Company & Sector Research

Europe

Vision Research

3 new Consumer short ideas

Vision has issued 3 new consumer shorts in the past 3 weeks, 2 being European and 1 US. The most recent European short has a market cap >$3bn, trades >$25m/day and SI% <10%. The company has experienced market share losses and is seeing new entrants from Asia, potentially over-earned during the pandemic, has bullish estimates, and channel inventories that look bloated. European short ideas Vision has closed over recent months include Allegro (55% alpha), Colruyt (40%), Thule Group (>30%) and Nokian Tyres (>20%).

TT Equity Research

Manipulating its way to reaching targets - delivery on near-term objectives (predominantly FCF) has been driven by management’s "creative solutions". Competition, cost and wage inflation should maintain pressure on profitability. Simple cost analysis shows that sustainably lifting the operating margin towards the targeted 4% seems impossible unless costs are capitalised, provisions released or costs are reclassified to “other income and expenses”. Cash generation has been driven by deteriorating the quality of working capital. This will become increasingly difficult. At some stage stretched payables should reverse which will further increase debt. 50%+ downside.

Woozle Research

88% of payment specialists interviewed by Woozle expect Adyen’s share of payment volumes to increase in their companies, as well as Adyen's overall market share to increase during the next 6 months - strong performance will be driven by its reliable unified commerce system, omnichannel presence, and superior integration capabilities. The few negative comments refer to the processor’s lack of flexibility in solving specific use cases for merchants, as well as the quality of the company’s fraud tools, compared to alternatives.

Arete Research

Jim Fontanelli thinks IFX’s portfolio has one of the most defensive revenue mixes in semis going into a 2023 demand environment where consumer is the lead concern. He also believes IFX’s share loss headwind in EV’s (in the transition from IGBT to SiC) is coming to an end as it brings additional SiC capacity on-line through 2023 and 2024. IFX has seen a notable de-rating over the past 18-months - moving from a 5-year average 30% P/E premium to the SOX to a 16% discount. Jim thinks this is harsh, given IFX’s total and autos revenue growth has outperformed peer average. TP €39.30 (45% upside).

Stockcube

Europe Top 200 Weekly Technical Strategy report

Buy-the-dip - Indices have rallied into short term downtrends but recent lows should hold. At a sector level, Energy reasserts medium term uptrends, Basic Resources approaches resistance, Retail develops a short term price and relative base, Chemicals encounters short term downtrends, Industrial Goods encounters medium term downtrends and Media encounters medium term relative resistance. Stockcube’s Model Portfolio is 26% net long (34 longs / 20 shorts) with very small sector positioning. This week they opened longs in Sika (forms short term bases) and Neste Oil (reasserts medium term uptrends).

North America

New Street Research

Guidance up. Targets up. Valuation up - EBITDA beat estimates and guidance raised (consensus is too low for 2022). New Street now assumes FYBR deploys fibre to 11m locations rather than 10m. The company adds $2bn+ in equity value for every 1m locations they upgrade ($9/share). There are another 1m locations that could be upgraded organically and 3-4m that could be upgraded with subsidies that New Street are ignoring for now. TP increased to $126 (380% upside). FYBR remains the most compelling way to invest in broadband infrastructure.

Huber Research Partners

Using Craig Huber’s 2024 EBITDA estimates and segment multiples in his SOTP analysis suggests that the current price is implying an overly punitive 42% conglomerate discount to NWSA’s valuation. If management won't break up the company, then they should at least sell / spinoff Subscription Video Services and break out Professional Information into its own segment. Craig notes that there are signs that NWSA’s portfolio is moving in the right direction including some shrewd acquisitions as well as content licensing deals with Google, Facebook and Apple, but the stock has been trapped in underperformance (7 of last 9 years) and something big needs to change here.

MAPsignals

Unusual buying strengthens, why you should bet on Discretionary

Betting on the Consumer Discretionary group is a mean reversion trade - the worse the performance has been, the better the outlook. The sector has outperformed the S&P 500 by an average 5.8% in years following its weakest 12 month stretches. Now, if you’re worried about the macro situation deteriorating…the recent negative Q2 GDP print has in fact historically been a contrarian buy signal. Furthermore, MAPsignals’ data shows the Big Money (institutional capital) has recently begun piling into more and more discretionary stocks - the most in 6 months. Click here to read more.

Off Wall Street

Checking in with the hotels - bearish thesis on the Midscale hotel segment playing out; unit growth story appears to be broken. OWS’ latest field work finds little evidence that franchisees are interested in building new units. ADR price inflation should begin to reverse as the labour market improves. This should weigh on RevPAR (and franchisors’ royalty revenues). Furthermore, OWS found evidence that demand in key areas is softening.

TobaccoIntelligence

Doing better than expected - VLN ready to expand way beyond Chicago trial

22nd Century Group said its very low nicotine (VLN) cigarettes pilot in Chicago is exceeding expectations, leading the company to accelerate its launch plans, including taking VLN into the Colorado market in September. The company also plans to target additional markets in Asia and Europe and to apply early feedback from the South Korean market further to refine the packaging, product and marketing mix ahead of a more comprehensive launch project.

Memphis Research Group

Over the last 4 quarters GSHD has experienced increased churn within its agent base and a slowdown in the recruitment / signing of new agents (both in-house & franchise). This at a time when its go-to-market strategy should be yielding cyclically high agent income. This is the “canary in the coal mine” moment for its “disruptive” business model. Memphis’ field work indicates that GSHD’s agent compensation model can only thrive in certain limited markets, the vast majority of which are already populated with the company's agents. The slowdown in residential home sales will severely expose the limited TAM of GSHD’s model beginning now.

Abacus Research

Abacus' 40-page initiation report finds the market is too bearish - 2022 is an anomaly. ALGN's business model and competitive position have not been impaired. Downgrades were part of the pandemic dislocation and management’s over-optimism. ALGN’s near monopoly position unlikely to change (the D2C model has basically failed and Abacus cannot see any way for it to be revived). Forecasts earnings to grow at a 30% CAGR from 2022-25 driven by a recovery in revenue growth and operating margins. Forward P/E is below historical average and low relative to peers; sees ~80% upside over next couple of years (TP $514).

Singular Research

This undervalued small cap is poised to see much higher than expected growth - outperformance to be driven by KE’s impressive order backlog (>$1bn), improved leveraging of its completed facilities, and a continuing easing of global supply chain constraints. Singular’s new FY23 estimates are for sales to rise by 20.6% to $1,627m and EPS to rise by 99.3% to $2.47. Forward P/E of 8.4x is lower than the average competitor. 12-month TP increased to $31 (30% upside) - blended valuation methodology (50% relative P/E ratio and 50% DCF model).

New Constructs

Economic earnings, the true cash flows of the business, have plummeted from $47m in 2011 to negative $743m over the TTM. Falling NOPAT margins and invested capital turns have driven ROIC from 7% to 3%. To justify its current price, Realty Income must improve its NOPAT margin to 49% (vs. 36% TTM) and grow revenue by 14% compounded annually for the next decade. Given that NOPAT has grown by just 8% compounded annually since 2016 these expectations look overly optimistic. 40%+ downside.

Summit Insights Group

Beating expectations - investments in R&D and S&M paying off as the revenue acceleration continues for the fourth consecutive quarter. Srini Nandury expects this outperformance to continue for the rest of this year and into 2023. He likes the aggressiveness of management and expects QLYS to continue to make tuck-in acquisitions to round out its product offerings. Following 2Q22 results, Srini has significantly increased his EPS estimates for FY22 and FY23 (which were already materially ahead of consensus) to $3.59 and $4.11 respectively.

Blueshift Research

Unlikely to see a resurgence in its growth prospects anytime soon - faces major challenges across each of its key segments. Blueshift’s sources were highly critical of COUP’s approach to its flagship spend management platform, disparaging the company for having unknowledgeable sales reps, using far too aggressive sales tactics, and allowing its technology to fall behind competitors in important areas. One contact said his large national grocery chain might consider alternatives if COUP fails to innovate. In addition, sources were mostly sceptical about the company’s upside in supply chain software following its $1.5bn acquisition of Llamasoft.

280First

Rapidly detecting meaningful language changes in 10Qs / 10Ks

Analysis of the data and subsequent insights are driven by AI, NLP, data analytics and qualitative analyst oversight. Recent examples:

New Relic (NEWR) - Added the following wording to its 1Q23 10Q, “Businesses may look to rationalise their spending in response to such factors, which may impact our sales and renewal rates and negatively impact our business”.

Broadridge Financial Solutions (BR) - Added to its 2022 10K, “And the loss of any of such clients could have a material impact on our revenues and also result in an asset write-down of our client onboarding costs”.

Avnet (AVT) - Clear concerns re. cancellations, inventory and pricing.

Advanced Micro Devices (AMD) - Minor amendment to its 2Q 2022 10Q suggests they are more positive on cash flows.

Australia

Global Mining Research

OZL rebuffs BHP's A$25/share cash offer - goal is now to try and extract a higher bid, but with limits as it is not a “must have” for BHP (11% more copper, but not worth the effort from an EBITDA perspective; main appeal is safe jurisdiction with assets near one of BHP’s key mines). OZL’s Carajas projects would likely be sold, but West Musgrave is an interesting potential growth asset. The offer price is equivalent of US$0.26/lb of OZL’s contained copper in resources, which is on the lower side to recent deals. For 2023, GMR estimates the combined copper assets would have a sales revenue of ~US$3.6bn, EBITDA ~US$1.4bn, copper production ~340kt and an AISC ~US$2.20/lb.

Japan

LightStream Research

Turning a corner - the share price has fallen 55% over the past 18 months, but is up c.25% from recent lows and has seen higher than usual trading volumes, suggesting plenty of investor interest. With narrowing Mobile losses and outperforming E-commerce and Fintech, Oshadhi Kumarasiri thinks it is unreasonable for Rakuten to trade at a 40% discount to the bottom end of the long-term trend channel and feels an appropriate EV is somewhere around ¥2,000bn. This would put Rakuten on 9.0x consensus FY+2 EBITDA which seems more than fair considering the company’s growth and historical multiples.

Emerging Markets

Periscope Analytics

Is looking to sell up to 118.176m shares to raise up to US$2.5bn - pricing at HK$143.5-165.5/share is a 38.6%-29.2% discount to China Tourism Group Duty Free (601888 CH). Brian Freitas believes the stock could be added to MSCI China Index in November and to the FTSE All-World and FTSE China 50 indices in March. Southbound Stock Connect could come online on 19 September providing opportunities to trade the A/H spread.

Tabbush Report

Indonesia is seeing a strong recovery in lending growth, which adds to the positive trifecta for BNI - improving margins (NIM up from 4.5% to 4.9% in 2Q22 Q/Q. There are few banks in Asia-Pacific that show this type of NIM expansion), with improving loan volume, and better credit metrics (BNI is one of those banks that appears to have taken far too much credit costs during FY20 and FY21). It just so happens, that BNI’s market capitalisation of IDR154tr is a fraction of the IDR970tr for comparable peer bank Bank Central Asia.

Copley Fund Research

Turkey: Time to buy?

Every time Steven Holden looks at Turkish allocations among active EM investors the picture looks worse - all 4 of Copley’s ownership metrics have fallen to all-time lows, something Steven doesn’t recall ever seeing before. Just 40% (of 275 funds covered) have exposure to Turkey at an average weight of 0.44%. The bulk of the holdings distribution lies below 2%. The most widely held company is BIM Birlesik (12.7% of funds invested). The banks are almost universally avoided. High conviction fund holdings are led by Mobius Emerging Markets in the small-cap names of Logo Yazilim (2.9% stake) and Mavi Giyim Sanayi (2.67%).

Macro Research

Developed Markets

Alternative Macro Signals

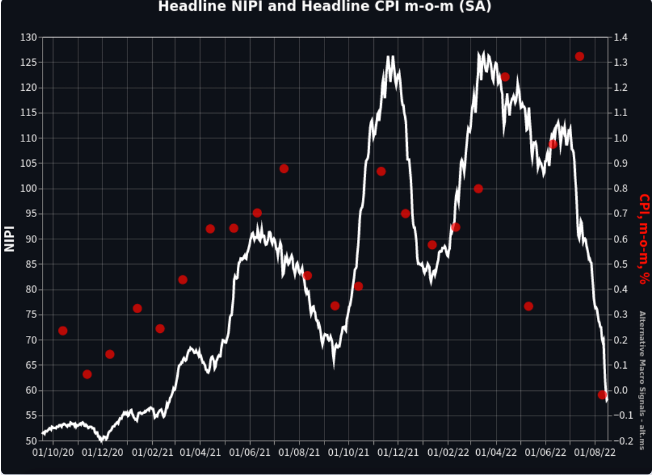

Forecasting inflation with NIPI and NVI

Alternative Macro Signals’ News Inflationary Pressures Indices (NIPI) can be used to spot inflation turning points and forecast trends. The chart above shows the NIPI (white line) and US CPI releases (red dots) as of release date; the NIPI is available daily and without lag. Prior to US inflation surprising consensus to the downside, the NIPI indicator has done a good job signalling upside risks. It continues to excel and has been signalling a negative turning point in a timely fashion, with the usual 1-2 months lead. Combined with the News Volume Index (NVI), we can see how quick and pronounced any turning points will be.

Click here to read more.

Longview Economics

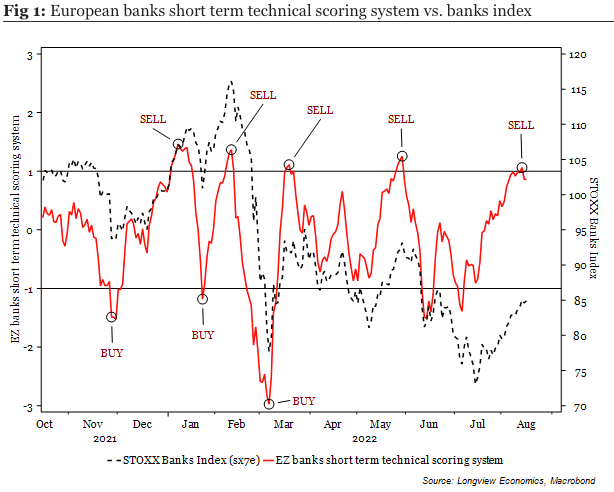

Eurozone banks

With evidence suggesting that the bear market in global equities will endure, Harry Colvin suggests investors should look to trade Eurozone banks, which typically underperform in bear markets. With high recession risks in Europe, tight credit and monetary conditions, further weakening in credit growth and money supply, Harry’s short- and medium-term models are generating a clear SELL message. Move SHORT Eurozone banks (Sept futures, Bloomberg code CAU2 index), with 75% of the position at current levels and the final 25% on strength, if forthcoming (i.e., at 86.20). Place stop at 88.7 and risk 100bps on this trade.

Aitken Advisors

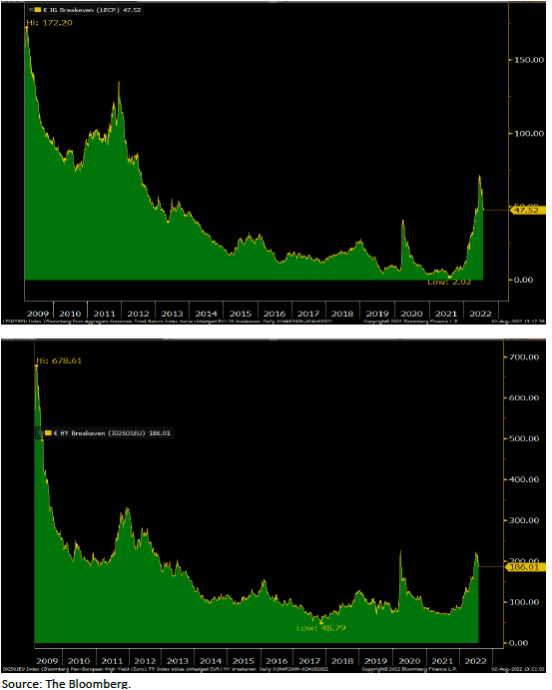

European credit breakevens

James Aitken opens up his latest report with something a bit unusual. In credit, the breakeven spread can offer insights into whether there may be a margin of safety in corporate bonds, or not. Chart 1 above shows that in June, at an index level, European investment grade credit breakevens (at ~70bp) were well through the pandemic peak, leading some to conclude that at a broad level, European investment grade credit provided a healthy cushion against future rate or future spread widening. Chart 2, showing that in June European high yield credit breakevens revisited the pandemic peak, also led to the same conclusion as above. The takeaway? As awful as the European economic outlook and energy insecurity situation would appear to be, if your clients pay you to take risk, then that’s what you do.

CrossBorder Capital

Fed’s QT summer lull weakens US Dollar

Michael Howell comments that the latest weekly balance sheet data from major Central Banks show aggregate liquidity in local currency terms shrinking by just 3.5% (3m ann.). The same trend is evident in global liquidity measured in USD but to a much greater degree. The lull in Fed QT continues and has coincided with dovish comments by Fed Chair Powell that the Fed funds rate has reached a “neutral” level. This has thus far outweighed a faster pace of tightening at the ECB and BoJ. The USD has reacted accordingly; from its mid-July peak, when the US unit hit parity with the €, it has lost some 3% versus the euro and pound sterling, and nearly 4% against the yen.

Benderly Economic Insights

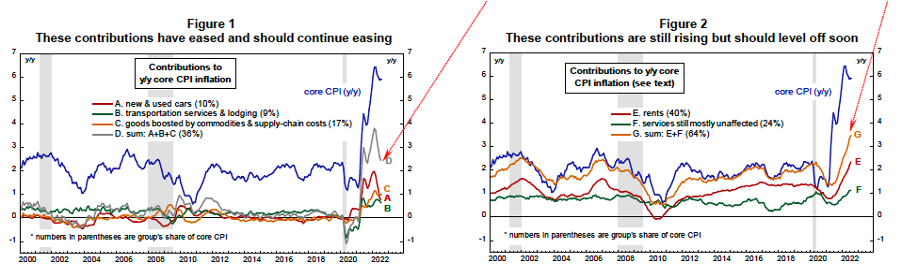

US: Inflation not as entrenched, nor as broad-based as feared

Total CPI remained unchanged in July and falling energy prices in August should produce a small m/m decline in total CPI, lowering the y/y increase to about 8% from 8.5% in July. Core CPI increased 0.3%, originating from prices that previously had been boosted the most by supply/demand imbalances and supply chain disruptions. Much of these increases are a reset to relative prices and their boost to inflation will end once the reset is over (see figure 1). Figure 2 shows the contributions from the rest of the core CPI which are now levelling off at a 3.5% contribution.

Musha Research

The sophistry that Abenomics has failed

Musha Ryoji’s latest report looks at the legacy of Abenomics, denouncing many of the false claims made against the era of Shinzo Abe. His key takeaways include the significant employment growth and women’s entry into society, the dramatic improvements in corporate earnings and tax revenues, improved pension finances and a positive impact on health and wellbeing. Abenomics has defined Japan’s modern history, and due to the diplomatic initiatives of the Abe administration, we will see the significant economic results come to fruition over the coming years.

Valens Research

Market Phase Cycle framework

Valens Research uses a systematic framework called the Market Phase Cycle to be able to simplify the signals the market is seeing. By starting with market cycles and drilling down into equity and credit valuations and market sentiment in a consistent repeatable way, the framework can help investors see better short-term and long-term signals for client asset allocation. In this day and age of significant market swings in response to any recessionary signals from the Fed, commodity prices and interest rate movements, a systematic macro framework can ensure investors have stronger conviction with their individual stock selection.

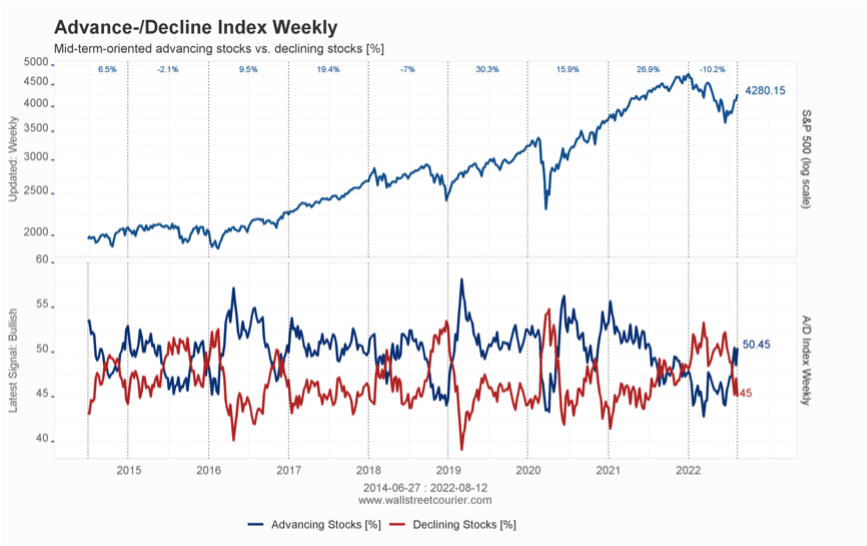

WallStreetCourier

Chart of the fortnight

Robert Koch comments that the current rally in the S&P 500 is based on broad leadership (as the percentage of advancing stocks is outpacing the declining ones). Historically, such a high tape quality was quite supportive for risky assets.

Emerging Markets

Andrew Hunt Economics

Asia: This time it’s different

North Asia faces its biggest economic challenge since 1997, according to Andrew Hunt. As policymakers expand their foreign exchange reserves to buy time for their private sector borrowers to discharge FX debts, we are seeing a race between the rate of depletion of Asia’s reserves vs. the Fed’s rate of tightening and the rate of foreign debt repayment by Asian entities. If Asia starts to lose the race, expect sharper rates of decline in Asian currencies, which Andrew sees as possible in Q4/2022. He expects very weak growth trends in the region and continued pressure on Asian exchange rates until year’s end.

Copley Fund Research

The ASEAN rotation

In Steven Holden’s latest report, which features a comprehensive analysis of active EM fund positioning in the ASEAN region, he finds that the region has been a key beneficiary from a drop in EM Europe allocations following the Russian exodus. Indonesia and Thailand have captured the lion’s share of the rotation, whilst investors sell down stakes in non-benchmark Singapore exposure. Above all, this rotation comes at a time when allocations are at their lowest levels on record for many countries in the region.

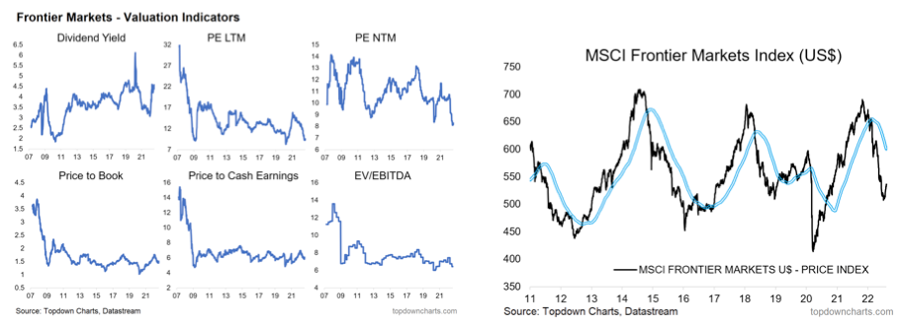

Topdown Charts

Moving bullish on frontier markets

After a -26% drop, Callum Thomas claims frontier market (FM) equity valuations are much improved, looking cheap on a number of metrics (see charts). Technicals are also improving, with breadth metrics tentatively turning up after going oversold, and the MSCI Frontier Markets index bouncing off support. Callum also comments on EM FX, with recent EM currency weakness pushing the valuation indicator into extreme cheap territory. With the highest expected returns, Callum is bullish FM equities.

Greenmantle

Argentina: Stepping away from the brink of a big economic hole

Newly appointed Economy Minster Massa is going into his third week on the job with more promises than certainties. He has announced some fiscal consolidation steps (~0.5% of GDP) and Niall Ferguson expects him to push further liquidation of agricultural exports. But stepping away from the brink does not make Argentina’s economic hole any smaller. Shortages will hinder economic growth, inflation is running at ~100% annualized rate, and reserves are at dangerous levels. Despite Massa’s proven political abilities, Niall is sceptical his honeymoon can alter the dire economic dynamic that will lead Peronism to a defeat in 2023.

Variant Perception

Brazil: Government bonds an investment opportunity

VP's Brazil leading indicator for growth has ticked up, driven by a higher manufacturing production tendency. Inflation has also converged lower with his own inflation model which indicates that the hiking cycle is now coming to an end. Money markets are starting to price in cuts, which has preceded a more meaningful bond rally; VP is BULLISH Brazilian local government bonds, currently his favourite EM investment. EM currencies tend to sell-off into an election, and bottom on the date, and VP comments that this is the last major overhang for Brazilian assets.

PRC Macro

China: Rate cuts strengthen PBoC’s defense of RMB

William Hess sees the PBoC strengthening FX intervention to confine USD/CNY within a narrow range between 6.6-6.9 ahead of the party congress, and market speculation over risks of USD/CNY devaluation will only strengthen the PBoC’s resolve. The focus of PBoC intervention will be concentrated in the relatively thin offshore USD/CNH market via intervention by state-owned banks with the goal of compressing the onshore/offshore FX spread. William also forecasts interbank rates staying lower for longer in the absence of a major credit impulse associated with land/property sales, and also because William expects further cuts to mortgage rates and average corporate borrowing costs.

Horizon Insights

Inflation’s impact in China

Horizon Insights’ latest report looks at the inflationary environment in China, examining the structural trends that have occurred in the fallout of Covid and the Russia-Ukraine war; such trends are often overlooked amid the headline numbers but are crucial in long-term investment. The trends indicate lucrative potential equity returns in some sectors, with the report highlighting China’s beer, frozen food, and chain restaurant industries, where their sustainable pricing power and upside are becoming more evident in their recent grassroots channel check. Expect the structural rebalances within the economy to continue in the months ahead.

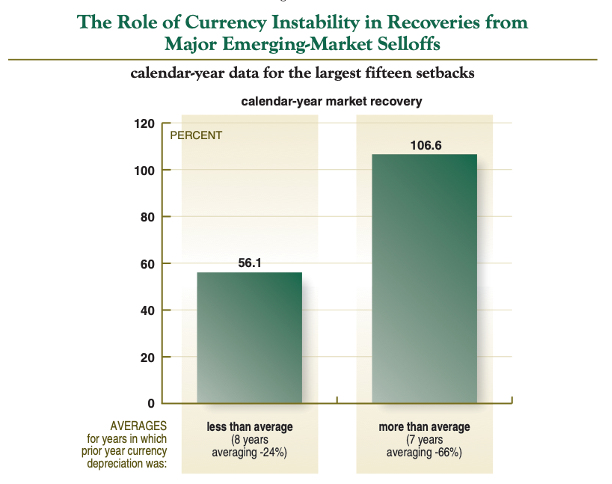

HCWE & Co.

Why it pays to invest in the dogs

In his latest report, David Ranson examines large EM setbacks since 1975 and subsequent market trends. He finds that supernormal returns can indeed be expected after a big fall in a country’s stock market, with the bulk of the rebound occurring between 8-15 months after the end of the setback. Interestingly, David discovers that countries with the greatest currency depreciations are those that see stronger rebounds. Investing in the dogs is a viable strategy after all, but currency behaviour is a more profitable and reliable basis for choosing opportunities.

Commodities

Global Macro Investor

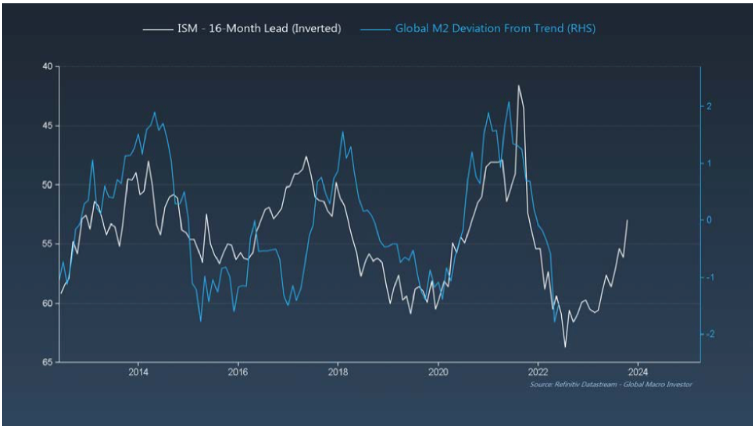

Crypto market fireworks are around the corner

Raoul Pal is starting to feel like he pretty much nailed the low in crypto markets. Bitcoin is the most oversold ever vs the log trend and has bounced, but as expected Ethereum has been the star of the show in the major tokens and is up 100% from the low - expect it to continue to outperform Bitcoin. For the crypto market to really take off we need to see the turn in Global M2. ISM leads it by ~16 months and the turn is very, very close…

Greenmantle

MENA: Short supply, but stay short

Oil supply has been slow to rebound given sustained high prices. On August 3rd, OPEC+ increased production quotas by just 100,000 bpd. Niall Ferguson expects the bloc to maintain this cautious approach at its September meeting. Meanwhile, nuclear talks with Iran have entered their tenth round but a breakthrough remains unlikely. Libyan oil production has returned to 1.2 mmbd after a month-long shut-in, but Niall anticipates further disruptions next month. Finally, Iraq faces a major political crisis that could boil over later in the year. Despite these headlines, however, Niall remains SHORT crude on a pessimistic demand outlook.

Commodity Intelligence

Nigeria: Indecisiveness could discourage investment in oil production

Exxon announced in February the sale of $1.3bn worth of shallow water fields in Nigeria. Since then, Nigerians have been indecisive, with President Buhari attempting to prevent the deal. Allowing it will welcome and encourage the major oil companies’ capital, but this freedom also implies the right for Exxon, and others, to exit ageing infrastructure in areas where local factions run riot at the expense of the oilfields. Buhari needs the major capital; he wants the EU gas deal desperately; those pipelines to Europe are potentially a life saver for Nigeria. But having Big Oil leave the difficult areas? That is a disaster.

CPM Group

Manipulating silver investors: JP Morgan verdict, spoofing, and silver inventories

In his latest video, CPM Group's Jeffrey Christian discusses the verdicts in the JP Morgan spoofing case, what they reveal, and what they mean for metals markets. He also puts the recent declines in London and New York silver inventories into perspective, highlighting and refuting various inaccurate interpretations of the drop in stocks. The relationship between reported market inventory levels and silver prices is also shown to be much different from what promoters would have investors believe.

Watch here.