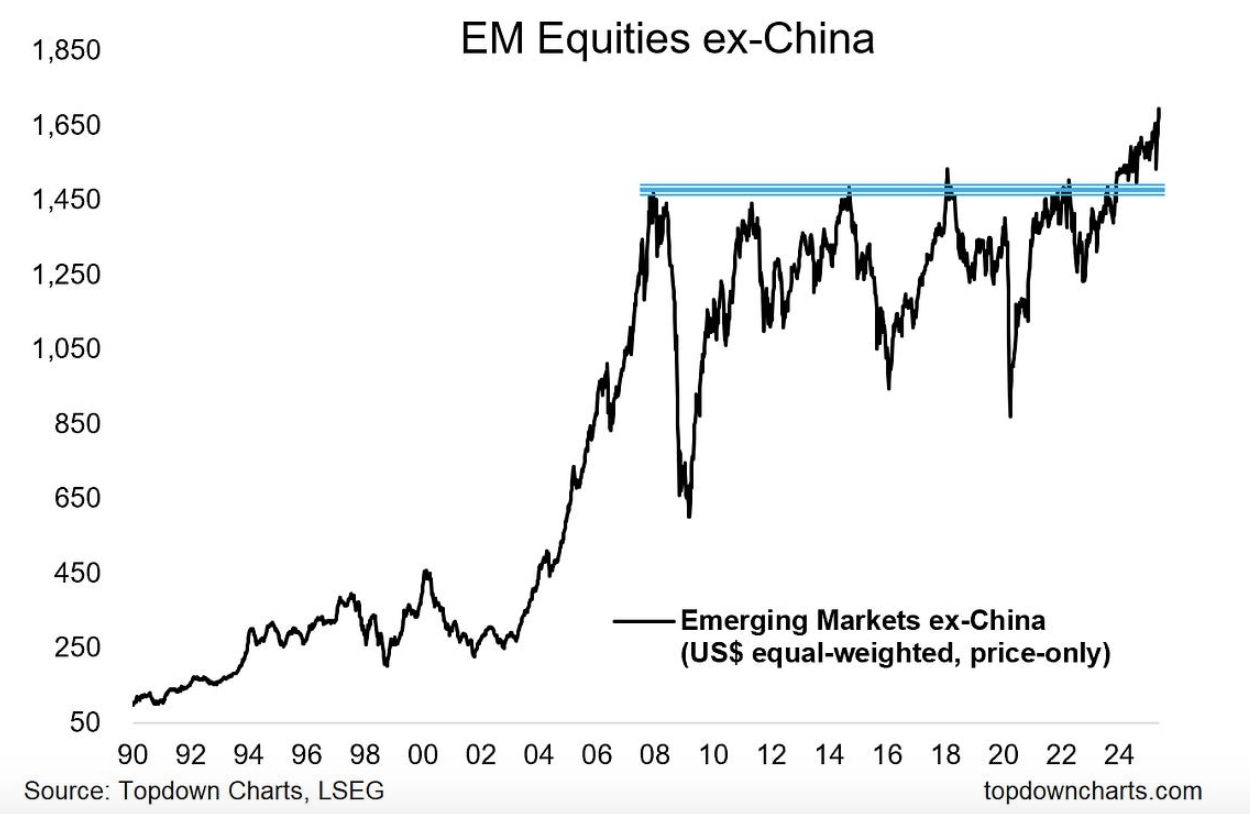

Topdown Charts

The EM Breakout

Callum Thomas comments on one of the most important charts that many investors have never heard of, which he first posted in July last year. It shows EM equities ex-China breaking out from a Brobdingnagian Base 16-years in the making. Not only has the breakout withstood the tariff tantrum, the index has gone onto new all-time highs. There are many examples of similar patterns throughout history where the scene is set for a multi-year bull run. Ultimately, EM equities are undervalued, underowned, and underestimated – and it seems investors don’t realise what’s underway.

PRC Macro

US-China ceasefire doesn’t eliminate market risks

The US-China tariff ceasefire is a win for Beijing. From what William Hess can tell, the Chinese side committed to very little in securing a broad tariff rollback, including a reduction of de minimis tariffs to 54%. However, when markets reopened, they were not trading as expected. William sees markets in Asia trading around two themes: 1) The very modest recovery to metals prices reflects lingering concerns over global growth and the risk of Beijing failing to deliver meaningful stimulus. However, investors are expecting more front-loaded restocking of imports from China by US firms. 2) A rebound to gold prices and a weaker dollar suggest that other US trading partners, especially the EU and Japan, will follow China’s lead and take a tougher stance in future trade negotiations with the US. William thinks investor concerns are warranted and doesn’t see the US-China tariff ceasefire as a credible put against market volatility.

Andrew Hunt Economics

China’s hidden USD assets

Andrew Hunt believes China’s true net foreign position vis-à-vis the USD may be several trillion dollars more in China’s favour than official data suggests. Mr Bessent had a weak hand when he flew to Geneva. There are few – if any signs – that much of this money has moved from the USD so far. Much of it may be tied up in illiquid investments. If China’s asset managers were to redeploy (rather than repatriate?) these funds, the positive impact on crypto, gold and other alternatives would be significant, as would the damage inflicted on property prices and other conventional assets. Any redeployment could force the Fed into a direct YCC policy. In many respects, any attempt at a significant redeployment of China’s monies in the USD would represent a form of MAD – higher inflation and weak asset prices in the USA and an economic calamity in China. The stakes are high.

Alberdi Partners

Feeling Chile

Chile is entering electoral mode, with candidates competing for support, but over half of voters remain undecided. While voters may punish the outgoing leftwing administration, the moment is ripe for an anti-elite candidate with a law-and-order, pro-growth message. Marcos Buscaglia has revised his 2025 GDP growth forecast to 2.1% from 1.9%, despite expecting a slowdown in the second half. Inflation surprised to the downside at 0.2% month-on-month (vs. 0.3% expected), but core prices rose, and the fiscal anchor remains under pressure, suggesting inflation is likely to exceed consensus. Although some expect rate cuts, Marcos believes the central bank should maintain or raise rates to restore its lost inflation anchor, as his Taylor Rule model does not support cuts. However, with the central bank considering a 25bp cut at its last meeting, a reduction remains plausible.

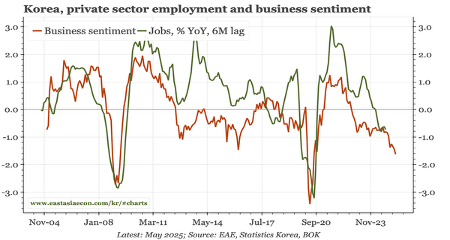

East Asia Econ

Korea: Structural changes weakening the labour market

Paul Cavey notes that unemployment remains low in Korea, but wage growth isn't accelerating. The reason is the big structural changes in the labour market of recent years, which have increased the number of part-time jobs. That shift is likely to reduce the bargaining power of labour and generate a structural slowdown in wages. Cyclically, the labour market isn't a driver in how the BOK will think about inflation. The unemployment rate in April remained below 3%, as employment ticked up while the participation rate was unchanged. However, while the rise in employment in April was driven by the private sector, that isn't likely to last, with business sentiment continuing to signal a decline in hiring over the next few months and the openings rate falling fast.

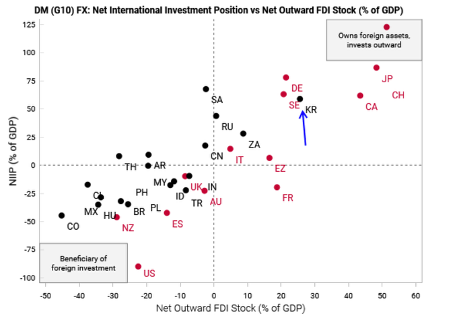

Variant Perception

Korea: Taking the long view

South Korea is a less extreme version of Taiwan, where current account surpluses have also been recycled into US assets. Despite persistent current account and basic balance surpluses, the KRW real effective exchange rate is very weak, making Korea an outlier within EM. The country’s net international investment position is very large relative to GDP at 60%+, which is also reflected in the balance sheet. Similar to Taiwan, the BoK has been accumulating foreign assets and partially sterilising since the GFC, and just like Taiwan, the KRW may appreciate as these decade long structural imbalances start to normalise. To help control for the carry of a long KRW position, the Variant Perception team like shorting CNH against a long KRW position.

Krutham (formerly known as Intellidex)

South Africa: The cost of the deal

President Cyril Ramaphosa is scheduled to meet Trump next week, raising expectations that a trade deal could be signed soon. However, Peter Montalto is skeptical about what can be delivered next week or indeed in the short to medium run. South Africa has set its sights on negotiating a trade deal with the self-proclaimed deal artist, Trump, framing the deal as serving two purposes: appeasing Trump’s transactional approach to foreign relations to get him off their back and to respond to tariffs and threats to South Africa’s eligibility for Agoa. However, the Trump administration is unlikely to separate foreign policy concerns from trade issues. The lack of meaningful preparatory bilateral negotiations below principal level also means more time is needed. South Africa therefore faces the difficult task of making some compromises which could be tantamount to giving up some of its sovereignty, as well as making trade concessions – or preparing for a four-year-long US onslaught.

Commodities

Astris Advisory Commodities

US-China: Good news for all… except ferrous

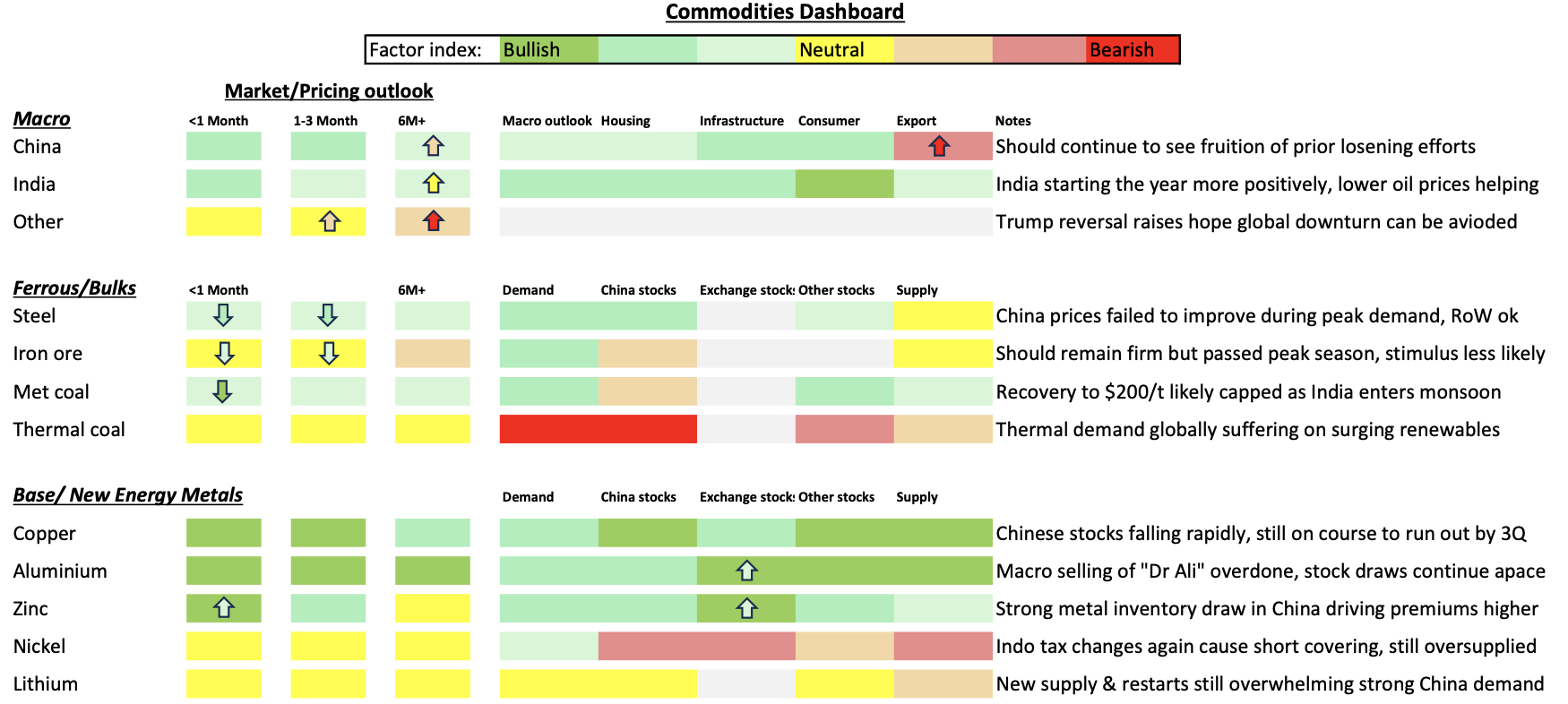

Alongside gold, Ian Roper points out that the one sector that looks consequently less attractive post a significant deal between the US and China is ferrous. Chinese steel demand is passing its seasonal peak, and iron ore prices may come under pressure as Chinese steel output declines. Met coal prices may come under renewed pressure after their recent rally back to $200/t, Ian sees a very depressed outlook for thermal coal in light of the accelerating shift to renewables in many key markets. Base metals should see more relief on a trade agreement. Zinc is seeing China inventory drawing to extreme lows as steel output continues to grow, and onshore metal premiums have recently soared, leading Ian to expect a reversal of its recent underperformance. Ian also comments that despite strong inventory draws, aluminium appears to be the most oversold on macro.

WHB Energy Research

Oil and gas: Changing sentiments

William Brown remarked a few weeks ago that the onerous tariffs and potentially debilitating impact on the economy and in turn on refined product were self-inflicted and could be reversed. Sentiment has shifted, as expected, although William remained steadfast in his long-standing base case for economic activity. With the recovery in crude oil prices, the NYMEX crude oil contract is about $2.00 per barrel below the peak of his previously delineated trading range. As such, William would only add to that length upon any retracement, barring unexpected bullish news and/or data. In terms of natural gas, he believes selling August NYMEX natural and buying September, either legging in or as a spread has modest profit potential.

Global Mining Research

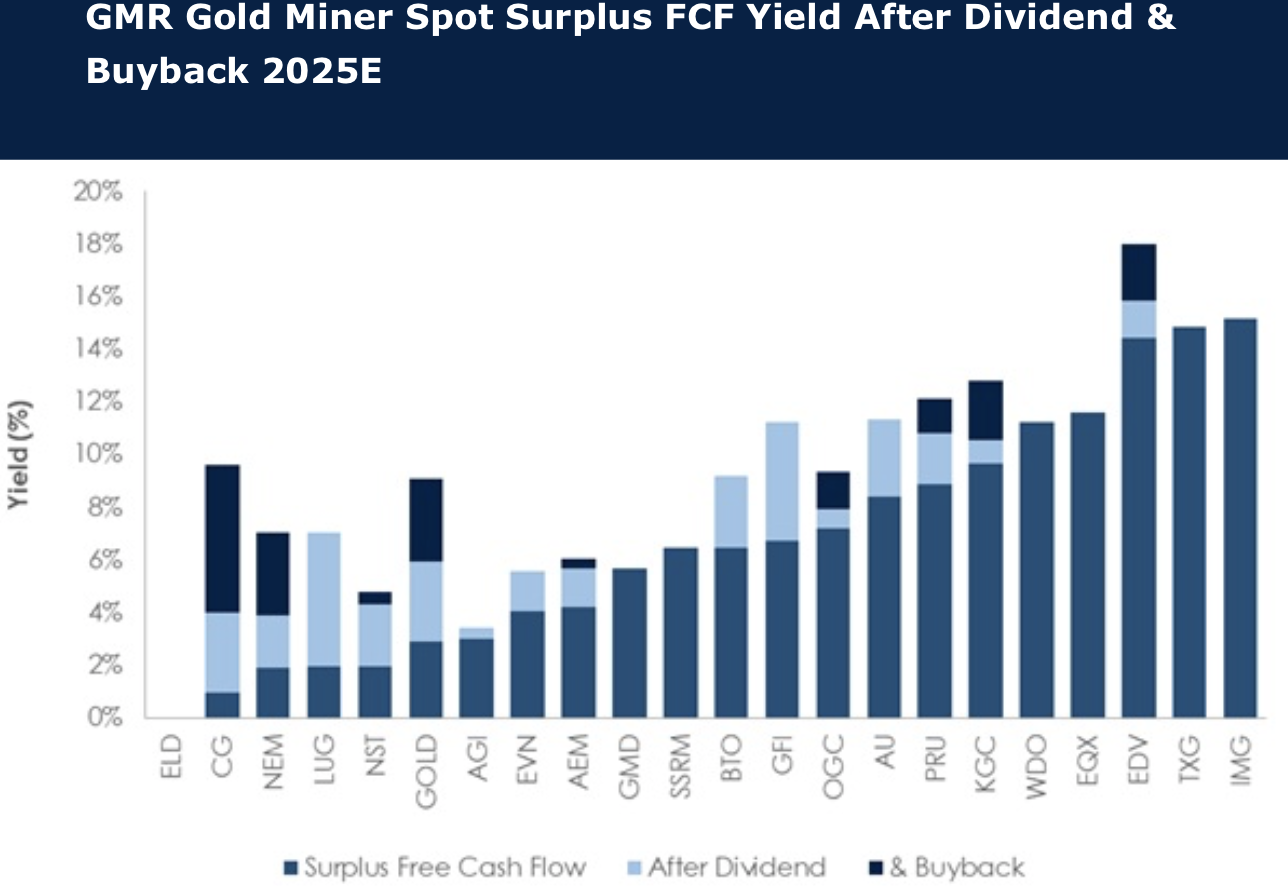

Gold: Are buybacks a fad?

In the face of meaningful cash surpluses, miners are repurchasing shares in record amounts. Some 40% of the Global Mining Research team’s gold coverage have active buybacks in 2025E, equating to ~US$3.7B of cash returns, a record level for the sector and equivalent to ~US$110/GEO. The impact on share prices is subject to debate. The team find that at spot gold the 2025E FCF yield of the sector after expected dividends and buybacks is ~4.6% (and ~8.5% in 2026E). So, shareholder return potential is still to the upside whilst gold prices remain elevated. Stocks least progressed (~20% or less) with buybacks include Carlyle Group, OceanaGold, Barrick Gold, Kinross Gold and Agnico Eagle Mines. Stocks trading at larger discounts to 2025E spot FCF include IAMGOLD, Torex Gold, Endeavour Mining, Equinox Gold and Wesdome Gold Mines. Preferred stocks of these are Kinross Gold, Agnico Eagle Mines, IAMGOLD and Equinox Gold.

10x Research

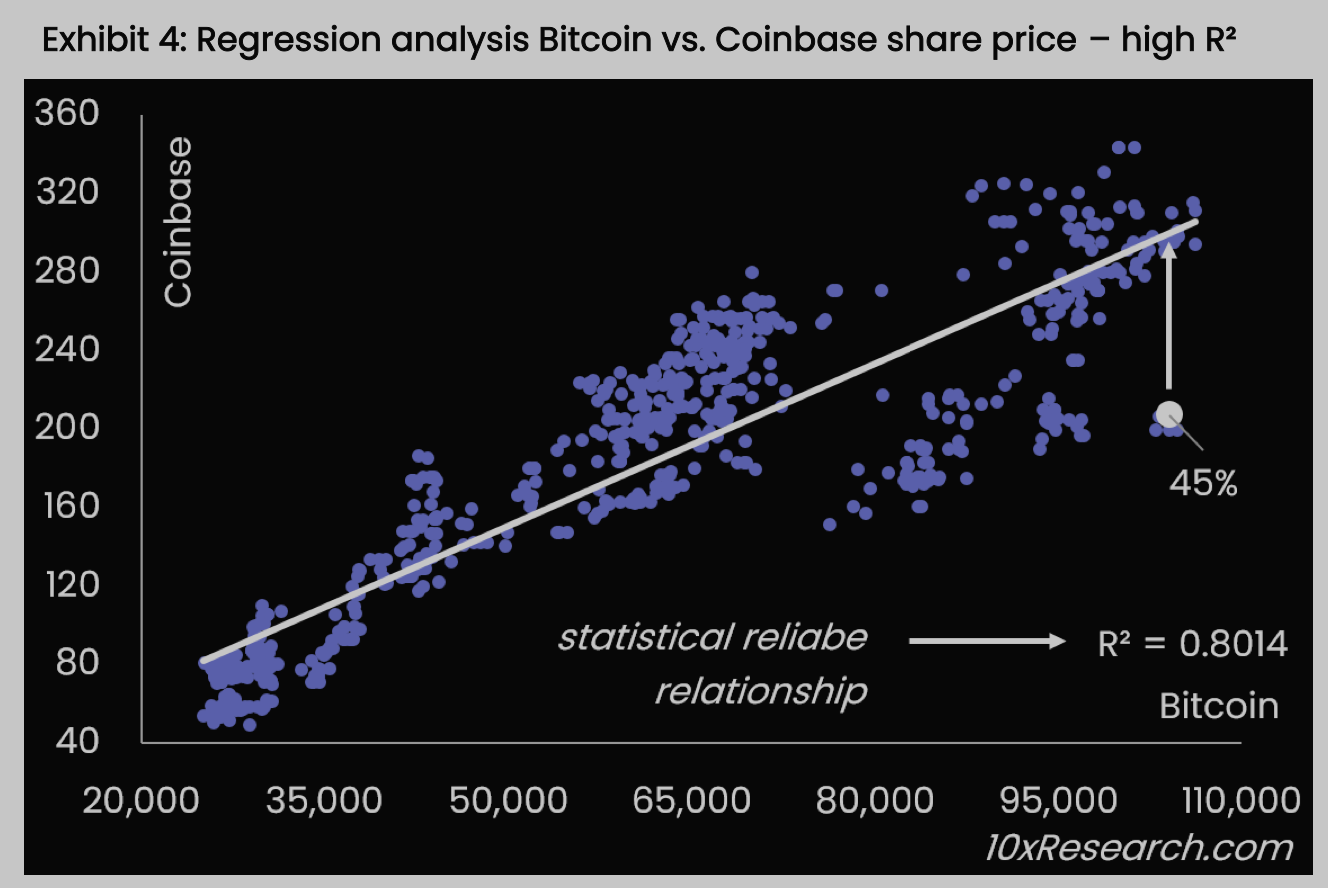

Crypto: Soaring higher

Bitcoin's explosive +160% rally since January 2024 has exposed the fragile economics of Bitcoin miners, with most struggling to keep pace. 10x Research reveals that only a few miners, such as Core Scientific, which achieved +187% gains, have outperformed Bitcoin, while others face rising costs and declining profitability. In contrast, Coinbase offers a more compelling opportunity, with a clear correlation between its stock price and Bitcoin, making it a better play in the current market; their regression with Bitcoin analysis reveals a potential upside of +45%. The team also recommend a spread trade: long Bitdeer vs short Marathon Digital. As Wall Street eyes crypto IPOs worth $100 billion, the stakes have never been higher for the crypto industry.

CPM Group

Gold and silver: Seasonal weakness

In his latest video, Jeff Christian, provides an in-depth update on gold and silver prices, which have seen significant volatility amidst ongoing economic and political uncertainties. He looks at recent US inflation data, offering a clear analysis of trends affecting consumer prices, and explains the market reactions to tariff announcements and international political developments. Additionally, Jeff honors the legacy of Don Mackay-Coghill, whose visionary leadership profoundly influenced the global bullion market. The presentation concludes with a look at CPM Group's latest forecasts for gold, silver, platinum, and palladium and the indicators that could predict the next moves for the metals. Jeff expects some seasonal softness in the prices of gold and silver in Q2 and Q3 but remains bullish about the outlook further ahead.

Click here to watch.