Europe

Top large cap picks for 2H25

Following a strong H1, AIR remains focused on companies that can continue gaining market share through exceptional management, innovation and cost discipline - all driving rising operating margins and FCF, even in challenging environments. The following names pass all 45 of AIR’s proprietary filters (3 layers of 15 valuation and quality criteria) and are expected to significantly outperform over the next 12 months: 1) Adidas - ranked No.1 in AIR’s quantitative system, with accelerating EBIT, margin gains and surging FCF. 2) Aena - best-in-class margins, strong traffic growth and a robust balance sheet. 3) Prysmian - a key player in energy transition and digital infrastructure with a record €40.3bn order book. AIR rates all three stocks as Strong Buys, with 50-100% upside potential.

Fabricio Bloisi, CEO of Prosus since Aug 24, has purchased €20m of stock at €48.29, increasing his stake by ~325%. This is his second purchase since joining, following a €4m purchase at €31.71 last year. Notably, this latest investment is 5x larger and made at a 50% higher price - underscoring growing conviction in the company’s outlook. Meanwhile, three Nordea Bank directors bought a combined €189k of stock at ~€12.20 post-earnings. Jonas Synnegren (Non-Exec since May 20) made his first buy since joining (€104k), Petra Van Hoeken (Non-Exec since Mar 19) made her largest buy to date (€35k) and Lars Rohde (Non-Exec since Mar 24) bought €50k of stock in his first purchase. Smart Insider assigns both stocks a +1 rating (highest conviction).

Telcos: More selective stock picking required

Communications

European telecom stocks have outperformed YTD, adding to 2024’s gains and validating New Street’s long-term thesis of regulatory improvement. However, with sector upside narrowing to 17% (vs. 31% at the start of the year), returns are likely to become more stock-specific and increasingly dependent on M&A. They highlight French names and Telecom Italia as most geared to deal-making. New Street’s top picks are BT (strong FCF growth); DT (German and US upside); Bouygues (undervalued FCF growth and M&A upside); and Vodafone (special sit. with value to be unlocked). They also recently upgraded Telia to Buy seeing good cost control and the possibility for extraordinary cash returns.

Communications

Doug Arthur comments on UK media reports suggesting Accenture and WPP have held preliminary talks about a potential transaction. The timing aligns with WPP’s appointment of Baiju Shah - Accenture Song’s former Chief Strategy Officer - to lead its struggling digital agency, AKQA. While ACN has rapidly built the world’s largest digital marketing platform (pre the planned merger of Omnicom and Interpublic), WPP remains challenged, with its stock near 20-year lows, FCF yield close to 16% and a 4x EBITDA multiple. Doug acknowledges the scepticism around a deal, but a buy-low strategy on WPP would quickly catapult ACN atop a consolidating industry. Stranger things have happened.

Technology

NOKIA is undergoing a major transformation under new CEO Justin Hotard, who brings a Silicon Valley mindset to this legacy European company. The recent Infinera acquisition signals a strategic pivot from legacy RAN to high-growth hyperscale data centre infrastructure. The RAN business appears to have bottomed after a multi-year downturn, with pricing power set to improve amid the first hardware upcycle in a decade and increasing replacement of Huawei equipment in Western markets. NOKIA also benefits from stable IP licensing cash flows, expansion into new areas (Amazon streaming) and renewed momentum in networking. Despite a strong balance sheet, ~3.5% dividend yield and a clear path to margin expansion, the shares trade at just ~12x FY26 EPS. With potential EPS power of $0.70, the stock could “easily” double with minimal downside.

North America

Consumer Discretionary

Paragon Intel is launching a bespoke CEO assessment project on FLUT’s Jeremy Jackson and DKNG’s Jason Robins. While both leaders boast headline achievements, they now confront converging pressures - higher state betting taxes, rising CAC, regulatory scrutiny and complex integrations. With Robins shifting focus towards FCF generation and Jackson tasked with defending FanDuel’s margin edge amid intensifying competition, Paragon will evaluate whether each CEO possesses the capital-allocation discipline, governance model and operating rigour to convert scale into durable profitability. They will also explore how differences in ownership control impact succession, strategic agility and shareholder alignment as the US sports betting market matures.

Consumer Discretionary

Chuck Grom upgrades WSM to Buy, forecasting a Q2 sales rebound (+3% SSS) that could mark the start of a multi-year furniture industry recovery. Pent-up demand (particularly among higher-income consumers), easing macro headwinds (tariffs, remodelling slowdown, etc.) and increase in the SALT cap, are all expected to benefit WSM. The company’s strategic move away from heavy promotional activity over the past two years also gives WSM more pricing power in a sector that is likely to see price augmentation. Emerging brands and a growing B2B channel offer longer-term growth optionality. Chuck raises his FY25 and FY26 EPS estimates to $8.75 and $9.40, both above consensus.

Financials

EWBC is a US-based commercial bank headquartered in California, operating across 110 locations in the US and Asia. With a strong focus on serving the Asian American community, the bank has demonstrated consistent growth, expanding its deposit base at a 13% CAGR over the past 20 years. Its loan portfolio reflects a disciplined approach, with 68% comprising commercial and residential mortgages - averaging a LTV ratio of 50% - and the remaining 32% in commercial lending. Given the strong cultural ties to their customer base and their conservative leveraging, Ben Jones believes the business is well placed to grow without significant threat to its equity.

Strong 2025 short performance, consistent long-term hit rate

Healthcare

Bios Research has published 7 short ideas this year, with 5 generating absolute returns. This builds on a strong trailing 12-month run with 13 of 18 short calls delivering positive returns. Positions closed in recent months include Bio-Techne (-22%) and Butterfly Network (-43%), Repligen (-26%) and Twist Bioscience (-25%). Since inception in 2012, Bios has published 183 short ideas with a 69% hit rate and 42% producing >25% returns. Focus areas include medtech, commercial biotech, services/tools and potential frauds. Bios currently has 13 active short positions and will soon launch a new $10bn+ biotech short which Aaron Fletcher believes has up to 80% downside before the end of 2025.

Industrials

GXO has significantly outperformed the S&P 500 since its April lows, but Boyar believes the rally is still in its early innings. As the world’s largest pure-play contract logistics provider, GXO is poised to benefit from powerful secular trends - including rising supply chain complexity, increased outsourcing and growing demand for warehouse automation. Boyar highlights GXO’s high-quality earnings, strong FCF and sticky customer base, which support durable growth and pricing power. With further margin expansion and operational efficiencies on the horizon, they see meaningful upside from here. Boyar’s intrinsic value estimate implies ~70% upside, based on a conservative 13x EV/EBITDA multiple.

Aviation Weekly: Tactical insights & trading opportunities

Industrials

Reno Bianchi offers incisive commentary on key developments across the aviation sector. Highlights from his report this week include Delta’s strategic push towards AI-driven pricing, persistent capacity constraints from Pratt & Whitney engine issues and the latest fallout from the EU-US aerospace tariff standoff. In credit, short-dated EETCs like UAL B 4.6% due 2026 imply spreads near 1,000bps and offer compelling value if sourced at quoted levels. For AA tranches, Reno recommends 5yr paper with spreads ≥130bps; for A tranches, selected issues offering +200bps or more. He continues to favour Spirit’s 2015-1 B tranche. Term loans and senior secureds remain expensive, with Spirit and JetBlue as notable but risky exceptions. Domestic unsecureds are best avoided on tight spreads. LATAM remains his his preferred international credit, citing low leverage and relative upside.

IT Survey: Robust spend, GenAI boom, staffing cuts

Technology

Rosenblatt’s July survey of 100+ senior IT managers reveals a surprisingly robust IT spending outlook, with two-thirds of budgets being revised higher since the start of 2025, despite macro concerns. GenAI is the top investment priority, with 60% increasing spend and nearly 70% expecting a material organisational impact. Over 75% expect developer staffing cuts of 10%+. Cybersecurity remains a defensive spending priority with investment flowing towards securing modern, distributed environments (Cloud, SASE/SSE) and data itself - benefitting CrowdStrike, CyberArk, Palo Alto, Zscaler and Fortinet. AWS fared much better, ranking first in "cloud service provider best positioned in AI", with 28% (vs. 16% in Dec 24), surpassing Google and Microsoft. Infrastructure names like Snowflake, Rubrik and MongoDB are also well-positioned amid data estate modernisation.

Technology

Despite a solid Q3 beat and raise, MU shares fell on misplaced concerns over HBM oversupply. Arete sees strong FY26 growth, with HBM projected to reach ~40% of DRAM sales by late 2026, reinforcing MU’s status as an essential yet still undervalued AI stock. Nvidia continues to request additional HBM and potential resumption of H20E (with HBM3E-8Hi) sales could act as a catalyst for further global supply tightening. MU must demonstrate HBM4 competitiveness (16-layer stacking capability) within 6-8 months to ease investor concerns. Arete also expects MU to gain eSSD market share at the expense of Samsung and SK Hynix. A combination of stable traditional DRAM pricing and rising HBM mix to drive a 63% Y/Y rise in FY26 EPS to $12.78. TP increased to $150 (35% upside).

Technology

Forensic Alpha has raised PAYX’s risk score to the highest level (10/10), citing a sharply rising trend in DSO as a key flag in the company’s latest 10-K. The increase stems from significant growth in “Purchased Receivables” tied to PAYX’s Funding Solutions business, which provides non-recourse payroll advances to staffing agencies. These receivables rose 23% Y/Y to $1.2bn, now ranking among the largest items on the balance sheet. Given its growth and size, Forensic Alpha was surprised there is only one passing reference to it within the investor presentation and no mention of it on the Q4 earnings call. Changes in cash flow presentation and more optimistic revenue recognition assumptions further raise concerns about transparency and earnings quality.

Technology

At Revelare’s TMT Investor Idea Event, a long thesis on Unity argued the company is entering a turnaround phase after missteps in M&A, leadership and pricing strategy. With both Create and Grow segments rebounding, 2025 is expected to be a reacceleration year. The launch of Vector, Unity’s new AI ad platform, could restore momentum in Grow, while Unity 6 is showing early traction in Create. EBITDA in 2026 could be $600m+ vs. the Street at $440m. Revelare also hosted a separate discussion with a former Unity executive to further explore the company’s strategic reset and execution path. Since these events Unity’s shares have risen ~40% with further upside anticipated.

Utilities

BEP signs a landmark Hydro Framework Agreement with Google, representing the largest-ever corporate hydroelectric power deal. However, Veritas estimates the deal’s initial pricing of $56-76/MWh is below BEP’s current US hydro average of $83/MWh in 2024, contrasting with management’s expectation of ~2-4% annual FFO growth from hydro recontracting. Furthermore, BEP faces significant barriers to scaling beyond the initial 670 MW, including long-term contractual commitments and geographic mismatch between available hydro capacity and Google’s priority markets (PJM & MISO). Despite the market’s positive reaction to the news, Veritas maintains their Sell rating and TP of US$20 (30% downside).

Emerging Markets

Brewing Wars: The latest developments in China's tea market

Consumer Discretionary

The competitive landscape in China's tea beverage industry remains dynamic, with signs of easing price wars but intensifying brand differentiation. While product offerings across brands are largely similar, investors increasingly focus on differences in supply chain efficiency and, more importantly, operational capabilities - especially in digitalisation and private traffic management. CHAGEE continues to generate polarised views due to its premium pricing and same-store trends. Meanwhile, MIXUE's expansion potential remains a key debate point, with opinions split between saturation concerns and confidence in further growth across lower-tier markets. As product boundaries blur, brands like Luckin Coffee are entering the tea space, raising the question of whether long-term competition will centre around operational strength more than product category.

Financials

AlphaMena remains bullish on CIB, citing Egypt’s ongoing recovery, solid 1H25 results (+21% Y/Y net profit) and strong fundamentals. CIB has rebounded from regional conflict and delivered a +20.4% YTD return (+16.8% in 1 month). The Central Bank’s current wait-and-see approach provides comfort to CIB’s NIM (8.94% in H1), while low funding costs, supported by a robust CASA deposit base, further enhance the bank's profile, particularly should the easing cycle resume. AlphaMena forecasts sustained NII growth, driven by healthy loan expansion and deposit mix strength. Significant sovereign asset exposure is improving asset quality, with the NPL ratio dropping to 2.63%, alongside a high coverage ratio >300%. CIB delivers best-in-class operational efficiency, with a cost-to-income ratio of 13.8%. Positive earnings momentum supports enhanced capital returns.

Materials

WCC has issued a positive profit alert, forecasting 1H25 net profit to rise 80-100% Y/Y. Lucror reiterates a Buy on the WESCHI 4.95% 2026s at 90.5 / 16% YTW / 0.9Y, noting the attractive yield for a short holding period. The bonds have rallied ~10 points since mid-Jun, supported by Xinjiang asset sales, which enable WCC to repay over one-third of the USD 600m notes. A tender offer and new issuance could follow. Further non-core disposals in Guizhou and growth in African operations may improve refinancing flexibility and recovery value. Despite expected negative FCF in H1 due to capex and acquisitions, fundamentals are improving.

Developed Markets

Forecasting 2yr swap rates

DeepMacro’s Short Term Rates-1 (STR-1) model provides forecasts of 2yr swap rates for the G10 countries over the next three months. Jeffrey Young chooses 2yr swap rates because they are an estimate of the market's expectation for monetary policy over the medium term, which he believes is usually a function of economic growth and inflation. It generates receive/pay recommendations based on the difference between model forecasts, and market forward interest rates. The inputs to the model are the DeepMacro growth and inflation factors, including "Big Data", and DeepMacro's automated, machine-driven analysis of central banks. Currently, in the US Jeffrey expects rates to rise but market forwards expect the opposite. For the EUR, Jeffrey is also going against the market, with expectations of rate declines vs market expectations of a rise. In the UK, both agree on rate declines, but Jeffrey sees them falling more than market forwards.

Political investments

Equinor’s huge write down on US wind investments illustrates the kind of stranded asset risks that are growing for investors in the UK energy sector. Mark Bathgate points out that given how hugely politically contentious net zero policies are – and the vocal opposition of UK’s highest polling opposition party – these are likely to receive more focus. Where investments are only viable with long term government subsidy, the stranded asset risks from government changes are substantial- these kind of govt subsidy-dependent investments are increasingly bets on political outcomes.

Europe vs China: The battle for automotive dominance

Wolfgang Münchau points out how China is far ahead of Europe in all the categories that will determine the competitiveness of next generation cars – batteries, rare-earth magnets, AI software, and key components of electric engines. In fact, the country has left the EU behind in virtually all dimensions of 21st century technology, even in clean tech which was previously touted as a valuable opportunity to carve out a niche. Wolfgang says a role as junior partner of China is what the EU should hope for, but the likelihood is that they cut themselves off through non-tariff barriers and protectionist policies. Germany’s economic decline is a failure of the corporate sector to invest in 21st century technologies, and a failure of the government to create an efficient capital market that penalises such situations. They’re not even talking about it.

The trade war is dead, long live the trade war!

Despite all of the dire headlines about the imposition of a 25% tariff rate on Canada and 30% on Mexico and the European Union, Cam Hui says the only trade war that matters is effectively over. China has won. In the short run, economic policy uncertainty is receding but it’s not fully normalized. According to Cam, it’s time to adopt a risk-on posture. US equities lagged most during the trade war panic, and they are recovering and should be the leadership in the short term. In the long run however, Trump’s America First policies of continuing trade wars and efforts to reshore low value-added industries are likely to erode U.S. productivity and competitiveness. The S&P 500 is already trading at a highly elevated forward P/E of 22.2. Cam believes that equity investors should not expect US equities to continue to outperform global stocks in the next expansion cycle.

US: What if courts strike down Trump’s IEEPA tariffs?

It’s an exercise in the unthinkable: what if the Federal Circuit becomes the third federal court to find the IEEPA tariffs unlawful, scuppering Trump’s tariff plans. A September ruling could mean that more than $100bn in tariff revenue will need to be funded if Trump fails to win. Should the courts decide against Trump, James Lucier expects the Federal Circuit to uphold the decision with an authoritative en banc ruling, which will render it much less likely for the Supreme Court to grant a stay and keep the tariffs in place. Global markets will be disrupted at the sudden elimination of tariffs and refunds may take time to sort out. Trump doesn’t have a Plan B, and any claims that he can use authorities such as Sections 122, 232 and 308 fail to recognise the relatively limited authority these provide compared to IEEPA. Trump will no doubt build a protectionist wall but will lack the free hand he hoped to have under IEEPA.

US: Claims about claims

Some investors watch the weekly fluctuations in initial claims for unemployment insurance benefits as if they are the secret to calling the next turn of the labour market or business cycle. Yet, the relationship has only a 0.34 correlation, and Carl Weinberg says attempts to ascertain a greater fit in the data fails. There are three factors that can make the unemployment rate rise or fall: a recession or fears of an impending one. Employees quitting without a new position to go into (which signals confidence in the labour market), and immigration. What we are seeing week-to-week is more noise than signal, and investors should instead pay attention to the monthly JOLTS data.

US: Volatility is embarrassingly underpriced

According to Danielle DiMartino Booth, the biggest disconnect on the Street is no longer between the data and high yield bond spreads, which has become so glaring as to be comical. Junk spreads are nearly a third of the levels that prevailed the last three times expectations for rising unemployment and falling home prices were so high in concert. Heck, not even stock market investors are sufficiently comforted by their paper wealth to report uplifted spirits in gauges of consumer sentiment. Danielle says that recognizing the elephant in the room of living on borrowed time makes volatility look ridiculously cheap here.

Japan: Ishiba drags his feet

PM Ishiba Shigeru denied reports that he will announce his resignation, but the party has made it clear they want a change in leadership. It’s not clear if this denial is a result of stubbornness or a belief that Ishiba can weather the crisis, but he will almost certainly be out of office by September at the latest. Despite lacking factions as a disciplining mechanism, party elders will try and consolidate the field in the coming weeks to avoid an overly chaotic and divisive election. They will attempt to coalesce around a single candidate, either Takaichi or Kobayashi, moving away from the more ‘liberal’ candidates that they feel have harmed their electoral chances. Meanwhile, among the party’s reformist wing, Koizumi is the most likely champion.

Emerging Markets

EM Alpha

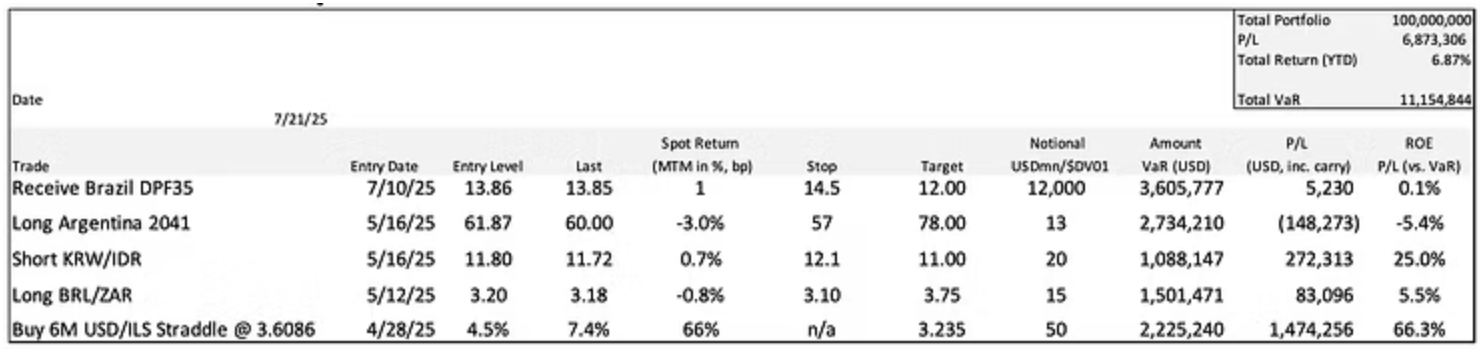

David Woo’s EM Fixed Income Alpha Portfolio is up 6.87% in 2025, 117bp in carry. He has added to the Brazilian rates position at 14% and is looking add more between 14% and 14.25%; he will stop at 14.5%. For long BRL/ZAR his position is up despite a 0.8% drop in spot due to the positive carry, and he is planning to add to this exposure around 3.15. David discusses the counterintuitively optimistic news flowing from South Africa, which he expects to deteriorate in the coming weeks despite the decision to dismiss Minister Nobuhle Nkabane. David also notes the lower-than-expected inflation data from Argentina, which he takes advantage of by adding to his exposure in the 2041 bond, just ahead of the Moody’s upgrade announcement.

Brazil inches towards settling down

Real growth has held up well, but Jonathan Anderson points at general signs of weakening in underlying activity data. Inflation numbers have peaked across the board and should be fading in the second half. And fiscal consolidation has been very visible on an annual basis. In this environment, both real rates and the rates/growth gap remain extraordinarily high - keeping BRL carry attractive and making eventual rate cuts the dominant theme of the coming 12 months. There are two trends to watch that could potentially impede the carry/easing trades: one is widening external deficits, and the other is apparent recent budgetary slippage. Stay tuned.

China: Losing momentum

China’s economy witnessed some respite from its long-standing weakness on the back of stronger exports and a very modest easing of fiscal policy during H1/2025. There was also some debt monetization by commercial banks that helped lift macro liquidity. In practice, funding difficulties plague the banking system and private sector credit trends remain soft. The public’s evident lack of trust in the banks as a safe repository for their savings is constraining the authorities vis-à-vis their rate-setting and QE-like policy responses – it would be dangerous to create more deposits or cut rates aggressively. Financial instability (inflation) could easily result if policy became too expansionary and people “dumped” cash, which Andrew Hunt points out is unfortunately a well-worn EM path. The ongoing credit crunch is sapping domestic growth and fostering a deflationary environment. Andrew expects the economy to now slow as global trade trends weaken, something that could weigh on equities and the CNY.

China: Exciting opportunity in the SSE

The Shanghai Composite’s (3,534) monthly chart features two major chart patterns: a 17.5-year+ symmetrical triangle and a 9.5-year rectangle. Chris Roberts’ main focus is on the 9.5-year rectangle, the resistance zone at 3,450-3,685 is once again being tested. Other advances have failed in the zone, or after minor moves above the zone. A confirmed breakout from the 9-year rectangle would be viewed as an exciting buying opportunity, leading to a test of the area of the 6,124 peak, set in 2007. The biggest risk Chris continues to see is that the 2007 peak is akin to Japan’s 1989 major top, and that the secular bear market is not yet complete, but this is not his base case.

Still a good morning in Vietnam

Vietnam continues to be hit by confidence shocks, with further capital outflows and FX reserve losses in the face of US tariff swings and policy uncertainties. Yet, as Jonathan Anderson points out, the economy continues to power ahead. Exports and tourism boomed in the first half of 2025, domestic credit growth is back to decade highs and local consumption and construction have grown steadily as well. In short, things are fully "back on line" after the 2022-23 recession. And as always, Jonathan stays with the underlying growth story. Risks remain if Vietnam gets caught in the middle of a worst-case US-China trade war, but with massive external "basic" balance surpluses, ongoing market share gains and strong domestic indicators, Jonathan holds his equity market position as the country continues its path as an Asian tiger.

Commodities

Pockets of value emerging in energy-linked single stocks

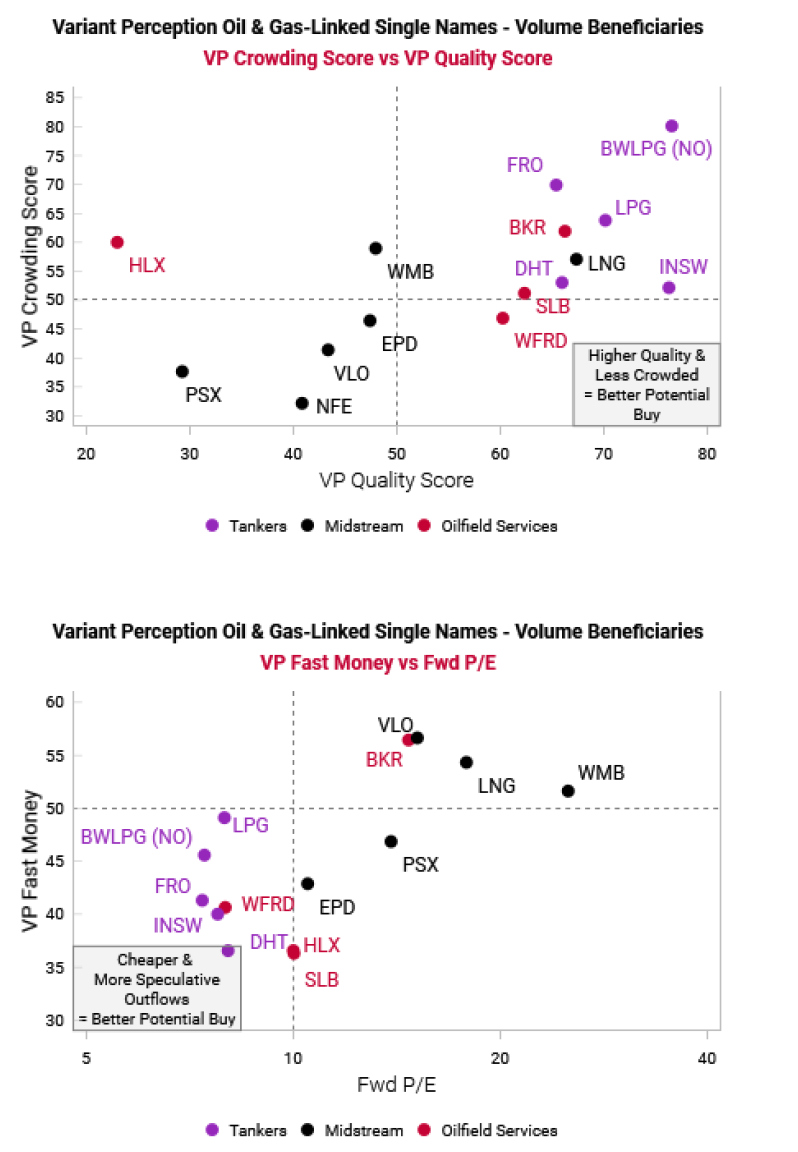

Variant Perception’s team suggest that underperformance in the energy market may continue, but they still see an opportunity for select single names if/when their tactical models turn bullish. They examine the market for single stocks that have favourable business models that benefit from higher volumes for oil and gas, and that screen well on VP metrics like capital cycle, crowding, and quality. Oilfield services, midstream and tankers are well suited, US-listed oilfield services are not. Despite appealing valuations, some midstream names still offer reasonable upside and volatility. However, among tankers, the team are highly cautious on LNG and product tankers as these have a glut of new builds coming online in the next few years relative to the existing fleets. Potential plays include

Schlumberger,

Baker Hughes,

Enterprise Products Partners,

Frontline

and

DHT.

Iron Ore: Higher prices, but still within medium-term trading range

Recently SGX 62% iron ore futures initially traded to lows of US$98.00/t CFR China in response to the release of a plethora of disappointing macroeconomic data. That said, there were several indications that some policy measures would be introduced soon to cut back overcapacity. Although the government's intentions will have a negative impact on China's iron ore consumption, the positive impact on Steel margins has counterintuitively dragged iron ore prices kicking & screaming higher. Accordingly, Atilla Widnell has updated his short-term target to US$100.14-101.55/t CFR China. As to the medium-term outlook, markets are entering a period of seasonably tighter iron ore supply through the third quarter. Atilla can't see how 62% iron ore futures trade outside of the current range unless there's a material black swan event. As such, he is only tightening the upper boundary given that he feels the upside potential is relatively limited, maintaining his medium-term outlook to US$95.70-105.15/t CFR China for Q3 2025.

Rising silver prices lead to a resurgence in Indian demand

Indian silver prices have posted a remarkable 32% ytd rally, touching a record high of Rs.116,551/kg. In contrast to the local gold market, where higher prices led to a slowdown in demand, silver consumption has strengthened in the wake of firmer prices. The Metals Focus team have also discussed with fabricators who are building inventory ahead of the festive season, and manufacturers are anticipating strong sales at the India International Jewellery Show (IIJS). Demand remains resilient due to high consumer confidence, the use of the metal as a substitute for pricey gold, and a healthy inflow into investment products such as exchange-traded products. Looking ahead, the silver market in India appears poised for further growth. However, if prices continue to rise and breach the Rs. 150,000/kg mark, some bars and coins may be sold back as investors book profits, impacting imports. Expect far higher prices to also weigh on jewellery and silverware demand.

Bigger and tastier shareholder returns?

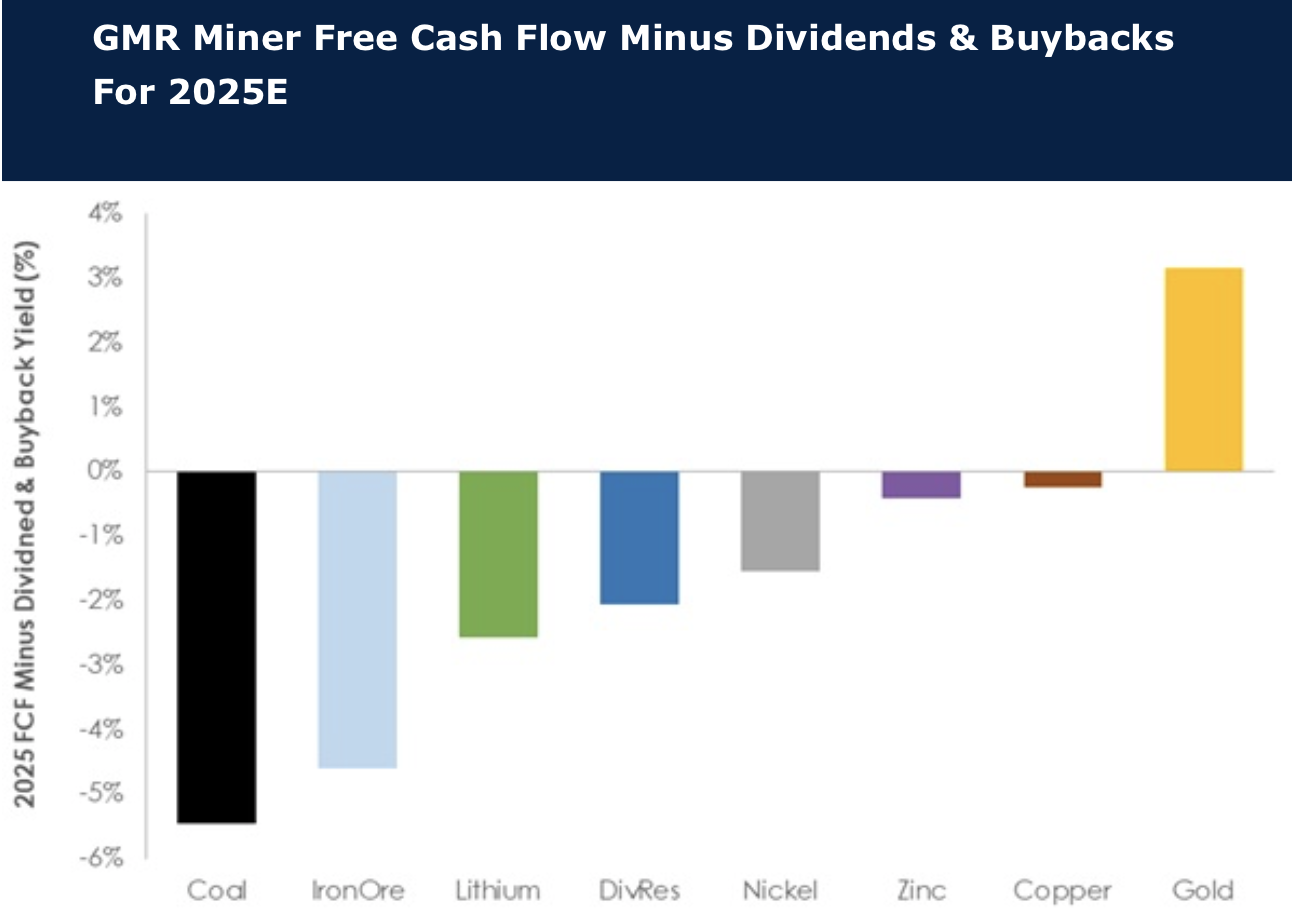

For investors, following the cash generation in mining has been a sound strategy. In David Radclyffe’s latest review, he focuses on sectors generating cash surpluses and those with deficits. From a cash generative perspective gold is the only sub-sector with investor appeal currently, with copper breakeven and a distant second, in terms of excess FCF after expected dividends and buybacks. Overall, the mining sector FCF yield has been deteriorating since the iron ore boom of 2021. The key conclusion is perhaps not only that gold stocks can pay more, but those sub-sectors such as coal and iron ore may payout less. David recommends an over-weight exposure to gold and copper. Diversified and iron ore stocks are feeling the pinch due to rising capex and contracting margins, while for coal and lithium the current bear markets continue.

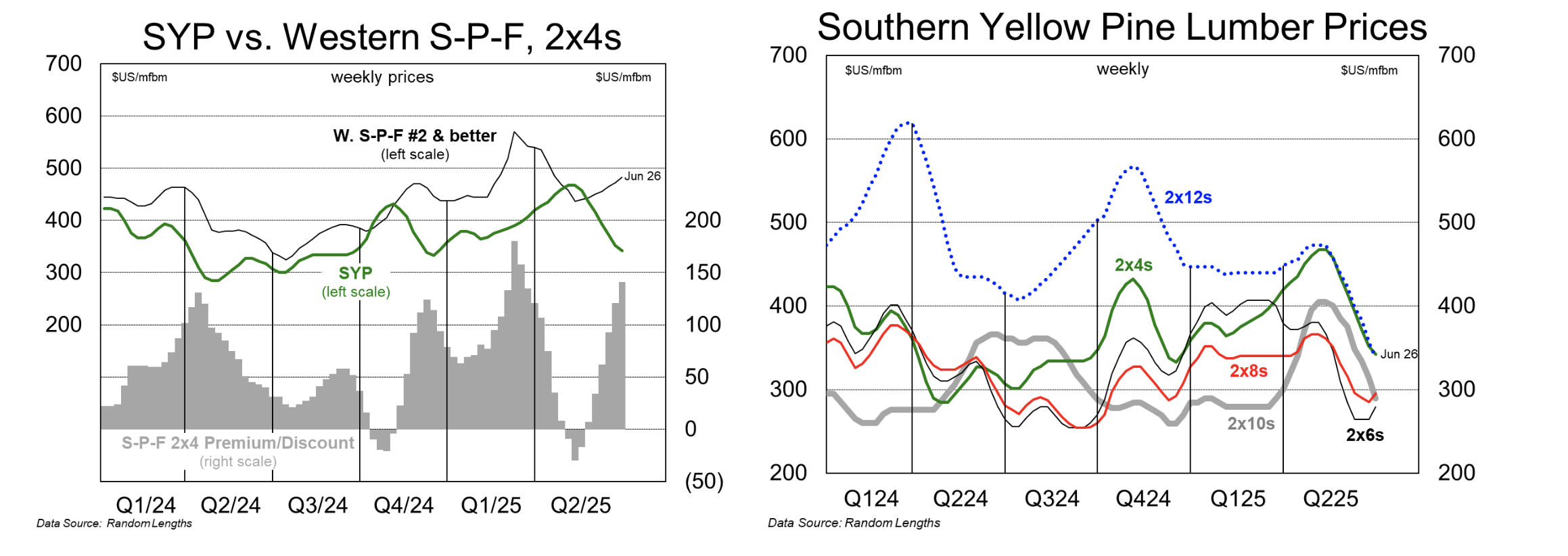

Lumber: Falling down

SYP lumber prices have been extremely weak in H1/2025, with 2x4 averaging $402 compared to S-P-F 2x4s averaging $479 (chart, left). Given these challenges, Canfor announced it will permanently close two mills. This may come as a surprise to some given the focus on trade woes and Canadian duties/tariffs, but the ERA team believe the move was sorely needed and sees future closures potentially following. SYP producers, as a whole, will benefit from marginally improved supply and demand balance over the near- to medium-term. However, with lumber demand expected to remain subdued through year-end and likely into 2026, further SYP mill capacity closures/downtime will be required before there is a sustained lift in SYP prices. The team continues to urge caution on Canadian lumber names given expectations for volatility related to the implementation of higher AR6 softwood lumber duties and a potential incremental tariff resulting from the ongoing Section 232 investigation.

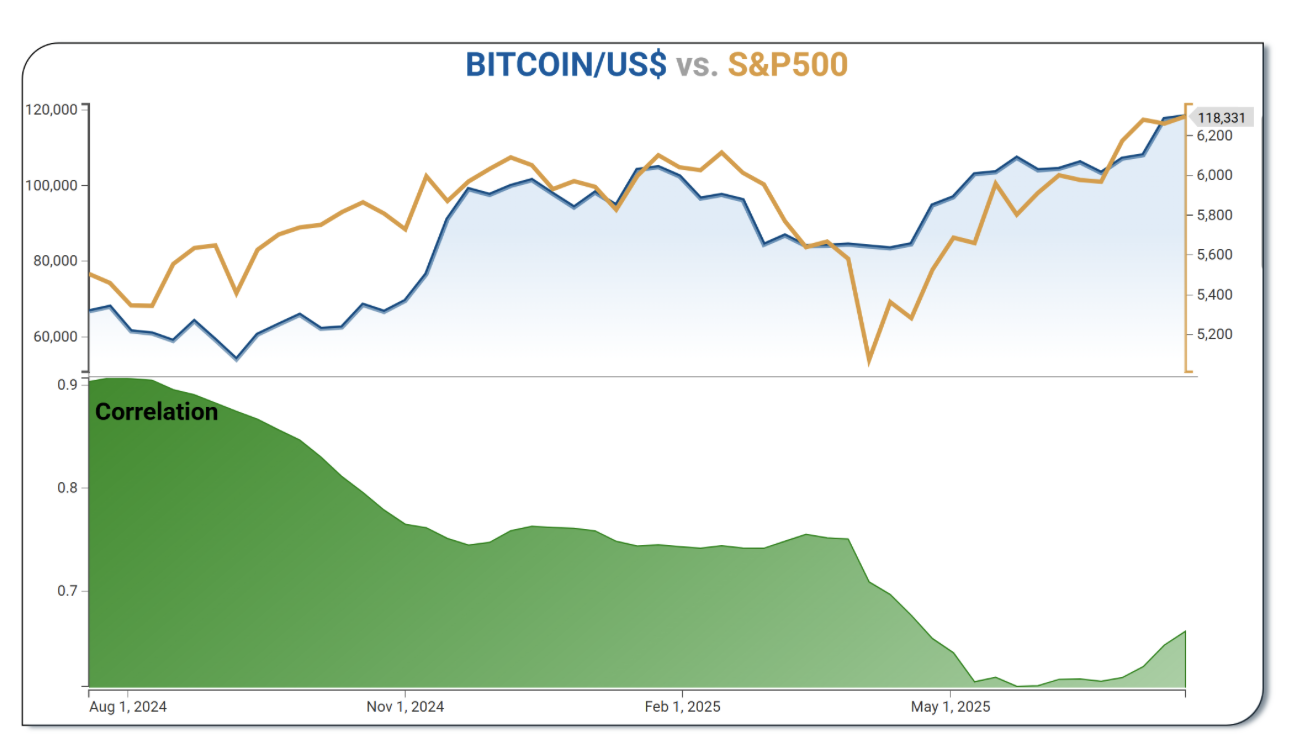

Upside for big crypto

Konstantin Fominykh’s models are flashing green for crypto, amidst improving regulation and wider adoption. He also points out that more signs of maturity are showing, with cryptocurrencies becoming less correlated to the immediate market moves; Bitcoin’s correlation with gold/equities has fallen to 50-60% (see chart), and the correlation between Bitcoin and Ethereum has fallen by 90% over the past year. Konstantin initiates a fresh buy on Bitcoin, forecasting 90% in 6 months, a fresh buy on Ethereum (+49%), and a buy on Solana (+25%).