Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

Europe

Short ideas deliver 100% hit rate in the first half of 2025

AIR delivered an exceptional 1H25, closing 20 out of 20 European Sell/Short ideas in profit, with an average return of +24.5% per idea. Standout trades included Stellantis (+56%), STMicroelectronics (+55%), Aston Martin (+54%), Remy Cointreau (+53%) and Swatch (+43%). Out of 28 Sell/Short ideas still in force (opened in the last 18 months), 20 are currently making gains. Notable winners include LEM Holding (+51%), B&M (+49%), Alten (+42%) and Mercedes-Benz (+32%). AIR continues to issue an average of 3 high-conviction short ideas per month, making them a must-follow provider for investors seeking consistent alpha from the short side.

Litigation Watch: Top focus names for Q3

MDC follows significant legal disputes to provide clients with actionable investment ideas. Focus List situations that they believe may be among the most actionable during Q3 include Burford Capital, Reckitt Benckiser and Bayer. Burford is a UK based litigation funder that has already been awarded a Judgment totalling $16,099,788,293. Now, the challenge is to collect from the Republic of Argentina! Reckitt along with Abbott Laboratories are facing product liability lawsuits in the US regarding baby formula products causing NEC. The next bellwether trial will be in the Diggs Case scheduled to start on Aug 8th. As if Bayer hasn't faced enough toxic tort litigation regarding its Roundup weed killer product, it now faces potential liability for Polychlorinated Biphenyls. The next PCB Trial is scheduled to commence on Sep 8th.

TEL has announced that it has agreed to buy GlobalConnect's (GC) Consumer Business in Norway. Not that many mature fibre assts have been sold in Europe, and so this deal is interesting on quite a few levels: for those thinking about what FastFiber in Portugal is worth or what Virgin Media might sell a stake in NetCo for, or what price Zegona / MasOrange might achieve in Spain, then this deal has relevance. Indeed, one could even argue that there is a read across for the incumbents themselves, as their fixed businesses will eventually broadly resemble GC. In this report New Street looks at what the deal means for fibre valuations, fibre capex assumptions and for TEL itself.

Tom Beevers of Forensic Alpha pitched ORSTED as a short at our latest Best Equity Short Ideas Conference, arguing that the company’s balance sheet is materially weaker than the market appreciates, with true leverage significantly higher than reported and free cash flow overstated. The stock scores a maximum 10/10 risk rating on Forensic Alpha’s platform, which leverages proprietary machine intelligence to detect red flags buried within financial statements and governance disclosures, across 35 risk categories. Click here to listen to Tom's presentation and here to access the slides.

North America

Rare buy signal confirms market strength and new cycle phase

ViewRight’s Defender Program, a rules-based framework developed by a century of market cycle analysis, has issued a rare secondary confirmation buy signal, marking the first such occurrence in its 40-year history. Triggered by a new all-time high in the NYSE Common Stocks Advance-Decline Line, this confirms a return to broad market strength and shifts Defender’s regime from 33% to 100% equity exposure. Defender has historically reduced bear market drawdowns by ~60% and delivered 5x the S&P 500’s returns with 30% less volatility since 1988. Notably, no bear market has ever begun with both NYSE All-Issues and NYSE Common Stocks Advance-Decline Lines at new highs - making the July 2nd signal a powerful disqualifier of longer-term downside risk. Defender now reclassifies the market phase as "Summer", a regime aligned with strong forward returns and broad participation.

Joe Cornell offers a detailed analysis of WBD’s planned spin-off of its Streaming & Studios segments. The move mirrors a broader media trend to separate faster-growing streaming assets from legacy cable operations. The split enhances strategic flexibility - Streaming & Studios could become a more attractive M&A target, while Linear Networks might be paired with a similar business. Joe’s SOTP valuation yields a consolidated target price of $15.00 per share (adjusting for a ~20.0% stake in the Streaming & Studios businesses) for WBD, which implies a potential upside of ~30% from the current market price.

Once a top post-Covid long idea, EXPE has ceded leadership to peers and the broader travel industry. Hedgeye believes the bull thesis - centred on margin expansion, mix shift and market share stability - has grown stale and is now reversing. Investors are 1) underestimating the magnitude of near term deceleration in the core B2C platform, 2) underestimating EXPE’s exposure to regional demand issues and incremental competition, 3) overestimating EXPE’s ability to leverage marketing and drive higher margins, and 4) significantly overestimating EXPE’s ability to maintain (or even grow) share of the total accommodation market in the coming years. While the stock screens as cheap, the risk/reward still skews negative, especially compared to Booking, their preferred long in Online Travel. Hedgeye's EXPE target price offers ~30% downside.

Sidoti sees GEF’s sale of its containerboard operations for $1.8bn as a defining moment in the company’s ongoing shift towards a more focused, higher-margin portfolio. A greater share of earnings will now come from Customized Polymer Solutions, which continues to expand and has stronger structural economics. Pro-forma leverage will fall below 2.0x by Sep, even without selling its Soterra land unit. GEF also raised FY25 FCF guidance for the second consecutive quarter, now targeting at least $280m, with Sidoti modelling $310m based on strong execution and continued cost optimisation. EPS estimates of $4.25 (FY25) and $5.35 (FY26) remain unchanged, but Sidoti believes further upside exists, especially with potential acquisitions. TP $93 (35% upside).

The secular bull market for Banks gets a midyear tailwind

US bank stocks can continue to hit new highs and assume a leadership role in the market, according to Charles Peabody. Fundamentals are excellent, balance sheets are strong and capital is abundant. Meanwhile, the next 12-18 months will likely include a reduction in capital requirements as part of the deregulation process. Reducing the CET1 ratio by 1% can add double digit earnings growth to banks either through buybacks or growing earning assets. Deregulation can also reduce expenses by 1-3% annually. While this process is in place, investors have become accustomed to one way headaches from regulators, and thus, deregulation is only reflected in stock prices after it happens. Charles' top picks are Citigroup, M&T Bank and Citizens Financial.

US Healthcare: What's next from DC

With President Trump signing the OBBB into law, Washington will now turn to other regulatory priorities and states will begin work on implementing the Medicaid reforms. Aldis Institutional's policy-focused events provide investors with timely and actionable insights into the DC landscape. This differentiated platform combines small group conversations with key stakeholders and policymakers, with real-time market commentary from Aldis' senior team. Recent and upcoming event topics include the change to the ACA exchanges and impacts on insurers (Centene, Molina Healthcare), Medicaid reform implementation - including work requirements and provider tax changes, and the outlook for home health and DME/CGMs after CMS's recent proposed rule.

CAT ranks among Two Rivers’ top short ideas within its Declining Business Model framework. Despite deteriorating fundamentals, the stock trades at historically high multiples - over 20x 2025 earnings. Sales have declined for multiple quarters (-9.8% in Q1), estimate revisions remain deeply negative and margins are rolling over from peak levels. Working capital is rising. Finished goods are slowing. Forecasts project cash balances to dwindle on large maturity payments leaving the company with a negative cash position without refinancings. At the last earnings release, CAT missed on the sales, EBITDA and earnings lines.

HBM stands out among copper producers due to its unique gold leverage, sector-leading cost structure and exceptional growth profile. Its high gold by-product production substantially lowers copper cash costs, making it the lowest-cost copper producer in Veritas’ coverage last year as well as 1Q25. The company is also at a profitability inflection point, with Veritas forecasting 2025 EPS to be over 3x higher than in 2024 and HBM’s growth pipeline among the best in the sector, led by its flagship Copper World project in the US, a low-capex, high-IRR development that could expand the group’s copper output by 50%. And this is before Trump's announcement that he intends to impose a 50% tariff on copper imports!

Channel Chatter: Regional Security VAR, ESX Conference, BEAD

SPR’s recent channel conversations highlight growing traction for emerging vendors like Onum and Cribl, which optimise SIEM data flow and reduce Splunk renewal costs. CrowdStrike remains a standout with strong SIEM growth and aggressive sales execution, though channel favouritism limits broader access. Cloudflare, despite a strong product, struggles with channel inefficiencies, while Fortinet is gaining share in select regions but not winning new logos with Lacework. Cisco’s security momentum may be challenged by the departure of Gary Steele. Meanwhile, BEAD funding delays and policy shifts are hurting traditional fibre and “turf” vendors, as fixed wireless and satellite gain favour. At ESX, Napco remains a solid player, but growth has normalised post-3G sunset.

Craig Huber initiates coverage on FICO with an Overweight rating and a 12-month TP of $2,100, highlighting the company’s dominant position in credit scoring, pricing power, high-margin Scores segment (88.5% EBITDA margin) and the early innings of the company’s software strategy, providing a significant opportunity for long-term growth. While the FHFA’s move to allow VantageScore for conforming mortgages has weighed heavily on the stock in recent days, Craig believes the reaction has been excessive. He expects minimal volume loss (~10%) offset by continued price hikes and sees little incentive for lenders to switch. With mortgage volumes 50% below historic norms and rates likely to fall, a refinancing wave in 2026 could be a major tailwind. He recommends using the pullback as a buying opportunity.

At MYST’s recent TMT event, one of the most interesting bearish theses centred on HUBS, described as the “poster child” for structural disruption from AI. The presenter highlighted two major LLM-related themes: 1) AI’s impact on Search Engine Optimisation; and 2) the emergence of AI coding assistants like Cursor and Replit. HUBS’ dominance in customer acquisition via Google Search is unravelling, with organic traffic plunging ~80% from its 2022 peak. This erosion is doubly damaging as HUBS’ Marketing Hub (~40% of revenue) also loses relevance. A deteriorating leadership structure, slowing revenue growth and stretched valuation (48x FY25 FCF) further reinforce the bearish case.

ORCL is entering a new phase of AI-driven growth, with a forecast 20-27% EPS CAGR through 2029. Abacus believes the company's success in cloud infrastructure (OCI) is now well-established, underpinned by accelerating demand and supportive long-term bookings. AI is driving a data layer investment cycle, boosting demand for modern databases - an area where ORCL is gaining share. A major potential upside comes from the $30bn Stargate contract, which Abacus forecasts will add ~$3.59 to EPS from 2028, leading to their FY29 estimate of ~$15.50 and supporting their TP of $400 (+70%). Despite some recent multiple expansion, they argue the full earnings potential is not yet priced in.

Emerging Markets

A decade of EM outperformance

Does a country’s broad equity market play an outsized role in driving the returns of individual stocks? For successful EM money managers, the answer is yes. And their advice is: if you are selecting stocks in the EM universe, you must verify whether the underlying equity market is broadly supportive. That is where Crystal Shore comes in. Every week, they rate 40 Emerging (and Frontier) equity markets on a Low Risk/High Risk, Buy/Sell basis - a framework they have refined over a decade. During which time their market scores have delivered a +58% total return vs. the +19.9% total return of the underlying Emerging Markets. It is a clear recipe for generating alpha: Successful Market Selection + Successful Stock Selection = Strong Outperformance.

Stablecoin adoption presents a unique long-term opportunity for BABA. As the US moves to legitimise stablecoins for global transactions and reserves, China must adapt, albeit cautiously. Hong Kong is emerging as a testbed, with Ant Financial well-positioned to play a strategic role. China’s strength in cross-border trade and BABA’s ~29% share in export e-commerce puts the company at the forefront of this transformation. While stablecoins are unlikely to replace domestic payments, they are poised to reshape international transactions and financial influence. BABA’s regulatory track record, global reach and fintech infrastructure give it an edge over peers like PDD, TikTok Shop and Shein. Blue Lotus maintains BABA as a Top Buy, while Futu is also highlighted as a likely long-term winner in the web3.0 world.

China Pharma’s strategic pivot and global impact

David Scott argues US efforts to lower drug prices are unintentionally accelerating the rise of Chinese pharmaceutical firms. Rather than exporting drugs, Chinese companies are licensing them to US firms and avoiding tariffs. This shift reflects a deeper evolution: China Pharma is moving from capital-intensive manufacturing to IP-driven innovation, as rising R&D-to-sales ratios confirm. Meanwhile, incumbents like Eli Lilly and Novo Nordisk face over-earning backlash, political scrutiny and disruptive competition. AI is also accelerating China’s lead times on drug development, especially in areas like obesity. David highlights Jiangsu Hengrui, 3SBio, Hansoh and Innovent as part of this structural shift. While many US investors tell him that they “can’t buy China”, he warns they can’t afford to ignore it, given the bearish implications for Western pharma incumbents.

Ranking the winners and losers in Global Payments

Victor Galliano introduces a proprietary payments scorecard, ranking companies based on weighted metrics including valuation, margins, EBITDA growth and valuation-to-growth. PagSeguro and Nexi remain top picks due to deep value characteristics and strong scorecard rankings. PayPal is upgraded to Buy, replacing Visa, supported by improved margins, stabilising net take rate and attractive valuation. Affirm is upgraded to Neutral, while KakaoPay is newly rated Sell. The stock has surged on stablecoin speculation, but Victor warns of underestimated regulatory risks, especially following Bank of Korea’s recent caution on digital assets.

Macro Research

Developed Markets

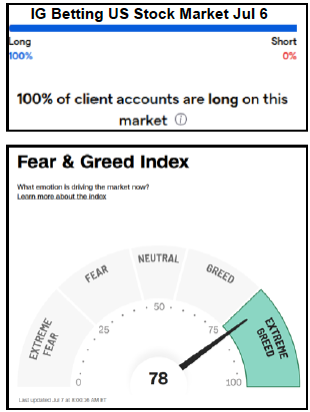

What happens when retail investors wake up?

The April-July rally was driven by the perception that the tariff war was over. Since then, retail investors have flooded the stock market with reckless inflows, remarks Michael Belkin. The IG stock market betting site registered 100% of investors being long this past weekend, which he has never seen before. Tariff rates have further to go, and this will be incredibly bearish for the stock market. Corporate insiders (like NVIDIA) are already selling shares, unloading into the unsuspecting hands of retail and institutional investors. Michael says it is clear that we are in a bubble, but many refuse to see it. Defensive sectors have a coiled spring forecast and a long-term model outperform forecast, but Michael’s top picks are gold and energy stocks, including Newmont and Barrick.

An insight into the world of hedge funds

Alternative Fund Insight is an intelligence platform providing leading insights into launch news, manager rankings, allocator intelligence, operational insights and other content focused on the industry itself. In one of their latest reports, they look into the trends and opportunities driving Q1 activity in 2025. The report examines the delays sparked by market volatility before the May/June rebound, the proliferation of SMA use in the start-up sector, and the two firms set for $1bn raises in 2025 (vs five in 2024). The multi-strategy segment of the hedge fund market is also on course to soon overtake long/short equity, reflecting the changing nature of the industry. Please contact us to find out more.

Missing the central banks of old

Wolfgang Münchau used to be a strong supporter of independent central banking, but that was during a time when central banks were focused on a narrow target – price stability in Europe, with the addition of stable employment in the US. Nowadays, we are seeing central bank mission creep. External shocks, such as climate change and wars, disrupt supply chains and can have a lasting impact on price levels, but Wolfgang struggles to see how either of them can have a lasting impact on inflation dynamics. There is broad agreement that the cause of inflation is a monetary phenomenon. It is not the job of a central bank to make money available to finance wars, or climate policies; that is the job of politicians. Wolfgang points out that the biggest shock to our economy this century were not climate change or wars, but central bank policies like QE that created more inequality than any fiscal policy in history.

US: An emboldened bull, dancing on the edge

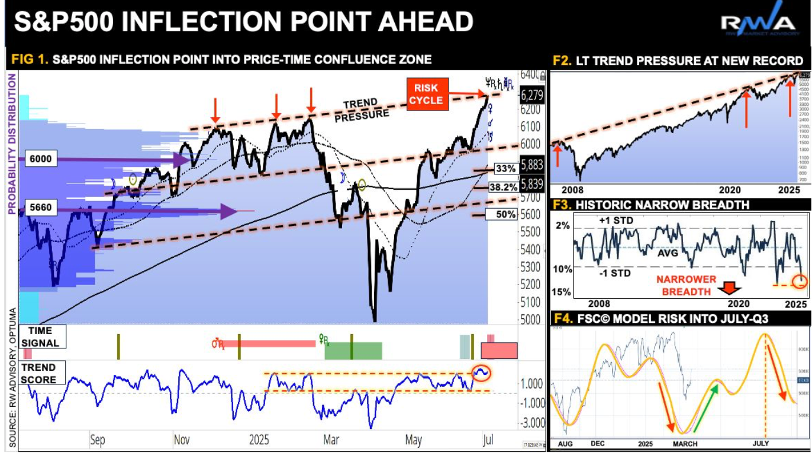

Despite US equities reaching record highs, surface strength masks underlying fragility. The market is pressured by a revival of triple whammy headwinds: momentum exhaustion, inter-market divergences, and macro-cycle pressures. Rising tail risks—such as escalating geopolitical tensions (e.g., a fragile Iran-Israel ceasefire) and potential US trade policy shifts (including 70% tariffs)—threaten to disrupt momentum and increase volatility. RW Advisory warns that timing models and liquidity indicators suggest a possible Q3 inflection point. Investors are urged to prepare by rebalancing toward higher-quality assets, increasing cash allocations, and utilizing tactical hedges. Defensive positioning now may help mitigate potential turbulence expected later in the year.

The demise of the USD?

Coupled with the passage of the Trump administration’s Big Beautiful Bill and fears of significant increases in US federal debt has been discussion of the end of US dollar dominance of the global financial system. Although AASE cannot look out many years in advance, Peter Stellios notes that they can at least assess the near-term prospects for the momentum of the USD, allowing him to comment on whether – in the short term – this decline is likely to continue. In this week’s Macro, Peter examines the key driver of movements in exchange rates – relative movements in excess money growth across countries – and he draws some conclusions in relation to individual currency pairs as well as DXY as an index. He concludes that the USD could benefit from a strengthening in momentum against the Yen and the Euro. In contrast, the excess money supply differential continues to provide support for the momentum of the Pound, Canadian dollar and Swedish Krona.

It’s hard to bet against the US

If you agree with James Aitken that the full-expensing provisions of the OBBBA will have a positive impact later this year, then you should probably also believe that expected 2026 US growth should be higher. It is hard to bet against US credit markets in general, let alone US equities in general if you think there’s upside risks to consensus forecasts. Hold the course. One estimate suggests the impact of the full-expensing provisions in OBBBA is to reduce the effective corporate tax rate from ~21% to ~12%; it is difficult to forecast an earnings recession when effective corporate tax rates are declining – but what it may mean for investors is that as the bull market rumbles on, they should own more of the direct beneficiaries of an accelerated manufacturing capex boom. More commodities and commodity business at still reasonable prices, less financial businesses at unreasonable prices.

US: America Party

Elon Musk has announced plans for the creation of the America Party. Brunello Rosa notes the Party, if it ever comes to fruition, would aim at breaking the system that has dominated US politics for centuries. A Musk-backed party would likely echo his commitment to technological advancement, placing innovation, scientific progress, space exploration and fiscal responsibility front and centre. Advocating for free speech and fewer regulatory constraints, such a party might attract entrepreneurs, technophiles, younger voters, and those disillusioned with traditional politics. As Musk is not American-born, he cannot run for President. Musk has said his party will aim at winning a handful of seats in the Senate and House, which could make the difference in key votes. The Party may split the right-wing electorate, potentially facilitating the victory of Democratic candidates.

Australia/New Zealand: Currency down under

The RBNZ kept rates unchanged, as did the RBA the day before, but in the opinion of Andreas Steno, there is a much clearer easing bias in the New Zealand communication compared to their neighbours. This quote is taken from the official release overnight: “Subject to medium-term inflation pressures continuing to ease in line with the Committee’s central projections, the Committee expects to lower the Official Cash Rate further, broadly consistent with the projection outlined in May.” To Andreas, this constitutes a clearer forward easing signal than what was heard from the RBA. Yet, markets remain convinced the RBA will do significantly more than the RBNZ from here. Andreas remains long AUDNZD based on this divergence and continues to see AUD as underpriced—especially considering developments in the metals space. If 1.09 breaks in AUD/NZD, it could go a lot higher.

Japan: An upcoming Nikkei fall

Four weeks ago, David Woo observed that the Nikkei was setting up for a rapid move after having traded in a tight range. With Iran taken care of and his tax bill passed, Trump has returned his focus to tariffs. David sees Nikkei as being particularly vulnerable, given its dependence on the auto sector. After breaking out rapidly from a range, there is a tendency for prices to reverse sharply as well. He has already seen profit taking in Nikkei above 40,000, which could be a precursor to such a reversal. In this event, David would expect the price to fall below the bottom of the prior range which means a move to about 37,000. He sold the September Yen denominated Nikkei future at 39,780, and will take profit on a move to 37,000 and stop out at 40,800.

Emerging Markets

Asia has not changed its model (yet)

The appreciation of Asia’s currencies appears largely driven by speculative inflows driven by rising liquidity in the DM; debt monetization increased in the G7 and capital flows returned to the region at a time during which Asia’s trade balances were being inflated by tariff forestalling. Andrew Hunt points out that the latter is now unwinding. Despite the large shifts in Asian FX rates, regional terms of trade appear not to have improved since export pricing was weak even in USD terms. Therefore, the boost to real incomes from the stronger FX will have been limited. Meanwhile, Asia’s savers look to have responded to the stronger FX / changed world by investing more overseas. This is not a new phase or even a “Reverse Asian Crisis Scenario”. Instead, the region gained from surging US import growth and strong capital flows, factors that could yet reverse over the coming weeks.

Argentina: Congress in revolt

Marcos Buscaglia points out that the government has chosen to bring inflation down rather than to purchase FX reserves. He sees renewed pressures on the ARS and rising political risks stemming from Congress, which is in revolt. The first signal of the revolt appeared a few weeks ago when the Lower House passed a bill that would increase pensions 7.2% among others. Marcos expects the credit to be under pressure in the near term as the opposition attempts to pass legislation that would increase fiscal spending. Inflation was close to 2% in June in his view and is likely to be somewhat higher in July. Real ex-ante rates are rising due to the reduction of inflation expectations in the front end. Marcos reiterates his view that the ARS will weaken by about 15% from end-June till the elections. In the short term, investors should watch Congress as they consider several initiatives that would weaken the government.

China’s digital yuan: Ain’t no dollar killer

As China drives forward the world-leading digital yuan project, Ed Yardeni dispels the notion that we are seeing a growing challenge to dollar supremacy. True, Trump’s trade war could be dollar negative, but the US economy isn’t having to deal with the Xi era’s glacial pace of economic and financial reform in a nearly $18trn economy. Although BRICS is gunning for a less dollar-centric future, the yuan sees only a 2.2% share of global foreign exchange reserves – the dollar sits on top with 58%. The PBOC also suffers a trust deficit – why would global institutions trust their e-CNY? There are some arguments that a digital yuan would help solve the country’s weak household demand, but Ed disregards the potential of this bringing enough significant change to cover the festering economic problems. At the end of the day, the nature of the digital asset a country chooses matters far less than the resilience of the economy that undergirds it.

Colombia: A shock to the downside

The Pacifico Research team interpret June’s inflation reading with caution. The monthly variation was at the lower end of Bloomberg’s survey forecasts for the second consecutive month. However, the most significant monthly declines were concentrated in volatile components such as perishable food and energy. As a result, the normalization of core inflation is proceeding more slowly than that of headline CPI. While the slowdown in monthly inflation aligns with seasonal patterns, this was the lowest June figure since 2021. Of the volatile downward contributions, the most significant was electricity, but this should see a less pronounced decrease in July. Food was also a contributor, as expected, but rent saw a downside surprise. Looking ahead, this result introduces a downward bias for July inflation due to the high weight of effective and imputed rent, which together account for 25% of the CPI basket, while also increasing the degree of uncertainty.

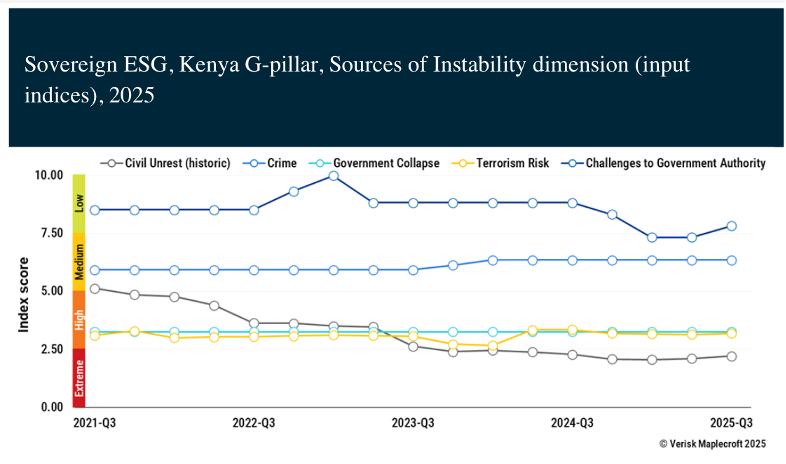

Kenya: At boiling point

The latest violent anti-government protests in Kenya have coincided with an IMF governance diagnostic mission to identify macro-economically critical governance weaknesses and corruption vulnerabilities. Despite some initial consolidation, Kenya remains very far from fiscal and debt stabilisation, and the latest political instability will throw a spanner in the works for a new IMF program. Senior Africa Analyst Mucahid Durmaz notes that, unlike previous demonstrations, the current protests are driven by an amorphous, Gen Z-led movement with no central leadership, complicating government efforts to negotiate. Even if President Ruto resigns, which Durmaz sees as unlikely, this will hinder efforts to put together a coherent political transition. The run-up to the 2027 election looks set to be fraught.

No reason to leave Mongolia

The macroeconomic environment in Mongolia has deteriorated slightly compared to a year ago on the back of softer commodity prices, affecting the external accounts and the budget. However, the tugrik is fairly stable and sovereign dollar spreads remain narrow - and with ongoing investment in export capacity and growing underlying export volumes, Jonathan Anderson continues to expect further macro gains ahead. The source of downside risk, of course, is China, as the current property market shakeout raises the potential for macro volatility in Mongolia's main (indeed, virtually sole) export market. But on balance, Jonathan believes that property woes will have only limited impact on mainland demand for Mongolian coal and copper, just like in the last few years. As a result, he stays invested in Mongolian equities and dollar credit on the back of medium-term structural growth prospects.

South Africa: A structural erosion of capital formation

Peter Montalto comments on the nation’s ailing investment profile as real gross fixed capital formation falls to 14.2%, its lowest level in 20+ years. Investment in machinery may have recovered slightly but spending on critical areas such as R&D and transport have continued to contract. Even in areas where investment has risen, meaningful productivity gains have failed to materialise. Peter remarks that if capital formation is to become a true driver of growth, public infrastructure investment must be stabilised, better targeted and efficiently delivered. Public–private partnerships offer some promise, but remain small in scale and require much greater institutional support. Without urgent reforms, as Operation Vulindela is trying to deliver, South Africa risks locking in a low-growth path defined by decaying infrastructure, weak or sporadic total TFP growth and chronic underinvestment in the very assets that drive growth.

ESG

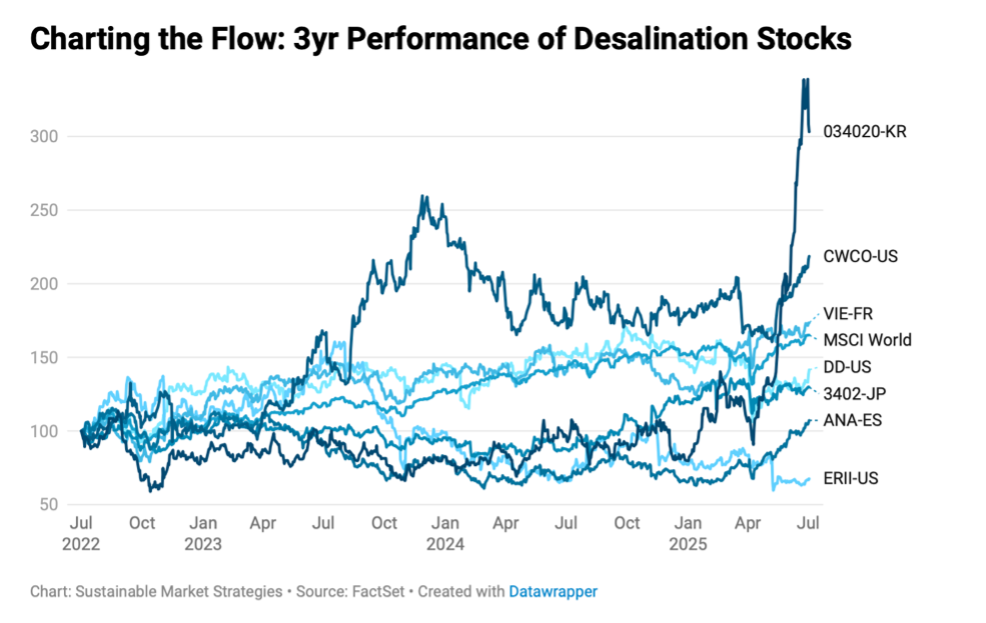

The investment case for desalination

Just as global energy demand is set to soar, a profound but often overlooked surge in water demand is looming. Driven by the immense cooling needs of AI-powered data centres, the water intensity of a growing population, and other demands, humanity will see an unprecedented strain on already dwindling resources. Understanding and mitigating this nexus will be essential for protecting portfolios and ensuring sustainable returns. Desalination costs have plummeted in recent decades, and investors should start tracking companies driving this transformation ahead of the inevitable surge in projects in the coming years. A balanced, high-conviction trio would include Energy Recovery, Acciona and Consolidated Water – each representing a distinct point along the value chain.

Commodities

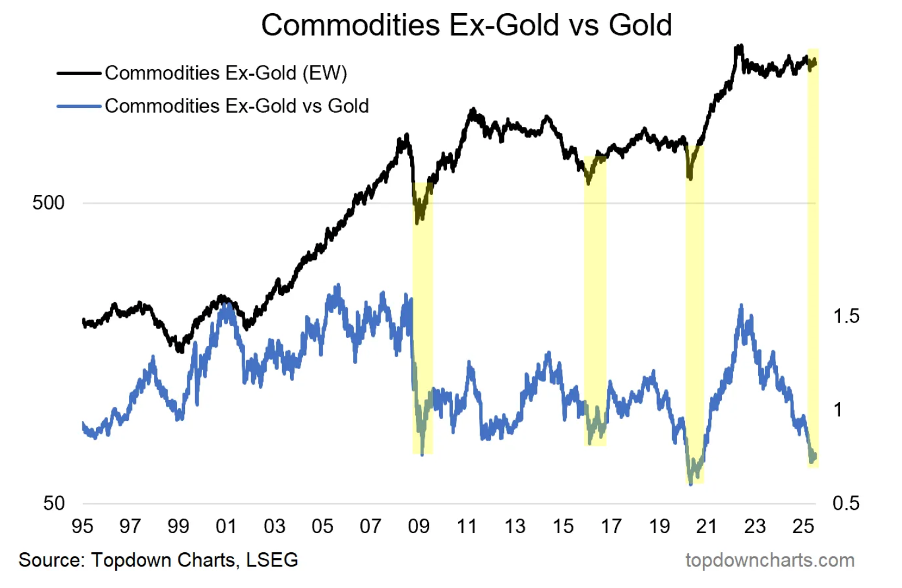

The great rotation nobody is talking about

Something is going on in commodities that only comes once every few years, an event that Callum Thomas says will bring big money to select investors. In this case, he’s talking about the commodity-to-gold ratio; whenever it plunges to an extreme low then turns upward, it flags the start of a new and substantial cyclical bull market in commodities. There are several key forces driving the change: capex, global economic upturn, easier financial conditions, and growing risk-on signs. Some of the key drivers fuelling gold demand are set to fade, too. The time has come for the rest of commodities to take the baton from gold.

Super Copper

Craig Ferguson points out that US tariffs uncertainty remains with 50% tariffs on copper imports spiking the metal to new all-time highs. He expects a supply deficit from next year, one that will last for years as electrification and the transition to renewables unfolds. Countries like the US will now build copper strategic reserves, so Craig would not fade this price spike. This may be the start of a major run higher in the commodity and inflation cycle with copper (and gold, uranium and platinum) already leading the way. This may suggest a new super cycle in commodities has begun. This would suggest a super cycle in big ASX miners and the AUD also has begun (be OW both). However, it also is inflationary and would complicate things for global central banks, bond yields and stock markets. Craig is surprised that both BHP and the AUD are not higher as both should be on this news.

Copper and aluminium remain strong, but ferrous weakness will continue

Despite ongoing US macro policy uncertainty. LME copper prices have exceeded $10k and aluminium prices have recovered well. Even after their recent outperformance, Ian Roper sees the two metals as his favourite for H2, with upside price risk from any potential disruption to US scrap exports as part of the Section 232 copper findings, and the current lobbying for restrictions on aluminium scrap exports. Meanwhile, the increasingly structural risks to Guinea bauxite supply remain and will become more discernible ahead of the country’s December elections. Elsewhere the ferrous space looks increasingly challenge given demand has been front-loaded in China this year, and Ian sees iron ore as having the most downside potential. Recovery for new energy metals still remains far off.

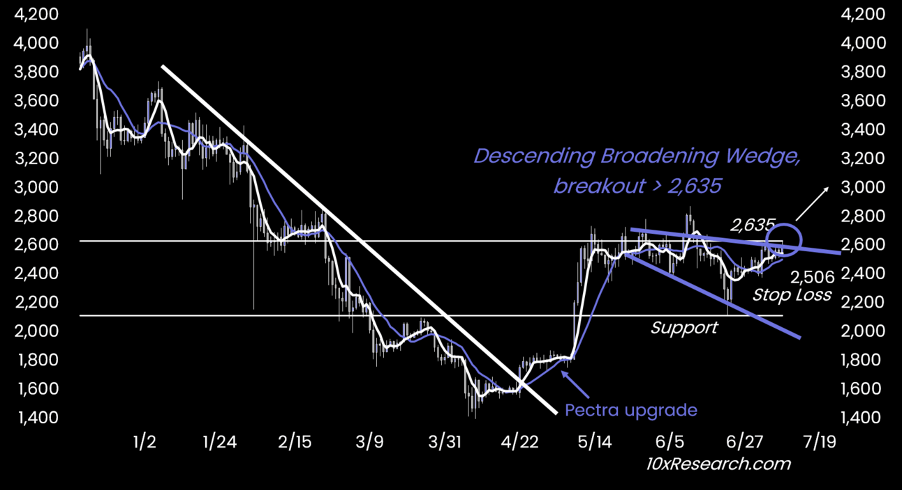

Ethereum: Potential breakout?

Markus Thielen points out that Ethereum continues to consolidate with a slight upward bias, increasing the probability of a breakout. The price has been confined to a narrow $2,400–$2,700 range, with tightening Bollinger Bands and bullish reversal indicators pointing to a potentially imminent move. A break above $2,635 would confirm a bullish descending broadening wedge pattern (see chart), while 2,506/2,512 offer support (stop loss for long positions). The trend model is nearing a bullish reversal, suggesting that the recent pullback may have merely been a pause in the broader uptrend. Weekly momentum has improved, but Ethereum must stay above $2,500, with $2,414 as the critical bull/bear threshold. Despite mixed monthly signals and a complex 12-month formation, Markus says the technical factors are aligning for a potential breakout.