Company & Sector Research

Europe

Hedgeye

Brian McGough believes we are nearing the “someone will take it private” price - while this would be a massive catalyst for the stock, Brian thinks the better play for shareholders is to realise the upside in the model over a TAIL duration in the public markets. He continues to see a leisure-led travel recovery, new peak operating margins, the Hainan JV with Alibaba, and significant financial de-levering as the cash flow story accelerates materially. Sentiment on the name is troughing and institutional interest is picking up. DUFN is the poster child for a company that will emerge from the pandemic stronger than it went in.

Holland Advisors

The pricing gap with pub peers is now the biggest it has ever been - bear in mind a 2% rise in prices alone boosts JDW’s net profits by c.40% in a year. Andrew Hollingworth believes the investment return prospects are excellent for those prepared to take a long-term view on JDW’s customer proposition and its continuing growth and dominance. Andrew’s previous model (when the share price was £9.11) forecast a 7-year investor IRR of 25% (assumes gradual rise to 10% margins). With a £43 share price in June 2029. Even keeping margins constant gave a 15% IRR. Reducing the start price to £7.20 increases these returns to 26% and 17% p.a. respectively.

the IDEA!

Despite a positive outlook for new orders SBMO shares still trade at a relatively high discount to NPV - highlights opportunities to win additional contracts with the likes of Exxon where FPSOs SBMO has been building are very efficient (breakeven price for the ONE Guyana FPSO is pegged at $29/BBL Brent). Analysts at the IDEA have previously demonstrated that each new FPSO contract could add up to €1 to €2 per share in the NPV of the company’s L&O portfolio. This value already amounts to between €19 and €23 per share based on discount rates of 8% and 6% respectively. SBMO shares currently trade at €13.70.

Galliano's Financials Research

Digital strategy is being successfully rolled out to all its geographies - current valuation does not reflect BBVA's competitive attributes and strengths. Forecast dividend yield is over 7%. BBVA's premium returns engine is Mexico, where it is well positioned to counter the threat from FinTechs, as well as exploit the Citibanamex sale process to selectively poach disillusioned clients. This is supported by improving returns in Spain where BBVA remains a digital transformation leader. In addition, Turkey offers exciting growth potential and with the latest offer BBVA should be buying out the Garanti minorities at an attractive price.

Smart Insider

CEO Armin Papperger purchases €493k of stock at €205 - this purchase is notable as it comes after the stock's strong performance over the past two months, a performance triggered by the announcement of the German government to raise its military expenses. Papperger last acquired €203k of stock at €78 and this is very encouraging to see him buying again in larger size now that the stock has more than doubled. He has made 9 trades since 2018, the majority of which have been very timely. Stock Rank +1 (highest rating).

TT Equity Research

No surprise that management continues to be unable to find an anchor shareholder - no doubt they are hoping for a full acquisition to help extricate themselves from the mess that has been created, but Teun Teeuwisse suspects that any interested party will come to the same conclusion that he has: 1) Real cash generation is non-existent. 2) Net debt is materially different from the net cash reported - normalising trade working capital alone increases debt by €153m, normalised VAT and social securities adds another €55m. 3) The equity is almost worthless - €54.3m or €0.51 per share vs. current share price of €5.30.

North America

MYST Advisors

Consumer Idea Forum

MYST’s group of Consumer specialists offered a diverse set of ideas ranging from M&A beneficiaries, capital return stories, “Value” bellwethers and potential overearners. Three of the most compelling ideas presented included…

Amazon (AMZN) - Self-help story with renewed focus on costs. AWS growth slowdown is temporary. Trades below tough valuation. TP $4970 (100%+ upside).

Jack in the Box (JACK) - Capital light with high margins and minimal cyclicality. Mispriced at 12x P/E (vs. peers at 20x+). TP $250 (200%+ upside).

MGM Resorts (MGM) - GGR growth to stall and margins contract even without a recession. With no fat left to cut, a 1% decline in GGR could wipe out FCF entirely. Selling real estate portfolio was “insane” given the permanently escalating rent MGM must now pay. TP $20 (40% downside).

Two Rivers Analytics

Solvency Risk Model: Best short candidates

Carvana (CVNA) - Cash burning, high capex and weak earnings. $5bn of net debt before Adesa acquisition and forced to accept some expensive debt terms to finance the deal.

Life Time Group Holdings (LTH) - Low on cash and not slated to produce excess cash flows any time soon. Estimates are being cut aggressively. Short interest is high at 15% of float.

Surgery Partners (SGRY) - Leverage is very high at 11x forward EBITDA. Growth slowing and the stock is expensive relative to historical multiples (23x 2022 and 20.5x 2024 EBITDA). Has increased share count by 72% over 18 months.

Boyar Research

Has Dotdash Meredith found hidden value in underappreciated brands? Jonathan Boyar discusses how Meredith’s legacy brands can help the company achieve the scale it needs to spin out of IAC and become an independent company making the $2.7bn acquisition look like a bargain. Dotdash has developed an effective playbook for building digital lifestyle brands and by engaging readers in their content (rather than treating them primarily as a conduit for advertising) it makes it an increasingly appealing alternative to large-scale subscription-based ad services run by the likes of Facebook and Google.

Huber Research Partners

Craig Huber makes the case for a $200+ stock price by year end - the media company will continue to outperform due to its attractive valuation, high FCF, historically low leverage, and expected very strong political ad revenue. NXST trades at only 6.1x Craig's average 2023/24(E) EBITDA and 8.9x (11.3% yield) unlevered FCF vs. Scripps at 8.0x, with a debt ratio of 5.5x (NXST 3.1x). FCF (after dividends) to total $4.3bn in 2022-24E, which is 65% of the current M/Cap. Note that his estimates do not include any benefit from being able to further monetise spectrum. Craig believes the share price will hockey stick up once the first material spectrum leasing deal is announced.

Quo Vadis Capital

Shares continue to trade on the company’s LT unit growth potential even as the financial profile of the business weakens - 2Q22 guide for profit per average unit implies 30%+ below pre-covid levels. ROIC is in the low single digits and below WACC. Rather than invest copious amounts in non-productive G&A, John Zolidis argues the company should slow unit growth and reinvest in its stores. The current consumer proposition (menu, price/value relationship) just isn't that compelling relative to alternatives. The Street thinks SHAK will inflect to a profit in 2023. John remains unconvinced.

Portales Partners

Quality on sale - Charles Peabody sees positive operating leverage emerging, capital being rebuilt, and management earning its spurs as the culture of SunTrust blends with that of BB&T. As cost cuts meet the impact of higher interest rates, TFC will generate some very impressive returns with premium valuations to follow. Re. the wider banking sector, Charles has urged caution over the past half year having officially turned bearish last October. However, he has recently been selectively upgrading names with TFC joining JPMorgan and Wells Fargo as Buy recommendations.

Expected a blowout quarter but 1Q22 came in even better than Northcoast’s most bullish expectations. Furthermore, in another positive surprise, CSL now expects to achieve its Vision 2025 this year. The biggest question going forward will be the sustainability of margins in CCM. Margins have been on a steady climb for the last several years and given the favourable dynamics and changes that have occurred in the industry, it is very possible margins continue to reset higher. Northcoast increase their 2022 EPS estimate to $17.45 (was $14.95) and 2023 EPS to $19.00 (was $16.15). TP increased to $320 (30% upside).

Paragon Intel

CEO Patrick Gelsinger remains overly optimistic about INTC's growth prospects and long-term margin structure - Paragon Intel continues to be highly sceptical that INTC will benefit from a “sustainably” larger client base. They also argue that full year gross margin guidance of 52% (which implies an improvement in 2H22) is unrealistic given the ramping of newer process nodes typically come with lower yields. Ongoing share loss in DCAI and a potential sharp decline in PCs means double barrelled gross margin declines are inevitable.

Abacus Research

Quality, growth, and a small macro tailwind - PAYC is well placed to beat street estimates. The company is effectively filling a gap in the mid-market for an integrated solution of Payroll and HCM products. This gives it a sustainable high growth rate for many years. Its proven profitability model is a key differentiator among other high growth SaaS companies. Meanwhile, low unemployment means it is even more important for employers to offer benefits to retain employees. These packages need additional HR modules providing upsell opportunities. Rising rates is also a tailwind for earnings due to interest on float at ~100% incremental margin. TP $390 (45% upside).

Japan

LightStream Research

Russia exposure is not as much as markets feared and there’s upside to DPS guidance - 1Q22 was stronger than expected with revenue and operating profit surpassing consensus by 5.2% and 20% respectively despite the Russia / Ukraine war. Although the company has maintained the semi-annual dividend at ¥75 per share, Oshadhi Kumarasiri sees room for ~¥25 per share upside to JT’s FY22 DPS guidance. With operating profit expected hit ¥534bn, the stock should trade above ¥4,000 per share, indicating upside of over 80%.

Emerging Markets

Copley Fund Research

Utilities ownership among active Asia Ex-Japan funds hits lowest levels on record

With risk assets taking a turn for the worse it is surprising that a safe haven sector is so far out of favour (average fund weight is just 0.98%) - the record underweight has been driven in large part due to benchmark increases in stocks that active managers have ignored (Adani Green Energy, Adani Transmission and Adani Gas). However, one can’t ignore the record low participation levels, with just 41% of managers exposed to the sector. With Aggressive Growth investors all but abandoning Utilities and only 35% of Growth investors holding a position, if risk assets continue to deteriorate, some of that rotation away from the sector should start to reverse.

Gradient Analytics

Thesis playing out - volume-based procurement has crushed two of AK’s largest segments and AK now expects Spinal and Trauma products to suffer the same fate during 2022. The company has reorganised its segment reporting as it tries to obscure the declines in its key applications. Longer payment terms continue to benefit sales as growth in aged accounts accelerated in 2H21. AK also increased its inventory by double digits y/y even as sales collapsed. The dividend payout has been reduced by 37.5%. The shares are down 46% since Gradient's initiation but further downside is anticipated.

Horizon Insights

The global market potential for ophthalmic drugs, consumables and devices will exceed US$100bn in the coming years - as a highly innovative company with strong R&D capability Eyebright looks well placed to benefit. Its existing major product lines are: 1) Cataract Intraocular Lens (IOL) - Eyebright’s market share has doubled from 5% in 2018 to 10% in 2021 (without profit margin erosion) and domestic brands are expected to continue to take market share from foreign brands. 2) Orthokeratology Lens (OK Lens) - Eyebright has seen a phenomenal increase in sales having sold 21.5m pieces in 2021 vs. 2.3m pieces in 2019!

From a credit fundamental perspective Azul’s unsecured debt has performed very well in the last three months and remains attractive considering the likelihood of further significant operating and financial progress in the current quarter. However, given the high volatility in the market Reno Bianchi believes an interesting way to play the Latin American unsecured airline market is to go long Azul 7.25% due 2026 while shorting GOL 8.0% due 2026 at an around flat yield level. This swap has the additional benefit of receiving ~4pts upfront while the same swap at the end of Feb would have required paying ~6pts upfront.

Churchill Research

Mike Churchill sets a 12-month TP of R$8.46 (70% upside) for this consumer electronics distributor - based on 9x 2024 earnings (10.5% FCF yield) which seems fair given its growth rate, net income margins of ~10% and solid balance sheet. It appears Multilaser's IPO last year was time to capitalise on the lockdown boom. The share price has followed a similar pattern to former Brazilian glamour stock Magazine Luiza, which was all the rage a year ago (billed as the Brazilian Amazon), but has since fallen by 80%. However, the big difference between the two stocks, is that Magazine Luiza still trades at 100x earnings and 2.7x book vs. Multilaser at 6.8x earnings and 1.1x book.

Macro Research

Developed Markets

Belkin Report

Heading down

Michael Belkin explains that investors were lured into a major stock market bubble by excessive stimulus. Now the stimulus is being withdrawn, the warped asset prices are now reversing, and the stock market decline is accelerating with margin debt and hedge fund liquidation keeping pressure on equities. Michael has several recent major changes in his portfolio, including LONG US TNote and TBonds, LONG Eurodollar futures, and a closing out of all long commodity positions, including energy. Investors should look to sell and short brief stock market rallies, BUY the TLT TBond ETF and BUY volatility.

CrossBorder Capital

The big liquidity squeeze continues

Weekly balance sheet data from major Central Banks show liquidity in local currency terms edging lower (latest -6.3% 3m ann.). The US Federal Reserve has led the 2022 downturn. This tightening has propelled the USD higher, forcing monetary adjustments in USD-linked economies. Mid-week saw not only the Fed hike rates but also the Reserve Bank of India and Brazil among others. Furthermore, non-US Central Bank liquidity is being devalued as the dollar strengthens. In USD terms, global liquidity is shrinking by some 24% (3m ann.): Michael Howell’s liquidity indicator started in 2010 and has never been so low.

High Frequency Economics

UK: A hike into a recession

Carl Weinberg is fully aware of the Bank of England’s price stability mandate, but their latest decision certainly isn’t a wise one. We are living in unusual times with an impaired supply curve heating up inflation, so why would the BoE seek to reduce the demand curve to match this? The MPC is ignoring the obvious problem: energy prices are rising faster than other prices! Carl says a negative or zero interest rate is needed, otherwise the BoE is marching us into recession at an even faster rate than is necessary.

Global Macro Investor

Germany: A bleak outlook

Inflation is having a toll on German consumer confidence and the manufacturing sector. Short-term industrial growth has peaked, confidence is low, growth in factory orders is about to contract and consumer credit growth is rising, which could prove to be a problem due to short-term rate growth. Raoul Pal isn’t optimistic. We’re going to see the country enter into recession this year, and it’ll struggle to get out of it.

Minack Advisors

US: Negative shocks have only delayed an equity rally

Gerard Minack comments that the resilience of equities he expected in the face of Fed tightening was too focused on the historical narrative, not considering enough the massive recent global shocks. However, he reaffirms his belief of US resilience and no recession until at least 2023. Once it becomes clearer to the markets that inflation is decelerating and that the US has coped with the first phase of policy tightening, there is scope for a tradable equity rally.

Macro Hedge Advisors

US: Long-term interest rate markets are broken – not just in Japan

Under a global market economy and a good regime, long-term interest rates would be set entirely free of official intervention and speculative decisions. Reality is painfully proving to be the opposite. The bunkum concept of the neutral interest rate is distorting the facts and leading investors down the wrong road, which Brendan Brown discusses in his latest report. He predicts that although 2% inflation may again be obtained in 2023-24, other episodes of high inflation now lie further ahead, and the US economy is heading into a financial crisis.

Beacon Policy Advisors

US: Charting the path forward on student loans

The call for action on student loans has become a progressive rallying cry that could help the President’s standing among disappointed voters. Reports suggest a $10,000 forgiveness per borrower is being considered to test the waters both against political blowback from the right and potential inflationary risks. Any form of debt cancellation could have a materially adverse impact on the loan refinancing companies, including SoFi and Navient, but the greater amount of cash at hand at consumers could be a positive for the consumer discretionary sector.

Emerging Markets

Totem Macro

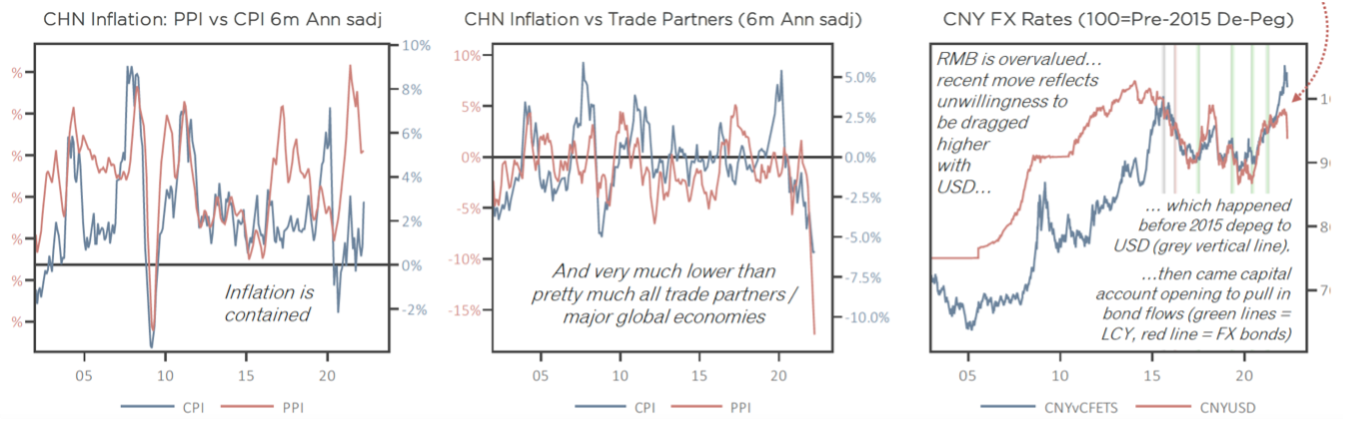

China: Stimulating questions

Whitney Baker remains firm in her belief that Beijing is not stimulus constrained: inflation remains low as does inflation differentials vs trade partners, and the recent FX move is a USD-specific phenomenon (see graph). The matter of fact is that China is currently easing. Unfortunately, it’s not enough, but expect more to come. Signs of stabilisation in the property sector are appearing, and worried investors should remind themselves that the borrowing drought is self-imposed; Beijing is able to reverse it, and they’ve already started.

Greenmantle

China: No end in sight

Fearing Covid mismanagement, local officials are now quick to escalate restrictions and slow to unwind them. Niall Ferguson predicts further downside to Chinese consumption and assets, including equities and real estate. Beijing’s monetary and fiscal responses will remain subdued in spite of growth concerns. Niall expects some moderately positive tailwinds for industrial metals and agriculture on the back of increased infrastructure spending and food stockpiling but expresses concern over Chinese vulnerability to new Covid variants, especially when winter arrives.

PRC Macro

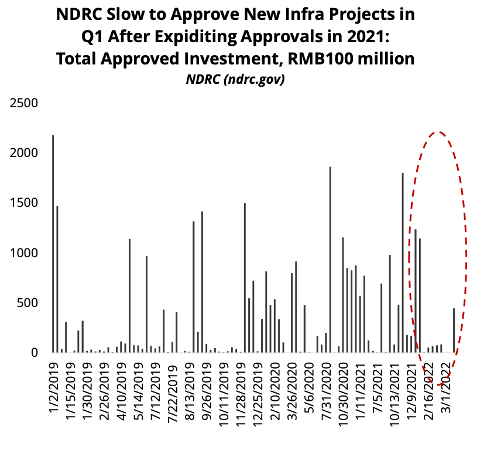

China: Will hopes for infrastructure stimulus fade?

Market hopes for stimulus are running high, but William Hess’s review of NDRC infrastructure project approvals and domestic resource flows suggests lower-than-expected progress on approvals on spending. LGFV bond issuance - a key source of leverage for local infrastructure investment - is down on a YoY% basis, raising the risk that such projects may be underfunded. William still expects Beijing to deliver additional stimulus soon, but market expectations for commodity demand will remain disappointed. He remains bearish on steel, copper and aluminium.

Andrew Hunt Economics

India: Short-term caution, long-term optimism

A poor economic outlook and the perennial problems of a large budget deficit, with the resulting domestic savings shortage, means Andrew Hunt has little optimism vis-à-vis Indian equities in the near-term. Yet, productivity is strong, CAPEX is healthy, and CPI is not hypersensitive to import price trends. Andrew believes that if the country can maintain positive FDI and service sector export trends, there is no reason it cannot remain one of the worlds’ fastest growing economies.

Signal Risk

Somalia: One extension, please

The Somalian government has requested a three-month extension on two credit lines - equivalent to USD $395m - due to expire on May 17th. The request comes as the country’s presidential election is scheduled for May 15th, with it being unlikely a new government will be installed in time to renew the funding arrangement. Funding from the IMF and other multilateral and bilateral organisations is paramount to maintaining fiscal stability in Somalia. Will the IMF agree to their request?

Teneo

Argentina: CFK duel with Fernandez points to planning for 2023

The civil war within the governing Front for All (FdT) coalition has recently intensified, with an increased spate of attacks against the economic-policy making team, the IMF agreement and President Alberto Fernandez. Such attacks wouldn’t occur without a green light from VP Cristina Fernandez, as it becomes clearer that the offensive is not just about recent events but her longer-term goal to remain politically relevant for the 2023 election. Ultimately, it comes at the cost of risking increasing government dysfunction and destabilisation.

Llewellyn Consulting

Ukraine: The financial cost of war

The Marshall Plan and the reconstruction of Europe cost the US 1% of its GDP. $150bn is needed to restore Ukraine’s destroyed capital stock, and a further $75bn/yr in annual financial support (declining progressively to zero after five years). This all amounts to just 0.25% of the combined GDP of the US and EU, or 0.5% of the latter. Preston Llewellyn comments that such figures are an order of magnitude smaller than the increases in government spending following the 2008 financial crisis and the 2020 pandemic.

Commodities

Topdown Charts

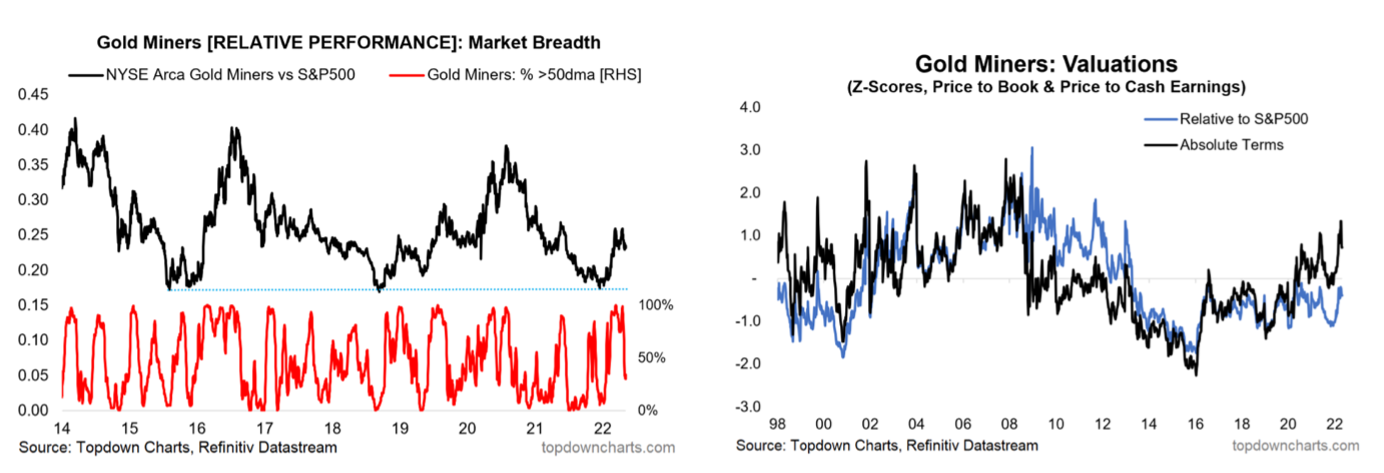

It’s all going wrong for gold

Sentiment/technicals/flows have turned down from overbought levels, and the gold price itself failed to break out to new highs and is now testing support. Rising real yields, strengthening USD, rate hikes and QT present real headwinds to gold. The value indicator has come down to neutral so it’s no longer expensive, but Callum Thomas claims it still isn’t cheap; absolute value range indicators look pricey, and relative value (vs S&P500) is at the top of the recent range. Drop the bullish gold miners call and go neutral.

J Ganes Consulting

Bearish bias across the softs

Judith Gaines remains fairly negative across the Softs Complex, citing USD strength and demand concerns. Coffee recently stood out with markets racing up on cold weather forecast, although Judith sees the gains disappearing just as quickly as they came. True, there are some underlying bullish features, but the market has already considered this. It would take dollar weakness and another shock to get the market moving back up, and Judith believes the market is overstaying its welcome over $2.

Greenmantle

Crypto: Terra Non Firma

Terra’s fall to earth will add to the downward pressure on other cryptocurrencies. However, Niall Ferguson explains that Terra is a special kind of crypto best described as a “coupon coin.” These have failed in the past and will fail again in the future, no doubt. This should increase risk aversion, compounding the downward trend in crypto assets as rising interest rates bite. A Darwinian process is at work and higher rates should mean that the less fit forms of blockchain-based token will not survive.

CPM Group

2022 silver market forecast

CPM Group has recently released the latest edition of its long-running Silver Market Forecast and Yearbook, with unparalleled insight into silver markets. Topics include the organisation of retail investors, bullion banks and ETFs, physical silver and derivatives, and more. For a small taste of CPM Group’s view of the market click here.