Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

General

Silk Road Research

Asia’s Covid Woes & Global Supply Chain Implications

More Asian countries are currently under some form of lockdown than at any point in the past year. This includes Taiwan, Thailand and Vietnam - all key source countries for global supply chains. SRR’s contacts in the Automotive and Automation industries now expect supply chain bottlenecks to persist for the remainder of the year with Logistics contacts expecting air and ocean freight to remain tight through to June 2022! SRR’s top picks for China exposure in H2 include Otis, ABB, Schneider Electric, Siemens, Yaskawa, Fanuc, Aptiv, Nio and Volkswagen.

Blueshift Research

IT Security Pros Can’t Cope; Supported AI Must Step Up

The stress on IT security professionals has reached an all-time high as relentless cyber attacks have exploded to a “war-like” level. The problem is causing large organisations to solicit mental health support for front line IT workers. However, going cloud is not a ready-made solution either. The cloud exodus comes with its own set of issues, primarily focused on the chaos at the end-user edge. Could a new industry built around a private, independent cyber warfare management sector be set to emerge?

Europe

Telecoms M&A Set to Continue…

Public market valuations do not reflect private valuations - the market is overly focused on very near-term FCF and capex gyrations without giving benefit for “good” capex or a likely return on capex spend. Iliad is a prime example of this. Xavier Niel recently made an offer for Iliad minorities at €182 - a sizeable 61% premium. While telecoms multiples remain low and fundamentals remain sound, such deals are easy to justify for any potential acquirer taking a medium to longer-term view. 1&1 Drillisch is likely to be the next takeover target.

VPK fails to measure up against the rest of Robert Crimes’ highly undervalued global infrastructure sector coverage (where the average upside is 75%) - he points to VPK's low visibility and volatility of end markets, high capex and reduced ROCE due to increasingly strict regulations, limited EBITDA growth and low attributable capacity additions. Insight are the only Infrastructure team to cover VPK and their analysis focuses more on LT FCF, DCF and IRR-Ke spread than near term earnings.

Holland Advisors

Ryanair (RYA ID)

Imagine RYA with pricing power! Andrew Hollingworth updates his bullish thesis focusing on the airliner’s end game - market dominance and higher yields (seat prices). While many analysts will be busy modelling near-term volume recoveries/units costs/carbon taxes etc. Andrew is looking further out. He was modelling RYA’s operating leverage for such an end game long before Covid struck and with the pandemic now easing (and c.20% of short haul capacity leaving the EU market) he thinks it right to start doing so again.

Bobst (BOBNN SW)

Investors continue to underestimate the expected improvement in sales and profitability over the next few years - following record sales in H1 and order intake +63% at the end of June, Research Partners are increasing their 12-month TP to CHF 100.00. Cost optimisation measures, economies of scale and savings from the reorganisation of the group’s structure leaves the company well positioned to reach 8% EBIT margin by 2025. Bobst shares are trading at an undemanding 6.3x EV/EBITDA(E) 2022, well below its long-term average (9.3x).

TeamViewer (TMV GR)

Playing for TeamPermira - with a CEO and board that is closely connected with Permira, it appears incentives have been designed to maximise the exit price for the UK PE firm. Management have employed several short-term tactics to achieve this outcome and sold an overly optimistic picture to the market. Consensus forecasts remain too optimistic, which is likely to result in further downgrades going into H2. StockViews' thesis already started to play out this week as H1 retention fell below expectations, resulting in the shares falling by 10%. TP €15.00 (40% downside).

North America

Event-Driven Legal℠ Investment-Research Opportunities

MDC’s “Event-Driven Legal℠” investment-research service follows significant legal disputes to provide clients with actionable investment ideas that tend to be non-correlated with the market. MDC has been providing its subscription “Event‐Driven Legal℠” investment‐research service since 2009. Typically, MDC keeps ~50 active cases on its Focus List and provides clients with breaking news/predictions during proceedings and analysis on important orders swiftly upon the Court publishing such information to its Docket. Current coverage includes: Amarin Pharma, Amgen, Biogen, Bristol-Myers Squibb, Catalyst Pharmaceuticals, Qualcomm, Renren and Xperi.

Capri Holdings (CPRI)

Blowout quarter, stock remains a double in 1-2 years. CPRI’s earnings power continues to be underestimated and Brian McGough is comfortable being the outlier (by a long shot!) - he increases his EPS forecast for the year from an already very bullish $5.20 to $5.50 (vs. Street/company guidance of $4.50). He argues that CPRI should be valued on a SOTP basis - the current share price assigns no value to Versace (should be worth $4bn by next year and $10bn by Year 5 of Brian’s model). In addition, CRPI will be debt free within a year and generating $5-6bn in free cash over the next five years...what will it do with all the cash?

Amazon (AMZN)

AMZN is at an important inflection point as it builds out an enormous distribution and logistics network - once completed no other company will come close to offering the same service. Management envisage that by speeding up delivery the market opportunity will be enlarged significantly. Scott Mushkin’s research strongly supports this notion. Further, as this natural monopoly matures, he sees a strong possibility that the government will step in and separate parts of the enterprise - this is likely to be value enhancing for equity holders.

Yum China (YUMC)

There are very few $26bn Mkt/Cap companies that can grow units sustainably at a DD rate - the combination of accelerating unit growth, resumption of share repurchases (has $4.3bn cash) and margin upside (margins and ROIC at the unit level are tracking ahead of pre-covid levels even as unit volumes have yet to fully recover) suggest upward revisions to future year estimates. In return for taking some China-related risk, you're getting access to a very attractive business trading at a meaningful discount.

Adding More Biotech Exposure

When the two-year ROC for Biotech/SPX approaches zero having been negative for more than six months, Biotech return profiles improve dramatically - three-month returns approach +15% while returns twelve months out exceed 35%. Besides strong seasonality, the sector is currently trading at a 10% DISCOUNT to the SP500 on a trailing basis. Oh, and don't forget The Cup and Handle!! - the Biotech Index has done nothing for years and traced out an extraordinarily large, some might say Brobdingnagian, base that projects significantly higher.

TFI International (TFII)

With a string of acquisitions under its belt, management seems to have hit on a gamechanger in buying the UPS Freight Business. Q2 gave investors the first look at the operational improvements management can make to the assets and there is a lot more to come (highlights real estate potential / excess capacity can be used to create additional value). An underfollowed and underappreciated stock that bounced around for years, TFII was trading at ~US$39 when Veritas turned bullish last year, the stock now trades at $110, but plenty of upside remains.

West Fraser (WFG CN)

Lumber prices have corrected sharply after reaching $1600+ in Q2, but historically high prices will persist for at least another year. Market downtime in BC (cost related) should keep the price floor high (~$600) for several quarters, benefitting producers in other regions (73% of WFG’s capacity is ex-BC). Prices may trend sideways for the balance of Q3 as supply chain inventories adjust, but ERA Research expect a strong seasonal trade (late-Sept to May) as R&R demand recovers and housing remains robust. TP C$140 (55% upside).

Crown Castle (CCI)

J Martin (Chairman) purchases 11,200 shares at $191.51, spending $2.1m - he qualifies as a "Smart Buyer" with an almost perfect record of 9 timely purchases out of 10 since he started buying in June 2002. This purchase is notable as the price has increased by more than 20% since his last acquisition in March. Bodes well for shareholders to see him continue to add at this higher price level.

UiPath (PATH)

Too much hype, too little differentiation, commoditising market, unsustainable valuation and slowing growth - Srini Nandury initiates coverage with a Sell-rating. Estimates 50% of RPA (Robotic Process Automation) projects are not delivering on their intended goals. Competition is intensifying and Srini considers Microsoft to be the most significant threat. TP $40 translates to 23x EV/C2022 sales - PATH should trade at a discount to high growth peer groups since most of its revenue is derived from on-prem sales. Lock-up expiration (Oct 18th) is likely to result in the shares coming under further pressure.

Suspicious Overearners: Buckle (BKE), HCA Healthcare (HCA) & Owens & Minor (OMI)

Two Rivers’ model seeks companies that are potentially “over-earning” - defined as companies with unusually high margins relative to their own history or relative to the industry. Provides fertile hunting ground for shorts if the reasons for the margin increase are either unsustainable or fraudulent. The best short candidates include:

BKE - No sales growth pre-Covid. Gross margins have since risen from 40% to 48% and EBITDA margins from 14% to 25%.

HCA - Incremental gross margins have reached 40% vs. sub-20% GAAP. Trades at record high EV/S and EBITDA multiples.

OMI - Stock trades based on the continuation of very high margins. Insiders are suddenly and sharply selling off shares.

Japan

Exciting Opportunities in Small Caps

Imagine a world where a company had a 99% share of a nascent market which could grow 15-20x were it to replicate comparator overseas peers. Where an initial shift towards digital marketing hinted at staggering growth potential. And where a largely alien concept product had started to permeate public consciousness on its journey towards becoming mainstream. That company exists in the ignored, unexplored, opportunity-rich plains of Japanese small caps. Now imagine what could happen if you owned it for the next 10 years.

Emerging Markets

China Credit Chronicle: Hazardous National Anecdote

The fall of HNA Group and others to come is a necessary step of the learning curve for investors in Chinese credits - recent events show us that Chinese mega corporates (i.e. China Huarong and China Evergrande) have enticed international investors (and perhaps rating agencies) to ignore credit fundamentals and believe they will be supported by the local/central government when necessary. The recovery value of HNA-related bonds has become uncertain with asymmetric downside risk to all HNA-related debt, let alone SANYPH 10/21s and HONAIR Perp.

Risky Business: China’s Tech Crackdown & How to Navigate it

While the official ban on the most lucrative activities in the after-school tutoring sector marks a new low in the regulatory crackdown, RedTech maintain that China is not trying to strangle the golden goose. A handful of big losers will be offset by a majority of companies that are well positioned for growth in a tighter regulatory environment. The less risky (Tencent) are being dragged down with the more risky (Didi), creating lucrative, long-term investing opportunities. Other companies mentioned include Alibaba, Ant Group, ByteDance, Douyu, Huya, JD, Meituan, Pinduoduo, Sogou and TAL.

Understanding Asia is Key to Understanding the Future of Esports and Gaming

This is the most comprehensive esports report on Asia that Niko Partners have ever published and is a critical resource for anyone investing in the industry. Covers markets including China, India, Japan, South Korea, Singapore and Thailand. Focuses on growth drivers, top game titles, teams, tournaments, the esports ecosystem and organisation structures, collegiate esports, women in esports, mobile esports, and more. Click here for further details.

Datayes' News Sentiment Analysis Excels in China A-Share Market

Sentiment is often a powerful driver of stock price trends in China. For offshore investors, deploying AI-driven Revenue Forecast and Sentiment Analysis can provide unique insights into the factors influencing valuations, momentum and risk. Leveraging advanced Natural Language Processing and Machine Learning capabilities, Datayes' News Sentiment data provides investors with an edge when it comes to alpha generation in the China A-share market. Click here to download the white paper.

Macro Research

Developed Markets

Intertemporal Economics

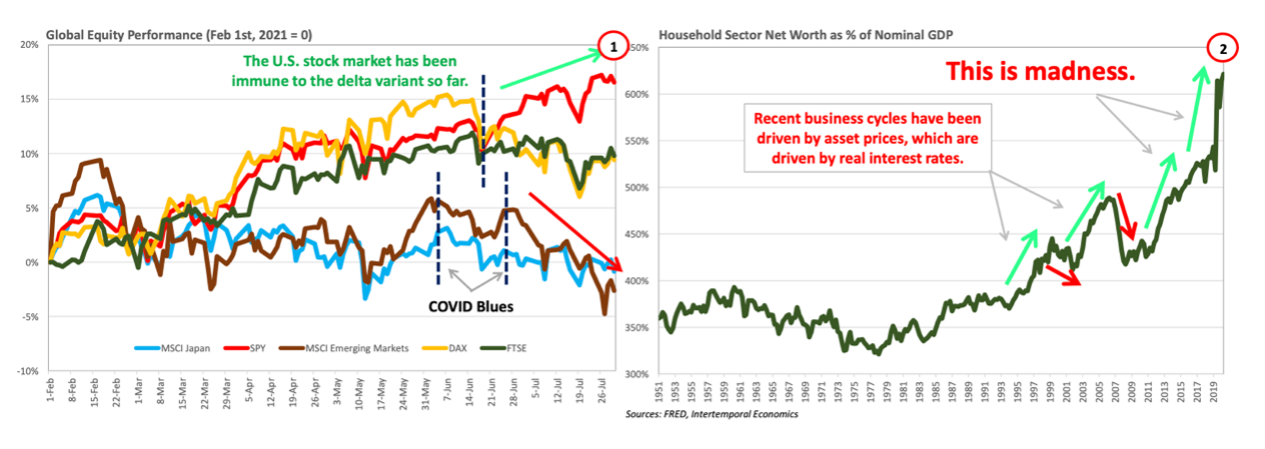

Chart of the fortnight: US - A Hayekian cycle is here

The US equity market has been immune to Delta Covid blues, despite Japan and European equities breaking down in June. What is the US outperformance built on? Brian Pellegrini claims it is the modern equivalent of the Tower of Babel. The current bubbles dwarf the DotCom and housing bubbles. This is a Hayekian cycle: beautiful to look at but terrible in its effect.

Most major economies slowing, but still above trend

Make no mistake, despite prevalent slowdowns in most major economies they remain above trend according to Jeffrey Young. A turnaround is taking shape on the inflation front, with falling rates in economies where it rose early on. Risk remains low. It all bodes well for the financial markets, albeit if a slightly more defensive posture is recommended.

Covid’s monetary response has run its course

Michael Howell’s analysis shows aggregate liquidity data growing at 6.9%, the lower end of the long-term pre-pandemic range. Liquidity growth is now normalising, with the Fed and ECB at the front of this normalisation dating from early April. The BoJ has added to the squeeze recently, and the PBoC has slowed its liquidity provision. Normality is returning.

Greater Fool Theory

In his latest report Ron William warns about the current paradoxical bearish market setup of overbought extremes and asymmetric risk. Seasonal patterns traditionally exhibit a climatic peak during August, as part of a “fall-crash cycle” into September and October, fuelled by high volatility. A growing number of markets are rolling over now below their short-trend averages, highlighting mean-reversion risk back into the 200-day line.

Forefront Advisers

UK: New government interventionism?

New government scrutiny of individual takeovers (incl. ARM and Newport Water Fab) has raised concerns over the UK entering a more interventionist paradigm. These forces shouldn’t be overstated according to Charles d’Arcy-Irvine: the UK is still an outlier among the G7 in its reluctance to intervene. That said, the cat is now out of the bag and politicians will continue to dance to the tune of interventionism.

Eurozone: Double-digit producer price inflation

Eurozone PPI was reported as 10.2% higher than a year ago in June. Carl Weinberg believes that an uneven spooling up of demand and supply in a relatively small number of products was responsible for boosting PPI in June above the 2% inflation target. Supply will catch up with demand, and investors should prepare for the price increases reversing soon.

Australia: Stagflation has arrived

The government’s policy response to Covid has created stagflation and real economic output trends have disappointed. Policymakers face a difficult question of reacting to inflation or sluggish growth. Andrew Hunt believes monetary policy will pay more heed to inflation than fiscal policy; investors should position for higher inflation and an eventual RBA response, although short-term market sentiment will be driven by lockdown news and weak real output.

Emerging Markets

Totem Macro

China: No longer the growth engine it once was

Whitney Baker explores in detail the terminal situation of Chinese VIEs/ADRs, where Beijing’s crackdowns will inevitably hit investors exposed to Chinese firms. Such a broad swathe of stocks are being affected that diversification seems somewhat implausible, and single-stock investors could face massive losses overnight. What’s more, Whitney believes China won’t be the important global growth engine it was in the last cycle. As the rest of the world releverages and booms in synchronised fashion, China is forced to deal with its massive debt binge. Chinese volatility is barely affecting EM stocks (ex-China) and its issues are no longer spilling into global growth. For investors with toes dipped in China, is it time to look elsewhere?

China: The dragon and its tech

Niall Ferguson has long been warning about Chinese tech companies becoming ensnared in political risks created by Beijing and the strategic imperatives of the Cold War II; such fears were realised in the stock market last week. New US transparency rules conflict directly with China’s new data security laws, with Chinese tech firms stuck between a rock and a hard place. Beijing’s rectification campaign will last until year-end. Afterwards, opportunities will still remain in China tech, but to spot them investors should look more towards Hong Kong than the US.

China’s CNY: Is this 2015?

Markets are boring and frustrating, but Julian Brigden is worried about the CNY. Just take a look at the divergence between USD/CNY and the Broad USD Trade Weighted Index and you can see that CNY is excessively strong (which was perfectly captured in CNY/JPY). Switching to USD/CNH for trading reasons, Julian recommends putting on half the position here because there is still a chance this is a false breakout. Add on a move above 6.55 - Julian’s target is 6.77 (with a stop below 6.45).

Independent Strategy

Be very cautious about Chinese equities

There are two key variables to consider when investing in Chinese assets. First, the change in Chinese Communist Party (CCP) policy, with its invigorated emphasis on national and international goals. Second, the inevitable decline in the economy’s expansion, to a 5-6% growth rate — a trend that was hidden by the saw tooth recovery from Covid that China experienced first. Together with the structural problems of over-leverage and malinvestment, David Roche is very cautious about Chinese equities, neutral on the currency and debt.

Latin America’s growth prospects

The region’s booming exports (due to high commodity prices), accommodative domestic policies and super-expansionary monetary policies will see GDP growth across all countries exceed consensus estimates, according to Marcos Buscaglia. However, when 2022 comes growth will fall sharply and political noise will burden investment. Investors should take advantage of cheap LatAm currencies with limited downside: Marcos sees upside in both the BRL and COP.

Peru: Sovereigns are oversold

After sending bond and currency markets into freefall last week, Peru’s newly inaugurated president Pedro Castillo has tried to course-correct with virtually no effect. Markets remain uneasy despite his attempts to appease. Niall Ferguson’s view is more sanguine: investment-grade Peruvian sovereigns are oversold. For investors who can stomach the coming weeks of volatility and confusion, there remains potential upside.

Parliament may at last reconvene in southern Yemen

The Hadi administration is seeking to strengthen its legitimacy with plans to reconvene parliament shortly. A successful legislative session could gain international leverage, as US officials visit the region to push for peace negotiations with the northern Huthis. However, it will garner little new support on the ground in Southern Yemen, where security and services remain key complaints.

ESG

Curation Corp

Lack of clarity on company emissions

Curation Corp comments that companies have a long way to go when it comes to clarity from organisations on emission disclosures. To keep within the 1.5C emissions target of 61.4 gigatons of CO2 equivalent, drastic cuts are required; right now, the budget is on course to run out in six years according to the MSCI Net-zero tracker. An international framework requiring firms to disclose climate risks may soon be reality, and it’s needed.

Marginal investment in social responsibility hurts corporations

Stephen Soukup argues that social responsibility measures are highly unlikely to be the driving force behind any alpha that a holding generates. In fact, social responsibility is the variable that provides the smallest amount of differentiation between companies. Firms that use profits to reinvest in environmental and social justice are in fact stifling their stock performance! ESG mandates will worsen things too by stymieing small company growth.

Commodities

Global Macro Investor

Ethereum: The Greatest Trade

Things are setting up for what Raoul Pal believes will be the best six- to nine-month trade in the history of financial markets! Ethereum’s supply has fallen dramatically and its block sizes have become more variable. The network is massively outperforming Bitcoin’s at the same number of addresses. This supply shock combined with exponential demand means the set-up right now is superior to Bitcoin’s in March 2020; make sure you have enough ETH, the rocket ship has taken off and you are not long enough.

Aussie golds spending their dollars

Australian gold companies are heavily reinvesting their cash surpluses. This increased investment indicates companies are becoming more confident in higher prices for the long-term, backed by unleveraged balance sheets. BUY rated Evolution Mining (target $4.80) is expected to reinvest ~US$400/oz in major/growth capital over FY22-FY24E. Northern Star Resources is looking at reinvesting ~US$195/oz but remains the preferred BUY rated Aussie gold with a target price of $14.00.

Gold reserves have fallen, but it's enough to support output going forward

Philip Newman comments that combined gold reserves at almost 400 primary gold projects, covered in Metals Focus’ Gold Mine Cost Service, fell by 10% in the last five years. Despite record high prices in 2020 and increased production, it is clear that exploration at the mines and resource upgrades have been unable to outpace reserve depletion. Nevertheless, Philip estimates that reserves at these operations are enough to support output for another 11 years, and converting current resources successfully could support for an additional 14 years.