Company & Sector Research

General

Radio Free Mobile

TSMC’s massive $40bn+ capex plans has all the hallmarks of peak cycle

Robert Windsor believes history will repeat itself and that there will be a sharp downturn as new capacity comes online and demand moderates at the same time. The industry has a fundamental mismatch between supply which is lumpy (fabs) and demand which is smooth, and so, while the causes of every semiconductor cycle are different each time, the result is always the same. The sector has performed extremely well over the last 18 months, but some valuations look pretty stretched and the looming downturn threatens to unwind a lot of the gains.

Space-based Earth Observation industry projected to be $27bn market by 2025

The inaugural edition of Quilty Analytics’ Earth Observation & Geospatial Quarterly Briefing series is kicking off with a report on the space-based EO industry followed by a deep dive into the expanding Synthetic Aperture Radar (SAR) imaging sensor market and the $500m+ in new capital it has seen since 2019 from start-ups including Capella Space, Iceye, iQPS, Synspective, Predasar and Umbra.

Europe

Arete Research

Playing to the crowd - DHER has exited Japan and Germany and pledged to focus on reaching profits by 4Q22E. Arete believes management is looking to shore-up its equity value while eyeing its next acquisition target (Just Eat Takeaway would be Arete’s preferred choice). The stock is trading at its lowest multiple since IPO even though sales in 2H21 will be 4x higher than 1H20 and DHER is well positioned to sustain high growth (36% sales CAGR until ’25, 18% until ’30). TP €170 (+120% upside) based on blending a DCF until ’30 and a 10x ‘23E EV/Gross Profit multiple.

Forensic Alpha

Blowing through cash - while VWS has delivered impressive top line growth over the past two years, declining cash conversion has received far less attention. The extent of the problem has been masked by the significant increase in the use of supply chain finance since 2019. Management points the finger at elevated capex, though Forensic Alpha’s analysis shows that capex is not out of line with peers. Additionally, the rapid growth in contract assets for the services business may raise questions around the quality of earnings which the market is rating so highly.

Insight Investment Research

Entering the end game of 3 independent TowerCos in Europe

Robert Crimes’ 16-page report details how the European Towers market is to undergo a final phase of consolidation with several large transactions resulting in 3 dominant TowerCos - Cellnex, Vantage Towers and American Tower Europe. He notes that it is significantly more efficient for MNOs to share passive infrastructure while Tower transaction valuations have recently risen allowing MNOs to generate large capital releases to fund investment in 5G and de-lever balance sheets (potential to monetise a further €85bn of Tower assets in Europe). Robert’s preferred stock is Cellnex (well placed to continue to grow acquisitively, raise tenancy and returns); TP €106 (+145%).

US potential and pivot to electrification pure play offers 45%+ upside - Sustainable Investing are more bullish on US transmission & distribution (T&D) growth than consensus (sees the market doubling to $600bn in a decade - 2x size of EU). NEX's leverage to US is underappreciated - it is currently only 22% of revenue, but will be closer to 40% by 2025, driving a 33% increase in group EBIT. The group's pivot to electrification pure play via the disposal of telco and industrial cable and the HVDC acquisition also drives margin improvement. 30% valuation discount to peers; NEX should be worth 9x EV/EBITDA, in line with Prysmian.

North America

AlphaSituations

Plenty of value left on the table - why investors should play the pending Discovery / WarnerMedia merger through AT&T. Robert Sassoon’s conservative TP of $41 for Warner Bros. Discovery still offers 40%+ upside from the prevailing share prices of both DISCK/DISCA. However, with AT&T trading on an EV/Consensus 2023 EBITDA multiple of ~7x, and assuming AT&T ex-WM continues to be valued at a similar multiple, then purchasing AT&T shares now gives investors a ~65% cheaper option to purchase WBD shares than through DISCK.

Blueshift Research

Have Apple’s new privacy restrictions permanently damaged Snapchat’s ad business? AAPL’s new anti-tracking restrictions represent more of a short-term headache than any permanent degradation of SNAP's ad value, according to Blueshift’s interviews with advertisers, agencies and other industry specialists. However, perception of SNAP as an ad vehicle skewed negative, with sources citing a lack of innovation, slow movement on e-commerce tools and a continued perception of Snapchat as a messaging app.

R5 Capital

Don’t be put off by daunting 1H22 comps - Scott Mushkin sees several positives coming together for the company over the next 12-24 months that ultimately have the potential to accelerate revenue growth over the next several years. Initiatives around optimising the store base / experience and its new Totaltech membership will collide with a powerful technology innovation cycle that will touch almost every category in the store. BBY is in a unique position to capitalise and grow market share given its omnichannel capabilities, superior / knowledgeable employee base, national footprint and importance to consumer electronic vendors. TP $140 (40% upside).

Gordon Haskett Research Advisors

Trading at ~6x 2023E EBITDA (20% discount vs. pre-Covid), Jeff Farmer views PLAY shares as increasingly compelling given: 1) Recapture of pre-Covid sales volumes. 2) Far less exposed to commodity price / wage rate inflation than a traditional restaurant business model. 3) Top line catalysts from a new CEO (e.g. more aggressive pursuit of traffic-driving strategies; increased sports viewing awareness; introduction of sports betting / partnerships; recently launched loyalty programme). TP $50 (40% upside).

For those interested in the wider restaurant sector, Jeff has also written a compelling report on the 10 dynamics that he sees having the greatest influence on share price performance in 1H22.

Paragon Intel

With renewed speculation that AUPH is a takeout target, Paragon’s JetTrack platform can help investors track potential acquirers - although Biogen is the rumoured potential buyer, Fulgent Genetics is the only healthcare company to have flown to AUPH’s HQ in Victoria in the last two years. They registered a 'New Location' flight on 30th Dec 2021 and this is the only flight the company has registered to Victoria in the history of Paragon’s data set (goes back to 2007). Investors can also track flight activity to the locations of AUPH’s facilities around the globe by setting up geographical triggers in the platform.

Abacus Research

Unappreciated quality - after splitting out Arconic, this critical component manufacturer is now a more focused, higher margin company. Capex is fading as volume increases and fixed-cost cuts during Covid look to be permanent giving high incremental FCF for the next 3-4 years. HWM trades at ~5% 2023 FCF yield and 13x 2022 EV/EBITDA, yet it will grow earnings ~30% annually from 2021-23. Abacus analysts see minimal downside even in their bearish scenario. TP $46 (35% upside).

ERA Research

4Q21 results will be boosted by the late-year pricing rally and following a remarkable start to the year 1Q22 is shaping up to be a blockbuster - lumber prices have rocketed higher over the past two months with supply interruptions (BC floods and Covid-related worker absences) a bigger driver than (steady, if unspectacular) demand. ERA continues to like IFP’s geographic diversity (and limited exposure to high-cost and freight-challenged BC) and its acquisition of EACOM strengthens this position further. TP increased to $55 (35%+ upside), based on a conservative 4.0x multiple applied to a 75/25 blend of 2022E/2023E EBITDA of $874m.

Gradient Analytics

Downside risk remains despite sell-off - Gradient’s main concerns include: 1) RNG operates in a highly and increasingly competitive industry. 2) Forward growth is dependent on continued success in transitioning legacy business comms. 3) Signs that RNG is drawing on contract sales at a faster rate than it has in the past. 4) Deferred compensation is becoming a rising headwind to margins. 5) Stock-based compensation is driving unsustainable cash-flow assumptions. A brief video introduction to Gradient’s report can be found here.

Sales Pulse Research

Channel contacts report further acceleration of spending on Cyber Security

High flying but volatile stocks like Zscaler and CrowdStrike are benefitting, but so are some less volatile vendors. Sales Pulse are seeing unexpected acceleration from…

Check Point (CHKP) - generates impressive cash flow but has lacked innovation and bled market share. Channels now see improvement in execution and benefit from spending by its massive installed base.

F5 (FFIV) - reaping the benefits of 3+ years of working on a broader security solution through organic development and acquisitions.

Tenable (TENB) - picking up a LOT of momentum based on the growing recognition by end users of the need to scan 100% of devices for vulnerabilities. This vendor is also the most direct beneficiary of efforts to address the Log4j vulnerability threat.

BWS Financial

Hamed Khorsand’s new “Top Pick” XPER is certainly worth a closer look given his previous choice (Verso) multi-bagged since upgrading the stock in Oct 2020. XPER offers multiple ways to grow revenue in the coming years, from AutoStage and AutoSense to hybrid bonding and content streaming intellectual property. Currently trading at ~10% FCF yield, XPER has been dedicating 50% of its FCF to debt reduction and the other 50% to returning cash to shareholders. As net debt continues to fall Hamed expects the stock to garner more investor attention this year.

Australia

Global Mining Research

Hermosa Taylor project value halves - GMR’s NPV for Taylor falls from US$1,120m to US$540m. Capex has increased from US$800m to US$1,700m with first production pushed back another year to FY27. The blowout for Taylor also draws into question market expectations for Ambler given harsher operating conditions in Alaska. S32 faces the difficulty of renewing most its asset base while trying to add or maintain value in a competitive world for M&A. While the shares offer exposure to alumina, met coal and manganese, GMR believes there are much better options elsewhere.

Emerging Markets

Aequitas Research

2022 Asia IPO pipeline

Aequitas are currently tracking 100+ companies that have filed for IPOs across Asia-Pacific and are likely to list in 2022. Hong Kong continues to be the market with the greatest number of pipeline deals, including Wanda Commercial Management (US$4bn) and Imeik Tech HK (US$3bn). In India, notable filings include Delhivery (US$980m) and API Holdings (US$843m), while the filing for the US$5bn+ LIC IPO is awaited. Elsewhere, the performance of LG Energy’s mega IPO (US$11bn) will set the stage for other large Korean IPOs.

Aequitas aims to cover all IPOs and placements with a minimum deal size of US$100m across Asia-Pacific (ex A-shares), including China ADRs. They ended 2021 with an accuracy rate of 72.4% across 127 IPOs covered and 73.1% across 141 placements.

Entext

Sean Maher adds Geely to his autonomous driving thematic basket which also includes Denso, Renesas and General Motors. Sean notes that Geely is planning a 2024 commercial Level 4 self-driving launch (much sooner than consensus expectations). He is seeking more China exposure this year - the country is starting to lead in automated deployment and local stocks have derated dramatically despite world class IP. On the big question re. whether Level 4+ autonomy needs Lidar - Sean would continue to bet on ‘belt and braces’ hardware redundancy winning and the Chinese crashing the cost of Lidar sensors as they scale up.

Galliano's Financials Research

Citi to sell its Mexican retail and SME banking operations - “new Banamex” is worth USD7-10bn according to Victor Galliano. Grupo Salinas owned Banco Azteca seems a strong candidate to make a bid, especially since Ricardo Salinas is close to the Lopez Obrador government. Carlos Slim’s Inbursa could also be a good fit. Both potential bidders are likely to attracted by the deposit rich nature of the Banamex franchise, as well as the capillarity of the branch network, even in these increasingly digital times.

Niko Partners

MENA emerges as a key growth region for the video game industry

Saudi Arabia, UAE and Egypt will have a combined 85.8m gamers (vs. 65.3m in 2021) generating $3.1bn in games revenue by 2025 (5-year CAGR of 13.8%) - growth will be driven by higher spending per user, additional government support (e.g. Saudi Arabia and UAE have introduced policies to encourage game localisation as well as hosting major esports tournaments) and more gamers entering the market. Nearly half of the MENA population is under 25 years old and have grown up as digital natives with gaming playing a huge role in their entertainment.

Macro Research

Developed Markets

Harlyn Research

Will value outperform growth?

Commentary on value > growth and a US to Europe rebalancing is rife, but Simon Goodfellow disagrees with such notions. Govt yield curves aren’t going to steepen dramatically as expected and there’s no reason to reduce tech exposure, nor increase financials exposure. Until the Fed commits to a policy of reducing its balance sheet as a % of GDP, hold off on the value/growth switch, but when the Fed does commit, Simon will be the first in line to do so.

What you're not hearing about why inflation is like Elon Musk in a biker bar

Conventional CPI, a weighted average, can be unduly influenced by a few outlier items or categories. Median CPI, using the same constituents, is far lower, showing today's inflation is not broadly based. Monetary policy errors lead to broad-based inflation by debasing the currency in which all items are priced. This is the highest inflation in 39 years, it is also the greatest divergence between average and median CPI in 39 years. Unless inflation is broad based, it will be transitory. Click here

Ekins Guinness

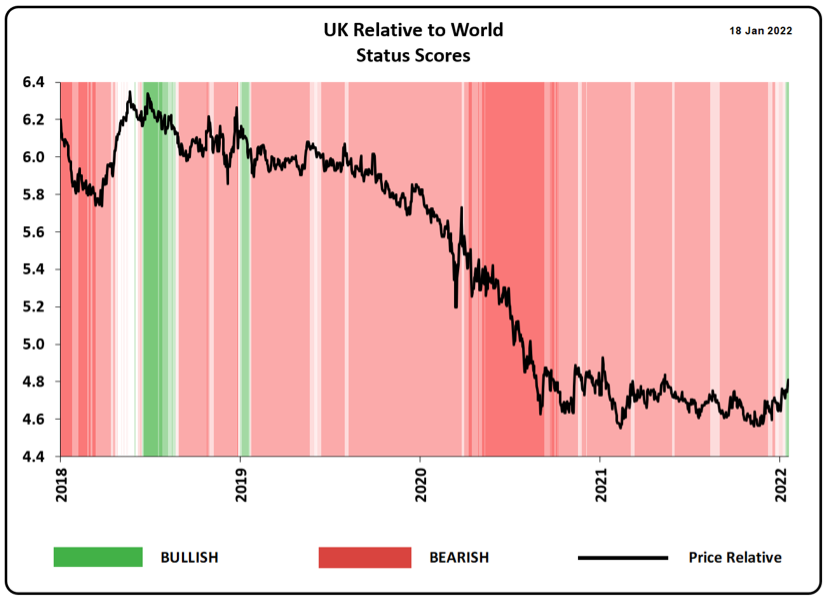

Chart of the fortnight: UK finally starting to outperform

For the first time in three years, Ekins Guinness’ Regional Equity Model has moved overweight in the UK. Although the UK has performed well in absolute terms, over the last 18 months it has broadly tracked other world markets and has suffered severely in 2019/20. Only now have UK equities established sustained positive relative momentum as the environment turns bullish.

Blonde Money

UK: BoJo a Go-Go

Momentum is all that matters in politics, and the momentum now is that Boris must go. The No Confidence vote is coming, claims Helen Thomas, and Boris is unable to pull it back from the brink. We have ahead of us a long and bloody battle for a successor, with policy twists and turns looking chaotic to confused financial markets. Helping out with energy bills, balancing the budget, managing covid restrictions; it all equals a formidable task.

Aitken Advisors

US: Taking advantage of Fed movements

Higher realised inflation + labour shortages > higher realised macroeconomic volatility > different reaction function from the FOMC and other central banks > higher policy uncertainty > abrupt multiple compression > good for unloved assets. It seems obvious to some, as James Aitken explains, but not to everyone. As risk premia is set to rise, investors should snap up shares from indiscriminate sellers in de-rated quality businesses, that is if they’re confident in earnings growth offsetting the Fed’s multiple compression.

Andrew Hunt Economics

US: The Fed’s calibration problem

Andrew Hunt expresses concern over how the government-enforced move towards a non-banking system financing of the deficit during Q2/2022, will bring with it the risk of a 1994-type event in the bond markets later this year. Should bond markets succumb to gravity, equity markets are vulnerable to an intense de-rating. Bear markets in Treasuries are rarely good news for EM assets on a relative basis.

Independent Strategy

Death of demand doesn’t mean death of Japan

Japan is an oddity. It suffered from the pandemic but none of the residual problems seen elsewhere have taken hold in the aftermath. Despite unfixable structural issues, David Roche is bullish Japanese equities, which will benefit from the economic backdrop and will be bolstered by a weaker yen – expect yen/equity correlation to reassert itself and go LONG Nikkei. David also remains SHORT yen vs USD and SGD.

Emerging Markets

MRB Partners

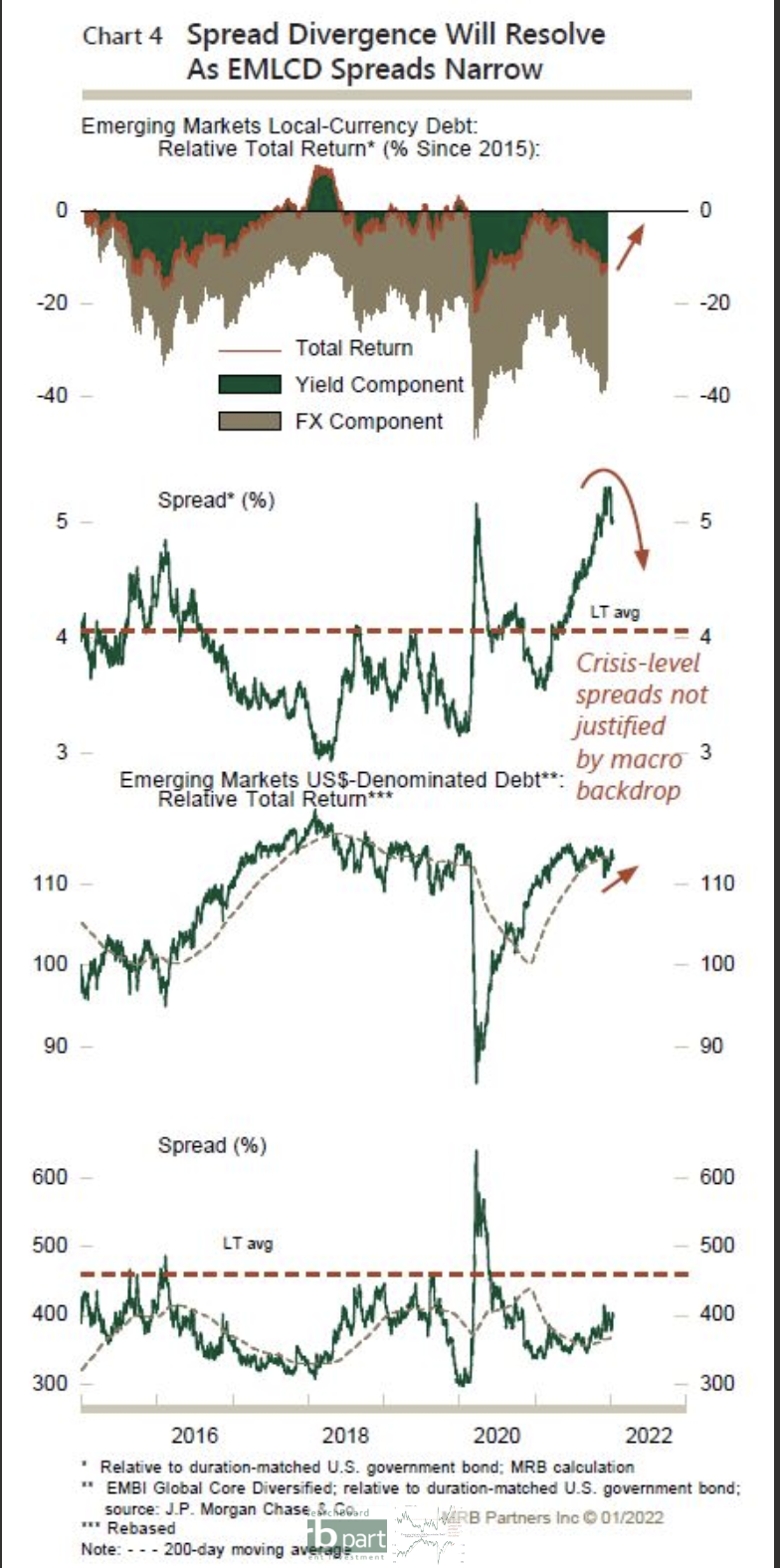

A barbell of yield and quality will outperform

Both flavours of EM debt (EMLCD and EM$D) will outperform US Treasuries (and G7 govt bond yields) in the year ahead, despite inflation headwinds. EMLCD will offer better returns due to relatively tight spreads – absolute returns will likely be muted, but historically-wide EMLCD spreads are inconsistent with the global backdrop, thus spreads will narrow. Investors should focus EMLCD holdings in a mix of high-quality and high-yield issuers.

Totem Macro

China: Reaching the point of max pain

An untenable large swathe of the most systematically important sector in the world, Chinese property, is now priced for distress. That outcome can’t and won’t be tolerated by policymakers, so Whitney Baker expects an imminent policy pivot, otherwise cashflow stress will spiral. Go LONG a diversified basket of the cleanest and largest Chinese property credits, with decent downside protection given current distressed levels.

Greenmantle

China: Old habits die hard

Beijing’s focus in 2022 is stability. Niall Ferguson expects China to announce a GDP growth floor of around 5% YoY in March, which will require more fiscal and monetary stimulus. The more that Beijing’s “zero-COVID” policy, export slowdown, and real estate deflation slow growth, the more the central government and the PBoC will turn on the fiscal and monetary spigots. Niall predicts a pick-up in infrastructure investment, looser credit conditions, and two more RRR cuts in 2022.

CHR Metals

China’s industrial production surprised on the upside in December

In Q4/2021, considerable prominence was given to reports of production curbs and cuts due to power shortages and efforts to improve air quality. It had been assumed that output would end the year on a stronger note as restrictions eased. Data show a much more robust rebound than expected with seasonally-adjusted output up by over 4% MoM. Annual output was up by 9.1%. An extensive review of the landscape is provided in Huw Roberts’ Global IP Watch.

Signal Risk

Ghana: Downgraded

Fitch Ratings downgraded Ghana’s sovereign credit rating from B to B-, affirming a negative outlook. Despite government contention, the de-rating was justifiable. The fiscal situation is dire, and the nation’s strong foreign reserves may struggle to maintain its status quo in the face of downside risks. The administration is as equally responsible for the financial malaise as Covid-19 is, and the country’s short-term outlook will depend very significantly on the nature of the government’s signals. Watch closely.

Alef Advisory

Iran’s involvement in Abu Dhabi attack is crucial to analyse

Hani Sabra doesn’t see Iran as being involved in the deadly Houthi attack on Abu Dhabi, with the attack instead marking a Houthi signal to the UAE and Saudi Arabia. This will result in the two nations growing closer over Yemen and a subsequent escalation in the war. However, if Iran had been involved, the enormous geopolitical ramifications could shatter the more positive dynamic that has developed over recent months.

Russia: A trade to consider, or time to reshuffle your portfolio?

Ukraine is slowly being encased in Russia’s fist, piece by piece. The next incursions will consolidate Russia’s land access to Crimea and cyber warfare has already begun. Such mischief offers significant volatility for trading. Expect energy and energy-related stocks and prices to accelerate. On the other hand, all else might free fall – predominantly European airlines, hotels and anyone trading with Russia or Ukraine.

ESG

The inevitable rise of agtech and how to play it

The inevitable growth of agtech, with its $300bn market growing at 7% CAGR, should not be overlooked. Companies in the industry offer attractive returns in excess of the cost of capital, consistently outperforming across the cycle. Dan Waterman delves deep into the market and identifies companies positively exposed to agtech themes, including ACGO, Deere, Genus, Zoetis, Darling Ingredients and Novozymes. Expect agchem manufacturers to feel the pressure in the face of increasing regulation, including BASF, Bayer and Nufarm.

Beacon Policy Advisors

Blue states’ growing crackdown on plastic

Democratic-controlled states have rapidly expanded laws taking aim at reducing consumer dependence on plastic. The surge in recycling laws, particularly extended producer responsibility (EPR) will raise costs for packaging producers, but manufacturers of more easily recyclable materials will benefit relatively. Aluminium is particularly well-positioned due to its properties, and manufacturers such as Crown Holdings, Ball Corp and Ardagh Metal Packaging will benefit from the Dem’s crackdown. Expect other companies leading the change from plastic to paper to also benefit, such as Graphic Packaging.

Commodities

Longview Economics

Gold: After a flat year, what’s next?

Gold has traded in a tight, narrow range for the past year and overall market timing models provide little insight into future direction. Fundamentals provide a clearer steer; Harry Colvin’s multi-factor gold model indicates gold’s price should have already broken to the downside. Harry expects 2022 to be a year of policy normalisation – rising TIPS will add pressure on gold prices and drive a breakout of the wedge pattern to the downside, leading to the selling down of net speculative long positions towards late 2013/2015/2018 net levels.

Crystal Shore Alpha

An extensive trading dashboard for commodity investors

Crystal Shore Dashboards covers an extensive range of commodities, including precious metals, carbon credits, energy and crops ranging from soybeans to oats, and even feeder cattle and lean hogs. With a 6-year outperformance of 56.4%, Gregory Shore’s weekly reports provides clear LONG/SHORT commodity trades with forward looking risk scores. Recent SHORTS include oilseeds, cotton, Robusta coffee, and recent LONGS include low sulphur gasoil and cocoa.