Company & Sector Research

Europe

Sarria - Credit Opportunities

Corporate HY & Distressed Opportunities: Recent coverage includes...

Iceland - Energy costs, food inflation, and return to workplace post-Covid all weigh on recent bond movements.

Tullow Oil - Spend a dollar to make a dollar; only hedged on the upside for 60% of their planned FY22 production at $78/bbl.

Vallourec - Opportunity in an ill-fitted balance sheet?

Click here for further details and updates on several other names including Douglas, Matalan, Standard Profil and TAP.

New Street Research

Inflation in European Telecoms

Can prices be lifted to offset rising costs? Some operators have a legally defined right in customer contracts to lift price in line with inflation - whether they actually will lift will come down to local competitive dynamics and consumer attitudes to rising prices. New Street’s proprietary consumer survey results suggest that companies need to think very carefully about lifting price, as attitudes have shifted toward being more price conscious, even for the incumbents. New Street thinks owning BT, Tele2 and KPN are the best ways to insulate against rising costs.

Forensic Alpha

A focus on improving cash flow and strengthening the balance sheet appeared to pay off in FY21, as net debt/EBITDA came well under target. However, a closer look at the accounts suggest that the company has been stretching out payables and resorting to factoring in order to achieve this. While this may have helped the CEO achieve her short-term goals, investors could be significantly underestimating leverage and overestimating cash generation.

Green Street Advisors

Property Insights: Grey swans galore

With many of the building blocks of real estate experiencing the mother-of-all cost spikes in recent weeks, active developers are potentially heading for trouble - over one-third of Green Street’s covered listed PropCos in Europe are developing real estate with a fully-loaded cost exceeding 10% of their existing stabilised property portfolio value. Of these PropCos, two-thirds are projected to generate profit margins above 30%. This implies that Spot NAVs currently bake in sizeable value-creation potential. In the context of rapidly rising construction and energy costs, such upbeat forecasts are at significant risk of downward revisions.

Smart Insider

Analysing share transactions made by directors & senior employees

Identifying ‘Smart Insiders’ enables clients to generate alpha. Recent highlighted transactions include…

Puma (PUM GR) - Bjorn Gulden (CEO) purchases €512,000 at €63.99, taking advantage of recent share price weakness - he is a rare buyer and previous purchases have been timely.

Watches of Switzerland (WOSG LN) - Two directors make their largest purchases. Teresa Colaianni increases her stake by 56% and Robert Moorhead by 42%.

Kezar Life Sciences (KZR US) - Franklin Berger purchases $1.3m of stock at $16.25. He has a great record in Essa Pharma, another company where he is a director. Interesting to see him making this large purchase given the stock has more than doubled in a year.

North America

MYST Advisors

Bear’s Den Idea Forum

Several ideas presented at MYST’s latest buy-side event focused on “misguided acquisitions”...

Carvana (CVNA) - Overpaying for “mediocre ADESA asset” increases balance sheet risk as competition intensifies (35% downside).

Celanese (CE) - “Massively overearning” in Acetic Acid segment; DuPont M&M deal increases leverage / cyclicality (30% downside).

Synaptics (SYNA) - Expensive roll-up of low-quality semiconductor assets at cyclical peak (45% downside).

New Constructs

Get alpha from 10-K filing season

The Journal of Financial Economics (see here) proves how New Constructs’ Robo-Analyst technology overcomes material shortcomings in legacy data firms to provide superior fundamental data, earnings models, and research. During the Real Earnings Season (Feb 14-Mar 18), the Robo-Analyst found 38,314 Core Earnings, balance sheet, and valuation adjustments with a combined value of $18.9trn.

American Airlines (AAL) - Losses still bigger than many realise. Earnings Distortions totalled $3.5bn (173% of GAAP earnings).

GlaxoSmithKline (GSK) - Growing Profits + Cheap Valuation = Very Attractive Rating. Core Earnings of $6.9bn > GAAP earnings of $4.4bn.

International Flavors & Fragrances - Why understated profits aren’t always a good investment.

In addition, material weaknesses in internal controls were identified at several stocks including CBRE Group, Coupang and SeaWorld.

Quo Vadis Capital

How NOT to run a discount retailer - management squanders its pandemic opportunity to capture incremental customers. John Zolidis sees three problems: 1) Chronic underinvestment in infrastructure. This explains the difficulty of dealing with supply chain challenges. 2) Must stop raising prices to protect “merchandise margins”. The value is not there, and that’s why traffic and loyalty members per store are falling. 3) Should staff its stores, rather than using labour as a lever to offset negative comps. Reflecting the reduced labour and service, S,G&A per avg. square foot has not increased in four years, in contrast to industry and competitor trends.

Gordon Haskett Research Advisors

P&C Insurance: S&P's capital model changes evoke frustrations

Laudable ‘big picture’ objectives are clouded by some perplexing technical changes - with the comment period on proposed changes to S&P’s capital adequacy model ending on Apr 29th, veteran independent analysts, William Wilt and Alan Zimmermann, highlight some of the more notable and controversial model changes and how they could influence corporate behaviours.

Valens Research

Following its acquisition of Aetna, CVS is in the midst of a transition from pharmacy business to a massively profitable medical data and technology company - this reflects what UnitedHealth accomplished with Optum, and gives CVS opportunities to monetise its existing pharmacy business in new ways which could accelerate profitability and growth. Uniform Accounting confirms that the transition is underway and that the market isn’t pricing this in. Considering management’s strong execution and alignment to continue executing, equity upside continues to be warranted.

Residential roofing checks reveal very strong start to 2022 - 1Q22 SSS growth expectation is 20-25% (Feb was insane with most contacts suggesting SSS up 40%+; Jan & Mar both likely grew 15-25%). Contacts suggest the Jan price increase is gaining solid traction and many think the Apr increase is going to be huge. Inflation is the offset which keeps getting worse, but the industry has benefited from inflation and Northcoast thinks this can continue. Overall, they view their checks favourably for manufacturers and distributors and raise their full year estimates for OC and BECN.

BWS Financial

Successful transformation leaves ECVT focused on environmentally friendly solutions for oil refiners, petrochemical, and mining companies - the stock trades at a noticeable discount to other specialty chemical companies despite sales forecast to grow by double digits this year. The continued FCF generation should result in a leaner balance sheet and for focus on faster growth through new product introductions. TP $18 (50% upside).

Alembic Global Advisors

Chemicals: Recent TiO2 share price weakness a buying opportunity

Fears around demand destruction on the back of higher prices unfounded - Hassan Ahmed’s analysis suggests that a 50% boost in ore costs, all other costs remaining flat, could be offset by a 14% hike in TiO2 prices and a mere 4% hike in coatings prices. Current TiO2 prices are only slightly above their 17-year averages and 2008/2009 distress period-levels, while fundamentals remain healthy. Top pick is Tronox (benefits from higher TiO2 prices, but can also, via the firm's integration into feedstock ore, hold onto margin). Chemours and Venator also offer considerable upside.

Huber Research Partners

Has proven time and time again that its business model can continue to grow through various global crises - the momentum that FDS has with its organic revenue growth (+9.9% y/y in 2Q22) is the best the company has produced since 2012. Craig Huber sees room for the firm to be more aggressive raising prices. He also rates the new CFO highly and believes FDS will be more acquisitive / use debt more (both of which just happened with the company’s largest ever acquisition) and expects aggressive share repurchases when they resume next year.

Off Wall Street

How long can HPQ keep raising ASPs while bleeding unit share? For the second quarter in a row PC revenue growth was driven far more by ASPs than volume. While management argues that this is the result of its strategy of targeting premium market segments, OWS notes that operating margins don’t appear to be benefiting. When supply chain problems become less of an issue, how will HPQ grow revenue or operating margin? Meanwhile, the Poly acquisition looks more like an attempt to forestall revenue declines than a brilliant strategic move. TP $19.50 (50% downside).

Emerging Markets

Niko Partners

Video Games: Genshin Impact is a smash hit in the global market

The game’s success points to a shifting balance of power in the $200bn p.a. global video game industry, which has long been dominated by Japan and the US. It is one of several Chinese games that have broken through - the others on a smaller scale - in the Japanese market. Only four years ago, Japanese developers held a monopoly on the top games in Japan. Now, about one-third of the top 100 mobile games in Japan come from China.

Propitious Research

Can sustained market share gains be transferred into sustained margin progression? Wium Malan provides his take following the market's disappointment in JD.com's 4Q21/FY2021 profitability levels. He examines relative market share changes, key operational drivers and longer-term margin expansion trends. Wium also notes that on a growth-adjusted basis, JD.com trades at a discount to peers and a PEG ratio of just 0.7x. Strip out net cash (31% of M/Cap) and JD.com trades on a normalised forward P/NOPAT multiple of just 6.6x - that looks attractive for what is China's largest retailer.

Hemindra Hazari

LIC’s share of a stagnating market declines - promised growth of insurance penetration a mirage? With LIC’s IPO deferred until next year, prospective shareholders have time to examine a disturbing trend in India: life insurance penetration has stagnated (and even fallen) in recent years. All discussion of the purported original purpose of opening up (to secure long term funds for infrastructure investment) have been abandoned. New players' strategies have just been to target the more profitable end of the market, leaving India’s largest life insurer, stuck with the lower end.

Entext

Biologics key play on Pharma moving to ‘Fabless’ outsourced manufacturing model - an increasing number of Biotech / Pharma companies are choosing to outsource production facilities to avoid navigating the increasingly challenging regulatory landscape on their own. By combining a CRO and CDMO business model, the result is a full-scale CRDMO providing a completely integrated suite of end-to-end pharma solutions, WuXi (and Samsung Biologics) are both in this elite category. At the end of 2021, WuXi had already secured 60 integrated projects from customers worldwide (+50% y/y). The recent share price sell-off on US sanction fears is overdone.

Silk Road Research

China Elevator: Encouraging start to 2022

Industry checks reveal a much better-than-expected order environment QTD - orders through the first two months of the year expected to only be down low to mid-single digit range (NB 1Q22 represents toughest comp of the year; 1Q21 orders >+20% y/y). Infrastructure orders are strong (provides further evidence of a pick-up in fiscal stimulus); Residential orders are down, but less-than-feared and absolute orders are well above 2019 levels. Given the downbeat forecasts by large Elevator OEMs such as Kone and Otis, SRR sees more upside than downside to expectations for the full year

Galliano's Financials Research

Plenty of value in Payment companies

Victor Galliano highlights PagSeguro for its attractive valuations vs. its Brazilian and global peer group. Getnet is also considered too cheap to ignore despite its challenging relationship with Santander. While Nexi is the only European payments company added to Victor’s buy list - negative sentiment as a result of poor execution on past acquisitions is more than well discounted in the share price. In the megacap names, Mastercard remains a key pick.

Macro Research

Developed Markets

Global Macro Investor

It is time to enter the Exponential Age!

Raoul Pal has been waiting for eighteen months to pull the trigger, and he is now confident the Exponential Age has begun. It will mark the incredibly fast adoption and astonishing advancement of new technologies, propelling certain stocks to soaring highs. We are never again going to have a chance like this to take advantage, BUY the GMI Exponential Age Basket. Raoul has already seen huge demand for his Exponential Age Digital Asset Fund of Funds, with more than $100m+ into the markets.

Independent Strategy

For a handful of dollars

Diminishing the US dollar’s role as the global reserve currency will be gradual, believes David Roche. Autocracies will accelerate their efforts to escape the dollar system following the Russian invasion of Ukraine, but doing so is not easy. For the moment, the USD will benefit from the Fed’s tightening policy and its position as a safe haven; David Roche is staying LONG the US dollar versus the euro and yen. In the long run it will inevitably weaken, and investors should be prepared.

Eurointelligence

Euro: Ask not when rates rise, but where to

Wolfgang Münchau can see the attraction of the notion of a terminal interest rate as a way of denoting the highest level of central bank repo rates in the current cycle. However, he’s skeptical that the underlying calculation is relevant anymore. In a global economy shaken by repeated consecutive shocks, linear economic reasoning is bound to miss important variables. The current market estimate of a 1% terminal rate is too optimistic, and Wolfgang believes the worst-case scenario could in fact be as high as 10%. Tread with caution.

Longview Economics

US: Momentum stalling?

Given the rapid rally by the S&P500 and other key equity indices from their lows, markets have become greedy, overbought and complacently priced. Elsewhere, models highlight how global equity momentum is seemingly stalling and certain markets are struggling at key resistance levels. Chris Watling recommends staying opportunistically 1/3rd SHORT S&P500 June futures (retain stop loss at 4,644.0).

US: What you’re not hearing about the flat yield curve

Powell's rhetoric is more hawkish than ever, and the Treasury curve is almost flat. The last 6 recessions were preceded by inversions of the 2-10 curve, but the inversions came too early to be useful -- on average, 19 months before the next business cycle peak, causing investors to miss out on 12% equity rallies. Today's curve is distorted by transitory inflation expectations pushing up short-term yields far more than long-term yields. The 2-10 curve is actually almost 2% steeper than it appears.

Click here to watch.

View from the Peak

US: Why Quantitative Tightening (QT) won’t happen

In the past 30 years no major central bank has unwound its QE programs by selling a single bond in the market; instead, they let bonds mature and do not replace them. The moment the Fed starts unwinding some of its $5.7trn of treasuries it holds, this will lead to an unruly spike in interest rates, tightening financial conditions, significant widening of credit spreads and a violent sell-off in global equities. The market is starting to price the prospect of QT, don’t make the same mistake yourself.

Andrew Hunt Economics

Japan: Sitting out the cycle

While global inflation is rampant, Japan is an outlier. True, rising energy and food costs will deliver inflation above 2% YoY for the first time since 2015, but there is scant evidence of a broad-based reflation being underway. Andrew Hunt expects the Bank of Japan to look through (or even welcome) the supply-side pressures on prices and maintain rates at current levels, at least until Governor Haruhiko’s term ends in April 2023, putting downward pressure on the yen.

Emerging Markets

Crystal Shore Alpha

An extensive EM view

Crystal Shore Dashboards generates weekly buy/sell risk scores on all 34 individual emerging countries and on a staggering 1,200 single stocks falling under MSCI Emerging Markets, virtually the entire universe of the ETF. In addition to this extensive view, Crystal Shore Dashboards also offers six defined strategies for investing in EMs through either single stocks or ETFs, all easy to manage and execute. To find out more, please get in touch.

PRC Macro

China: Are policymakers close to pressing the panic button?

William Hess believes policymakers are pivoting from prioritising growth to asset price stability. There are signs Beijing is working on a larger-scale campaign to stabilise the property market (and property prices), and William believes a key step will involve purchases of toxic assets from commercial banks by a state-owned fund, and is therefore bullish for developer and bank stocks. In the past, stronger policy support for property has initially boosted developer shares more than developer bonds, with the latter repricing anticipated benefits more slowly, providing potential opportunities for investors.

AAS Economics

China: A combination of contractionary forces

A fresh round of lockdowns will combine with the lagged effects of money supply movements to further constrict output and trade, with lagged monetary pressures due to depress growth rates for most of 2022. Lagged money supply growth differentials between the USD and Yuan continue to favour the latter, but Frank Shostak expects a sharp reversal in favour of the USD within a few months. AAS Economics recommends highly defensive portfolio positioning, both across asset classes and within them.

Greenmantle

India defies gravity

Macroeconomic metrics in India were hit hard by the pandemic, but you wouldn’t know it by looking at election results or the equity market. Two years of deeply negative real rates have sent Indian equity indices to record highs. Negative rates are here to stay. The rupee will continue to weaken but Indian inflation expectations are surprisingly well-anchored. Niall Ferguson remains overweight Indian equities and fixed income relative to EM indices.

Alberdi Partners

Higher commodity prices to delay impact of Fed’s tightening on LatAm

Previous Fed hiking cycles have resulted in increased capital outflows across LatAm, but Marcos Buscaglia believes the fundamentals to be more solid this time around; high real interest rates, already-wide debt spreads, high commodity prices and weak currencies will preclude a massive exit of foreign capital flows. Nevertheless, Marcos expects the region will continue to be characterised by subdued economic growth throughout 2022 with the exception of Colombia, which will benefit from the higher oil prices to reach >6% annual growth.

Krutham (formerly known as Intellidex)

South Africa: Employment metrics worse than they appear

Driven by households and agriculture, employment was marginally stronger than expected (3.2% lower YoY). However, Peter Montalto remains concerned about the very weak formal sector, which he believes to be severely lagged and still recovering from the middle of 2021, meaning we can expect unemployment levels to stabilise here rather than fall. Interestingly, formal sector employment is lower now than the worst point during covid, a testament to the country’s weak underlying potential growth, inequality, and inadequate labour laws.

Oxford Analytica

Risks to Sri Lanka’s banks will increase

The country’s foreign exchange crisis is putting considerable pressure on its banking industry. We will see pressure on domestic banks grow, as they are being relied on to subscribe to dollar-denominated government bonds. If several state lenders are trying to draw forex from other commercial banks to finance such investments, the stability of the sector could be at risk, regardless of what the CBSL says. Losses would hurt credit supply. Bringing further damage to the ailing economy.

Commodities

Aitken Advisors

This isn’t demand destruction, it’s demand construction!

The transitory inflation crew want you to believe demand destruction will soon restore commodity prices to normal levels, yet every so-called government solution involves subsidising demand! James Aitken reiterates how the largest commodities demand construction event is the climate transition currently underway. In fact, as important as the recent repricing of bonds has been, commodities are the world’s new risk-free curve, and everything is priced off them. Recommended related trades include LONG AUD, which will benefit as the world turns to Australia as a trusted commodity supplier, and staying LONG BP and Hess Corporation.

Global Mining Research

Preferred copper mine exposure

With copper trading above US$4.00/lb the ability for copper miners to fund initiatives is strong, providing a boon especially for small capitalisation base metals companies. In such a group, David Radclyffe’s preferred exposure is through BUY-rated Capstone Mining and Sandfire Resources, both offering a blend of value and growth, and which have benefited from M&A accelerated growth. Tony Robson considers Ero Copper after its massive underperformance; it is now more attractively priced and the company is pushing exploration hard, but growth is some time out, so he maintains his HOLD rating.

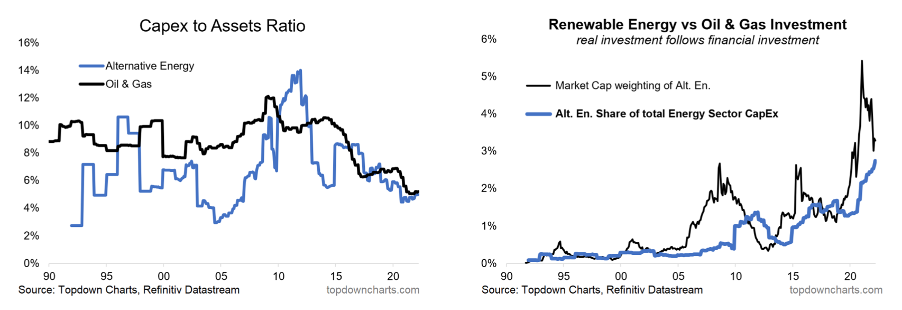

Topdown Charts

Clean energy’s golden era, coming soon

Clean energy stocks have lost a bit of steam as previous excesses unwind. Relative to traditional oil & gas equities, the underperformance is accentuated. If energy commodity prices rise further or at least remain elevated, and should we see a further follow-through of climate-related investment, investors should expect a new golden era of capex (aka real investment) in clean energy.

Vanda Insights

Crude backs off another cliff edge, but supply fears are entrenched

Although the $121 Brent levels last week were unsustainable, Vandana Hari believes global oil demand growth still has some runaway before high prices erode it enough to bring it back in balance with curtailed supply. In her latest report, Vandana examines the global oil and gas trade and ties being realigned in the wake of the Ukraine war. Key topics include the US ending Russian oil and LNG imports, a UK phasing out of Russian oil over 9 months, a spike of Indian oil purchases from Russia and a ramp-up of China’s Russian crude intake.