High risk - Forensic Alpha’s MI system reveals a rapid rise in the number of accounting red flags over the past 6 months. The most concerning of which relates to DSO given the sharp rise vs. historical levels. Headline "Trade and other Receivables" rose by 58% vs. an increase in sales of only 7%. Digging deeper, pure "Trade Receivables" grew by 19%, but there were a host of other asset accounts that grew even faster. Commonly known as "soft assets" they can be used to inflate earnings. A near-doubling should definitely raise eyebrows, particularly given they now represent over 60% of "Trade and other Receivables".

Big Tobacco’s RRPs showed positive performance in 2021 with promising signs for the future

Philip-Morris Int. reported a positive performance of Iqos Iluma in Japan and Switzerland, with significant growth in its heated tobacco portfolio, especially in the Middle East, Africa, South and Southeast Asia. Likewise, Japan Tobacco will prioritise its heated tobacco portfolio by 2027, while British American Tobacco’s revenue from its new products category rose by 42.4%, boosted by higher modern oral products sales. Swedish Match’s sales increased by 11%, driven by the smoke-free product segment, with solid growth in the US and Scandinavia for nicotine pouches and plans to invest further throughout 2022.

Vision Research’s short thesis is playing out as expected as HL share price crashes 15% following the release of results on 22/2/2022, resulting in a ~21% decline since the call was initiated 6/11/2020. During this time, the Stoxx600 rose 28%. The thesis focused on fee / commission pressure from Vanguard and fintech companies, difficult trading volume comparisons caused by unsustainably high activity during the pandemic, slowing net inflows, and rising costs per user. Vision currently has 14 European and 9 US active short ideas.

Following Intron’s deep-dive on once-weekly insulin icodec, they increase their peak sales forecast to $2.5bn and increase their TP to DKK800. The basal insulin market is a complicated arena with high levels of competition, differing views on how to treat patients, falling prices and adverse channel mix. Having spoken to US endocrinologists & community diabetes doctors, Intron have constructed a detailed bottom-up basal insulin model. They show that insulin icodec could achieve 25% market share and a daily net price of $5/day.

Recovery ahead of peers, expects strong traffic and FCF growth - Robert Crimes increases his TP to €296 (100%+ upside) vs. consensus at €155. Sell Side is too focused on Commercial reported financials (distorted by accounting MAG reversals), when it is better to analyse performance in simplified cash terms. Robert’s long-term forecasts show a recovery in traffic by 2024E, then +2.3% CAGR, equating to +79% in 2024-50E. Recurring FCF of €1.8bn in 2019 recovered in 2023E, then a consistent +1.6% CAGR in 2023-50E. Recurring FCF yield increases from 5.7% in 2022E to 8.5% in 2025E, attractive vs. Spanish 10YR bond yields. Dividend yield rises from 1.8% to 6.6% in 2025E.

Market moving legal disputes…

MDC's “Event-Driven Legal℠" Weekly Report summarises near-term legal events including analysis on their potential as share-price catalysts for the indicated companies. Recent coverage includes:

Arbutus Biopharma and Genevant Sciences recently filed Patent Infringement Lawsuit against Moderna seeking licensing fees for the manufacture and sale of Moderna’s vaccine for COVID-19.

IDT Corporation's Defense of a shareholder lawsuit challenging the repurchase of an Indemnification Claim from Straight Path Communications that spared it from having to pay $614m in FCC fines.

Sonos and Alphabet's continuing battles at the US International Trade Commission and US District Courts.

HPAI: Top trading partners ban US poultry exports

The risk to the poultry industry from Highly Pathogenic Avian Influenza remains extremely high as cases spread across the Atlantic and Mississippi Flyways increasing the risk that commercial flocks in a high-volume producing state will eventually face trade restrictions. Georgia, Alabama, Arkansas and North Carolina combined produce nearly 50% of all US poultry. An outbreak in any of these states would intensify the impact of trade bans, pressuring domestic prices and eventually production.

Good decision to explore strategic alternatives - ACI's strong financial performance is not being reflected in its equity. R5’s research suggests that ACI’s market share gains have accelerated further since the company reported 3Q results in early Jan. Despite superior performance, an incredibly strong management team and a meaningfully improved B/S, the equity trades at what has normally been associated with distressed firms in the supermarket arena at 4.6x R5’s FY23 EBITDA estimates and a P/E of just under 9.0x FY23 EPS. TP $50 (60% upside).

38% of sell-side analysts have the stock as a Sell. The short interest is 15%. Yet, the company keeps beating estimates (now nine quarters in a row). Analysts wrongly believe SFM is a story about price and the company will have to give-in to using margin-eroding promotions to drive comps. In reality, SFM is a merchandising story. The concept works by having a differentiated assortment and attracting customers looking for a different shopping experience. Under new management traffic is improving for the first time in years. New units are going to be higher ROIC. The company bought back 7% of shares last year. Stock trades at 12x P/E.

Brian McGough outlines why he thinks CPRI is primed to triple again from these levels. The stock has been a winner for Hedgeye (been long since ~$20/share), but it's all come from earnings, with close to zero multiple expansion. Brian looks at the sustainability of the earnings recovery and the levers that the company is pulling to create value. He believes Versace is on its way to becoming a $2.5bn brand pushing a 30% margin. Among other salient topics, Brian also explores what the company is doing with all its cash, including going over the M&A landscape.

Wrongfully tossed into the bad SPAC bucket - poised to benefit from rising pet ownership and rapidly rebounding travel demand. Furthermore, ROVR’s meaningful valuation discount relative to marketplace peers is increasingly unjustifiable with 1) fundamentals that are largely in line with / if not better than peers and 2) numerous potential top-line upward revision catalysts ahead (adjacent verticals such as pet health, expanding partnerships with retailers, etc). Trades at 2.5x EV/Sales (4.4x peer avg.) and 12x EV/EBITDA (30x for peers).

Growth at any price? While the acquisition of First Horizon certainly makes strategic sense as it expands TD’s footprint into attractive Southeastern US markets, Nigel D’Souza questions whether it makes financial sense. TD’s purchase price represents an implied P/B multiple of 1.75x. Even after fully realising expected cost synergies (which won’t happen until FY25), FHN is expected to generate a return of ~10% on invested capital. By comparison, North American banks that generate a 10% ROE typically trade at a 1.0x P/B multiple.

No brand identity or special sauce - UPST is a lending company disguised as a tech company and will end up like other previously "high-flying" FinTech platforms (e.g. LendingClub and Lemonade). Despite a ~65% decline from highs, the stock still trades at ~65x FY22 EPS, ~8x Sales, and ~21x BV. Provides a good setup for going short with expectations high after strong 4Q21. Consensus FY23 EPS is $3.25 but could fall to $1.50 if securitization market dries up. Sees no reason for it to exist in 5 years. TP $10 (90% downside).

Unloved Biotech

While Aaron Fletcher writes a lot of short research (with a focus on the 3 F’s - Fads, Fakes and Frauds), following the worst alpha year in biotech history, he currently sees the biggest opportunities on the long side. Aaron compares the sector to how energy was in the second half of 2020, when no one wanted to touch it. He expects M&A to pick up significantly later this year. IRF recently hosted a conference call with Aaron where he discussed his top picks for 2022 including TFF Pharma, Taysha Gene Therapies, Aptose Biosciences, IN8bio and Lantern Pharma. On the short side he highlights Ocugen and Moderna.

Has an appealing proposition for consumers in the emerging BNPL industry, but sellers are not seeing much differentiation among the leading competitors, according to Blueshift’s interviews with merchants, payment industry specialists and payment technology developers. Sources also revealed how the industry is ripe for consolidation (Amazon to acquire AFRM?); how BNPL will continue to grow in the US but won’t match the adoption rate internationally; as well as voicing concerns around credit risk and increased regulation.

Will beat and raise guidance when they report results for their most recent quarter (due 9th Mar) driven by robust execution and increased customer adoption. Russia's invasion of Ukraine will result in a material increase in cybersecurity spending. CRWD is the next-gen endpoint security leader in the cloud-native EDR space and the rapidly emerging XDR space. While there is currently too much hype and confusion caused by other security vendors over the true definition of XDR, as the dust settles CRWD’s superior / differentiated solution will be even better positioned to grow share at the expense of competitors whose solutions do not stack up technology-wise.

Always worth another look when the market is so bearish - the stock currently has no analyst Buy ratings. To GMR the underlying numbers (1.1x P/NPV or 0.4x @ spot; 10% dividend; 11% gearing) and the iron ore market outlook represent an enticing opportunity. Over FY23-FY24 GMR’s base case has a cash surplus for FMG of US$2.4bn post FFI (US$1.2bn) and dividends (US$8.8bn). China crude steel rebounded in recent months to ~1Bt/yr, supply remains constrained and demand solid. Product discounts troughed in late 2021. Yet there is a ~US$30/t arbitrage of the 2022 futures to consensus.

Chinese regulators come out swinging for round 2

After a period of relative calm which emboldened the bottom fishers, it looks like the Chinese state is not done with reigning in its technology sector. Richard Windsor thinks that the hammer of regulation will continue to fall hardest on the privately-owned Fintech sector. Tencent is likely to once again find itself firmly in the regulator’s crosshairs and given the importance of its Fintech business (+30% YoY growth in Q3 2021; made up 30% of total turnover), he sees the stock going much lower from here.

China's semi-finished food market booming

Predicted to become a trillion-yuan market in the next 3-5 years - the sector is in an early growth stage similar to the US (1960/70s) and Japan (1980/90s). The growth rate of the Business-end market is 20%+. Horizon Insights’ industry surveys show that 90%+ of restaurants, hotels, group meal manufacturers have started using semi-finished food attracted by the high degree of product standardisation and cost advantages. The Consumer-end market is growing much faster - online pre-made dishes have maintained YoY sales growth of 50-100% and offline sales are up 50%+. Companies well placed to benefit include Weizhixiang, Hema Fresh, Anjoy Foods and Longda.

India’s largest ever IPO - the government is looking to raise ~US$8bn for its 5% stake. In his 19-page report, Sumeet Singh runs the rule over this behemoth in the Indian life insurance space (market share of 60%+ in terms of both GWP and NBP). Positives: 1) Distribution strength stemming from its agent network. 2) Brand strength. 3) Industry growth expected to stay strong. Negatives: 1) Losing market share to private players. 2) Digital sales issues. 3) LIC has repeatedly been used to rescue government linked listings (most recently IDBI Bank). 4) Solvency ratio appears low vs. peers.

Sintex loan fiasco - is RBL’s acting CEO fit to be a banker, let alone run a bank? Approving a loan to a company which has a debt-equity of 10.5:1 and was already overdue on a loan to Deutsche Bank was either a case of extreme incompetence or ‘evergreening’. It also reflects extremely poorly on the independent directors in the credit and risk committees. The regulator must now investigate any other poor quality loans disbursed by the bank. A major implication of this story is that it is unlikely that interim CEO, Rajeev Ahuja, will be selected as permanent CEO; while an external appointment may disrupt the continuity the market was expecting.

Improving global market positioning whilst still trading at a discount to peers - SK Hynix trades on a 7.2x forward PE ratio despite commanding a strong position in the DRAM market and gaining significant market share in NAND over the last year (surpassing Western Digital, whilst Micron and Intel have also lagged). Following the completion of the first phase of its Intel NAND acquisition, SK Hynix should be the #2 manufacturer globally, edging out Kioxia (in which SK Hynix owns a 15% stake). Given the strong pricing environment Wium Malan believes consensus forecasts look very conservative.

Russia could exploit vulnerabilities in the Western financial system

Forget SWIFT. The single most important part of the sanctions is the freezing of the Russian central bank’s foreign assets. This unprecedented act concerns Wolfgang Münchau, who believes we are systemically vulnerable to Russian counter-sanctions. Take a Russian default on payments as an example (a major concern of Draghi’s) which could wreak havoc on an unprepared Western financial system. Sure, the targeted sanctions excluded oil & gas, but what’s to stop Putin using that against the West?

Go long government bonds despite consensus being massively short

Interest markets likely just hit a major inflection point, postulates Michael Belkin. This week he closes all US and global government bond short positions and goes LONG US 2yr, 5yr, 10yr and 30yr, along with European govt bond and Eurodollar futures. This may seem strange, but Michael believes a massive asset allocation shift out of stocks into government bonds could be underway in light of worsening Russia-Ukraine news and an oncoming stock market crash.

Removal of Russia from SWIFT is a big strategic mistake for the US

Removing Russia from SWIFT will force the world’s largest commodity-producing nation to de-dollarise. For the US as the owner of the world’s reserve currency, this isn’t good. China is rolling out its own Central Bank Digital Currency (CBDC), as is Europe and India, and the USD and SWIFT is the single point of failure for CBDCs. We will see a dollar shortage as Russian oil money is taken out of global circulation, potentially leading to a collapse in USD demand (and thus SWIFT usage) as China moves away to protect itself. The end of US Dollar hegemony is coming, and we’ve just accelerated it.

ECB credibility at stake

From the ECB’s perspective, the Russian invasion couldn’t have come at a worse time. Eurozone inflation has surged further, denying transitory claims. Food and energy prices will climb yet higher, and Phil Suttle argues it can only be stopped by monetary restraint. Tightening monetary policy into a war shock is hardly ideal but is the consequence of being far too permissive for too long in the “good times”. Expect the ECB to end QE mid-2022 and make a first 10bp rate hike in July.

EU fiscal policy in times of war

The economic decoupling from Russia will slow down growth and delay fiscal consolidation in the EU. We won’t see further prolonging of the suspension of fiscal rules beyond 2022, but the case for a phased return of fiscal constraints, flexibility for national spending and new EU borrowing programmes will be bolstered. As stagflation pressures bubble the ECB will find it increasingly difficult to normalise monetary policy and free itself from fiscal dominance; expect scrutiny against the plan to end net purchases before raising rates.

US: Can the Fed really exit?

Spurred on by misguided academics, the race is on among policymakers to shrink central bank balance sheets. The outcome could be disastrous; debt-ridden economies demand highly liquid financial markets to maintain these debts. In his latest report Michael Howell questions if the US Fed has become too big to exit. He points to warning signals present in the Goldman FCI which indicates that there could be much more frequent crises. Watch future central bank money growth closely, the dangers should be clear!

US equities outlook remains sanguine even in the face of Russian invasion

In his latest video, Barry Knapp explains why he sees little impact on US consumption stemming from the Russian invasion and explains his case for a capital investment boom currently underway. Key recommendations include overweight industrials (which Barry claims are the new tech), along with overweight US equities and underweight export-dependent economies. Barry also discusses the forces of deglobalisation at play and what it means for investors. Watch here.

Australia: Expect Growth outperformance to continue

In Macro Strategy Advisor’s equity universe, Australia remains his preferred equity market exposure with scores marginally better than EM. The technical scores are the same, but Australia’s advantage comes via a more attractive free cashflow yield. Buy Growth in Australia (vs Value in US) and expect the resurgence to continue until H2/2022. For defensive assets, recommends global property ahead of global govt bonds and Australian govt bonds.

Korea: Behind the curve

Korea’s external data is consistent with Andrew Hunt’s conclusions of his recent global inventories piece; supply chain issues are dissipating and export order trends are softer. However, Korea’s domestic economy is strong at present and a new, powerful credit boom appears to be in full swing. In general Andrew is at the dove-ish end of the spectrum with regard to global rate trends, but Korea is an exception. Market expectations for rates later this year are currently 50-100bp light.

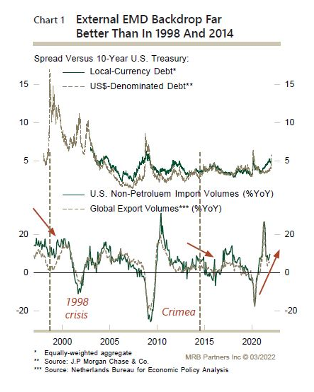

Chart of the fortnight: EM debt’s Russia problem – third time’s a charm?

Russian debt is on a slide towards what looks to be a technical default, and both other similar occurrences in 1998 and 2014 triggered contagion in the EM debt universe. Will it happen again? Phillip Colmar doesn’t think so. Despite the severity of the crisis, EM debt this time around enjoys considerable tailwinds (commodity prices, buoyant trade, undervalued currencies). He recommends overweight in both flavours of EM debt in a global fixed-income portfolio, with better upside for local currency-denominated instruments.

Can China tame global inflation yet again?

Since joining the WTO China has been a major global deflationary force, but many of late are doubting the continuation of this “China effect”. In David Rosenberg’s latest report, he shows that China’s focus on exports to fill the void from an imploding real estate sector, coupled with an unwinding of commodity reserves, could be a source of global disinflation many pundits have yet to consider. Expect China to export disinflation globally, including to the US who will benefit from lower import prices (see graph).

China: Geopolitical events will help China shift its sources of growth

William Hess believes the markets are underestimating the mismatch between demographics and China’s economic structure. The recent geopolitical fallout from Ukraine will hasten an acceleration to the build-out of China’s military industrial complex as a source of demand and growth output unrelated to demographics, infrastructure or property. In the meantime, expect policymakers (and the PBoC) to enact unconventional quantitative policies soon to stabilise the systemic stock of assets and liabilities, without which William claims China will be unable to achieve effective growth support.

Brazil and LatAm poised for outperformance

The agricultural powerhouse that is Brazil boasts extensive production in commodities ranging from sugar and coffee to orange juice and soybeans. In a world obsessed with inflation, Brazil should be an excellent hedge. John Karle expects more investment dollars to flow to LatAm if volatility continues to expand globally, especially in the wake of the Ukraine crisis. He adds a third unit of risk exposure to the iShares EWZ ETF to capture the anticipated returns, with a closing stop of $29 on the entire thesis.

The growing LatAm debt risk

Low-interest rates have led investors to take on progressively more risk in their quest for higher yields. Non-financial corporations in LatAm have taken advantage, with dollar debts growing much faster than their exports. In the process we have seen interest payments take a larger share of profits, yet this increased leverage has not raised the return on equity. John Llewellyn explains in his latest report the corporate level and systemic risks that are heating up; investors should watch closely since this could be the source of the next financial crisis.

Russia won’t cut off oil and gas supplies

Niall Ferguson believes that recent capital controls enacted by the CBR should be a sufficient stopgap for a few weeks. Nationalisation of foreign assets is a possibility but only as a last resort. The CBR’s decision to use exporters’ FX revenues to prop up the Ruble reaffirms Niall’s belief that Russia is unlikely to retaliate by cutting off gas supplies to Europe, but Western energy sanctions will be likely should the attack start targeting civilian population centres.

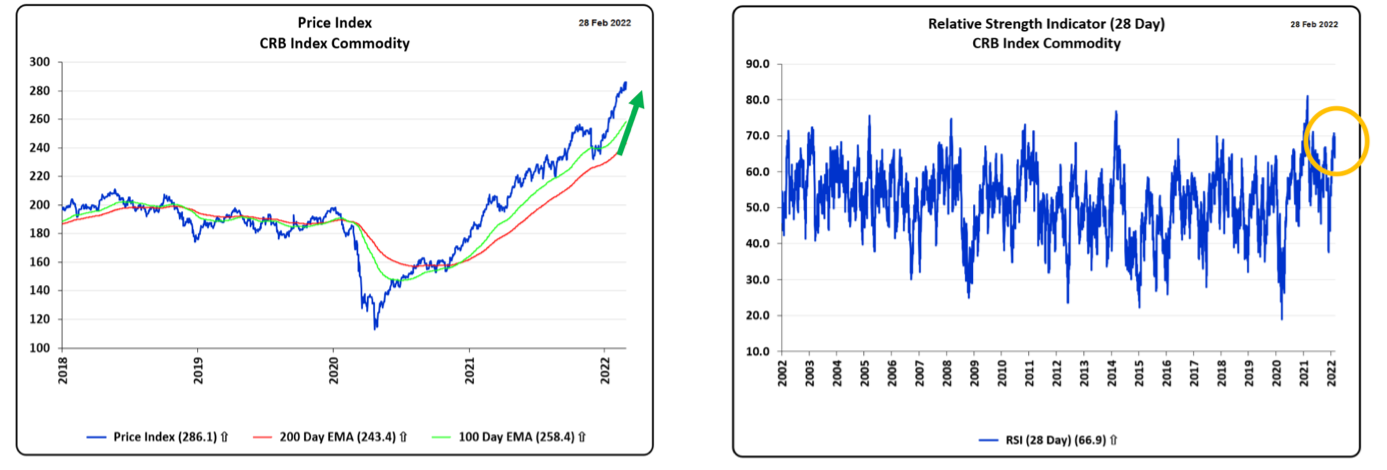

Commodity rally still not overbought

The commodity bull market, driven to strong highs by the huge expansion of US broad money created by the Fed, has rallied yet higher in the wake of Russia’s invasion of Ukraine. But inflation in the US has not yet peaked according to Charles Ekins. The Fed has hardly started to take remedial action to bring inflation under control and commodity prices, whilst strong, are not yet overbought. Remain LONG commodities and LONG Brent Crude.

Pulp prices to remain strong in coming months

Pulp exports from Russia’s large forest resource mainly head towards China, therefore Western sanctions will see little direct impact on pulp prices. Nevertheless, ERA Research expects pulp prices to remain stronger for longer in the face of logistical issues that will present themselves, with early-year strength continuing for longer before excess inventories are finally delivered. Recommended trades include LONG Mercer, with another quarter of low maintenance and good shipments expected (TP $16). Despite the strong pulp outlook, investors should EXIT Rayonier Advanced Materials with a heavy maintenance year ahead a key risk.

Expect oil to fall back to $80 over the medium-term

The West remains tepid in its response to Ukraine because it will not cut off oil and gas sales from Russia, although Paul Krake believes this may be coming (when the Saudis are on board). Putin’s demand for dollars will grow the longer this drags on and the only avenue he has is commodity sales, and you have to suspect he dumps oil and gas to China to prop up his reserves. Sure, $600bn of reserves is sizeable, but with the central bank raising rates to 20% Russia could be on the verge of a currency crisis.

Russia, Ukraine, gold and silver

In his latest video, Jeffrey Christian discusses the recent gains in gold and silver and how it fits into CPM Group's analysis of the Russian invasion of Ukraine. He then concludes the video by answering some recent questions, covering Silver American Eagles sold in January and February 2022, and the difference between trading volumes and open interest. Watch here.