Company & Sector Research

General

Insight Investment Research

The Arbitrage Between Unlisted & Listed Infrastructure Assets

Transaction volumes have risen from €20bn p.a. in 2019-20 to €58bn in 2021, with acquirers preying on listed assets, such as ASPI, Sydney Airport, OMA and IRB. Having reviewed the 109 largest deals (2015-21), Robert Crimes reveals transportation infrastructure listed valuations are at c.30% discounts to transactions based relative to Insight’s NAV.s (set by DCF.s) and share prices need to rise c.40% to close the valuation gap. His top picks (combining undervaluation and probability of a takeover) are Inwit, Getlink, Aleatica and Ferrovial.

Europe

MYST Advisors

Now trades at a meaningful discount to peers despite dominant position in ALL its major markets - this has been caused by negative, but “fundamentally meaningless” headlines over the last few months. Another issue is that US investors are still not familiar with the company despite FLTR’s US revenues being 50% higher than the No.2 player (its US segment’s implied valuation is just 3.5x FY23 EV / Sales vs. 8x for DraftKings). A spin-out of FanDuel (possibly in 1H22) should provide a catalyst to crystallise the company’s SOTP value; or given the ongoing consolidation in the online gambling space, could Disney be lining up a takeover? TP £200 (80% upside).

Forensic Alpha

The market still does not grasp the full extent of the turnaround currently underway - hidden value in the Partnership Housing division has been overlooked due to historical problems. This has led to a dramatic underperformance vs. Countryside and Vistry. However, deep-seated actions taken by management have now taken root which will result in an extended period of rapid growth and expanding margins. While its construction business provides a stable cash cow, Partnership Housing will become the most profitable division in the group by FY25. TP £38.00 (60% upside).

TobaccoIntelligence

European heated tobacco trials show promising signs - IMB said that the ongoing trials of its Pulze heated tobacco device and iD consumables in the Czech Republic and Greece were progressing well despite a global decrease in net revenues for the category in 2021. While net revenue for IMB’s smoke-free portfolio fell by 3.9%, this was due to the company's exit from several markets, including Japan and Russia, and the refocus of the category in line with its revised strategy.

Galliano's Financials Research

Garanti acquisition a shrewd move despite negative market reaction - BBVA’s offer to buy out the Garanti minorities values the Turkish bank at a PTBV ratio of 0.7x and prospective PE of 3.6x and is expected to be earnings accretive. The Spanish lender has plenty of experience in delivering premium returns from its operations in challenging neighbourhoods and by taking greater control will be able to further implement the group’s digital strategy and consolidate its risk management. BBVA shares are also supported by the prospect of share buybacks equivalent to ~10% of its market value.

NF Forensics

Share price tanks on disappointing 3Q21 figures - has now fallen 40% since Paul Nagy’s report in early Oct’21. Paul highlighted increased investment in working capital, particularly receivables, that has led to lower CFFO while adjusted EBTIDA has continued to increase. In addition, FCF has been consistently negative. Paul also noted that the pace of acquisitions has increased materially since 2019, raising concerns over integration risk, especially since the market value of BICO implied substantial revenue growth expectations from these acquisitions.

North America

Boon For Commercial Satellite Industry From US Military’s “Pivot to LEO”

The US Space Development Agency (SDA) is launching satellite services that will stimulate the commercial industry, according to leading Space sector analysts, Quilty Analytics. The 60-page briefing summarises the SDA’s plan, highlights sector developments and constellation updates for Amazon, OneWeb, SES, SpaceX and Telesat, and offers in-depth analysis on topics including space sustainability, Viasat/Inmarsat acquisition, and GEO satellite launches.

Gordon Haskett Research Advisors

Regaining its mojo - shares surge on Q3 earnings beat / decision to hire AlixPartners to review business. Looking ahead to 2022, Chuck Grom believes Macy’s can strongly build off its successful 2021 campaign, GPM in the high 30’s looks sustainable, and is excited about the launch of a curated 3P digital marketplace. The company’s more concerted effort to unlock value and overall improved margin / capital disciple now warrant a higher multiple than Chuck has been willing to underwrite in the past. He is modelling FY21 EPS of $4.73 (but sees upside well north of $5.00) and FY22 EPS of $4.75. TP $50.00 (55% upside).

R5 Capital

Widespread store execution and distribution challenges - Scott Mushkin downgrades the stock to Sell. He estimates that 10-15% of the store base is experiencing issues receiving consumable products, which make up over 75% of total company sales. Scott's store visits regularly found shelves to be empty, and while a lack of truck drivers is a key factor, warehouse and store staffing levels also remain suboptimal. Labour constraints along with building material scarcity will hamper store growth over at least the next several quarters. With DG’s core customer already struggling to deal with rapidly increasing costs of everyday items, Street estimates are too high.

Badger Consultants

Another well-timed short from Tom Chanos - having initiated coverage at $157 (Jun 21), the shares are currently languishing at $93. Tom describes NVRO as a one product company, who's product doesn't work! The whole premise that the Omnia is something new and exciting is laughable and smacks of a company in desperation mode. Competition (including a new, superior device from Saluda), pricing wars, takeover prospects (or lack of!) and insurers cracking down on approvals are all covered in Tom’s 45-page report.

AlphaSituations

The Great Break Up - splitting GE into 3 independent, unconnected companies makes strategic sense and should unlock meaningful value for its shareholders. Based on 2023 estimates, Robert Sassoon’s analysis indicates a SOTP value for GE of ~$152 (50% upside). Despite the extended break-up execution timeline (Healthcare by 2023 and Renewable Energy & Power business by 2024), Robert makes a compelling case for investors to use the current share price lull to jump in and enjoy the catalyst-driven ride.

US Environmental Protection Agency opens faucet to additional water growth - recent announcements by the EPA gives Alembic increased confidence that the ChartWater business is poised to see significant growth (even before accounting for the recently passed infrastructure bill). GTLS remains an unrecognised player in the water purity market and offers investors a unique opportunity to benefit from what analysts at Alembic see as a decade-plus global investment surge in the water treatment industry.

Smart Insider

Spun-out from International Paper Company last month, John Sims (CFO) and Gregory Gibson (Senior VP) have wasted no time in materially boosting their stakes - John Sims purchased $646,000 of stock at $30.46, increasing his holding by 44%. He previously made six non-option sells of IPC in the four years prior to the spin-out and never made a purchase. Gregory Gibson purchased $574,000 of stock on the same day, increasing his holding by 80%. These large purchases shortly after the spin-out are very encouraging. Stock Ranking +1 (highest rating).

Atlantic Equity Research

This damning 30-page report by Joe Gagan argues that PTC's management have made multiple material misstatements about their business - Joe argues that investors have been misled about the market acceptance and capabilities of its growth products and management have used the change to a new revenue recognition rule and the change to a new subscription billing method to cover up its real results. He sees similarities to recent cases brought by the SEC against Theranos, Nikola and Under Armour. TP $49 (50%+ downside).

Japan

LightStream Research

Revving up the hydrogen engine - in keeping with its penchant for developing every type of technology imaginable, Toyota has been working on not just fuel cells but also hydrogen engines. Now it is partnering with Mazda, Subaru, Yamaha and KHI to further expand on this concept and add synthetic carbon neutral fuels to the mix. These efforts could provide alternative zero carbon transition paths and are worth understanding, especially since EVs and renewables are nowhere near as mature for mass adoption as is generally portrayed.

Asymmetric Advisors

100% global share in a chemical that enhances chip package adhesiveness - MEC is certain to benefit from the coming capacity expansion in chip production. The surface area that these chemicals go on will increase with new chip stacking architecture. These updated chip packages will also increasingly use MEC’s newer generation chemical, thus improving sales mix. The fact that package maker IBIDEN predicts sales to double by 2026 further supports the positive outlook.

Emerging Markets

Propitious Research

Short-term headwinds, cash flow concerns, and a premium valuation - Wium Malan expects further earnings downgrades, driven by overly optimistic profitability (margin) expectations from the sell-side. He has concerns around Xinyi’s aggressive capacity expansion programme over the next 18 months and believes ASP’s will remain under pressure. The company's current valuation leaves no margin-of-safety, especially considering its poor historical FCF generation track record and working capital issues (highlights a staggering increase in receivables days).

Creative Portfolios

Korea's leading financial services provider boasts an impressive PH Score™ of 8.8 (top quartile globally from 2000+ banks). This is a solid, diversified, franchise, that offers enhanced capital returns at an attractive valuation - FV of 6%, PBV of 0.5x, Earnings Yield of 19.8%, Dividend Yield of 2.9%, and a Total Return Ratio of 2.2x. KB’s Q321 results highlight improvements in profitability, NIM/Spread, efficiency, provisioning, and headline asset quality. In addition to its stake in Kakao Bank, KB offers exciting growth opportunities with its new digital platform, super app ‘KB Star Banking’.

Horizon Insights

China E-commerce Q3 Local Surveys: Industry Competition Has Intensified

Horizon Insights' quarterly surveys pointed out that traditional e-commerce lost share due to increased competition.

Live-stream e-commerce continues to evolve. Douyin and Kuaishou have different business models, both have high GMV growth. More brands are establishing relationships with different hosts, using livestreaming as an online ”distribution channel” to gain sales volume. Kuaishou predominantly focused on influencer live-stream; this model has strong stickiness and high conversion. Horizon Insights believes Kuaishou's model will generate larger sales volume in the future.

In the community group buying space, top three players have emerged: PDD, Meituan & Alibaba.

Niko Partners

Cuts Forecast For China’s Video Game Market - First Time Ever!

Several factors including strict regulations on young gamers and a temporary freeze on game approvals, sees Niko Partners lower their forecast for the first in their 20-year history - they now expect China’s market to generate $47bn in 2021 (down $460m from previous estimate). The Asia games market specialists have also recently produced a Mobile PaaS Cloud Gaming white paper (this technology has the potential to dramatically impact the mobile and F2P games market); provided insight on how Chinese tech and gaming giants are embracing the metaverse despite state warnings; and why Roblox’s China ambitions risk falling flat.

Macro Research

Developed Markets

Longview Economics

Here comes the boom?

The US and global economy is at the early stages of an economic cycle. Harry Colvin postulates that once pent-up demand is released, we will experience a boom, supporting the case for an upward trend in bond yields and global equities. Whilst inflation remains a key risk, we are still in the early stages of the liquidity cycle and the environment will remain supportive of risk assets in the next 6-12 months.

RW Advisory

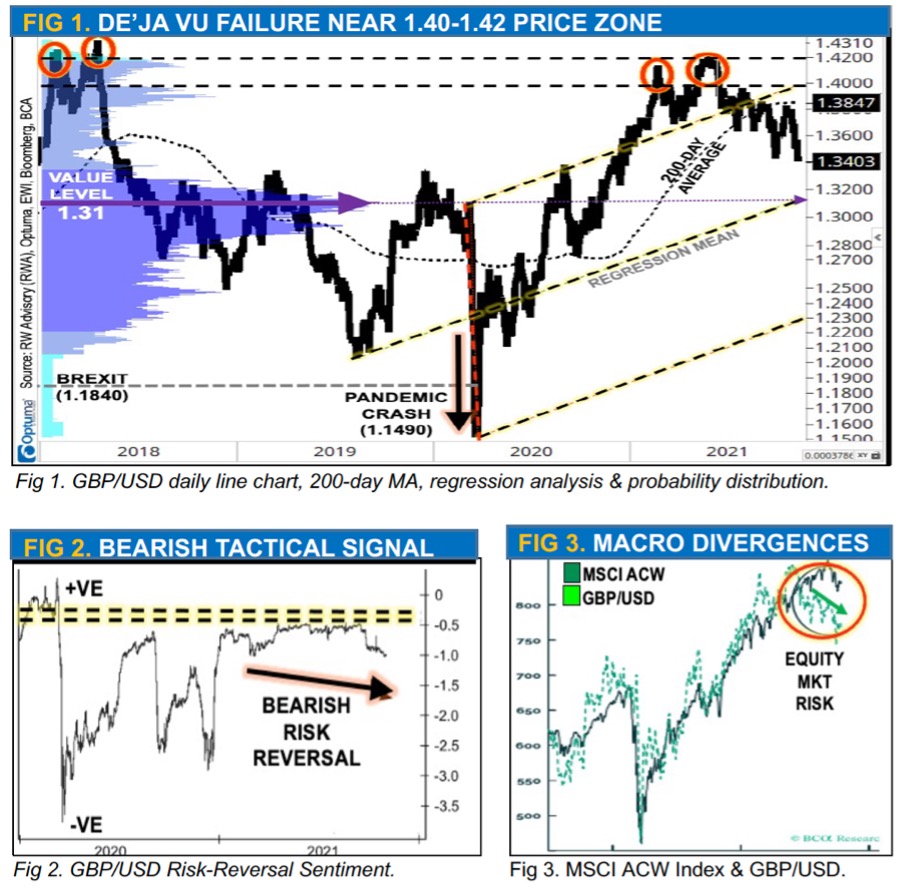

Chart of the fortnight: GBP asymmetric risk

Ron William discusses a GBP/USD asymmetric risk. He notes similar bearish sentiment to the 2018 peak after the Brexit crash lows of 1.1840 (fig 1). Headwinds are also growing, and Ron’s risk-reversal sentiment is turning negative (fig 2). There is also a risk of a correction in global equity markets, which Ron predicts, pressuring the divergent trend lower (fig 3). On GBP/EUR matters, a price move above €1.19 signals a resumption of the upward trend into an important make-or-break zone near €1.2080/90. A sustained rise would confirm a momentous breakout, targeting higher altitudes into €1.32.

Andrew Hunt Economics

Germany is already slowing

Andrew Hunt has long been commenting on Germany’s weakening competitiveness and poor demographic situation, and both structural issues remain. He also notes that cyclical trends are weakening, especially vis-à-vis exports. Moreover, household real income trends are weak, and mobility is being reduced by a fourth Covid-19 wave, which will steepen the winter decline as lockdown sets in.

Greenmantle

Germany’s coalition will drive forward Eurozone changes

Germany’s first three-way coalition will have significant implications for Eurozone policy going forward, according to Niall Ferguson. It signals a much more accommodative position that could lead to real advances in stabilising the Eurozone. Niall also sees Europe having a structurally less constraining fiscal future, stabilising the currency union, and that markets should expect a weakening of the ECB’s hawkish camp.

Talking Heads Macro

Where to be short into the December Fed

Manoj Pradhan reveals a number of strong risk-reward and asymmetric payoff trades to play into December. Key takeaways include short US Fed funds futures for Apr 22 and Dec 23; Italy’s spreads set to widen, especially to France; Sweden 1y1y since a serious inflation uptick is due; LONG oil plays as a hedge should the Fed turn out to be insufficiently hawkish.

Macro Hedge Advisors

US: Powell’s renomination, a brilliant stroke of monetary Machiavellianism

Chief Powell has been a failure. Two scenarios lay ahead: a further build-up of CPI inflation, or a sudden transformation of asset inflation into asset deflation, meaning a crash and a recession. The market’s response to view Powell’s renomination as a hard money signal is nonsensical, it is simply a move by Biden to deflect blame to the Republicans should anything go awry.

Musha Research

A global shift towards Japanese stocks

In the face of US supply constraints and mild inflation, and the shift from tech stocks to value stocks, the outlook for Japanese stocks is positive. High carbon energy prices will also benefit Japanese trading company valuations which own many resource interests. Concerns over Japan’s laggard behaviour in renewables are not unfounded, but in the era of coexistence of carbon and green energy, Ryoji Musha sees no shortage of business opportunities!

Emerging Markets

Topdown Charts

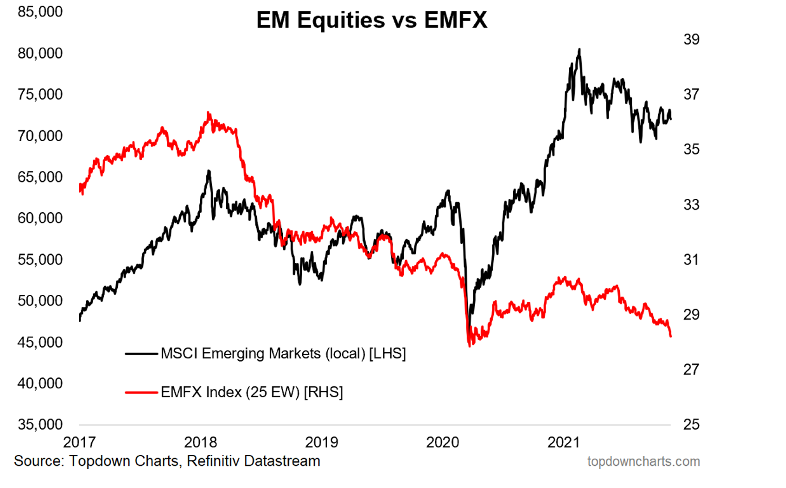

EMFX weakness could spill over to equity prices

Callum Thomas’s equal weighted 25-currency EM index continues on its declining trend. Even excepting TRY, the weakness is widespread, and if the current short-term persists we could see new all-time lows soon. Such trends in EMFX have often precipitated bouts of weakness in EM equities. Callum’s EM country breadth and sentiment indicators don’t look too comforting either, so Callum advises investors to keep a short-term risk watch on EM equities.

Macrolens

China’s slow-mo implosion

The Chinese economy is crashing, claims Brian McCarthy. Notions of a “transformation to a consumption-led economy” are utter fantasy. The RMB has hitherto benefitted from numerous tailwinds that appear set to reverse. Tie this in with a macroeconomic Ponzi scheme in the tens of trillions of dollars that is gradually unwinding, and the outlook is so dire markets can’t bear to look. Brian can’t fathom out what the official plan is: Xi Jinping is simply bad at economics, and potentially mad.

High Frequency Economics

China: Political egalitarianism

Last week’s Central Committee of the CPC concluded with a paper on the merits on the even and equitable distribution of the proceeds of economic activity. This validated President Xi’s campaign to level out some of China’s billionaires and their companies. Don’t be fooled by this apparent act of egalitarianism; as Carl Weinberg sees it, it is Xi’s get-out-of-jail free card in his quest for re-election. If the pie is not growing, shift the goalposts to income distribution.

MRB Partners

Waiting for the China bounce

Strong stimulus, EM monetary tightening and a regulatory onslaught in China have undermined EM equity performance this year. However, the tide will soon turn in China and we will see both China and EM outperformance in the year ahead. Stay overweight EM in a global equity portfolio but with a potential bias to downgrade with preference towards China, followed by India, ASEAN and Mexico.

Alberdi Partners

LatAM: Timing of the peso devaluation is of the essence

The timing of peso’s devaluation is key to decide whether to invest in USD-linked bonds or CER-indexed ones, explains Marcos Buscaglia. Those with liabilities in pesos or USD at the official exchange rate should just hedge their assets with their liabilities and future payments. Marcos expects the Argentinian government to be forced to devalue in January and prefers DLK bonds maturing in 2022 rather than CER linked ones maturing at close dates.

Greenmantle

Media underestimating risks associated with Russia's military build-up

Niall Ferguson believes the media does not fully realise the risks of a new outbreak of large-scale fighting between Russia and Ukraine. Moscow is surely putting the pressure on Europe by supporting Belarus’s manufactured migrant crisis and Gazprom’s unwillingness to send additional gas to Europe, so the military build-up could be a bluff, but markets have insufficiently priced downside risks which have significant political and financial implications.

Totem Macro

Turkey’s Lira: A thanksgiving slaughter

The media has been quick to blame Lira’s recent plummet on Erdogan’s bellicose rhetoric, but Whitney Baker claims the move is gas-related. BOTAS (who the CBT sells FX to meet dollar demand to pay for gas) asked the CBT for help a week ago, and Whitney reckons they told them to get lost. With BOTAS/gas importers caught short here, they had no choice but to slam the market to get the dollars they needed. We’ll see a large TRY bounce in coming days with this being a one-off event.

ESG

Europe’s EV miracle doesn’t live up to the hype

Stories about electric vehicles surpassing diesel in Europe mean little on the global stage. Emerging markets aren’t obsessed about climate change to the degree that Europe is, and it is those nations that will dominate future vehicle sales, opting instead for cost-effective vehicles (gasoline, for now). Subsidies help, but they barely move the needle in these nations. TrendMacro reiterates that oil is nowhere near “peak demand” stemming from the ascendancy of EVs and that we are also not in a “super-cycle” headed for $100+.

New Street Research

ESG boosts European Telcos performance

Russell Waller wasn’t sure what to expect when researching the financial merits of ESG investing in the Telecoms sector, but in his latest report he found clear evidence of better TSR for Telco ESG leaders, that those with better Governance (no Government ownership) outperformed, and that ESG can help companies in the sector have lower borrowing costs. Russell shows how the stocks stack up on a variety of ESG ratings and identifies which ones should do well from the next wave of ESG money. His “Climate Champions” include Deutsche Telecom, Telefonica and KPN.

Curation Corp

The inconvenient truth about tree planting

Countries including China and the UK are embarking on new reforestation projects, but Nick Finegold warns that they are far from being a silver bullet for climate change. Existing projects have failed due to improper locations and maintenance, not to mention the resulting spread of foreign invasive species. Instead, existing forests should be given the highest priority before we even think of planting new trees, and better forest management should be at the forefront of our minds.

Commodities

Oxford Analytica

Oil reserves collaboration will fuel OPEC tensions

As November PMIs showed inflation persisting, several major economies agreed to release strategic oil reserves including the US, Japan, China, India and the UK. However, unlike previous occasions when oil reserves have been released to combat a specific supply shock, this is an attempt to signal to OPEC+ that they must increase output. At the Dec 1st OPEC+ meeting, the policy preferences of Russia and the Gulf states will diverge, and tensions will bubble.

Belkin Report

Gold and gold mining stocks are attractive

Higher inflation is the catalyst that gold prices have been waiting for and it’s time to act; Michael Belkin recommends LONG GDX gold stock and GLD gold ETFs. Michael also follows every investable gold/silver/platinum mining stock in the world and advises investors to stay away from Newmont or Barrick, which are underperforming the GDX. Instead, opt for mid-sized producers such as Kinross, SSR Mining or Eldorado Gold.

Independent Strategy

Metals: The new Princes of Power

The electrification of the planet in the face of declining fossil fuel usage will result in a massive increase in the metals that contain and conduct that power. Copper is king and David Roche is already long the red metal, but the new princes of power will be cobalt, lithium and rare earth minerals, which investors should take out LONG positions on. The era of fossil fuels is coming to an end, get prepared.