Company & Sector Research

Europe

ResearchGreece

Following impressive FY21 results, ResearchGreece raise their 2022/2023/2024 net income estimates by +17%/+12%/+7% and increase their TP to €21.50 (40% upside) - the business model is working and they would rather weather the energy / geopolitics / inflation storm with a) a net cash balance sheet (25% of M/Cap); b) that trades at 8.1x EPS 2022E (ex-cash) and 5.5x EBITDA 2022; c) which continues to invest in the business (stores); d) will be paying a dividend yield of 5% - over any other Greek stocks.

Forensic Alpha

Questions management's narrative of experiencing a strong recovery from Covid - AIR achieves the highest risk rating in Forensic Alpha’s universe after several new flags are identified in its annual report. This follows the publication of FY results where Forensic Alpha had already picked up on growing DSO and Contract Assets. Receivables past due has risen from 18% of trade receivables in 2020 to 29% in 2021. AIR now has more than €1bn of trade receivables past due more than 3 months (equal to more than 20% of invoices). Furthermore, a massive €635m of those receivables are past due more than 1 year!

AIR Capital

Rising cost base - the recent jump in energy prices is adding pressure to inflated input costs. This fibre optic cable manufacturer's gross margin has already fallen from 39.7% in 1H21 to 36.7% in 2H21 as record prices in energy prove difficult to pass-through to customers. Elevated R&D expenses (6.5% of sales vs. 4% in 2019) and higher capex will only compound the issue. Higher operating expenses (highlights increases in wages, travel and marketing) will negatively impact EBIT margin. Share price resilience YTD will not last.

This leading manufacturer of carbon and graphite products can grow profits by more than 50% by 2025 - many of MRN's products are essential to the energy transition which will help drive strong organic growth over the next 3 years (highlights major capacity investment in the US, Solar and EV exposure, as well as benefitting from its expertise in semiconductor manufacturing). Julien Onillon sets a target price of €45 (45% upside), valuing the company at 1.2x Sales. At this price MRN would trade on a EV/EBITDA 2024 multiple of 7x - a slight premium vs. European competitors is warranted given the group’s strong reputation and better prospects.

TT Equity Research

Close to fully utilising its commercial paper facility - implies clear breach of covenants. This means that additional to Teun Teeuwisse’s original short thesis (sustainable cash flow generation of €200m at best and €1.8bn of hidden debt in factoring, stretched payables, delayed tax and social securities, and from unpaid capex), a potential capital increase is now added. While Teun assumes further cash outflows in 2022 and more margin pressure, to bring real net debt/OMDA to a manageable 1.5x the company needs to raise €1.5bn vs. its current M/Cap of €2.5bn. Shareholders face massive dilution.

North America

Aviation Insights & Trading Recommendations

Anyone who believes there are no investment opportunities in this sector is not looking hard enough - Asterisk’s 60-page weekly Aviation Update covers all the key events in the space (e.g. Russian sanctions on aircraft lessors, Covid restrictions on individual countries, impact of the Chinese 737 crash, new financings, and M&A activity) as well as highlighting all the major long and short opportunities for Airline and Lessor paper (including EETCs) - predominantly fixed income but also a focus on the underlying equities.

Off Wall Street

High conviction shorts offering 30%+ downside

Choice Hotels (CHH) - Brand commoditisation + long-term supply overhang = broken unit growth story. Once the 2021 pent-up leisure boom passes, CHH’s multiple will contract to reflect its reduced long-term growth prospects. TP $69.

Focus Financial (FOCS) - Roll-up strategy is destroying value; questionable accounting. Cash ROIC continues to look very poor. TP $25.

Louisiana-Pacific (LPX) - OSB supply response will happen much faster than bulls expect. Accelerating capex / capacity expansion near cyclical peak is a mistake. TP $30.

Radio Free Mobile

Price of free speech - TWTR's board caves to shareholder pressure, but Elon Musk is unlikely to make any money from this deal. Richard Windsor expects a complete management and board clear-out and much greater clarity on content moderation policies. He sees Musk’s offer as very generous and shareholders should take the opportunity to sell given the shares are probably worth closer to $20. TWTR’s best growth is behind it and would need to generate ~$3.4bn in FCF every year in order to justify the offer price (it has averaged about 1/3rd of this level over the last 3 years).

R5 Capital

Envisioning Tractor 3.0 - Scott Mushkin provides his thoughts post the 1Q report, where every metric exceeded his forecast, which drove a significant bottom line beat. As impressive as this was, R5’s research continues to point to even more opportunities for the company in the future. Specifically, they see an expanding TAM driving sales, EBIT and EPS growth, as well as higher ROIC. TSCO remains R5’s top long-term Buy idea. TP increased to $277 (35% upside). However, if same store sales run ahead of their forecast, which they did in 1Q, upside is well north of $300.

Quo Vadis Capital

Opportunity to buy a hardline growth retailer with perhaps the best combination of unit growth, unit level ROIC and economically defensive model in the market - John Zolidis believes the Street is underappreciating the company's ability to benefit from trade-down, the stickiness of higher ticket (which has a margin benefit), as well as conservative guidance (EYE has beaten analyst estimates for 10 consecutive quarters). He also sees some optionality for remote testing to structurally reduce operating costs. 60% upside.

DTC Index: Relative valuations at multi-decade lows

Douglas Lane’s DTC Index trades at a 45% discount to the S&P 500, which is the lowest prospective relative P/E ratio for the Index since the tech bubble 20+ years ago - Douglas argues value-oriented investors may want to start to move into some of the names in this group given their financial strength, above average gross margins, strong FCF generation and pricing power in what tends to be more defensive product categories. Buy-rated stocks include Herbalife, Nu Skin and Medifast.

Valens Research

Current valuation fails to recognise the operational transformation STZ has undergone over the past several years - its portfolio shift to growing beer brands such as Corona, Modelo, and Pacifico, and its focus on premiumisation, have propelled profitability to new heights. While markets seem concerned about the potential of new growth opportunities, the firm seems particularly well-positioned to weather inflationary and pandemic-driven concerns given its close alignment with broader alcohol consumption trends.

Portales Partners

Volatility and price weakness mask solid fundamentals and good value - Charles Peabody projects operating expenses to be declining at a mid-single digit rate (Y/Y) by 4Q22, while revenues are growing at a low-to-mid single digit rate. Improvement in operating leverage should be more than enough to offset any normalisation in credit costs and still allow earnings growth to accelerate in the second half of the year. WFC will achieve >10% RoTCE for 2H22. Don’t rule out another double-digit dividend increase in 4Q22 and share buybacks to ramp up again. TP $60 by end of 2022.

Alembic Global Advisors

Chemicals: Natural gas price spike concerns overblown

This decade could see US ethylene margins even stronger than last decade's lofty margins - in addition to discussing how the crude oil-to-natural gas price ratio remains squarely in the US chemical industry’s favour, Hassan Ahmed contends that higher margins are sustainable, particularly keeping in mind that 79% of all ethylene capacity expected to come online between 2021-2026 will be based in the cost-disadvantaged regions of Asia and Europe. His analysis suggests that as much as 21% of this incremental capacity is at risk of being cancelled or delayed, which bodes well for Dow Inc (TP $75), LyondellBasell (TP $120) and Westlake (TP $140).

Sales Pulse Research

Further acceleration in cyber security; other areas of IT spending are mixed

SPR's preliminary survey results report strong momentum in Q1, and the majority see continued, or accelerated growth for the rest of the year - consistent with previous views and recent reports, those Security Vendors most called out as seeing strong growth are Palo Alto, Zscaler, CrowdStrike, Fortinet and SentinelOne. Also consistent with views from last quarter, vendors with improving checks include Tenable, Ping Identity and Check Point. In contrast, SaaS vendors are having to work much harder to achieve their goals - SPR’s channels noted that SaaS projects were among those that were being pushed out.

Australia

Global Mining Research

Offers an attractive combination of high production growth, low costs, assets in safe jurisdictions and a management team with an impressive track record - all points of differentiation to intermediate peers. GMR discusses how consolidation in 2021 has created district plays in the portfolio and EVN has a clear pathway to 1Moz/yr (or ~1.5Moz/yr GEO) in FY24/FY25. Critically, Cowal and Red Lake have the potential to demonstrate they are “true Tier 2” assets. While M&A is part of the gold miner's DNA, GMR believes options are limited right now, although management may consider a Mt Rawdon replacement or merger further down the line.

Japan

LightStream Research

Mio Kato still expects a profit collapse as frothy conditions sets the stage for a big disappointment - Mio believes concern regarding China could be the initial catalyst to drive the stock down and could be followed by suspensions or delays in EV and battery capex as raw material price increases start to hit financial statements. Mio no longer considers Fanuc to be superior to peers and actually views its long-term growth outlook to be impaired vs. Yaskawa. The stock remains an extremely attractive short - at 10x ¥110bn in operating profit Fanuc’s implied TP would be ¥8,783 (60% downside).

Emerging Markets

Copley Fund Research

GEM Funds Investor Positioning Insights: India maximum divergence

Stephen Holden’s data highlights the growing divide between Value and Aggressive Growth managers in India - while Aggressive Growth investors double down, especially in Financials and Tech, Value managers are finding fewer opportunities to invest, and appear comfortable allowing their underweights to increase. That’s not to say there are no Value opportunities in India, just not enough to match either the benchmark weight, or the weight of their Growth peers. As the world focuses on a potential Growth to Value switch, in EM at least, India will be a key driver of relative performance between the two sets of investors.

Stocks highlighted include HDFC Bank, Housing Development Finance, Indian Oil Corp, Infosys and Tata Consultancy.

Silk Road Research

China: Industrial surveys paint bleak picture

SRR’s latest readings fall sharply to levels last seen during the 2020 lockdowns with four out of five sectors tracked deteriorating (Autos, Commercial Vehicle, Construction & Mining Equipment, Elevator). While SRR expects most companies to report relatively solid results out of China for 1Q22, there is clear downside risk to forward guidance. The one exception to the Q/Q declines in their surveys was Automation - where sales, orders, outlook indices rose, as did SRR’s pricing indicators, which hit three-year highs. Anecdotal evidence suggests that book/bill remains >1, with order growth rates in the HSD-LDD range.

Hemindra Hazari

Citi’s well-off retail clients may not travel meekly to Axis Bank - while its acquisition of Citibank India’s consumer finance division has been applauded by the stock market, shareholders should consider that Citi’s retail customers are used to superior service standards from a robust technology platform and a dedicated and well-paid staff. Unfortunately, Axis Bank’s technology systems are less reliable, and a toxic work culture has impacted staff morale and customer service. Meanwhile, competitors have already chalked out strategies to poach Citi’s premium customers.

Creative Portfolios

From an Asset Quality stance, the Chilean Banking sector is the most resilient in LATAM with meagre or even mild Asset Quality erosion in contrast to all regional peers. Household Liquidity is elevated and credit is expanding at high single-digits. Profitability and Efficiency are on an upward trajectory while Capital is stable. Paul Hollingworth highlights BCI (PH Score™ 8.1, FV of 11%, PBV 0.95x, Earnings Yield 12.3%, Dividend 3.8%, Total Return Ratio 2.4x) and Itau CorpBanca (PH Score™ 9, FV of 10%, PBV 0.5x, Earnings Yield 21.8%, Total Return Ratio of 1.44x). For both banks, the value-quality PH Score™ gauge is elevated and indicative of strong relative returns going forward.

Aequitas Research

Sumeet Singh runs the rule over SK Telecom’s cybersecurity arm as it looks to raise US$860m in its upcoming Korea IPO - a key issue for Sumeet relates to the proportion of revenue that SKS derives from related parties. It has increased from 15.7% of revenue in 2019 to 25.5% by 2021 and accounted for 43.4% of growth in FY20 and 65.6% in FY21. In addition, he has previously flagged how SKS’s physical security and cybersecurity segments have been suffering from margin pressure for several years and the fact that the company is now heavily in debt. The stock is being offered at an expensive looking 8.2-9.3x FY23 EV/EBITDA, 2.4-2.7x FY22 EV/Sales and 44-55x FY22 P/E.

Macro Research

Developed Markets

Andrew Hunt Economics

Could inflation soon become deflation?

Andrew Hunt fears that the world is defaulting towards an “anti-goldilocks” scenario, where we will witness the imposition of monetary conditions that are too tight and the creation of deflation within the non-traded/service/property sectors. If this is the case, the USD should remain well bid and there will be a buying opportunity in bonds before too long, and investors should expect a tough time in the equity markets. Other scenarios could occur, but Andrew claims most of them involve the market underestimating both inflation and growth rates.

Aitken Advisors

Cheap European cyclicals

James Aitken comments that by some valuation measures (incl. relative 12-month forward P/E) European cyclicals (excl. tech) have only been this cheap vs defensives twice in the past twenty years. Sure, EMU may be facing a colossal existential threat that demands a heavy discount on European cyclicals, but corporate reporting and earnings commentary has been rock solid the past week. Over the past 14 years, when the consensus narrative goes from dreadful to less bad it can generate an outsized move higher in cyclicals. Could we see this happen again?

Quill Intelligence

Industrial recession goes global

PMI signals appear comforting: Japanese PMI remained positive, US flash Mfg PMI hit a 9-month high and German PMI remained above 50. However, take a look under the hood and you’ll see warning signals flashing! Japanese and US confidence is ailing, and German manufacturing output has fallen for the first time since June 2020. Danielle DiMartino Booth sees further downside to industrials as the magnitude of fresh Chinese lockdowns exacerbate the stagflation being sustained across the world’s factory floors.

Longview Economics

US: Will SPX downward momentum persist?

Levels of fear and panic in markets increased significantly this week, with weakness in US equities led by growth heavy indices such as the NASDAQ100 (-3.9%) and Philly SOX (-4.4%). Both the SPX and NDX closed near their March lows, but Chris Watling sees a likely relief rally in equities over the next 1-2 weeks with his models indicating a strong BUY message. Stay ¼ LONG S&P500 June futures and retain stop loss at 4,130.

Beacon Policy Advisors

US: Bullish on reconciliation

Is reconciliation back for the Democrats? Despite the scepticism, Stephen Myrow seems to think so. With re-election in 2024, Joe Manchin will be open to a deal, just as long as it isn’t called BBB. Some sceptics highlight the division between Manchin and Sinema on taxes and pharma, but Stephen points to an overlap on offsets between the two. The support of the two will bring Biden on board, who still holds power among Democrats in spite of ailing approval ratings.

Belkin Report

US: FAANG – From the Penthouse to the Outhouse

As rate hikes, QT and the Ukraine/Russia conflict push investors out of stocks, FAANG comes out on top of Michael Belkin’s models when it comes to sell recommendations. But after FAANG comes a wide array of SELL and SHORT recommendations - which Michael comments are mostly non-consensus - in industries ranging from semiconductors and computers to securities brokers and banks. These are mostly popular longs for hedge funds and momentum funds; don’t get hurt in tech liquidation!

Greenmantle

Australia: Morrison returns

Both the polls and the betting markets are against incumbent Prime Minister Scott Morrison winning the May 21st election, but Niall Ferguson’s analysis indicates that he will come from behind and win. Meanwhile, expect the RBA to address inflation with at least two hikes this year starting after the election, but beyond this it will hold rates for longer than market expectations. In the short-term, Niall remains bullish on the AUD in the face of RBA hikes and commodity prices.

Entext

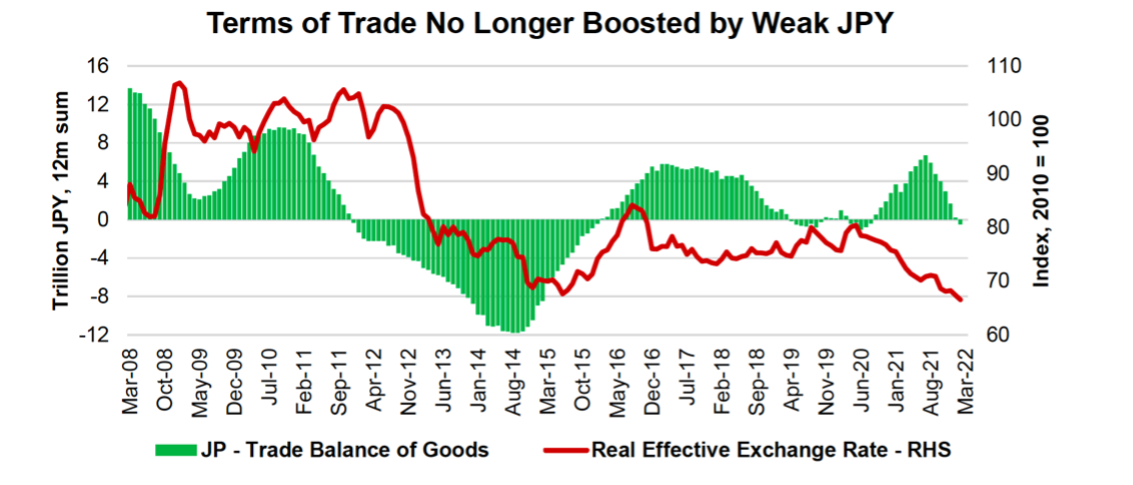

Japan: Land of the falling Yen

The selloff in JPYUSD to approach 130 has panicked Japan's corporate elite who reject the BoJ's view that weakness is net positive. In his latest report, Sean Maher explains that the BoJ is oblivious to a structural change in Japan’s business model over the past 15-20 years which makes an excessively weak yen a margin hit, and comments on the limited choices the BoJ has ahead. He therefore replaces his tactical Nikkei long with a 50:50 gold/silver alternative.

Emerging Markets

Topdown Charts

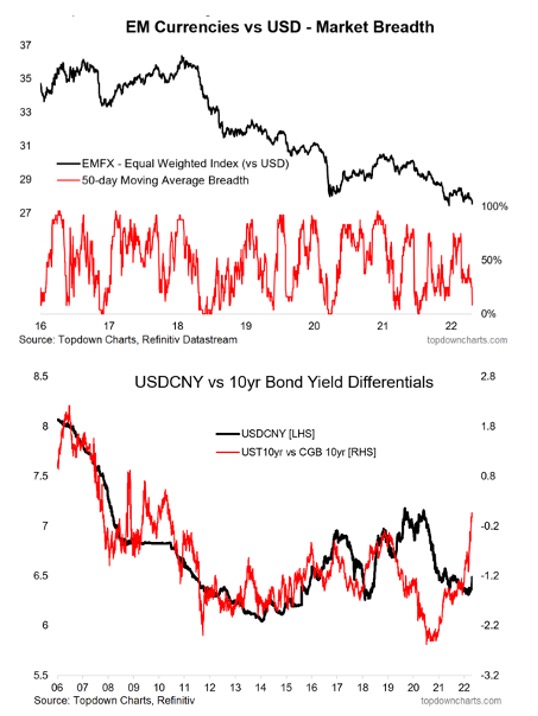

EM/Asian FX selling continues

Callum Thomas comments on how EMFX is coming under further pressure with the latest weakness largely centred in Asia, although even the previously strong LatAm index is stumbling. We’ve seen EM Asia central banks hike an average of 15bps, far behind the 350bps average of EM ex-Asia. USD/CNY is starting to move too, with the path of policy/bond rate differentials pointing to devaluation risk. Further short-term downside looks likely for Asian/EMFX and warrants short-term caution on EM assets.

High Frequency Economics

China: Lockdown depression

Tesla’s Giga Shanghai plant shut down for 22 days on March 28th and is still running at half capacity. It may be one factory, but Carl Weinberg sees it as a microcosm of a wider Chinese economy being massively unsettled by lockdowns. Since there’s a 1-2 month lag in shipping from China to most destinations, expect to see the effects very soon with the shock to supply chains bringing forth a profound global recession.

Llewellyn Consulting

China’s continuing growth slowdown

Preston Llewellyn explains how four of China’s historically most important drivers of economic growth (population growth, increased participation, employment and longer working hours) have slowed down, with some now even detracting from growth. Claims that productivity improvements will offset this are misguided, as Beijing’s ‘Dual Circulation Strategy’ and regulatory crackdown on the services sector will drag on productivity over the coming decade, alongside the reduction in leverage-supported demand growth. The days of double-digit growth in China are finally over and the metrics will continue to decline even further.

PPG Macro

Signs of overshoot in credit hedges, China rates

While risk justifiably remains under pressure, the great rush to buy protection has made some hedges attractive. The hedges, that have worked, could easily rally while underlying cash comes under pressure. Patrick Perret-Green looks at a few examples: China sovereign CDS is at 80bps; CDX HY has widened from the broad Bloomberg USD high yield index (see graph 1); money rates in China are falling rapidly and bank NCDs are showing no signs of stress (graph 2); and CNY NDIRS are looking like a receive, given the fall in repo rates.

Alberdi Partners

Peru’s pension fund withdrawal bill

February’s small decline in activity confirmed the stagnation seen in recent months in Peru, and Marcos Buscaglia retains his forecast of close to 2% growth for 2022. Meanwhile, congress is treating a new pension fund withdrawal bill, with subsequent withdrawals estimated to be worth USD ~$4.5bn. Marcos believes this implies considerable sales of foreign investments, with these offsetting forces keeping the FX close to the current level in coming months, with the uncertainty effect prevailing later on and driving a depreciation at end-2022 to 4.05 and 4.20 in 2023.

Teneo

Fresh sanctions likely in Guinea and Burkina Faso

Having failed to meet the April 15th deadline set by the Economic Community of West African States (ECOWAS), the military juntas in Burkina Faso, Guinea and Mali will be hit with new sanctions from ECOWAS and possibly Western allies. Although initial sanctions will not be stringent, they will only deepen a rapprochement with Russia; longer term, split alliances between Russia and the West will weaken the economy, politics and security of the West African region.

Commodities

Queen Anne's Gate Capital

Oil prices will explode higher

The US is somewhat insulated from the shift away from Russian oil and gas, Europe much less so. The change in elasticity in demand for gasoline that Kathleen Kelley has long spoken about is going to change the way this oil shock plays out. But the shift from Russian supply is taking its time. The market expects oncoming tightness but it hasn’t shown up yet. There are no more longs to shake out of the market – when the tightness is clearer, the market will explode even higher.

Dollar strength to result in commodities correction, especially copper

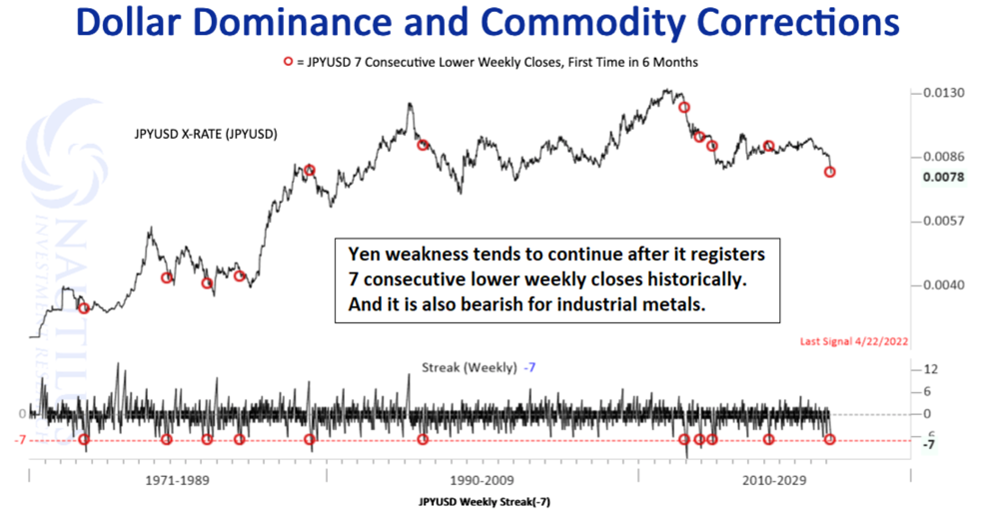

As the USD registers 7 consecutive weekly higher closes against the yen, the Nautilus team comment that similar USD strength has preceded a meaningful commodities correction; the S&P GSCI Index declined by -9.38% twelve months out, with copper facing significant -15% losses. The preconditions are now in place for a major top in copper, keep an eye out soon for the signals to indicate a SHORT.

HED Capital Management

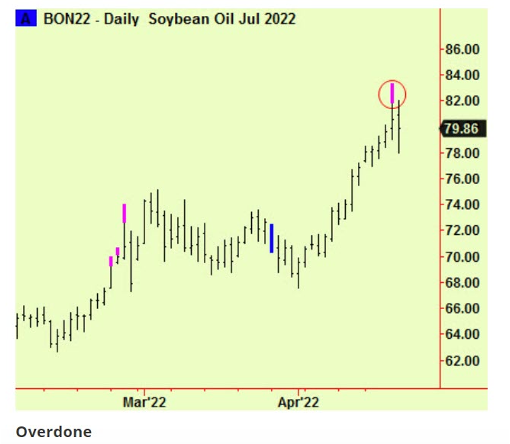

Soybean rally doesn’t match up with the facts

In the face of the huge, stranded harvest problem in Ukraine, soybean oil has been rising like all grain markets. Yet, Richard Edwards believes this move doesn’t reflect reality; Ukraine isn’t a large producer of soybeans. Instead, the rally is largely a result of substitution pricing (Ukraine is a big sunflower oil producer), a sympathy rally, and worries about a shift in planting intention away from soya in the US. None of this is directly attributable to any immediate shortage in soybeans or bean oil, sell SHORT.