Container Shipping: Blockbuster earnings & logistical log jams

Drewry examine the implications of current congestion at key global ports such as Yantian in south China - sees it leading to further tightness of capacity and box supply, pushing up freight rates. Drewry now estimate an industry EBIT of ~US$80bn, representing an operating margin of 24% - a major upgrade from their previous estimate of US$35bn. For 2022, they expect an EBIT of US$50bn with a margin of ~18%. In other work, Drewry have also been investigating how the shipping industry faces one of its most significant challenges - to decarbonise its operations.

Apparel Retailers: Store Checks, Promotional Summaries & Key Data Points

LVMH - less enthusiastic when it comes to pre-Fall product, perhaps too much use of animal prints on classic shapes? Also wondering if the move back to smaller cross body bags creates a lower AUR mix shift for the industry.

Hugo Boss - summer sale tells the story. According to SW Retail’s proprietary data ~60% of total SKUs are on discount this season (US 63%, UK 58%, Germany 58%) vs. 27% for Ralph Lauren and 36% for Tommy Hilfiger.

Burberry - finally serious about promotions being a thing of the past. Recent price increases (Mid to HSD %) have gone largely unnoticed, but handbags continue to disappoint vs. competitors (lack of bright colours).

Royal Dutch Shell (RDSA NA)

Early innings of a complete narrative change - RDS to become an alternative energy leader in a decarbonised world. For a company with a large Mkt Cap, RDS offers a unique opportunity for outsized returns of 50%+ as investors better appreciate the SOTP valuation of its various businesses. Dividend capacity is also ramping up considerably paving the way for significant shareholder returns. Recent Dutch court ruling (re. carbon emissions) to serve as an ‘activist’ catalyst.

GlaxoSmithKline (GSK LN)

Disputing Elliott Advisors’ 45% upside - Intron's SOTP analysis explains why this is unlikely to occur within the timeframes proposed. GSK Pharma (ex-ViiV) would have to trade on 59x 2022 PE and CHC on 30x 2022 PE whilst ViiV would have to trade on 12x 2022 EPS despite the DTG patent expiry in ~6 years. However, Intron does support Elliott’s view that the board needs more industry knowledge; plus the incentivisation scheme needs a major overhaul in-line with the most innovative companies in the sector such as Novartis and AstraZeneca.

Ferrovial (FER SM)

Robert Crimes increases his valuation for FER’s 43.2% stake in the 407-ETR by €2.5bn to €18.7bn; explains why he considers it to be the most valuable toll road in Insight’s coverage. Their Willingness to Pay framework suggests tolls could rise up to 2-3x. Share price over discounting temporary low traffic levels and WFH concerns which will be offset by growth in Heavy Vehicles and 'other'/leisure uses. SOTP TP €57 (130% upside).

OCI (OCI NA)

Nassef Sawiris (Chair since 2021, CEO since 1998) has purchased €251m of stock at €20.60, increasing his stake by 18%. He has a strong record as a buyer across his previous 44 trades, qualifying as a "Smart Buyer". The latest purchase is notable for its size, it is 6x larger than any previous purchase and comes after the shares have doubled from the lows. Stock Rank +1 (highest rating).

Intriguing Merger Spreads

Among the universe of live M&A deals that AlphaSituations monitors (US M&A deals of >$400m) there are several transactions with the potential for annualised returns of over 20%. Robert Sassoon believes Magnachip Semiconductor provides the most enticing risk:reward profile. Potential bidding war brewing and in the event that there is no deal, a return to the $20 level would be the worst case scenario and most likely very short-lived given the fundamental outlook for the business.

Krispy Kreme (DNUT)

Dough-not buy this wildly overpriced IPO - DNUT was one of the stocks featured when New Constructs CEO David Trainer appeared on CNBC recently to discuss expensive IPO’s. The current valuation implies DNUT will simultaneously outgrow its peers while doubling profit margins - a highly unlikely scenario, especially given the shift in consumer preferences toward healthier foods and the failure of its past growth strategy to achieve the economies of scale needed to operate profitably. The stock is worth no more $10/share (70% downside).

Ulta Beauty (ULTA)

ULTA is enjoying a rapid recovery, driven by improvement in store productivity and strong replenishment trends across all categories. An emerging uptick in spending on makeup (40% of revenues) is now unfolding reflecting not only replenishment, but also a positive response to new product innovation. For example, Lancôme recently pushed up a new lipstick launch to meet higher demand. As a result, ULTA plans a strong host of prestige makeup brand introductions this month. This new trend is embedded in JJK’s +43% 2Q revenue and $2.37 EPS outlook, above +39%/$2.31 consensus and $12.50 F21 EPS forecast vs. $12.10 consensus.

Canada Goose (GOOS)

GOOS China to accelerate growth in FY22 driven by retail expansion and same store sales growth - JL Warren forecast sales up 50-60% in mainland China and believe the group can double its locations in the next couple of years. They estimate ~15-20% SSSG by launching more spring collections and improving conversion rates. On e-commerce: GOOS Tmall GMV nearly doubled YoY in June; for FY see ~25-30% GMV growth on Tmall and WeChat stores; believe the company will soon launch a new store on JD.com.

Ameresco (AMRC)

The technology agnostic renewable energy pure-play - an expanding portfolio of high-growth, high-margin energy assets makes AMRC a clear-cut and relatively safe way to play the broader energy transition. In addition to its favourable business model, Webber Research highlight the group’s significant backlog, visibility and momentum, as well as its early focus on the exciting RNG space. $80 TP is based on an EV/EBITDA multiple of 26x and 2022e Adj. EBITDA of $167m.

ABM Industries (ABM)

Short on unsustainable margin spike - ABM has temporarily benefitted from the introduction of its high-priced Covid cleaning services and aggressive management of labour costs. Earnings shortfalls to occur as margins revert to their prior ranges in this price sensitive business. Secular trends are working against the firm; remote work will affect office real estate demand for years (if not permanently). Also noteworthy, insider holdings are low and selling has increased significantly recently.

Extremely bullish set up for rates and equipment rental stocks

No let up in demand, undersupply to last well into 2022 - the situation appears even more acute and prolonged than TRG had originally anticipated. One of their equipment rental contacts provided a clear view of the current situation - “there’s not a rental company in our region that has enough equipment”. This early read leads TRG to expect strong Q2 results and raised FY21 guidance/outlook from United Rentals, Herc Holdings, H&E Equipment Services and WillScot Mobile Mini Holdings.

Carlisle Companies (CSL)

Nothing but blue sky's ahead - Northcoast upgrade the stock to Buy following their latest roofing checks. Underlying demand is building and prospects for pricing are improving. CSL has now announced 2 price increases in the last 2 months which will result in the company being price/cost neutral in 2021 (prev. expected ~$30m headwind) with sizeable tailwinds next year. Northcoast also believe CSL should divest its other segments and become a pure-play in CCM (its building products platform).

Ceridian (CDAY)

Underappreciated opportunity - CDAY’s Dayforce Wallet is the company’s first foray into a very different segment of the fintech ecosystem: digital wallets and earned wage access solutions. In this industry primer, Veritas assess the competitive landscape and compare CDAY's offering to products launched by Apple, Alphabet, PayPal, Square, Mastercard, Visa, Tencent and Alibaba. Veritas think the long-term gains of developing a fintech ecosystem are incredibly attractive and CDAY’s unique distribution advantage will help carve itself a piece of the market. Estimates that the module can generate ~US$220m of annual net earnings and be worth US$19 per share.

Intel (INTC)

New CEO Pat Gelsinger will fall short in his attempts to rejuvenate INTC’s innovation engine, prevent market share losses, and protect margins in the face of secular technological trends and unrelenting competitive intensity. Paragon’s short thesis also includes interviews with former colleagues and industry sources who worked with Gelsinger. He is characterised as an uncreative thinker and a weak team manager. Gelsinger’s ManagmentTrack Rating is 1.0 (proprietary score combining Performance and Integrity Rating; range is 0.1-9.9) - only 10 out of 3,468 executives have a lower rating across Paragon’s platform.

SailPoint (SAIL)

Sales starting to ramp up following the company’s progress over the past 18 months in enhancing their SaaS solution, Identity NOW. SAIL’s growth has previously lagged other high-flyers in the identity management segment due to their focus on a premise-based solution. However, following recent feedback from Sales Pulse’s partner contacts, sales momentum has improved significantly, growth is set to accelerate and performance in calendar Q2 has been strong. They expect the vendor to beat earnings expectations.

After 10 years it is finally time to own Chinese Telcos

New Street explains why they believe Chinese Telcos now offer the best risk:reward among large caps in the EM Telecoms sector. They are set to enter a multi-year period of outperformance and are likely to double on a 2-3 year view. Increases China Mobile target price to HK$90, China Telecom to HK$6.2 and China Unicom to HK$10.2. These are big upgrades and New Street do not take them lightly, but this is a very unusual situation. CT is considered the best near term pick, while CU has the most upside.

Alibaba (BABA)

Have consensus forecasts finally bottomed? Rickin Thakrar has previously written extensively about how the biggest hindrance to the BABA investment case has been the continually flawed forecasts. However, with BABA’s 2022 EPS expectations dropping by c.30% in the past six months, his EBIT/EPS estimates are no longer dramatically lower than consensus. Trading on a 20x forward PER and given Rickin is predicting 17% EPS CAGR over the next five years the shares now offer a compelling buying opportunity.

Tisco (TISCO TB) & Thanachart (TCAP TB)

Daniel Tabbush is very bullish on the prospects for Thai Financial stocks and given it is highly unlikely that rates in Thailand will be rising anytime soon the large dividend yields on offer are now also much more valuable. TISCO stands out at 7.1%, it is one of the finance companies to survive the Asian Financial Crisis and its earnings have been relatively steady. TCAP reports the highest dividend yield at 8.8%; it is unique with its 52% equity/asset ratio, ROA of 4.3% and with cost/income in rapid decline.

China Elevator checks better than expected

Absolute level of demand inconsistent with China downturn scenario; OTIS share gains continued; prefer OTIS over KONE - 2Q21 Elevator orders were cited in the +20-40% range relative to 2019 (+10-20% y/y) and with most manufacturers only forecasting order growth of +0-10% y/y for 2021, bias to management guidance remains to the upside. OTIS’ strategic initiatives continue to bear fruit - more competitive and aggressive marketing is leading to increasingly sustainable share gains. Shanghai Mitsubishi has lagged significantly through 1H21 with KONE also underperforming.

A closer look at Chinese Developers’ JV exposure

Lucror’s Asia Monthly is intended to broaden investors' understanding of the Asian USD high-yield market. In this report, they discuss how Chinese developers have increasingly been using JV projects to scale up. In 2020, an average of c.40% of developers’ contracted sales came from unconsolidated JV projects, significantly higher than 23% in 2017. Companies flagged with extensive JV exposure and possibly considerable off-balance sheet debt include Yuzhou, Sino-Ocean, Jinmao, CIFI, KWG, Logan and Times Property.

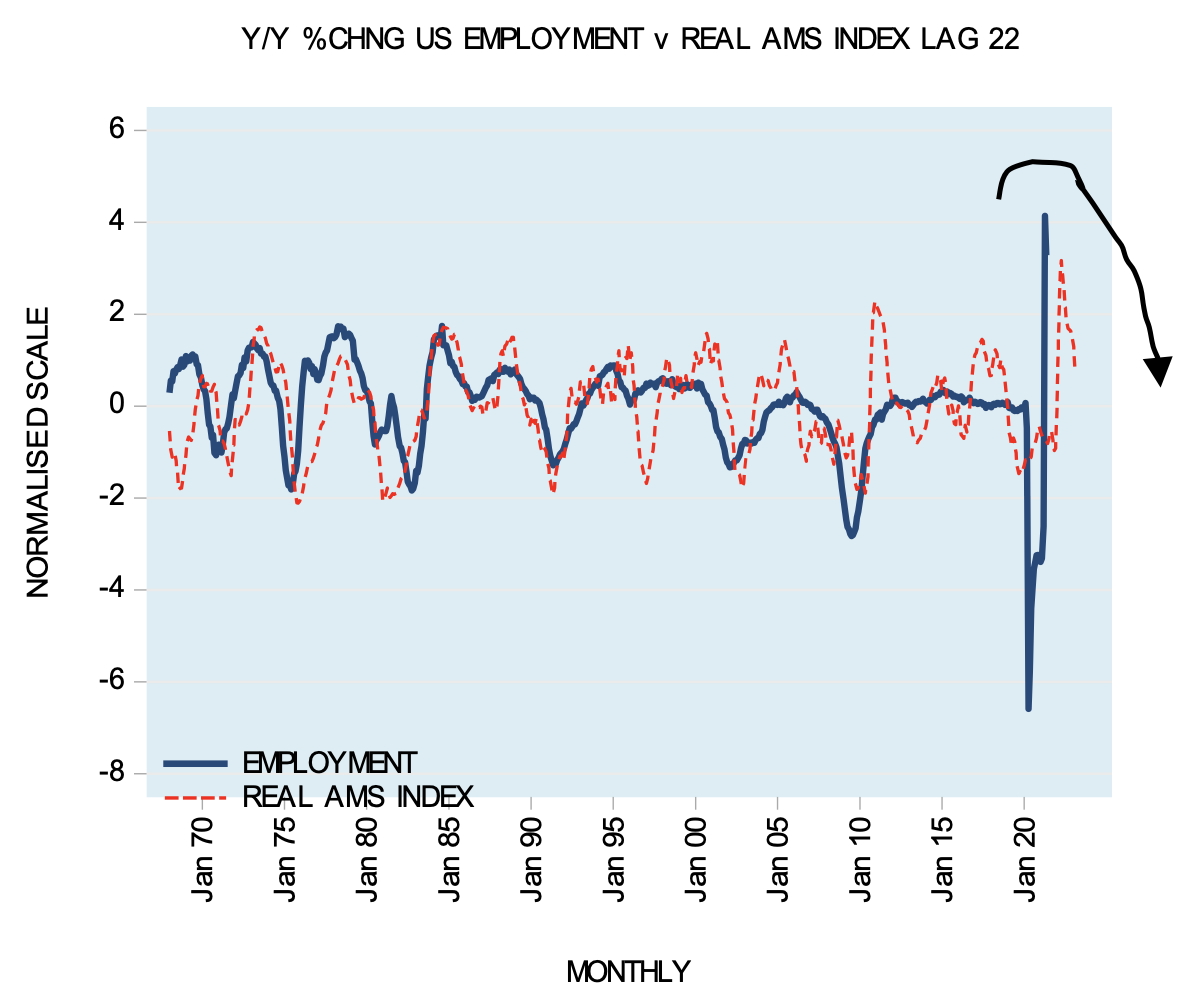

US employment momentum is weakening

US employment increased by 850k in June after a 583k increase in May. However, look deeper into the numbers and you’ll find that the yearly growth rate declined from 9% to 5.8%. Frank Shostak explains that the lagged momentum of the US real adjusted money supply (AMS) raises the likelihood that employment momentum will weaken further in the coming weeks.

US monetary policy made in China?

Are bond markets reacting more to slowing business activity than to tightening threats from the US Fed? Latest economic momentum data, calculated from economic surprises, show a sharp and accelerating decline across Asian economies. The culprit is China. Could this growth hiccup warn that policy-makers have started to tighten too soon?

UK: Sorry Mr Johnson, there is no free lunch!

Andrew Hunt believes that the UK govt has been seduced by the apparent ability to fund a deficit from the banking system without pain (via QE). Although QE may be appearing to fund the government’s deficit, in reality it is the foreign sector that is propping it up. Andrew comments that if the ECB ever decides to move against inflation, the BoE will be forced to follow their lead, or the UK will have to accept a soft currency and decline in real incomes. For all the talk of Brexit and trade, the UK’s real dependence on Europe is through its capital account.

When will Germany return to the debt brake?

Christopher Glück comments that Germany's debt brake will remain suspended until the end of 2022 at the earliest, and maybe even until 2024. This will bring forth tough decisions; despite the €48.2bn surplus Germany plans to dip into, it will still need to find some €4.9bn in savings and cut spending by €15.2bn in 2025. If the Greens manage to step into power in a coalition, higher spending will delay the return to a balanced budget even further.

Euro: Euribor next

On 14th April Julian Brigden recommended shorting the Bund market at around -26bpts with a target of ~+20 by Q3’s end. He believes higher PPI would drag HICP well over 2% and questioned when the hawks on the ECB council would re-emerge. Julian sticks with his trade, with fundamentals such as growth continuing to move in line with his prognosis. He recommends selling Dec 2023 Euribor at 100.31, stop above 100.45 (the end Q1 local high), target 99.50 by the end of this year for a 4:1 risk-reward.

Eurozone vs US: The tortoise and the hare

Headline data suggests that the US has recovered from the pandemic much better than the Eurozone. Such data is misleading and can be attributed to policy response; in reality, the EZ has a strong recovery story with less volatility than the US. David Roche believes the Fed is underestimating risks – catching up to them will be positive for USD. Investors should remain short EUR vs USD, overweight EZ equities and short Bunds and BTP’s.

Too early to bail on yield curve steepeners

The FOMC meeting two weeks ago triggered some volatility in the bond market and across risk assets. Still, MRB expect 10-year U.S. and G7 government bond yields to move higher in waves and yield curves to steepen further. The negative outlook for government bonds stems from MRB’s above-consensus inflation forecast, while deeply negative real yields underscore the potential for materially higher bond yields over the next 6-12 months.

Japan’s monetary boom coming to an end

Andrew Hunt points out that despite improving throughout 2020, Japan’s monetary data has softened of late. The BoJ has tapered quite aggressively, although the commercial banks have made a surprise return as buyers to the JGB markets. Private sector credit trends have also weakened significantly. Japan’s monetary boom of 2020 is on its way to ending.

Brazil: Scandal takes toll on Bolsonaro’s popularity

A new survey revealed a sharp increase in the disapproval rating of President Bolsonaro and his government, the highest since he first stepped into his role. Although his irregular purchasing of Covid-19 vaccines is partly to blame, some people were willing to cut him some slack; according to Joe de Courcy, the corruption allegations - which fly in the face of what Bolsonaro campaigned against - are a step too far.

The Chile we know will soon be gone

Chile is in the middle of a transformative process that will give the state a larger role in the economy. Marcos Buscaglia claims the country will continue to be pushed down the path of fiscal indiscipline and knee-jerk anti-market policies, and we will see in the coming months that Chile is no longer the fiscally responsible, market friendly country it has been for 30 years. He also forecasts the central bank to also raise rates by 1% by the year-end, with the first hike due in August.

China: A stronger agenda and a stronger military

Joseph Kasputys does not expect any political easing now that the Party centennial has passed. On the contrary, we will see strengthened efforts to maintain political unity and ensure progress with tech, energy and agricultural independence under the decarbonisation agenda. President Xi’s comments also make clear there will be increased spending through the military industrial complex over the next five years.

China: The Green Leap Forward

The ambitious carbon neutrality goals that President Xi Jinping announced last September are impacting all levels of China’s political and economic system. Niall Ferguson is increasingly confident that they are feasible. Top-level political pressure and new incentives for local officials will support rapid adoption of green technologies such as transit electrification, energy storage units, battery swapping, and charging infrastructure. But coal and oil consumption will not peak until 2025, due to concerns about energy security and baseload power.

India: Delhi will proceed cautiously with Lakshadweep plans

Modi’s government has encountered protests over plans to transform the Lakshadweep islands into a tourist haven, with a handful of draft regulations aimed at paving way for its modernisation plans. Although locals are keen to preserve their centuries-old way of life, Modi will push through the agenda, regarding it as key to extending its economic growth strategy beyond its political strongholds in Northern and Western India.

Taiwan – recycling riches

The jump in Taiwan’s already large external surpluses is not a one-off increase that will be corrected. Demand for the country’s exports remains robust and broad-based. Indeed, for many of its products there are no alternatives. Recycling these sums is proving increasingly difficult, which is being reflected in the acceleration of central bank reserve accumulation and rising domestic liquidity. The economy is hot; it risks overheating. Keeping the local currency weaker than it should be seems the ideal way to achieve this undesirable outcome. Remain long the Taiwanese dollar.

XRP, the crypto to watch out for!

According to Raoul Pal, Bitcoin doesn’t hold a candle to XRP, a crypto designed to facilitate cross-border payments. He believes the current SEC case against XRP platform Ripple will be settled and the media will turn to being super bullish as XRP paves a new way forward as the first crypto with complete clarity across the US govt. Raoul sees a rise from the current price of $0.64 to $7-10, and believes it could even reach $25!

Nickel’s price isn’t quite right

Tony Robson’s latest report explains that the price of nickel is not fully supported by the fundamentals. It is true that demand growth rates have been strong, but so has the surge in production from Indonesia, which will grow from 150kt in 2015 to 1,330kt in 2025. Positively, Tony expects EV’s to account for 21% of global demand in 2025 (from 2% in 2015). The best listed exposure globally to Indonesian growth is through BUY-rated Nickel Mines, while HOLD-rated Norilsk Nickel has the best dividend yield.

Weakness ahead for commodities

Commodities as an asset class are the most crowded long trade amongst asset allocators right now. Chris Watling explains that there is plenty of fuel for ongoing commodity price weakness in coming months as those long/OW positions unwind, triggered by a combination of tapering, slowing global growth momentum and a phase of USD strength.

Could blockchain facilitate peer-to-peer water trading?

The state of Colorado has turned to blockchain to help manage its depleted water supplies, allowing the trading of water to areas with scarce resources. The energy sector has already adopted the approach of “tokenised” energy, could water be next?