Company & Sector Research

General

Intron Health

FDA Aducanumab Approval - Calculating the CDMO Windfall

Intron Health have conducted a detailed analysis which shows how much aducanumab will need to be produced, who the winners are likely to be and the revenue uplift - they estimate that there are ~30m potential patients and a need for ~30,000kg of aducanumab. Biogen will only be able to produce ~25% of the quantity required, the rest will go to CDMOs. Biggest beneficiaries include Lonza (could see a 14% EBIT benefit and an 11% sales uplift vs. Intron’s 2024 forecasts) and Samsung Bio (potential 37% uplift to EBIT).

Europe

TT Equity Research

Just Eat Takeaway.com (TKWY NA)

Faces increased competition as Rocket enters the Dutch market and DoorDash targets Germany, another of TKWY’s key markets. To maintain market share, TKWY was already shifting further towards the loss-making own delivery side of the business. Now, with Rocket focused on marketplace revenues (offering lower commissions to restaurants to boost market share), TKWY is also being attacked on the cash generating side. These latest developments only strengthen Teun Teeuwisse's short thesis.

Holland Advisors

Boohoo (BOO LN)

Same share price as last year, but now offers an even better risk:reward - BOO has gone from having just four brands to thirteen, has trebled in size, wields enormous social media influence and pivoted its product offering on a sixpence during Covid. It not only has the platform, but also the desire, hunger and ability to buy failing brands and consolidate them all online. The fact that Next and ASOS have recently started to pivot in this direction is notable - are they threatened by the opportunity BOO has created for itself…?

Smart Insider

Zalando (ZAL GR)

Interesting to see two of the biggest shareholders making large purchases with the shares near all-time highs - Cristina Stenbeck (Chairman of Supervisory Board) purchased 495,000 shares at €89.55, spending €44m. The Stenbeck family has a meaningful stake in Kinnevik, which is the largest shareholder in ZAL (20% holding). Last year she purchased shares at €47 and €52, but those were small purchases compared to this recent one. It also follows a €40m purchase at €86 from Anders Povlsen (Supervisory Board) for a Danish investment fund (10% holding). Smart Insider increase the Stock Rank to +1 (highest rating).

Creative Portfolios

National Bank of Greece (ETE GA)

A standout in Greek banks - ETE is in its third year of a transformation plan which is beginning to show tangible operational improvement including a strong performance in e-banking. Asset Quality ratios continue to make great strides and less than 7% of moratoria beneficiaries are in early arrears (>30dpd). On the capital front, ETE has enhanced its position, delivering CET1 and Total CAD ratios of 16.1% and 17.1% respectively. The share price has risen over 90% in the last 12 months, yet ETE remains attractively valued with a FV of 5%, a PBV of 0.44x, and an Earnings Yield of 12.45%.

Betaville

Deutsche Wohnen (DWNI GR)

When it comes to breaking M&A news Betaville Intelligence prove to be ahead of the competition once again - on 18th May they revealed that DWNI was in focus amid talk it could soon be involved in a major corporate transaction with rival Vonovia. Six days later Bloomberg followed up with its own version of the story and the following morning the two companies officially confirmed the merger. The news led to a 16% gain in DWNI’s share price. Other takeover deals recently identified by Betaville Intelligence include Elementis (+25% gain), Telit Communications (+59%) and Signature Aviation (+35%).

North America

Paragon Intel

ManagementTrack: Real Time Monitoring, Ratings & Background Checks on 3,000+ Executives

ManagementTrack allows investors to quickly diligence and compare C-suite executives for companies in the Russell 1000 & more. Each executive has a proprietary Performance Rating and an Integrity Rating. Real-time alerts on executive behaviour provide investors with an edge on current events that move stocks such as criminal and civil litigation, insider transactions, real estate transactions and media appearances. In addition to the aggregated data, ManagementTrack also contains in-depth diligence reports on externally hired CEOs by Paragon's investigative journalists. For further information click here. Free trial available on request.

The Edge

Exploiting Special Situations in Your Equity Strategy

The Edge CEO & Founder Jim Osman, who flagged a big contrarian call in Harley-Davidson (+98% gain) and the king of SPACs Playboy (+425%), will be pitching his next big call live at the MoneyShow (Fri, 11th June) in Orlando, Florida. Interested in hearing the next idea? Click below to set up a call and benefit from catalyst ideas that consistently show excess returns. The Edge will also be hosting a Spinoff Webinar (Thurs, 24th June) - How to Play Profitable Spinoffs that The Street Misses. Click here for further details.

AlphaSituations

Discovery (DISCK)

Robert Sassoon explains why market apathy towards Discovery’s merger with AT&T's WarnerMedia is a gift to value investors and believes the $43bn deal will give Warner Bros. Discovery a real shot at competing more effectively in the DTC streaming market. Robert sees 30%+ upside over the next 12-15 months (based on a very conservative 10x 2023 EV/EBITDA), with the prospect of a greater than 100% return should investors become “a little more excited” about WBD's streaming service strategy as they have done with Netflix and Disney.

Blueshift Research

Facebook (FB)

Facebook Shops are far from delivering on immense promise - Blueshift primary research reveals a “clunky” shopping experience for users, generating minimal revenue for merchants (ROI $1.00-$1.50 per $1.00 spent vs. $3.50-$4.00 seen from other channels). Issues include confusing rules for opening a shop, trouble optimising products and glitches where the platform rejects products. The meagre initial results created a cycle where sellers are reluctant to shift ad dollars from other channels and steer traffic to their Facebook Shops.

Huber Research Partners

Fox Corp (FOXA)

The new Fox is more profitable than investors expected - two years after it split from 21st Century Fox, the group continues to routinely beat expectations and often by significant amounts. Management are making smart decisions including taking a low-risk, high-reward path to streaming via Tubi - which is on fire (+150% in Q3; FY21E revenue target increased to $350m), avoiding large deals and hoarding cash ($5.8bn). Following yet another earnings beat, Douglas Arthur increases his FY21E & FY22E adj. EPS to $2.95 and $3.05/share (from $2.68 and $2.84). TP increased to $48 (~30% upside).

Two Rivers Analytics

Monro (MNRO)

Fighting negative secular trends in a near commodity business - margins have been declining for five years and will continue to do so. The company's intentional shift towards the tire business makes it more of a lower margin distributor as opposed to a service company. Eric Fernandez describes MNRO as a "no-to-slow growth business". A lack of online sales, limited pent up demand and the impact from ride sharing/WFH on miles driven will soon cause the Street to reassess MNRO’s prospects downwards.

R5 Capital

Dollar General (DG)

Impressive earnings beat and bullish near-term outlook, but Scott Mushkin believes the real story lies in the potential for growth to accelerate in 2022 and beyond. He sees the company moving quickly to increase the store build of pOpshelf and DGX. Scott describes pOpshelf as “the best new format he has seen in 20 years”. While DGX is a better-merchandised, lower-priced offering vs. traditional convenience stores which should gain share rapidly. DG is a must-own equity. TP $292 (42% upside).

Quo Vadis Capital

Ollie's Bargain Outlet (OLLI)

Overearning, underinvesting and not providing enough value to its customers - investors are going to be left nursing heavy losses as sales disappoint and margins come under pressure. The business is facing four quarters of negative comps and traffic declines in an environment of rising costs. Analysts think EBIT in FY21 and FY22 will be higher than both FY19 and FY18 suggesting that Covid will have a LT structural benefit to OLLI's profitability - this is a mistake.

Alembic Global Advisors

PureCycle Technologies (PCT)

PCT is a pioneer in the growing and untapped polypropylene recycling market with a novel and low-cost technology. Its fixed product price, which is at a premium to the market, and fixed raw material costs will result in stable and very healthy EBITDA margins exceeding 50%. Hassan Ahmed’s 12-month TP of $30 (50% upside) uses a plant level DCF analysis that conservatively only credits valuation for the start-up of 9 facilities by 2027 even though management are aiming to have 10 up and running by 2024 and 30 by 2030.

Global Mining Research

Freeport-McMoRan (FCX) vs. Grupo Mexico (GMEXICOB MM) vs. Southern Copper (SCCO)

GMR provide a comprehensive review of these 3 copper producers who together make up 15% of global copper supply. GMEX is their preferred choice on valuation grounds given it trades at ~1x P/NPV (vs. 2.3x for FCX and 2x for SCCO) and 4.6x EV/EBITDA (vs. 8.4x for FCX and 9.1x for SCCO). GMEX's significantly higher dividend (6.5%) will also appeal to income-hungry investors. GMR see no reason to own SCCO (rated Sell) since it can be bought effectively much cheaper via parent GMEX. While FCX is acceptable at spot prices, it looks very expensive on LT copper US$3.25/lb.

Summit Insights Group

CrowdStrike (CRWD)

Following stellar results and with the company once again ending the quarter with a record pipeline, Srini Nandury expects further beats and raises in H2. He continues to expect higher levels of security spending with different players winning in various segments of the market - CRWD to triumph in the EDR space and make a strong run in the SIEM space. Srini also notes that customer interest in Humio is very high which is likely to pose a problem for Splunk. CRWD’s moat is becoming deeper and broader. TP $275 (25% upside).

Japan

Asymmetric Advisors

Nikon Corp (7731)

News that Nikon will be ending production of its heavily loss-making single lens digital cameras only increases Asymmetric Advisors bullish view of the stock. Despite the shares having risen ~30% since Asymmetric made their contrarian Buy call back in February, analyst’s ratings remain overwhelmingly negative. Nikon’s low PBR and high net cash position (c.40% of mkt cap) combined with its lower cost base, pick up in higher end camera sales and rising stepper orders suggests further significant upside remains.

Emerging Markets

Horizon Insights

Opportunities in China’s Beauty Market

According to Horizon Insights’ monthly E-commerce data tracking, high-quality domestic brands have been increasing their market share as sales of mid- and low-end overseas cosmetics brands continue to decline. ‘Guochao’, the consumer trend to watch in China, has helped names such as Huaxizi and Perfect Diary challenge many of the international brands. Horizon Insights have also been exploring the medical aesthetics boom in China (believes market could double in size). Imeik and Bloomage are highlighted as very interesting investment cases with exciting growth potential.

Entext

JD Logistics (2618 HK)

Sean Maher has taken advantage of a modest day one IPO rally to add JD Logistics to his automation-themed basket of stocks (incl. Rockwell, Keyence, THK and Blue Prism). The logistics market has seen a brutal price war among major couriers, but JD Logistics’ differentiation is in offering “integrated supply chain” services. Stock to double within the next 2-3 years as a play on domestic consumption and technology licensing to third parties outside China. Its valuation vs. Ocado looks anomalous given its vastly superior relative scale, IP depth and growth opportunity.

Global Equity Research

AiHuiShou (RERE US)

Turning the vicious cycle into a virtuous one - Arun George examines the prospects for this exciting upcoming Chinese US IPO. Backed by JD.com (~35% stake), AiHuiShou operates the largest pre-owned consumer electronics transactions and services platform in China. The company is ideally placed to benefit from the huge demand for second-hand devices in China - a market that is 3x the size of the US and is expected to grow at a 30.8% CAGR from 2020 to 2025. Given the business model it will also appeal to investors with an ESG mandate.

Macro Research

Developed Markets

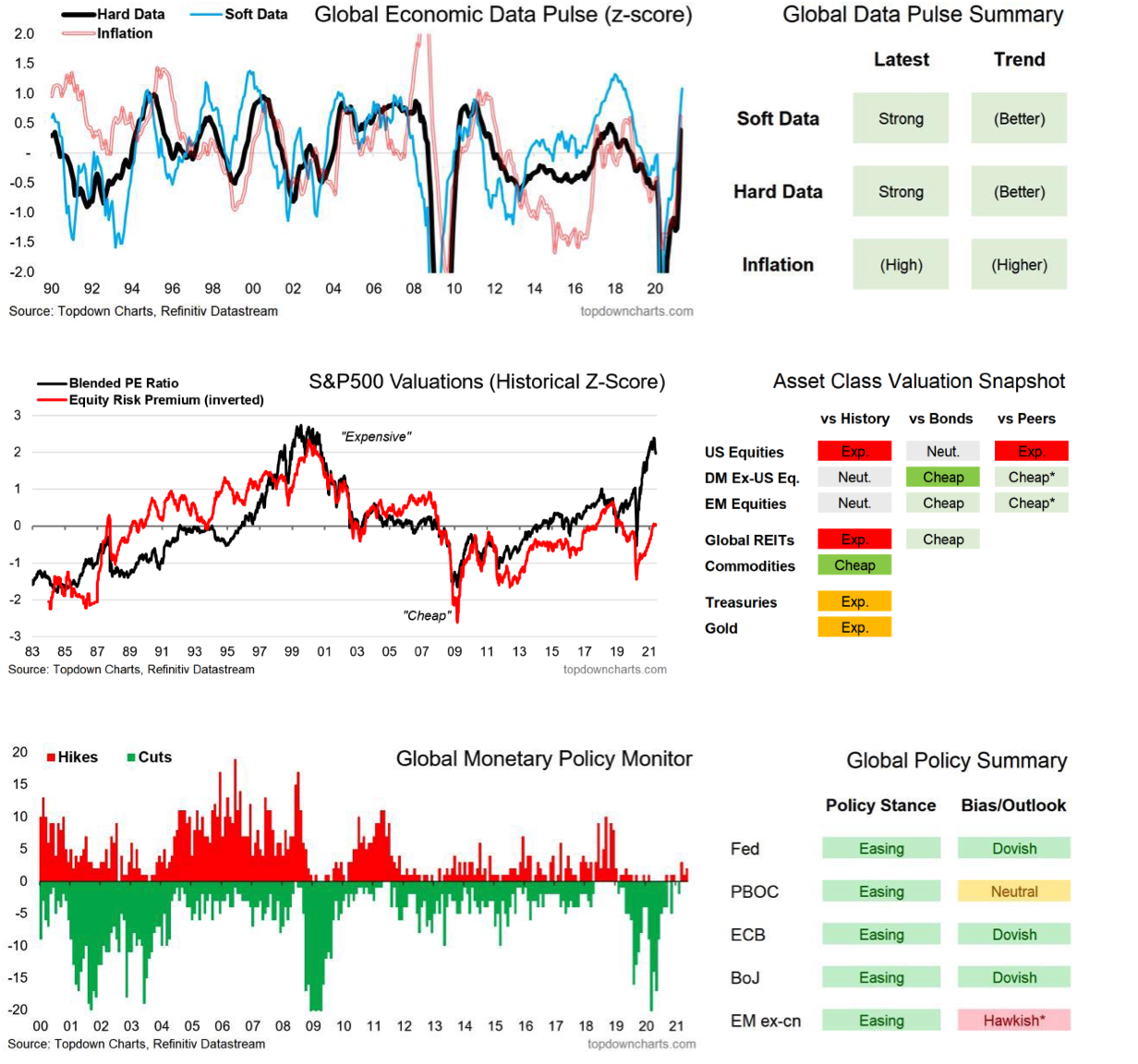

Topdown Charts

A more familiar pathway out of the pandemic

May highlighted the benefits of taking a more nuanced approach to asset allocation as we progress through the cycle - with some overlooked asset classes topping the table. It is key to pay more attention not just to the high-level allocations, but also within asset classes e.g., focusing on relative value as absolute valuations edge higher. But in terms of the high-level allocations, the progression of the macro/market cycle is definitely front of Callum Thomas’ mind as we transition from deflation to inflation, contraction to expansion, and ultimately from unprecedented monetary policy easing to tapering and then tightening.

Greenmantle

UK: Teflon Tory heading for re-election

Newly married UK Prime Minister Boris Johnson seems to be made of Teflon. The Tories’ resounding victory in local elections on May 6, even in the face of mounting scandals involving the prime minister, has emboldened the party. Their strong parliamentary majority will enable them to push through legislation this year that will allow Johnson to call early elections in 2023. While Niall Ferguson thinks forecasts of Labour’s death by the UK press are mostly overdone, he doubts that the party can stage a strong comeback before the next general election. Johnson is here to stay.

High Frequency Economics

Inflation: Just a transient blip

To the inflation hawks on the planet, Carl Weinberg says he isn’t seeing what they’re saying. YoY changes in core CPI are all below target and only slightly higher the past month. Their velocity and acceleration are suggestive of transient blips in supply chains as sectors of the economy spool up from a dead stop to full throttle. If we look at headline CPI, the runaway prices for energy prices are more the result of the falling basis in prices last year than any increases right now; in any case, fluctuations in energy prices are outside the realm of things central bankers can try to affect with monetary policy.

Belkin Report

US: Making sense of a warped economic cycle

Michael Belkin explains that consensus economic expectations are all far too high. By focusing on YoY data that has been completely warped by last year’s economic collapse, investors aren’t seeing that we’re actually at a peak right now – this is as good as it gets for US economic data. Stagnant demand will thwart the recovery; thanks to the artificial signals sent out by massive stimulus, companies will ramp up production just in time for falling end-demand. Wall St isn’t expecting this. Avoid buying cyclicals, expect TBonds to rally, expect defensive interest rate sectors to outperform, and expect a shake-up of an extremely inflated US Stock index.

Talking Heads Macro

Yields will rise to 3.5% as inflation falls

Manoj Pradhan believes that three inflation cycles are playing out at once, but only one is reflected in the price: the Covid stagflation cycle. Markets have failed to consider the cyclical overheating and structural stagflation cycles. As the former takes hold, yields will start to rise to 3.5%. Investors should take advantage by playing long high beta EM, low-flation EM (incl. SAF bonds and FX) and economies where growth outstrips inflation risks (incl. Korea and Taiwan FX and equities).

CrossBorder Capital

US: A skidding dollar?

The US dollar looks set to fall. Michael Howell’s analysis suggests 10-15% is likely, but he cannot rule out a more than 20% slump. The reasons are numerous and include the Fed’s easy monetary policy, the growing ‘twin deficits’ and the rival threat from China/Asia. But applying Occam’s Razor, the standout risk is the changing direction of ‘safe’ asset flows out of US assets. Foreign investors are starting from huge relative positions in US safe assets built up over the past decade, with foreign issuance stepping up, competition is hot.

AAS Economics

US monetary environment is changing dramatically

The trajectory of US money supply growth (AMS) has changed dramatically over the last two months, and Frank Shostak now sees a sharp peak in AMS growth and a rapid deceleration following the most extreme monetary printing in over a hundred years. His latest report focuses on the impact of this reversal on the US economy, with implications for US stock and bond markets. Frank mentions it is now more critical than ever to watch developments in US money supply and liquidity!

Minack Advisors

Australia's outlook brightens

The country’s good pandemic brought on the risk of a bungled recovery, a risk that is now fading. The outlook for wages remains uncertain, but Gerard Minack believes if the border is closed until mid-2022 we will see wage growth accelerate and lead to an RBA hike before 2024. The domestic equity market, following its peers, has priced in a robust recovery – Gerard comments that equity gains from here will be slower and bumpier.

Emerging Markets

Crystal Shore Alpha

Low risk opportunities in the Middle East

Over the past six months, there are two markets that have delivered relentlessly strong returns with almost no downside whatsoever; Energy Markets (+47% return) and the Saudi Arabian stock market (+25%). Greg Shore currently sees no reason for these two markets to stop delivering these “risk-free” returns. But while the United Arab Emirates have matched the excellent Saudi returns, for Qatar, Kuwait, Bahrain and Oman, the past 6 months have seen returns hovering close to zero. The good news: all of these Arabian markets present a low-risk of capital loss / highly attractive opportunity for investors.

Blonde Money

Asian aftershocks

With the latest Covid-19 variant taking hold in Asia, another supply shock is penetrating through the global economy, one that will not recover any time soon. Demand across the world will be pulled downwards as closures hit poorly vaccinated nations. Monetary and fiscal stimulus won’t help. It all comes to nought again in 2021.

High Frequency Economics

China: Yuan’s unstoppable ascent

The yuan broke to a three-year high against USD this week, prompting state-run media to declare continuous Yuan appreciation implausible. Yet with relatively little PBoC inaction, Carl Weinberg explains that Beijing isn’t all that concerned. The Yuan’s strength stems from balance of payments issues, and will continue to appreciate against both USD and its trade-weighted basket in what will be an unstoppable ascent towards global transaction currency status.

Inferential Focus

China’s Deep Sea Research

Chinese researchers recently put their soft-body swimming robot at the bottom of the Mariana Trench, where they moved around easily despite immense pressures. Deep Sea research is not even on the list of critical advancements for China’s five-year plan, yet they are rapidly expanding their technologies which will allow further research for critical minerals and resources in the ocean depths.

Horizon Insights

China: Weaker activity and stronger input costs

China’s economic momentum eased slightly last month as costs surged, and business activity is continuing to edge downwards. The month also saw rising input costs continuing to weigh on factory activity, stymieing demand for project machinery and electronics. On top of all of this, banks appear to be cautious to cater to non-property loan demand, despite Beijing’s calls for further credit support to small enterprises.

Oxford Analytica

Brazil’s infrastructure investments will fall short

Infrastructure concessions will not generate enough investment to compensate for low public infrastructure spending, exacerbating fragilities that will affect short- and long-term competitiveness. Droughts will cause energy sector concerns in coming months, with energy price increases resulting from the use of thermal power plants and imports. Bolsonaro’s disregard for public spending continues to ail the nation; a recourse is needed.

Alberdi Partners

Bullish Brazil

Marcus Buscaglia and Patricio Navia are more bullish than consensus when it comes to Brazil’s growth and FX. However, there are two visible shocks that could threaten their view. The first one is the ascendency of Lula as a likely president elect in 2022. The second is a potential taper tantrum in August 2021. Nevertheless, investors can expect the nation to withstand both shocks well relative to other LatAm countries.

Alberdi Partners

Chile: Hike to arrive sooner

Fiscal policy has gone into overdrive, with a structural fiscal deficit that will reach 9% of GDP this year. Hence Marcus Buscaglia notes that monetary policy should take notice and signal a change of tack. He expects the Central Bank of Chile to remove its forward guidance and he expect it to hike twice, to 1%, by yearend.

Greenmantle

Peru: Razor-thin election

The margin between the two top candidates - pro-market right wing Keiko Fujimori and left-wing firebrand opponent Jose Castillo – is nail-bitingly tight, especially when one considers the radicalism of Castillo’s program. Niall Ferguson believes the latter will be declared the victor but he will nevertheless be unable to implement his radical agenda. Volatile swings can be expected in currency, assets and copper markets exposed to Peruvian volatility as both sides contest the legal challenges.

Commodities

Janus Analysis

Bitcoin the new gold? No, it’s Tulip 2.0!

Gaius King explains in detail why Bitcoin is doomed to collapse. The energy-intensive currency - a CDO without any collateral – is being pushed up by speculators who fail to understand what constitutes a currency; Gaius estimates almost 100% of cryptocurrency transactions today are speculative. He recommends a number of shorts, particularly mining companies including Marathon Digital Holdings, Coinbase and Riot Blockchain. If you want to buy then look towards reliable gold, with Gaius recommending the likes of De Grey Mining and Gold Road Resources.

Longview Economics

Commodity prices: Ascension dissension

A major theme of the pandemic has undoubtedly been the broad-based rise in commodity prices. Despite the significant increases made in the likes of gold and Brent, several major commodities have begun to pullback from their highs. Is this recent price softness the start of a general trend of commodity price weakness, or is this a temporary pullback in an ongoing inflationary environment? How the Fed acts in coming weeks will be a key part of the equation in determining which outcome comes to pass.

J Ganes Consulting

Coffee: A healthy bull market correction

Market corrections are normal and a necessary, healthy part of any bull market. Judith Ganes’ fundamental perspective on the market is not rattled by a pullback. Forecasts for rain don’t dampen her sentiment either. The market still has significant supply issues oncoming, especially when considering restocking of supply channels emerging from the pandemic and logistical issues in the shipping industry. Judith remains bullish coffee.

Vanda Insights

Crude may be at an inflection point, but $80 is a stretch

Vandana Hari expects crude to see modest gains over the next three months, pushed up by bullish US oil demand and a hawkish OPEC+, along with a recovering India. We will see refined products (excl. Jet fuel) in Asia recover as governments turn to effective test and trace over lockdowns. Nevertheless, plentiful supply capacity and Chinese restraint will stop it reaching $80. Expect Brent at $65-75/barrel for H2/2021.