Europe

Starlink: What impact might it have on the telcos?

Communications

New Street assesses the potential threat of Starlink to European telecom operators, emphasising that the risk comes primarily from Starlink’s direct-to-dish broadband service rather than the more publicised direct-to-device satellite offering, which they see as limited and possibly even accretive to mobile operators. Currently, Starlink's penetration in Europe is just 0.3-0.4%, with existing infrastructure supporting up to 1%. A full rollout of the V2 constellation could raise that to 1.4%, while a longer-term deployment of 15,000 V3 satellites could theoretically push penetration to 8-10%, though this would take over a decade. However, FTTH rollout, dish siting constraints and pricing remain key barriers, and New Street sees limited near-term disruption to wireline telcos.

Consumer Discretionary

Following publication of the company’s FY24 annual report, Iron Blue’s DHER score of 30/60 remains top decile and fertile grounds for shorting. Stripped out costs remained elevated and materially exceeded FY24’s €48m PBT adj, while capitalisations expanded to 28% of total FY24 R&D expense from 20% in FY23. There were 2 changes to the group’s contingent liabilities disclosure: 1) a significant increase in the range of potential financial penalties from investigations into the legal status of riders to €440m-€770m; and 2) a new claim against Glovo Spain from Just Eat alleging unfair practices. Iron Blue also notes a reduction in Woowa’s goodwill impairment test margin assumption to 23% from 30% (albeit offset by a higher growth expectation).

Is liquor the next luxury?

Consumer Staples

David Scott argues that luxury liquor companies are facing the same structural challenges confronting luxury apparel. While pandemic-era demand and post-Covid inflation masked underlying weaknesses, those issues are re-emerging. Key headwinds include shifting demographics and declining alcohol consumption among younger generations, as well as industry overpopulation and fragmentation. Liquor companies are experiencing falling asset turns but margins have not risen to compensate and the operating leverage effects will be "very vicious" as a result. David also sees the rising use of weight-loss drugs like Ozempic as a further negative catalyst. Companies discussed include Diageo, Pernod Ricard, Brown-Forman, Kweichow Moutai and Wuliangye Yibin.

Office Real Estate outlook

Real Estate

Kolytics’ report assesses the rapidly evolving office real estate sector, where shifts in work preferences and economic softness weigh on demand. While US markets face oversupply and high capital requirements, European markets benefit from lower vacancy and more stable fundamentals. Deep discounts to replacement cost offer selective opportunities, but investors must be wary of capex traps and polarising tenant demand. In a fragmented landscape, landlords who adapt quickly and investors who stay selective will be best positioned to capture risk-adjusted upside. Buy-rated stocks include BXP, Castellum, Covivio and PSP Swiss Property. Sells include British Land, Inmobiliaria Colonial and Mobimo.

Technology

Besi surprised the market at its latest CMD by significantly raising its long-term financial targets for the first time in 3 years - particularly its revenue outlook, which increased by 15-45%. While improvements in gross and operating margin were expected, the scale of the revenue uplift signals strengthening demand for semiconductor back-end equipment and a more optimistic outlook for hybrid bonding. Though these targets lack a fixed timeline, Besi now projects mid-point revenues of €1.7bn, gross profit of €1.1bn and operating profit of €0.8bn, implying EBITDA of €850m. With an EV of €9.25bn, this equates to a modest 11x long-term EV/EBITDA. The upgrade supports a compelling growth story likely to attract renewed investor interest.

North America

Do tariffs and pricing matter?

Trivariate used NLP to analyse 2,488 earnings calls since Mar 25, finding that 37% of companies mentioned both tariffs and pricing - most notably in Materials, Consumer Discretionary and Consumer Staples sectors. Lower-quality and value stocks were more likely to raise the issue. The most cited terms were “uncertainty” and “indirect impacts”, flagged by 584 companies including Microsoft, JPMorgan and Coca-Cola. From a performance lens, firms discussing tariff benefits or direct price pass-throughs outperformed by over 3% vs. those referencing absorption or uncertainty. "Price increases" and "surcharges" were associated with weaker performance, while "wait and see" commentary outperformed.

Breaking Growth: Best short candidates

This particular model from Two Rivers identifies stocks where the growth narrative is called into question. It flags names with slowing growth, margin declines, earnings/sales misses, troubling working capital trends, poor estimate trends or lowered guidance, among other characteristics. These potential shorts typically carry moderate-to-high betas, time horizons of 3 to 12 months, higher valuations due to historically strong growth and are often “market darlings”. From ~40 flagged names, Garmin, Freshpet, SharkNinja and Sportradar are discussed in further detail.

Communications

A high-quality business with a sustainable competitive advantage, underpinned by strong FCF generation, limited debt, low stock-based compensation dilution and 70%+ EBITDA margins (with incremental margins over 90%). Its proven dominance in gaming advertising through advanced AI engineering is now being leveraged to expand into new verticals like direct-to-consumer ecommerce, where Abacus sees a high probability of success. The 2Q25 launch of self-service tools could further accelerate growth, supporting a bullish outlook for this year and next. Abacus expects rapid FCF growth through 2027, which the market has yet to fully price in. Their TP of $635 offers 65% upside.

Communications

Andrew Freedman initiates a short on RBLX, contending the market is underestimating structural headwinds that will pressure the stock over the next 12-18 months. His proprietary Metaverse Tracker shows strong 2Q25 DAU trends - driven primarily by the success of Grow a Garden and favourable calendar dynamics - marking what he views as peak growth. However, Andrew’s analysis points to limited runway for sustained user acquisition at current growth rates, a more challenging competitive landscape and increasingly difficult comps. He expects a sharp deceleration in growth and monetisation, diverging meaningfully from consensus. At ~$95, he sees limited upside ($10-15) and significant downside risk ($30-40).

Consumer Discretionary

Chuck Grom maintains a Buy rating on FIVE following a strong 1Q25, with 7.1% SSS growth and $0.86 EPS, both ahead of guidance. The company's swift turnaround, driven by leadership changes and a return to core strengths in merchandising, marketing, value and customer experience, has exceeded expectations. Traffic growth (6.2%) and broad-based sales gains support Q2 SSS guidance of 7-9%, which Chuck sees as potentially conservative by ~300bps. He believes FY25 EPS could plausibly exceed $5.50. FIVE stands out as one of the few names he covers that can strongly argue the case for both EPS upside and a higher multiple.

Drug Pricing: MFN outlook & IRA guidance

Healthcare

Over the past several weeks, the Trump Administration has aggressively moved forward with its drug pricing agenda, including releasing its Executive Order on Most-Favored Nations and, perhaps more importantly, guidance on how the Administration will implement the IRA’s negotiation provisions. To examine this evolving legal and policy landscape, Aldis hosted a discussion with former Senate Finance Committee Staffer Anna Kaltenboeck. Key topics included: 1) Outlook for a Trump-era MFN pricing policy revival: legal feasibility, policy options (IRA vs. CMMI) and market risk. 2) Implications of recent CMS guidance on IRA price negotiation. 3) SubQ drug formulations: payer incentives, coverage challenges and Part B-to-D transitions. 4) Industry strategies to mitigate IRA revenue impact amid pipeline repricing pressure.

Healthcare

Bios removes its high-conviction short on TWST following a 25% decline since initiation (vs. S&P +20%, IBB -10%). Their original thesis cited commoditised gene oligomer revenue, slowing growth, high OpEx, lack of product differentiation and overhyped DNA storage tech. While TWST remains unprofitable, cost discipline has improved, margins are recovering and the recent decision to spin off its DNA storage segment is strategically sound. Bios still views TWST as overvalued but acknowledges a more realistic path to profitability, warranting conviction removal. Bios continues to find success with short ideas in medtech, commercial biotech, over-hyped AI, and medical supplies and tools.

Industrials

Hamed Khorsand reiterates a Buy on ARLO with a TP of $24 (40% upside), highlighting the company’s stronger-than-expected growth trajectory after surpassing $300m in ARR a month ahead of schedule. This milestone reflects success from consolidating subscription tiers and prioritising service revenue, including selling cameras below cost to drive post-trial subscription conversions. With over 50% hardware-to-subscription conversion, an upcoming product refresh and positive FCF, Hamed believes ARLO is attracting broader investor interest. Continued buybacks offsetting stock comp further support the bullish case.

Technology

2Xideas sees KEYS as a high-quality compounder with strong competitive advantages and secular growth tailwinds. As the global leader in RF test and measurement solutions, the company benefits from resilient R&D-driven demand (~60% of revenue), ensuring high margins and customer lock‑in. It has built a powerful flywheel around its PathWave software ecosystem. Structural growth trends (5G Advanced, 6G R&D, data centre networking led by AI/ML, automotive electrification semiconductors) drive increasing complexity and testing intensity across value chains, supporting 5-7% organic revenue growth. Operating margins to expand by 480bps to 30.5%, with EPS expected to grow at an 11.4% CAGR through FY31E. 2Xideas sees a potential 2x return with upside from M&A and buybacks.

Technology

SPR’s latest channel checks suggest RBRK is evolving from a backup player into a recognised leader in data security. Systems integrators report strong traction in large enterprise accounts, driven by RBRK’s security-first messaging, ransomware protection and smooth implementations. Channel partners note upbeat sentiment, strong execution and growing confidence in the company's ability to deliver. In cloud marketplaces (AWS, Azure, Google Cloud), RBRK’s visibility is increasing thanks to deep cloud-native integrations, AI-driven features and new partnerships like Rackspace’s Cyber Recovery Service. With a ramping product roadmap and rising adoption across cloud and security use cases, RBRK’s momentum looks set to accelerate through 2025.

Emerging Markets

Consumer Discretionary

Report by

Blue Lotus Research Institute

Blue Lotus sees BABA as the likely winner in China’s intensifying O2O war, thanks to its unmatched SKU breadth, vast dormant customer base, Ele.me infrastructure and Alipay ecosystem. O2O provides a strategic opportunity for BABA's new management to refocus its e-commerce business. Meituan and JD face structural limitations: Meituan lacks SKU depth; JD lacks cross-sell leverage. JD may emerge as a secondary winner if it can convert Plus members to food delivery users, though heavy 2025 losses (~RMB12bn) are expected. PDD is most at risk without swift action. Government pressure to cool price wars favours BABA. Meituan’s 618 Instashopping saw explosive growth, but margin challenges remain. JD’s strong start in food delivery may stall amid subsidy rollbacks and financial constraints.

Energy

EM Spreads recommends buying Vista’s new 2033 bonds, citing an attractive 8.5% yield and shorter duration relative to the 7.625% 2035 notes (yielding 8.3%). The bonds offer a more compelling return within Vista’s debt capital structure and screen wide relative to the broader EM BB and LatAm BB curves. Strong execution on well tie-ins and midstream expansion supports the group's ambitious EBITDA and production targets. EM Spreads views Vista as a top credit pick for exposure to Argentina’s energy sector, with relative insulation from sovereign risk. They believe operational momentum and an improving macro backdrop, including easing capital controls, could drive bond outperformance over the next 9-12 months.

Real Estate

Lucror holds a "Negative" fundamental credit bias on Longfor, expecting continued declines in contracted sales and earnings in FY25 due to slower land-bank replenishment. However, they see low near-term default risk, supported by the company’s pipeline of new malls, which should help maintain access to secured bank loans for refinancing. Lucror also views management’s commitment to further debt reduction positively. Despite the negative bias, they maintain a Buy recommendation on the LNGFOR notes, with the 3.375 '27s at 88.1/10.7%/1.7 years and the 3.85 '32s at 70.4/10.1%/5.3 years. They view the low double-digit yields as attractive, considering Longfor's sound fundamental credit profile and their expectation of further government support for the property sector.

Developed Markets

The return of Yellen-omics

Global Liquidity is rising again. The weaker USD is allowing foreign policy makers to ease. There is evidence of recent surges in Chinese liquidity. Alongside, despite a seemingly more ‘hawkish’ Fed, Michael Howell remarks that the US Treasury appears slated to continue ‘Yellen-omics’, namely deliberately funding fiscal spending in short-term markets and, hence, monetizing the Federal deficit. He advises to watch T-bill issuance and bank balance sheets — they’re the new drivers of asset prices. Stagflation is the growing risk, and traditional Fed easing may stay in the background. The US Fed is frozen by inflation concerns, but the Treasury is pumping liquidity. The ‘everything bubble’ continues, with Michael positing our position as being in late-cycle regime that has many parallels with the late-1980s. More global liquidity will support risk assets.

UK: Mortgage lending retreats after stamp duty rush

Mortgage approvals for house purchases dropped to 60,000 in April, below the first quarter’s 65,000 monthly average but in line with the 2010-2019 norm. The decline reflects an unwinding after transactions surged ahead of April’s stamp duty increase. Transactions leapt to 177,000 in March, then fell similarly in April, averaging 120,000 monthly across the two months, versus 90,000 in 2024. New mortgage interest rates held steady near 4.5%. Following March’s £13bn spike in net mortgage lending, April recorded a slight contraction, with annual lending growth easing to 2.5%. Cash ISA deposits hit a record £14bn in April, offset by a £17.75bn fall in instant-access deposits. Overall deposit growth slowed to 4.9%, though still surpassing household loan growth. As interest rates continue to drift downwards, growth in household deposit and loan growth will, in Darren Winder’s view, become more closely aligned, boosting household spending accordingly.

EUR/USD: Stability in rocky waters

The EUR/USD pair performed in line with ABCG Research’s forecast, briefly touching a new high near 1.1490 but remaining firmly capped below the 1.1500 resistance level. While the broader outlook for the euro remains constructive, short-term risks have resurfaced, driven largely by geopolitical tensions and shifting monetary dynamics, and increasing defence budgets leading to heightened fiscal concerns. Economic data shows signs of recovery, adding a layer of stability and support to the euro in the medium term. ABCG Research’s technical analysts highlight the possibility of a short-term pullback toward the 1.1100 support zone, especially if the USD Index (DXY) experiences a rebound in the wake of US-China trade developments or higher-than-expected US inflation. Despite short-term downside risks, ABCG Research maintains a bullish medium-term outlook on the EUR/USD pair, expecting it to eventually break above the 1.15 barrier as macro fundamentals in Europe continue to improve and the U.S. dollar remains structurally pressured.

US: A cluster of sell signals and complacency

A net 10% of Variant Perception’s trading signals on ETFs and single stocks are active and flashing sell (see chart). Equity traders are looking too complacent, which the team define as when the S&P500 is not reacting to rising risk signaled by 10y yields, the VIX or the MOVE over the past 1 month. Tariff front-running has propped up economic activity, but as this exhausts the country is moving towards a window of growth vulnerability. In terms of hedging structures, the team like August VIX call spreads offering 7:1 max payout: buy 1x VIX 25 Call 08/20/2025 expiry, sell 1x VIX 30 Call 08/20/2025 expiry. Alternatively, given the rise in yields since May, the team like buying cheap optionality on more Fed cuts before year end, betting on 2–3 additional cuts. They like 1x2 call spreads on SOFR Dec 25 for zero/minimal upfront premium: buy 1x SOFR Dec 2025 96.25 Call, sell 2x SOFR Dec 2025 96.75 Call.

Trumping the agenda

According to Helen Thomas, the BoJ, the Fed and the BoE will all be unchanged next week. The first two want to wait and see what happens to tariffs, whilst the BoE remains split over how soon to deliver the next interest rate cut. The BoE can't even rely on data as their guide, not that the data really matters right now, with political decisions the driver of the economy. Fiscal policy, trade and tariffs will be right back in focus before Congress breaks up for summer after Independence Day, with President Trump hoping the Big Beautiful Bill has become law, that the pause in reciprocal tariffs has yielded big beautiful trading partnerships and the NATO Summit has the whole western world, rather than just America, tooled up and ready for war. Expect a ramping up of threats, intimidation, handshakes and back slapping, all at once.

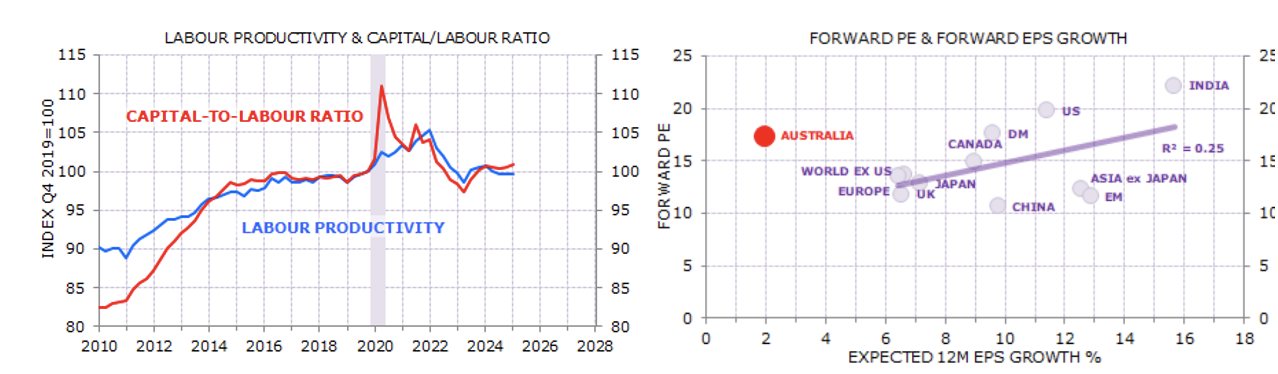

Australia: The stagnation nation

According to Gerard Minack, Australia remains stuck in a macro rut. GDP is stagnating, with per capita GDP having grown in only one of the past 11 quarters. The key problem is flat-lining productivity, and that reflects the lack of capital deepening (see chart 1). Low investment and fast population growth prevent capital deepening and productivity growth. The result is stagnant real incomes and falling per capita GDP. The RBA may have room to keep cutting, but that will provide only symptomatic relief to what are structural, not cyclical, problems. This malaise is also reflected in anaemic corporate earnings, but not in the equity market’s premium valuation. The country offers European-style growth at a US-style multiple (see chart 2). The high valuation may reflect domestic investors’ willingness to pay a premium to access high tax-advantaged dividend yields, but it may also reflect the pressure-cooker effect from Australia’s enormous compulsory investment savings.

USDJPY could head to the 120s this year

Neil Newman expects the Japanese yen to strengthen significantly in the second half of 2025, targeting the ¥120s by year-end, driven by structural pressure from ongoing trade negotiations with the US. The US Treasury has called on the BoJ to tighten policy, signalling growing US-Japan consensus on the need to correct the yen’s weakness. The weak yen over the past three years has raised import costs, fuelled inflation, and contributed to a surge in Japanese SME bankruptcies, as energy, food and material prices soared. Trade negotiations between Japan and the US, covering sectors like autos, agriculture, and defence, are likely to conclude soon and could act as a key catalyst for a stronger yen. Meanwhile, President Trump’s push for a weaker dollar has added momentum to the downward trend in USD, reinforcing the case for a significant yen rebound in the months ahead.

What ails JGBs

The MoF understandably believed that it was being prudent by trying to bolster Japan’s fiscal reserves over recent weeks. However, this overfunding of the deficit, on top of the BoJ’s QT, a weak net external counterpart to liquidity growth, and against a background of only modest JGB demand from the banks, has placed upward pressure on yields and crashed monetary growth when the real economy is already softening. High food prices are inflationary to the CPI but deflationary for growth. Andrew Hunt finds that Japan now possesses a small negative output gap for the first time since the pandemic. Given these trends, investors can expect the MoF/BoJ to conduct a further policy U-turn despite high price rises. Andrew suspects that the BoJ’s actions will soon lean more doveish. Indeed, he says Japan’s shift from over-funding to under-funding could occur as the US Treasury begins its own heavy issuance later this summer, ultimately favouring the USD.

Emerging Markets

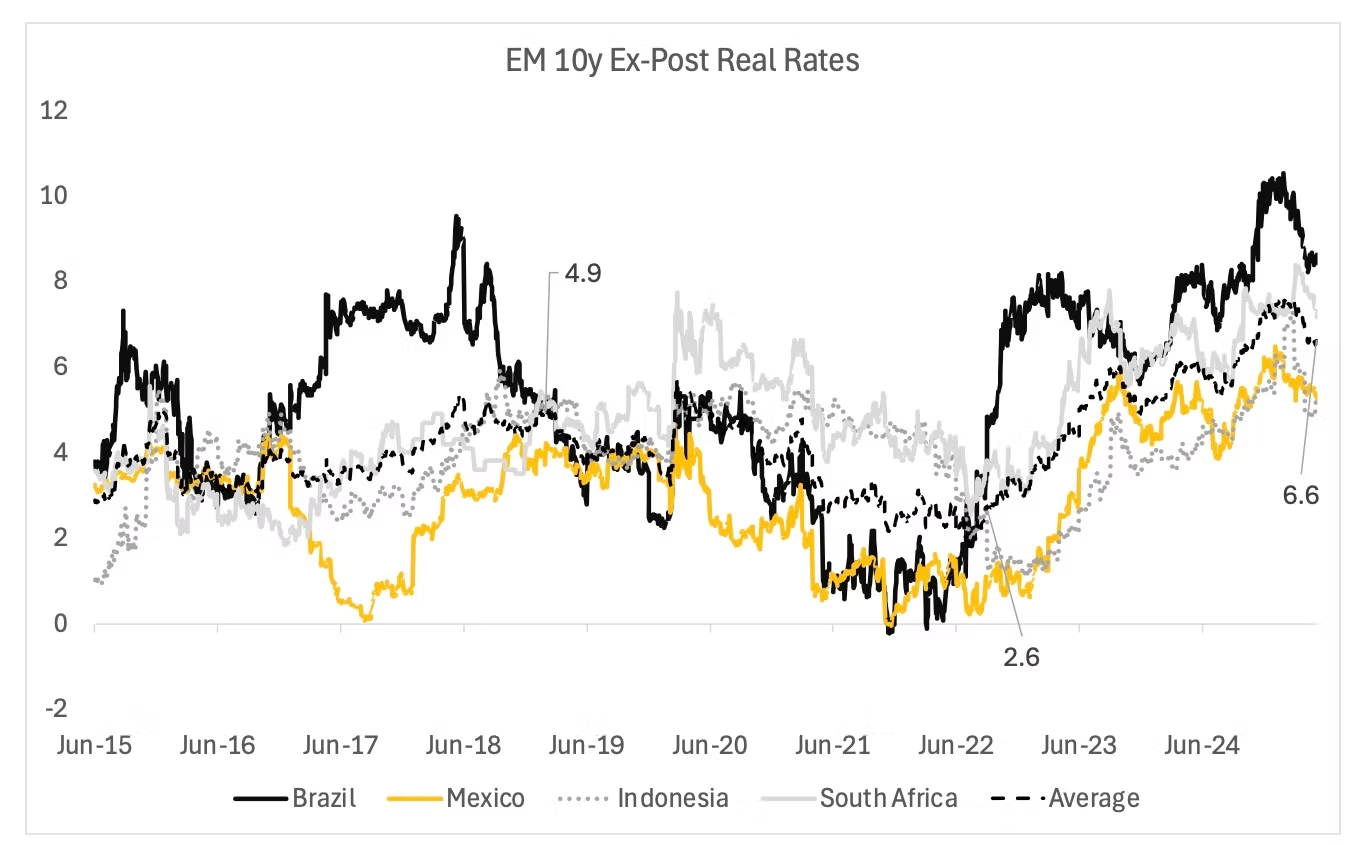

Despite easing, EM still offers standout real yields

Against the backdrop of the trade war, weaker USD and widespread easing of monetary policy, David Woo has been taking advantage by entering long duration exposures in Brazil and Mexico. The weaker USD has also collaborated to a large EMFX outperformance. EMLC total returns this year reached 9.2%, outperforming AGG, HYG and LQD, and even SPY total returns at 2.6%. Term premium in EM local rates remains extraordinary. In the chart, David collected ex-post real 10y interest rates (10y – realised CPI). For the most popular local bond markets in EM a simple average of these economies’ real interest rate was 4.9% before the Great Lockdown, and the average real rate is still extraordinary, at 6.6%. To put this in perspective, 10y TIPS yield is 2.2% and the simple average of these four countries CDS is 136bp. Adding these two together would imply a fair value real rate of 356bp, or 300bp below the current real interest rate in the four markets.

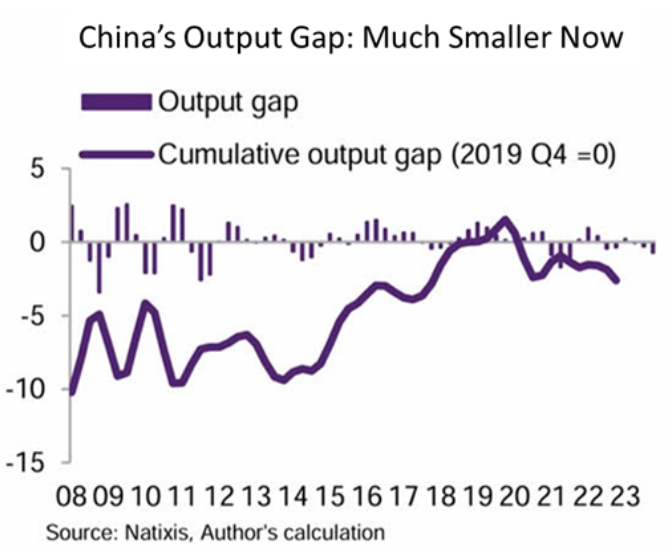

China: Overblown concerns

Manoj Pradhan points out that China’s fiscal support started last September, with stimulus starting before the Trump threat even materialised. Stabilising the property sector is a must for releasing consumption, with the ban on mortgage refinancing and falling house prices being some of the biggest reasons for the country’s ailing consumption. Manoj claims that concerns about China being a source of persistent deflationary demand are overblown, with the structural inflection occurring instead over 2012-15. He points to research estimating that China’s output gap over 2012-15 was nearly four times the size of the output gap in the recent downturn (see chart). China is also set to gain more than the US from de-escalation in the trade war. Stay long CHN.

China: The RMB’s implicit trading range

William Hess points out that under PBoC’s rigid dollar peg the path for USD/CNY has increasingly resembled that for USD/HKD, with upper and lower trading bands. William expects renewed USD weakening, given that the ongoing trade talks are not sufficient for PBoC to abandon its current target range. His team predict that the Bank will likely allow +/- 2% movement in USD/CNY relative to its daily fixing. Elevated trade tensions and external uncertainty will only reinforce PBOC’s commitment to defending this trading band. Moreover, PBoC’s management of moves to USD/CNY within this trading band appears to be asymmetric. The Bank appears to be more stringent with defending the trading band and daily fixing when the RMB is under greater pressure to depreciate. Against this backdrop, William believes the PBoC will continue to confine USD/CNY to the 7.05-7.35 range for the rest of this year while the RMB depreciates against the CFETS currency basket ~10% by year end.

China: Indomitable innovation

Sharmila Whelan has just returned from an intense 2-week visit to China. She observed that the economy has yet to bottom and that the profit cycle downturn is worsening; As of April, 30% of manufacturing companies were loss making, up from 25% in November. Nevertheless, China is back in business and innovation knows no bounds. Geopolitics and Trump’s trade war are re-shaping alliances. For Europe, China has become even more vital to its green transition. The shift in the Chinese government mindset – now clearly more pro-private sector – means that domestic innovation in green technology, AI, advanced manufacturing, biotech (among others) is advancing at a breathtaking pace. As a result, Sharmila is bullish on the sectors mentioned above, while underweight on consumer discretionary, property and export cyclicals.

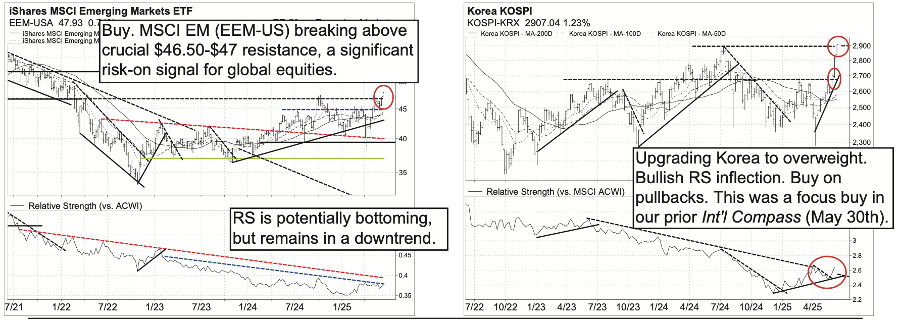

Korea shines amidst EM breakout

MSCI Emerging Markets (EEM-US) is breaking above $46.50-$47 resistance, continuing the bullish short-term trend. The Vermilion Team are buyers on this breakout, with Korea being their top country to buy. The team are upgrading Korea (KOSPI) to overweight; in their latest report, they discussed how the KOSPI was breaking out of a 10-month base (May 30, 2025), highlighting several large-cap financials and other stocks to buy. The KOSPI has exploded higher since and is now reversing its 2-year RS downtrend. Buy any pullbacks.

Nigeria maintains the stabilisation trade

The NGN rate has remained unified with the black market rate and the central bank has kept rates high, now positive in real terms. The combination of FX weakness and financial tightening is not great for domestic demand, but it has put the external balance back in surplus and is a positive signal for transparency and for export investment. On the other hand, Jonathan Anderson is still waiting for evidence of sustained fiscal improvement, which keeps money growth and inflation pressures strong. Fiscal, money and inflation concerns make him ambivalent about owning local fixed income or equities. By contrast, he continues to see value in hard currency debt and maintains his dollar sovereign position.

Commodities

Ferrous scrap: Bulk benchmarks re-priced down

Turkish HMS 1&2 (80:20) slipped back US$3-4/t over the past week to US$339-340/t CFR Turkiye (TKY), as heat continued to slowly dissipate out of overinflated ferrous scrap benchmarks. Atilla Widnell believes the deterioration in US-China relations contributed to the reversal in sentiment-driven gains in Shanghai Rebar futures prices over the same period. Unsurprisingly, this deterioration in Shanghai Rebar futures directly resulted in physical Asian-origin Billet export offer prices being revised markedly lower. It was, therefore, unsurprising to hear of fresh physical Chinese-origin Billet offers being re-priced down to US$450-455/t CFR TKY over the same period into Turkiye. Across the pond, US ferrous scrap suppliers are waiting to understand the impacts from President Trump's doubling of US Steel import tariffs. Atilla anticipates local merchants may upwardly revise ferrous scrap prices, but claims that investors will first need to wait and see how recent policy changes impact domestic HRC sales, trickle down to regional ferrous scrap costs, and affect US East Coast purchase prices.

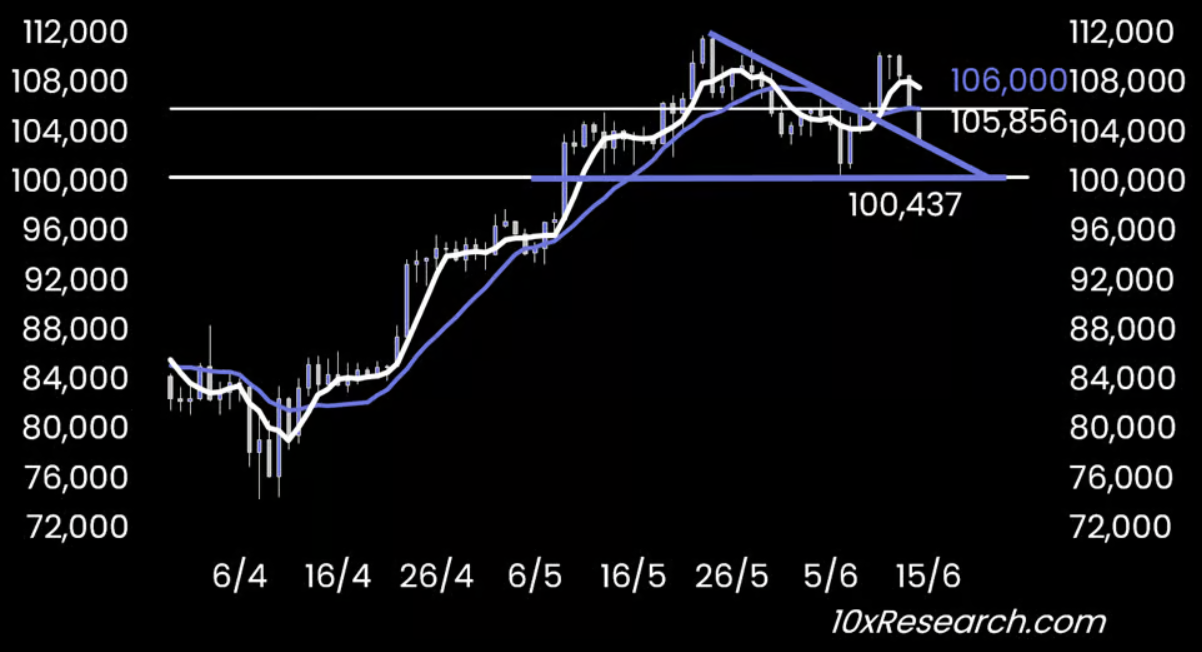

Bitcoin just lost its breakout

The breakout above $106,00 didn’t hold, reinforcing Markus Thielen’s cautious stance. He suspects that the initial hype around the Circle IPO may have temporarily reignited speculative interest, triggering the breakout in both BTC and ETH. However, this Ethereum move lacks strong fundamental backing and appears to be driven mainly by speculative positioning. Bitcoin has minor support around $104,000, with more substantial support near the $100,000–$101,000 zone. A close below these levels could signal a return to a broader summer consolidation phase. The $95,000 to $98,000 range remains a critical support zone for Bitcoin, with several key indicators, including Markus’ preferred 21-week moving average and various on-chain metrics, shifting from bullish to neutral or bearish. A break below this $106,000 level has turned him neutral again, and he prefers to step back and wait for a more favourable setup before re-engaging.

Iran’s potential threat to oil markets

Unsurprisingly, oil prices jumped in the aftermath of Israel’s strikes against Iran. Wolfang Munchau ponders over the reasonable worst-case scenario. One must consider the 3.3m b/d of exports that could be lost, although this will pale in comparison to Russia’s 9-10m b/d before war with Ukraine, not to mention that most of the oil goes to China and is relatively sanctions proof. Should Iranian oil export infrastructure be targeted by Israel, OPEC spare capacity (est. 5.3m b/d) could absorb the damage. However, should Iran try to block the Strait of Hormuz in retaliation, this would potentially severely limit Iraq, Kuwait, Saudi Arabia, and the UAE’s ability to deliver oil to the world market. This would be extremely risky for Iran, with severe diplomatic repercussions with all Gulf states. The US is, so far, keeping its distance from the spat, but directly threatening global oil supplies could change that.

Is the platinum price surge temporary?

In this presentation Jeffrey Christian of CPM Group looks at platinum’s price surge over the past few days from $1,041 at the start of June to as high as $1,232 on June 10th. Jeff discusses the real reasons behind the spike, misunderstood fundamentals, jewelry demand, optimism around auto catalyst demand. He also discusses the large surpluses, not deficits, in new platinum supply, explaining the reasons behind discrepancies in market commentary. He reviews the role of aboveground inventories, and how investor behavior, not fabrication demand, has often driven price spikes in the past. The presentation concludes with a look at gold and silver markets, and why June 9th was a very strange day for the precious metals.

Click here to watch.