Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

UK Alternative Network Providers

Further signs of an over-heated sub-sector - Axione (the French fibre JV between Bouygues and Mirova) has announced plans to build FTTP to 4m premises in the UK in sub-urban and rural areas. New Street believes the company is entering an increasingly crowded UK FTTP market (estimates there is already c.15% overlap among the altnets today); argues the economics looks very challenging and consolidation among the players is long overdue if they are ever going to improve their returns and stop competing against each other, as well as Virgin and BT.

Holland Advisors

A forgotten and neglected share - few investors take the company seriously and fewer properly think through its market position and what it could become/the profits it could produce. Andrew Hollingworth discusses the margin recovery story underway and why he believes the price of the employee earn-out (£10.00) and Mike Murray’s new incentive (£15.00 in just 4-yrs) are realistic targets despite the startling difference when compared to today’s share price of 680p. FRAS remains a high conviction Buy.

Nova Ljubljanska Banka (NLBR SV) El Salvador

This innovative bank is evolving into a south-eastern European powerhouse, commanding a potent market share in the six countries where it is active. A FV of 8%, a PBV of 0.65x, an Earnings Yield of 25.9%, a Dividend Yield of 1.8% and a Total Return Ratio of 3.9x catch the eye for a value investor. NLB commands strong fundamental momentum and value-quality attributes, plus a technical tailwind, and is one of Paul Hollingworth’s preferred financial entities in Europe.

TKH Group (TWEKA NA) Netherlands

Recovery much faster and stronger than anticipated for this telecom, building and industrial solutions company - the operational leverage, the focus on high-margin products and services and the still to be realised cost savings will enable TKH to achieve an EBITA margin of at least 15% in the medium-term. Share buybacks are also expected to become a regular part of the company’s capital allocation (focus on organic growth will leave much of its FCF unused). Valuation multiples are undemanding and offer ample room for share price appreciation.

Technicolor (TCH FP) France

Hollywood Magic Maker - major restructuring last year has resulted in a significantly improved performance. The disposal of the remaining legacy units will result in a “new and lean” business. Demand for its Connected Home broadband boxes as well as its Creative Studios VFX technology will continue to grow rapidly. As the world’s largest player in visual effects for the movie industry, TCH is set to benefit from a resumption of activity in Hollywood studios. TP €5.00 (67% upside).

North America

One of Nutstuff’s “sleeping gems” - stock could treble in the next year. VEON is absurdly cheap, trading on just $40 a sub and EV/EBITDA of 2.5x. Will Nutting considers it to be a great EM proxy and it benefits from Russian Rouble (20% undervalued vs. oil) and other EM currency reflation. Demand for EM telco data services is exploding and with Capex to Sales back up to 25%, organic growth is set to accelerate. VEON can grow underlying EBITDA 5-10% p.a. and pay 20-30c in dividend. TP $6 doesn’t take into account the tower spin-off / market waking up to the JazzCash opportunity.

Violating the rules of Retail Fight Club - the more time Stacey Widlitz spends at REAL stores the more she is convinced luxury goods players will take back the second-hand market (not only to capture revenues but also to control brand pricing and image). Stacey uncovers authentication issues (despite claims of a month-long process involving three layers of ‘experts’), poor customer service and inadequate training of staff.

The Battle vs. The War - ballooning freight costs may have obliterated DLTR this year, but the real call is on breaking the buck. Looking towards 2022, Brian McGough argues that DLTR has one of the best earnings setups in all of retail. The Street is underestimating TAIL earnings power and the impact of breaking the buck by over 40%. Meanwhile, management is wisely deploying capital with accelerated buybacks at these temporarily depressed EPS/stock levels. TP $200 (>100% upside).

The stock should experience high volatility when the US Court of Appeals for the Federal Circuit issues its Decisions in Case Numbers: 20-1933 and 20-1673. These Decisions are significantly overdue. MDC Financial Research have been following these Cases closely and believe that there is a greater than 50% chance that this will go in favour of BIIB for its Tecfidera product. If correct, could add ~50 points to the current share price (~15% upside) vs. minimal downside.

Specialised infrastructure distributor capitalising on multiple secular trends, including the domino effects from a post-Covid population shift (driving residential, non-residential and municipal demand) and growing environmental factors driven by climate change. CNM commands a 14% market share in a fragmented market ripe for consolidation. Multiple levers for top line, margin growth and strong cash flows = a winning combination. 12-month TP $37.00 (30% upside).

Valuation anomaly - priced for permanent profit decline despite being aligned with favourable market trends and positioned to grow profits over the long term. New Constructs’ reverse DCF model shows the stock is worth $411/share today (75% upside) based on CMI growing NOPAT by 6% compounded annually over the next decade (NOPAT has grown by 8% compounded annually over the past five years). Should CMI grow profits closer to historical levels, the upside in the stock is even greater.

Investor enthusiasm unwarranted, price rises will be unable to offset cost pressure - the price hike will only help 15 days in 3Q and BTN believes commodity inflation has worsened since the price increase was announced. SEE’s easy comps are over and the company will miss guidance this quarter. The stock remains a high conviction Short idea with an EQ (Earnings Quality) rating of 2 (Weak) - indicating that results have benefitted materially from aggressive accounting.

Blueshift Research

Has ESTC found the right formula to stand out from the competition in search, security, and observability? Source feedback was far more negative than in Blueshift’s previous report, especially around the threat from Amazon. One source even suggested it would be “game over” for ESTC if AMZN offers a fully managed version of its forked Elasticsearch service. ESTC’s recent license model change (aimed at preventing AMZN from reselling its product) is unlikely to have much impact.

One of those rare hardware-centric companies that is putting up software like growth numbers but is still trading with a hardware multiple - PSTG can return to 20% revenue growth as the pandemic abates and as subscription sales accelerate Srini Nandury expects the stock to continue its recent re-rating (+30% in last 2 weeks). Its investment in addressing enterprise workloads will pay off as many customers are looking to wean themselves away from Dell/EMC complex. FlashArray//C to continue to be its fastest-growing product.

Australia

Unregulated, efficient, undervalued with an improving Asian driven passenger mix - SYD has the highest EBITDA margins in Insight’s airport universe (81.5% in 2019). Following 1H21 results, Robert Crimes updates his long-term model forecasts (beyond 2030) and believes the recently proposed offer by an IFM led consortium to be highly opportunistic (it was rejected by management) - the A$8.45/share offer represents a 42% discount to Insight’s target price.

Emerging Markets

IPO Equity Research: Aequitas’ impressive 74% hit rate

Aequitas is a leading ECM research firm with a focus on IPOs and placements across the Asia Pacific. Since 2015, they have covered 600+ IPOs and 750+ placements with an accuracy rate of 74% and 67% respectively. Recent coverage includes:

Helen’s Intl (IPO Hong Kong) - Selling cheap drinks but at an expensive valuation.

Simplex Holdings (Pre-IPO Japan) - Steady top line growth but appears to be at peak margins.

Aditya Birla Sun Life AMC (Pre-IPO India) - Strong profit growth but losing market share.

Propitious Research

Tencent (700 HK) Hong Kong

Wium Malan estimates that the current fair market value of Tencent's listed associates has recently declined by a whopping 26% (RMB378bn). Given that Tencent already faces very tough comps from its online gaming revenue segment, not to mention uncertainty around the Chinese regulatory environment, Wium expects a significant earnings miss in 3Q21 reported numbers. On a more positive note, its consolidated operations currently trade on only a 12.1x NTM PE ratio, which offers an extremely attractive longer-term entry point given NOPAT is expected to grow at mid-teens levels from next year onwards.

GlobalWafers (6488 TT) Taiwan

Top runner on the brownfield track - set to benefit from lighter brownfield capex intensity (one-third lower than greenfield) and stronger 12” ASP momentum. NDR’s analysis shows that industry ASPs would need to grow ~40% by 2024e from 2020 levels for greenfield projects to achieve an EBIT of 20% for wafer makers, providing a key advantage to GlobalWafers who can continue to run on the brownfield for 2.5 years. Initiates coverage with a Buy-rating and TP of NT$963.

RedTech Advisors

Although this Chinese company dominates the online market for connecting independent truckers with shippers, early leadership belies the many challenges it faces. FTA's initial success may prove fleeting and with greater regulatory scrutiny it will need to compete on the strength of its offerings going forward. Truckers and brokers clearly want options and with new competitors on FTA’s home turf as well as in new markets, it risks being outflanked and overtaken.

Ming Yuan Cloud (909 HK) Hong Kong

A digital transformation in the Chinese real estate industry is inevitable and this property technology firm is ideally placed to benefit - huge opportunity given the penetration rate of software solutions is currently less than 0.1%. Real estate developers are willing to spend on digital products to help improve sales and management. New product launches will increase ARPU and the emerging demand from state-owned enterprises also provides an additional avenue for growth.

China Fall: Gap to US largest in history

Global Funds Positioning Analysis - allocations in China & HK among Global active managers have fallen to below pre-2017 levels. This allocation drop is in stark contrast to what is occurring in the US, with allocations powering to all-time highs. If Global managers are to increase weights in China, Steven Copley believes they will have to broaden their investment horizons. He compares Global stock holdings in China with their GEM peers - the rapid rise in investment by GEM Funds in Ping An Insurance, Meituan and JD.com suggests they can take a greater share in Global Fund portfolios in the future.

Macro Research

Developed Markets

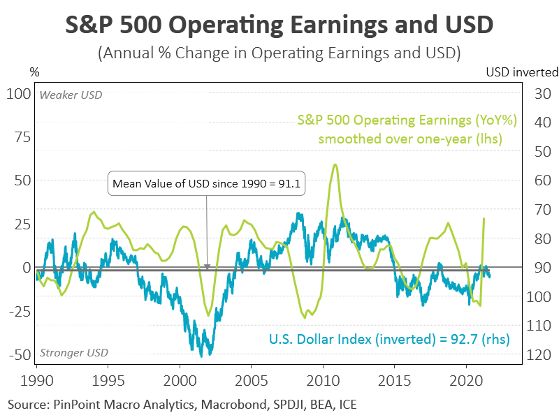

Chart of the fortnight: USD to rise, S&P500 earnings to fall

The depreciation of USD played a helpful part in lifting S&P500 operating earnings to their highest annual growth in a decade in H1/2021. Looking forward, the USD is close to its four-decade average and will modestly appreciate as the Fed commences tapering. Richard Grace believes the positive impact the USD played on S&P500 earnings won’t be sustained, and we will see a lower average rate of growth in S&P500 earnings throughout 2021.

Is a collapse in the US economy imminent?

Jeff Christian discusses the state of the US economy - he addresses the real concerns we face and contrasts economic realities with the constant warnings of imminent economic collapse. Watch here.

MRB Partners

US: Beware the Fiscal Cliffers!

Concerns that the US is approaching a fiscal cliff are misplaced. Fiscal policy won’t be a drag in 2022 and will in fact still be providing stimulus to the economy. It’s crucial to note that government transfers to the private sector are not directly counted in GDP, but rather only when the funds are actually spent. The huge pool of household savings sitting in cash will be spent over time as consumers feel more confident and spur greater investment and consumption with a long lag.

Macro Intelligence 2 Partners

US: Don’t be fooled by Powell’s platitudes

Powell’s Friday speech was greeted with predictable jubilation in risk markets, but Julian Brigden claims that equities have overlooked the fact that the balance sheet is also a significant and much more imminent threat to lofty valuations than interest rates. If anything, signalling further hike delays increases the odds of the Fed needing to taper PDQ to arrest economic trends. There’s also the fact that, as credible as Chair Powell is, the Fed is trying to run it hot, and his job is to play it down regardless of the economic reality.

Llewellyn Consulting

The 3 R’s: Recovery, Relocation and Resilience

In the face of rapidly changing supply and demand, structural policies are more crucial now than ever before. In Preston Llewellyn’s latest report, he ranks countries’ supply-side policies. Key takeaways include Denmark coming on top with Finland and Sweden in the top ten; Japan being the one economy that is consistently in the top 10; and, surprisingly, the UK coming in second place, largely due to its strong showing in product market regulation.

Forefront Advisers

Uncertainties about the formation of the next German government

The upcoming coalition government talks will prove more complex than ever with a deal possibly taking months to secure. In an unprecedented situation, we will see all of the real kingmakers – the parties needed for all plausible coalitions – hold talks with all potential partners, but internal struggles pose a looming threat to some deals being made.

Is the Bank of Japan being overwhelmed?

Only six months ago it appeared that the BoJ was set to allow yields to rise in the economy. However, yields have recently declined despite a sharp slowdown in the Bank’s purchases of bonds. It seems that the BoJ may be struggling to hold yields up, even as monetary growth decelerates. Andrew Hunt believes the excessive levels of global liquidity / weakness in the economy – and perhaps that in the PRC – is beginning to overwhelm even the BoJ’s ability to influence domestic markets.

Emerging Markets

Totem Macro

The EM earnings boom

EM commodity producers are now seeing the strongest earnings revisions in the world. This earnings outperformance is the beginning of a reversal of the last cycle’s trends, and Whitney Baker sees it being sustainable. The growth ripple from commodity windfalls is only just starting; as the income surge swirls around economies, a self-reinforcing, income-driven boom will come about. Right now, Chile and Turkey are among those with the strongest disconnect between valuations and earnings strength. Investors should get in before the stock markets catch up!

Buy Chinese equities, short Chinese government bonds

Deep Macro’s Turning Points Trade Tool superimposes phase angles of market conditions on top of the macroeconomic state in order to effectively screen for high conviction macroeconomic transitions and trades. Their latest recommendation is to go LONG China equity via the Shanghai SE Composite Index, since cyclical trends and inevitable policy measures will bring about a market rally, and to short China’s govt bonds. To play it right, investors should offset with short NZDUSD and short UK equity which are not normally pro-cyclical trades.

China: Make more babies

Hedgeye has often argued that China is inevitably going to move further away from family limitations and toward pronatalism. Beijing’s recent policies confirm this. Its new baby boost policies, including child tax credits, as well as an end to fines for families who have too many children are all part of its strategy to reverse the country’s falling fertility rate. China is pinning its future on its new, more relaxed approach to larger families. That’s good, because it’s needed.

Chile: Hawkish bias is reinforced

The BCCh hiked rates 75bp on Tuesday, which came along with a hawkish statement in its September Monetary Policy Report where they pledged to hike rates to their neutral level by mid-2022. Marcos Buscaglia comments how much more hawkish the BCCh is compared to the consensus, as shown in the chart.

India: Robust GDP rebound faces challenges

Official data shows a record 20.1% yoy growth in April/June, a strong turnaround from the massive contraction in the second quarter of 2020. Nevertheless, don’t be too excited about the government’s claims of an imminent V-shaped recovery, Covid cases are ticking up and could bring on a third wave. With only 10% of the population vaccinated there is significant downside risk to the country’s near-term GDP growth.

Russia: Stable and steady

Persistent inflation has pushed the Russian central bank (CBR) into a sharp tightening schedule. The CBR has increased rates 225 basis points since March, and Niall Ferguson expects more hikes to come as 6.5% yoy price growth inflation prompts CBR Governor Elvira Nabiullina to worry about what she describes as a potential “inflationary spiral”. Niall is bullish oil prices and he sees few political risks to the ruble ahead—all of which make Russian assets attractive.

Venezuela: Opposition to participate in November elections

Venezuela’s main opposition parties, the umbrella opposition coalition (MUD), announced that they will not boycott the regional and municipal elections in November. Patrick de Courcy sees this is as an implicit recognition that opposition leader Juan Guaidó’s maximum pressure strategy of boycotts and sanctions, with the aim of securing free and fair elections, has failed. Instead, MUD will put their faith into the ongoing dialogue process with Mexico and President Maduro’s administration, but things don’t look promising.

Commodities

Wake up and smell the coffee!

Greg Shore comments on the commodity investors and traders who have suffered as a result of markets trading sideways for the past four months. At some point in time, commodity markets will break out strongly higher or lower, but for now, these markets require strong nerves and lots of coffee. Coffee, in point of fact, has been the only sure thing in the commodity world since freakish freezing temperatures wiped out a large chunk of Brazil's coffee crops in early July. Greg still sees plenty of upside here for both Arabica (+25% since 10 July) and Robusta (+15% since 10 July).

When should energy portfolios be trimmed during an oil price boom?

David Ranson's latest report explains how energy-stock returns no longer respond to growth and inflation that has already occurred. To anticipate the performance of energy stocks, extremely early leading indicators are required. Two market signals can do the job: the price of gold and credit-spread movements. Both of these leading indicators rose several months ago, and gains were realised, but the time has now passed and the energy sector is no longer attractive.

Global Macro Investor

Solama, the new darling of crypto?

Raoul Pal has very high hopes for Solama (SOL). Not only is its new ETH-style blockchain very fast and very cheap, but its ecosystem is incredibly expansive for a crypto that emerged only in 2020! Although Raoul considers Ethereum the highest quality trade right now, he predicts SOL to soar 18x going ahead.

Responding to extreme weather events

The Jackson Hole speech offered some support for many commodities, but at the end of the day, Kathleen Kelley claims that numerous commodity sectors are moving on good old-fashioned weather rather than macro factors. Now that most of the world has been subject to extreme weather events, the next big question for energy and oil is how many storms will plow through the gulf and what impact it will have. Ultimately, Kathleen believes that you can bet it’ll be supportive for energy prices.

A high conviction trade despite risks in Kurdistan

DNO is the latest to feature in Black Robin Group’s new series of High Conviction trades. Despite the risks stemming from its Kurdistan-based operations, the Norwegian exploration and production company has a solid operation and sound metrics. Management has a proven track record in managing the company and fulfilling their obligations to creditors. The company should also appeal to ESG investors too meeting carbon standards, and bringing social stability to the Kurdish region.