Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

Europe

Auto Trader (AUTO LN)

Losing its Shine - overly reliant on aggressive price increases to drive growth in an industry that is set for disruption. The company is highly dependent on small dealers, but these dealers are looking increasingly fragile and will struggle to absorb further price rises. StockViews’ research suggests dissatisfaction and bad will towards the firm is growing. In addition, CarGurus is now focusing its firepower on the UK market, while pure-online dealers, Cazoo and cinch, are growing rapidly and ultimately could disintermediate AUTO entirely. TP 400p (40% downside).

Iliad (ILD FP)

Mounting evidence that a large buyback is imminent - New Street notes that the last time ILD bought shares in the market (July 2019), an offer from Xavier Niel was made for 20% of the freefloat a few months later. New Street also address concerns surrounding the company's new capex strategy (a return on this capex is effectively a free option in the current share price). Trades at ~3-yr low in multiple terms, and in-line with incumbents on EV/EBITDA multiples despite much better growth (+8.3% 20-23 CAGR vs. incumbents +3.8%). TP €220 (85% upside).

EquiVal Research

Personal Luxury Goods Stocks: Europe's answer to the US tech giants

In the space of just five years, the share prices of the three French heavyweights, Hermès, Kering and LVMH have more than tripled - this is not far short of FAANG-style performance. However, given the scale of the growth and the return expectations already discounted, Piers Nestler wonders if these stocks are beginning to have a scarcity value themselves. If there is some value for money left, he believes it is most likely to be found in the watches and jewellery segment (highlights Richemont and Swatch), which has at least the potential to surprise on the upside.

Colruyt (COLR BB)

Belgian’s grocery market share leader looks expensive when considering the market is mature, elevated competition that is only increasing, one-time margin benefits in the prior year, and the unwinding of Covid tailwinds, especially after COLR just reported its lowest market share in more than 5 years.

DiaSorin (DIA IM)

Covid durability & Luminex upside - Intron's analysis points to a Covid resurgence in 2H21 in the West. Test sales will last considerably longer than most anticipate (they will be required for years to come). Intron also expect the Luminex acquisition will be ~30% EPS accretive by 2024 (consensus is yet to include pro forma numbers in its forecasts). Forecasts 7% CAGR EBITDA growth 2021-25 and Intron are 21% above consensus 2022 EBITDA. Net debt will rapidly fall (1x EBITDA by 2023) so M&A offers further upside. Abbott's profit warning last month has limited read-across to DIA.

North America

Airbnb (ABNB)

Double Upgrade (to Buy) - GHRA’s digital engagement data indicates trends have materially improved since ABNB last updated markets in mid-May, which when combined with still-elevated ADRs and lengthening stays suggest there is ample 2Q topline upside and EBITDA flowthrough relative to current estimates. ABNB warrants a valuation premium vs. peers given its (1) best-in-class brand recognition (2) faster recovery relative to traditional OTAs, (3) upward revision momentum ahead and (4) continued product improvement.

Interpublic (IPG)

Shares soar over 10% on stellar 2Q21 results and raised guidance which still looks conservative to Craig Huber. IPG remains his favourite ad agency stock. It has the best business mix in the industry and the Acxiom acquisition is proving to be a huge winner. Craig believes IPG’s profits and margins will be materially better off post the pandemic. This GARP stock is trading at only 14.4x/13.5x 2022/23(E) EPS (30-32% discount to S&P 500), 9.4x/9.1x EBITDA and 12.7x/12.1x FCF.

Sysco (SYY)

Behind the Numbers added SYY to its Top Sell list (11th June) arguing the recovery seemed more than priced in, Covid-related market share gains would quickly be lost and there was little room left to grow by acquisition. In addition, SYY has a history of reporting results with unusual items that allow it to top estimates. The last quarter was no exception. BTN identified over 7 cps in unusual benefits without which the company would have reported a miss. The stock is down 9% since addition but they see a strong possibility for disappointment in upcoming quarters.

Trupanion (TRUP)

Real competition has finally arrived - will result in higher CAC and lower ARPU for TRUP. Zoetis' pet insurance offering (Pumpkin) has gained traction in the market YTD. Its ability to bundle multiple services allows ZTS to offer Wellness Programs at a superior value, while Lemonade also poses a significant threat. Estimates Pumpkin and LMND are priced ~15%-25% below comparable TRUP plans. Negative impact is already evident: unique visitors to TRUP’s websites decelerated sharply y/y in April and May; Credit card panel data shows a deceleration in spending trends for the company; Pet Acquisition Costs increased to $279 vs. $200 pre-Covid. TP $60 (48% downside).

Etalon Investment Research

Vontier Corp. (VNT)

Rerating imminent for this high FCF, low CapEx business - impressive FY20 and Q1 FY21 results only confirm Alex Gavrish’s increasingly bullish position. Catalysts for a revaluation include VNT’s recent acquisition of DRB Systems, a provider of solutions to the car wash industry (notes favourable valuation vs. Mister Car Wash IPO) as well as the possibility for more aggressive M&A in the EV charging space. Currently trades at 10.7x EV/EBITDA and FCF Yield of 12.5%.

Verso (VRS)

Stealing Paper - Hamed Khorsand argues that the recent takeover bid of $20 a share from current shareholder Atlas Holdings materially undervalues VRS and the current state of the business. VRS has yet to report quarterly results showcasing the benefits of a series of price increases announced earlier this year. While the coated paper industry is cyclical, the current market conditions provide ample room for VRS to generate in aggregate ~$190m in FCF (or $6.42 per share) in 2021 and 2022. TP $30 (58% upside).

Shopify (SHOP)

Exceptional management and a powerful platform provide SHOP with the potential to layer on many additional services and continue its rapid growth. Desmond Lau can see a Prime-style membership being offered to consumers; while a digital wallet could enable P2P payments for Shop App users to connect to merchants using SHOP’s new Balance banking product. CEO Tobi Lütke has fostered a corporate culture that is innovative, highly motivated and adaptable to change, which is exactly what is needed in the rapidly evolving ecommerce landscape.

Gradient Analytics

Telos (TLS)

Concerned this IT and cybersecurity firm will soon report material losses from under bid contracts as its mix of risky fixed-priced contracts reaches an all-time high. Gradient also flag rising competition for sole-source contracts; surge in unbilled receivables; how a drawdown in deferred revenue is at odds with recurring revenue model and that management-bonus targets are being met with subjective accounting.

Zebra Technologies (ZBRA)

Sales are stampeding ahead - Northcoast’s latest survey of industry contacts/VARs was the most optimistic they have ever had in their 10 years of covering the company. 2Q21 was extremely strong - resellers experienced average sales growth of 14.0% and 22.8% respectively for the AIT and EVM segments. Contacts expect historic levels of demand to persist and the only obstacle to sales in 3Q21 will be securing products to fill orders. ZBRA is experiencing unprecedented pricing power; competitors Honeywell and Datalogic recently announced price increases, ZBRA is expected to soon follow suit.

Arista (ANET), Juniper (JNPR) & Cisco (CSCO)

While checks on product and sales execution have been steadily improving for JNPR and ANET, they are declining for CSCO. Sales Pulse believe that investors who are looking for any improvement for CSCO are going to be disappointed. While ANET's stronger performance may be expected, JNPR's appears less well known.

10Q/10K Text Analysis: Real time alerts on the data that matters

Text discussions within financial filings contain material information. By utilising AI, NLP, data analytics and qualitative analyst oversight, 280first can glean material and actionable insights on companies which will be missed by most institutional investors. Recent highlights include:

Fastenal (FAST) - Customer retention concerns.

FedEx (FDX) - Likely to face an even more competitive environment.

Herc Holdings (HRI) - Ready to initiate dividends?

Patterson Companies (PDCO) - Changing supplier relationships and margin impact.

Japan

Hitachi (6501) & Descente (8114)

Industrials & Consumer Discretionary

Hitachi - shares are up >50% since last highlighted in The Cut but still good value. This transformed group with its core focus now on power grid transformation work and industrial digitalisation is a multi-year growth story.

Descente - an underperforming athleisure company that Itochu took over and is transforming and only Asymmetric has been covering. Via a partnership with Anta Sports, the China store network is being aggressively rolled out ahead of the Winter Olympics and China earnings will rise from virtually zero to become the main contributor.

Emerging Markets

Datayes’ innovative AI revenue forecasting significantly outperforms consensus

Being the first in China to put Quantamental Investment philosophy into practice, Datayes facilitates your investment decision making with its flagship product - AI revenue forecasting - it is based on Datayes’ advanced forecast framework that combines machine learning with knowledge graph. With 83% winning rate as per FY20 results, Datayes covers 2200+ of China A-share companies and the list keeps growing. Click here for further details.

Global Equity Research

JD.com (9618 HK)

A critical quarter is on the horizon - JD.com is set to face the first in a series of brutally tough comps from last year. Rickin Thakrar expects 2Q21 earnings (scheduled for 18th Aug) to disappoint, negatively impacting JD’s valuation as well as estimates for the rest of the year. In addition, further scrutiny is likely to arise on the durability of JD’s cash flow which deteriorated significantly in 1Q21. Most analysts are pencilling in ~4bn RMB in working capital outflow, however if trends persist from 1Q, Rickin believes further downgrades to estimates will occur.

Investec (INL SJ)

Deposit base and Book Value do not reflect medium-term targets - the current PBV of 0.59x is way too low, especially given Standard Life’s recent acquisition of Liberty for >1x BV. The South African Deposit base is (roughly) rated in line with FirstRand which leaves the UK operation (47% of Deposits, 46% of Credit) valued at next to nothing. The current ROE stands at 5%, management aims to hit 11-15% in the UK and 15-18% in South Africa over the next few years (achievable though cost-cutting and greater digitalisation/technology adoption). Even a pre-pandemic ROE of 12% puts the shares on a PER of just 5x. Shares are far too cheap.

DMCI Holdings (DMC PM)

Philippine stocks are looking extremely cheap. Mike Churchill highlights several names that look particularly appealing including DMC - a conglomerate that churns out lots of cash. Over the past decade the firm has averaged a 20% ROE and now trades at 1.04x Price/Book vs. an avg. of >2.0x. Given the firm’s favourable mix of businesses (coal and nickel mining exposure are particularly constructive in the current environment), Mike sees no reason why DMC can’t get back to doing a considerable portion of its former ROE. Current dividend yield is 7.5%. TP PHP 10.4 (62% upside).

Is China Building a Data ‘Great Wall’ or World Leading Digital Regulatory Framework?

While Didi’s treatment may have shocked investors, China is attempting to achieve in cybersecurity/data privacy what it did in 5G by setting the global standard to gain a first mover advantage and dominate the market. Sean Maher believes this would ultimately be bullish for mainland tech and believes a China over US internet valuation mean reversion trade is becoming attractive. Sean also covers internet deglobalisation, Chinese companies listing abroad and how recent events will have huge repercussions for VC exit strategies.

Macro Research

Developed Markets

Llewellyn Consulting

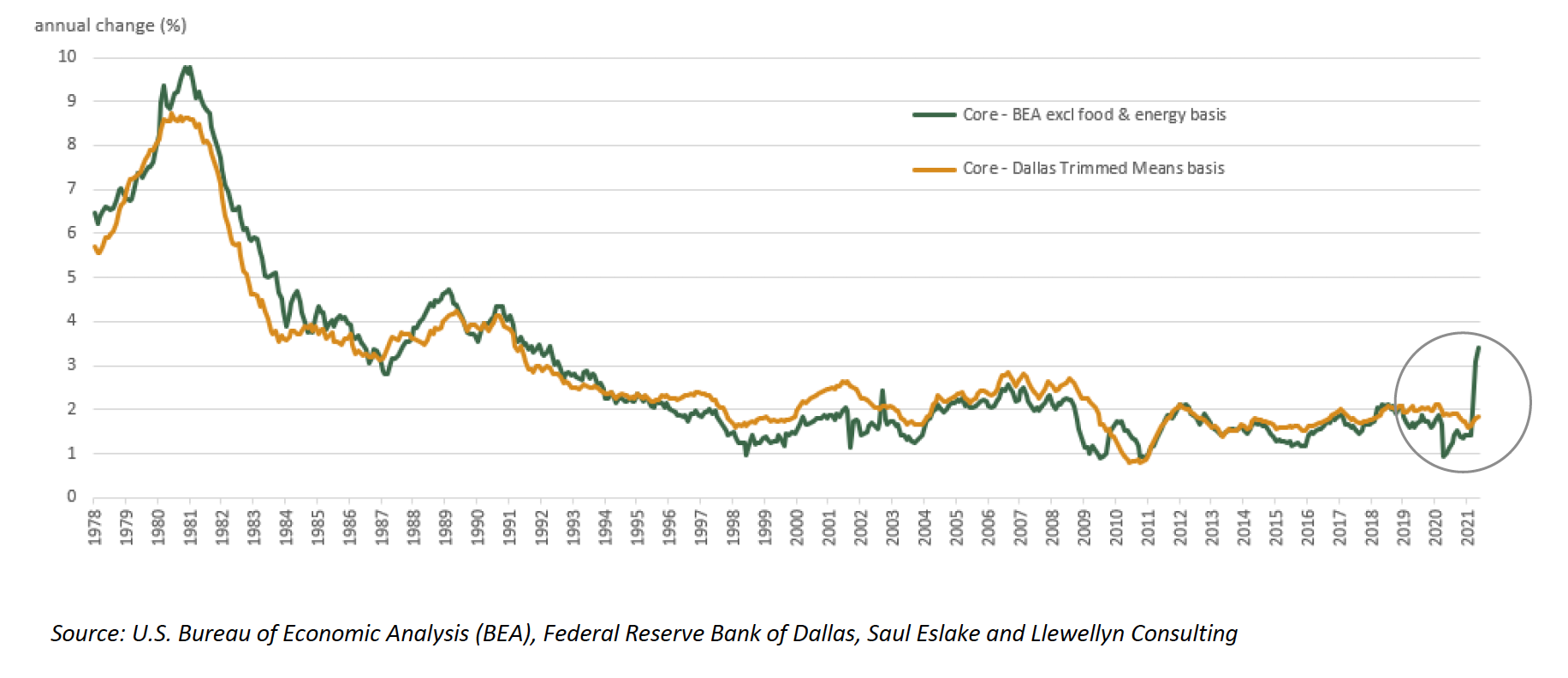

Chart of the fortnight: Which Fed price index matters most?

Price indexes monitored by the Fed are saying different things. The ‘core’ PCE deflator, which excludes food and energy, has inflation increasing by 3.1% in April, 3.4% in May. But the ’trimmed means’ measure, which currently excludes mainly prices of used cars and trucks – registered 1.8% and 1.9%. Which is the Fed to believe?

Totem Macro

BOOM BOOM BOOM

Whitney Baker examines the current upswing at play, one that is extremely unusual at this point in the cycle. Driven by lack of investment across the past decade and a shift in demand, it will be near-term inflationary but will bring more supply down the road, reinforce global leveraging and add legs to the cycle for years. Whitney comments that when such rapid growth is investment-driven, it is often positive for earnings, multiples and stocks. Play relative stock gains in value markets (that benefit from rate rises) and also expect US yields to rise sharply into next month.

The Three Musketeers

There are three camps underneath what is becoming an increasingly eerie calm, explains Manoj Pradhan: the noflationistas who see no chance of sustained inflation; the inflationistas like Manoj and Charles Goodhart who see sustained inflation in the 3-4% range; and the agnostics who are unsure of what is transitory and what is persistent. Manoj is convinced that most of the agnostics will become inflationistas, but they’re not yet big enough to turn the bond market. We need to be patient. Watch this space.

The metastasizing global debt bubble

Alex Krainer believes that the markets are still in denial about the unprecedented monetary experiment that is underway. We will see the real economy plunge into disaster with resource misallocation, stagnation, and a decline in opportunities and creativity. Alex claims investors should preserve their purchasing power with exposure to commodity prices incl. energy, metals and agriculture, but also seek diversification with precious metals, farmland and even cryptos.

4X Global Research

UK: Sterling’s coming home… albeit slowly

GBP/EUR is up 6%, in line with Olivier Desbarres’ bullish outlook. The catalyst for this performance has been the widening differential between UK and EZ CPI-inflation, which will widen even more. Olivier believes the MPC is divided but will turn increasingly hawkish, and UK GDP growth will be above the BoE’s peak forecast of 3%. Expect modest Sterling appreciation to Q3’s end.

Longview Economics

UK: Economic growth to remain robust

Although consensus points to a bearish second half when it comes to UK growth, Harry Colvin is confident that growth will be strong. Healthy UK banks, the mini-leveraging cycle that is underway, and strong household spending capacity (despite recent splurges) will provide the ingredients for a robust H2/2021.

German DAX: Heavily owned and vulnerable

The increasing reliance on equities in the last couple of months has been unstoppable, but the equity market’s assumption that the Fed’s hawkish pivot was a ‘good tightening’ worries Julian Brigden. Right now, the charts are ugly. In particular, he mentions that DAX is heavily owned and vulnerable to Europe’s premature reopening. Julian recommends selling half a risk of unit here (see graph) with a stop above the all-time highs of 15,850. Add the rest on a move below 14,800 with a trailing stop. The initial target is 13,100 and then 12,000.

Harlyn Research

Pharma: Saviours of the world

The global healthcare sector has begun to rally hard after hitting all-time lows in terms of its recommended weight vs benchmark. It had been previously ignored since it doesn’t fit in the current debate about growth vs. value, but Simon Goodfellow thinks it is worth another look. The risk of price controls on US prescription drugs is much lower than feared; Congress has no time for legislation in the run up to elections, and public opinion may have changed after the success of Covid vaccines.

Korea: A stronger KRW?

There are signs of inflationary pressures building in Korea’s strong economy, explains Andrew Hunt. He believes the BoK is signalling discomfort and may well be among the first countries to break rank with global consensus and begin tightening. The signs point to a potential strengthening of the KRW as pressure mounts on short-term rates.

Emerging Markets

Asia’s Bretton Woods

Michael Howell believes that there is compelling evidence that pan-Asian policymakers have been targeting their currencies in a de facto Asian currency unit akin to the Euro. EM economies, led by Asia, are targeting their currencies by managing capital inflows and outflows, and thereby allowing capital flows to largely dictate their domestic monetary policies. Although bullish near-term, it will be a drag in the longer-term as EM policymakers are forced to shadow a tougher Fed. Watch closely.

Africa’s poor cybersecurity

A growing number of key government activities, including elections, visa payments, taxes and more, are being digitised across Africa. The new technologies and rising use of ecommerce can help reduce corruption, but Matt Ward explains that cybersecurity will not improve at the same rate. We will begin to see numerous cybercriminal attacks in the years ahead as well as election manipulation, and African governments are poorly prepared.

Argentina: Capital controls tightening

The central bank and market regulator have tightened capital controls, aiming to reduce the access to the blue-chip swap market (CCL) via the bond market. Marcos Buscaglia claims this will follow the same logic as a floating exchange rate regime (e.g. expectations of monetary expansion leads to FX jumping instantly). With FX pressures frontloaded and upcoming elections, we will see pressures on the FX gap continue in coming months but with limited downside.

China: GDP on track to miss target

Carl Weinberg’s seasonally adjusted data suggests GDP in H1/2021 grew at only 3.1% at an annualised rate compared to H2/2020. No matter how you figure it, these results aren’t strong enough to achieve 6% growth this year. Carl therefore expects a massive fiscal stimulus to be enacted as soon as possible, and for the PBoC to ease monetary conditions repeatedly over the next six months to juice up the economy.

Inflation: Made in China

China has long been a key deflationary force in the global economy. The flood of Chinese exports has lowered goods prices over the past two decades, which was offset by Chinese commodity demand. Niall Ferguson believes that times are changing. Rising labour and input costs, a rising Yuan, and China’s green transition will push up Chinese export prices in the short- and long-run, even as commodity prices continue to rise. The shift from a deflation exporter to inflation exporter will stoke fears among central banks already sensitive to the inflationary risks of their loose monetary ways.

El Salvador’s Bitcoin currency

Concerns have been sparked over the choice to adopt Bitcoin as legal tender alongside USD, which may throw into doubt a $1.3bn financial assistance programme that El Salvador is negotiating with the IMF. There is also a worrying concern that a financial bubble could result, driven by Bitcoin’s volatility. Despite the issues, this could be the start of a broader trend among similar nations, with Paraguay and Panama potentially following suit.

Commodities

Canadian Oil & Gas

Even with recent OPEC+ news, Veritas Research expects the global oil market to remain undersupplied until 2021’s end, with a floor of $60 per barrel through 2022. With this low case, the setup for Buy Rated Oil Sands Producers is attractive, with Canadian Natural Resources, Cenovus and Suncor all attractive options (FCF Yields of >15% and Net Debt/FFO <1.0x).

Brazil’s coffee: A touch of Frost

Damage from recent frosts are wider spread than ever anticipated. Younger and vulnerable plants, ones that would be producing in 2023/24, may be destroyed. Judith Ganes comments that the damage is far worse than from the June drought. This setback will further hurt farmers, who have been unable to deliver crops and have committed to below-market prices. Judith explains that depending on whether or not farmers hold onto coffee as a form of insurance, we could see significant market ramifications resulting.

Covid, Crude, Copper and Coal

The market’s obsession with inflation has obscured the reality that Covid is continuing to erode reopening momentum, even in China, writes William Hess. People have focused on the prospect of weakening US/China activity levels as a catalyst for a derating of the reopening/reflation narrative, but the larger impact on growth should come from the impact of the delta variant on the rest of the world. Bond markets have listened, but commodities markets have yet to do so. William believes this creates the potential for a further correction. In his latest report, he summarises his key views on crude, copper and thermal coal.

Its decision time for gold

Michael Belkin believes that gold assets are in a tug of war between deeply negative interest rates and a potentially stronger USD. Gold loves real negative rates, and the developing global risk-off environment could be a positive for safe-haven gold. But a stronger USD will fight back. Nevertheless, Michael’s analysis indicates gold and gold stocks as recommended LONGs for now.