Company & Sector Research

Europe

Betaville

Merger and Acquisition scoops

Darktrace (DARK LN) - on Aug 15th with the shares trading at 420p Betaville revealed that the company was at the centre of takeover speculation. DARK subsequently confirmed it had received an approach from US PE firm Thoma Bravo, pushing the cybersecurity company's shares ~25% higher.

Micro Focus (MCRO LN) - on Feb 10th with the shares trading at 466p Betaville revealed that the company was under the spotlight amid takeover talk. Canadian software company Open Text and MCRO have just announced a recommended takeover offer at 532p a share.

Bunzl (BNZL LN) - one of Betaville's latest alerts reveals the FTSE 100-listed distribution giant to be the centre of takeover speculation. This story is yet to be confirmed...

New Street Research

Has been linked to numerous potential M&A deals and New Street’s latest piece shows that sensible assumptions could allow for a significant €47bn value unlocking if management is willing to execute. In turn, this could allow considerable cash returns through buybacks and incremental dividends and valuing the stock on a sector multiple could lead to values as high as 240p/share, more than double the current price. These deals could all act as catalysts but in the near-term, the Hungary disposal and a sell-down of Vantage Towers could take leverage below 2.2x (below management’s 2.5x threshold) and be the start of incremental cash returns.

Huber Research Partners

A simpler WPP is a stronger WPP - laser-focused around faster growth end markets including ecommerce, retail media and tech. WPP has already raised guidance twice this year, almost completed an £800m buyback and increased the interim dividend by 20%. In addition, a ‘Transformation’ programme is on track to deliver £300m in operational savings. Management’s new full-year guide still implies a significant slowdown in H2 despite it being WPP's seasonally stronger part of the year. Furthermore, there has been no indication that large accounts have plans to cut spending. Douglas Arthur expects forecasts to be beaten this year and next. TP £11.00 (50% upside).

Creative Portfolios

Paul Hollingworth’s Buy call (July 2021) has yielded a return of ~60% but given fundamental and technical momentum remain positive (PH Score™ 8.0), Paul sees no reason to alter his constructive stance. Investors should focus on medium-term profitability targets driven by positive changes in efficiency metrics which would make current valuations attractive. If the mid-point of the ROE target of 12-16% is met, the current PBV of 0.83x is too low given the Earnings Yield would be 17% (vs. 12.2% currently), while also remembering that Standard Bank Group acquired Liberty for >1x BV last year.

ResearchGreece

Not for turning - Board rejects Lone Star’s latest €1.51 per share offer. What should shareholders do? If you believe BoC’s RoTE will not exceed 5% by 2024 you are better off selling at any price close to €1.50. However, ResearchGreece’s base case scenario is that BoC’s RoTE will reach 7.5% in 2024 and rise to 8.3% in 2025 (both of which are below management guidance) and calculates the equity is worth €2.08-€2.19 per share (60%-70% upside). Sees no reason for the bank to trade below the average 0.43x P/TBV 2023E of its Greek peers or even below the 0.50x-0.54x of best NPE/CET1 positioned Eurobank and National Bank of Greece.

Green Street Advisors

Fallen Angel - affiliate-party transactions skews valuations. Green Street NAV is -25% vs. company-reported. Leverage and debt/EBITDA are amongst the highest across Green Street's coverage - rescue rights issue a distinct possibility in the medium term. Issues examined in their 37-page report include complex capital structure; unusual financial engineering; poor management track record; corporate governance issues; disclosure that lacks transparency and obfuscates the market’s ability to derive an accurate valuation.

Iron Blue Financials

A score of 33/60 is top quartile for Iron Blue, which suggests fertile ground for shorting. BAB’s turnaround is proving lengthy and challenging. Accounting red flags include still elevated one-off costs, further historic restatements, and ongoing working capital normalisation. New auditors have introduced a “control deficiencies” key audit matter. Underlying returns remain pressured with FY22 EBITDA margins -150bp yoy. Headline EBITA margins expanded 20-30bp yoy but only because of lower D&A following stripped out asset impairments. The introduction of cost inflation (vs. fixed price contracts) is an emerging principal risk / key source of estimate uncertainty.

North America

Badger Consultants

A complete disaster - six quarters in a row of declining results, despite management talking about a turnaround. Yes, negative cash flow is now (only!) $411m, instead of -$600m, but there is now no growth in subs (4Q22 was the lowest quarter for net sub adds in PTON history; 1Q23 will be worse) and the churn rate almost doubled! PTON is hitting the wall at 7m total members and <3m paying members. This is exactly what Tom Chanos predicted when he first shorted the stock at $102 back in Sep 2021. The whole bull story is destroyed. Tom cuts his target price to $5.00, but the stock will most likely go to zero without a buyout.

Holland Advisors

Created a niche specialisation in flooring that no competitor can come close to matching - has done so using a scale economy shared model, and as a result now looks to have a long runway of growth ahead. During the last decade sales are up 29% p.a. and EBITDA +35%. Comparable store sales averaged growth of 14.5%. Market share has grown from 1% to 8% and is targeting 33%. $17bn of sales at a 16% EBIT margin gives EBIT of $2.7bn / net income of $2.04bn. A 20x multiple of this figure results in a M/Cap of $41bn (vs. $9.4bn today), that gives an investor IRR of 23% over 7-8 years (capital appreciation only).

Two Rivers Analytics

This new short idea was generated from Eric Fernandez's Earnings Quality Model - the core lawn care business is caught between rising fertiliser prices and declining demand after the Covid “fix-up-your-home” wave began to dissipate. At the same time, SMG’s cannabis growth strategy has fallen apart. The cannabis industry faces overcapacity that has decimated its Hawthorne segment, leading to a 65% decline in sales last quarter. Leverage remains alarmingly high (proforma leverage is 6.8x next year’s EBITDA) and while management has embarked on a restructuring plan to reduce expenses and inventory, and reclaim margins, Eric believes forecasts are overly optimistic.

TobaccoIntelligence

FDA issues first warning on flavoured nicotine gummies

The FDA has issued a warning letter to a Florida-based manufacturer, VPR Brands, doing business as Krave Nic, for marketing flavoured nicotine gummies - the first such warning over this type of product. According to the agency, they could cause nicotine poisoning or even kill a young child. Further, the company has not submitted a PMTA for this synthetic nicotine product and does not have a marketing authorisation order to manufacture, sell or distribute it in the US.

Portales Partners

Bank Stocks: PPNR is accelerating!

Pretax, pre-provision net revenues, the most powerful dynamic driving bank stocks, are projected to grow 7% in Q3’22, 15% in Q4’22, and 31% in Q1’23. These revenue and net income comparisons improve from near last in early 2022 to near best in 2023 for all S&P sectors. Obviously, top line revenue growth is almost assured given the shift in the yield curve, yet not so obvious is that credit quality appears quite stable through year end. When markets conclude that a recession is not inevitable, or that credit costs are manageable, Charles Peabody believes that bank stocks should respond quite favourably. Top picks include PNC, Wells Fargo, JPMorgan and Truist.

Singular Research

The largest gold ore purchasing and processing company in Peru boasts a healthy balance sheet (debt free / no need to raise additional funds) and growing dividend (3.2% currently). Trades at an EV of $538 per ounce - a significant discount to the peer group average despite strong cash flows and having reported its eleventh consecutive year of net profit in 2021 including record production of 106,892 ounces of gold. EPS has grown at a CAGR of nearly 25% during 2017-2021, while sales have grown at a CAGR of 14%. Singular Research looks for undervalued small / micro cap stocks initiates coverage with a Buy rating and a 12-month TP of $3.75 (65% upside).

Behind the Numbers

AFFO = Absurd Funds from Operations. Many investors do not realise that the company’s definition of AFFO features adjustments that are completely unrealistic and that without these adjustments, AFFO does not cover the dividend. BTN’s note examines this as well as multiple one-time benefits that made the latest quarter’s figure even less reliable. Click here to read more.

Paragon Intel

Evidence suggests CEO Schulman is not the leader to put out the fire he started - has missed numerous opportunities to keep the company ahead of an ever-rising competitive intensity in the fintech space. Schulman is a chronic underperformer who has destroyed (72%) alpha during his CEO tenures at PYPL and Virgin Mobile USA. His ManagementTrack Rating is well-below average at 3.0 (vs. median rating of 4.9 across Paragon's platform) and he has 18 level "2" or "3" audit, financial, and governance red flags identified including material impairments, Benford's Law, Financial Restatements, and Internal Controls during both of his CEO tenures.

Belkin Report

Tech back at No.1 ranked short

To flesh out the dichotomy between market sentiment and reality, Q2 S&P 500 operating earnings according to index provider Standard & Poors are $47.25. That annualises at $189, which is -17% below current Wall Street consensus earnings. Michael Belkin’s downside target for annual S&P 500 earnings is $107 (12-18 month view) which puts the index at a forward P/E multiple of 38. Tech is back as the #1 short and underweight recommendation in Michael’s model forecast. Utilities and Consumer Staples remain an overweight recommendation for any long stock market exposure. Company specific ideas are available on request.

Japan

Asymmetric Advisors

Contrarian Buy - Asymmetric are the only broker with a Positive rating on the name. Shares are up 90% since they turned bullish in Feb 2021. Citizen has been able to engineer a strong earnings recovery after restructuring, promoting its higher end watches and a recovery in its machine tool business. 9x CoE (but heading for substantial earnings overshoot due to FX so more like 7-8x); FCF yield of 14%; 5% dividend; 0.7x PBR with ¥86bn net cash (49% of M/Cap) - the stock looks great value and has strong momentum following the company’s impressive 1Q results.

Emerging Markets

LightStream Research

The shares reacted positively to quarterly results, but Shifara Samsudeen has questions over the sudden increase in losses booked under unallocated items (c.RMB2.0bn in 2Q22 vs. RMB381m in 2Q21) as well as the company not disclosing the key operating matrices for core businesses. Going forward, Shifara also expects Meituan to face severe competition from Ele.me as the latter has formed a partnership with ByteDance’s Douyin to create a take-out mini-app on the video sharing platform. Shifara is also keen to emphasise the fact that the regulatory probe on Meituan is still far from over.

Aequitas Research

Pre-IPO analysis - Chinese EV maker aims to raise ~US$1.5bn via Hong Kong listing. Leapmotor's revenue has grown by 26.7x (FY19-21) and it aims to launch seven more models over the next few years which should help to prop up growth. However, its linked entity, Dahua Technology, is on US’s entity list which will ward off some investors. In addition, it needs a whole lot of cash to scale up and appears to be lagging its larger peers. In a previous note Aequitas discussed the company’s past performance and PHIP updates. In their latest piece they undertake a peer comparison.

Galliano's Financials Research

Victor Galliano believes that the NAV is underestimated - separate from Itausa’s stake in XP, Itau Unibanco, which is Itausa’s core holding with a 37.2% stake, has a direct 9.96% XP stake. Adding its indirect XP stake share to Itausa’s NAV implies a sizeable discount of 27%. Since December 2008, only on 11% of the month end datapoints has Itausa’s discount exceeded 25%. This historically big NAV discount presents a buying opportunity.

Churchill Research

Mike Churchill tops up his holding in his Classical Insights portfolio - this homebuilder / real estate developer is too cheap trading on a P/B of 0.5x with solid financials and a growing top line. Part of the issue could be that the stock only listed two years ago and the firm is based in Recife (Northeast Brazil) so foreign investors may not be familiar with the story (foreign ownership is very low). Net cash position should grow despite ploughing money back into launches. Gross margin rose to 36.4% in 2021, which is a fantastic figure for this industry in Brazil (the Sao Paulo builders have been struggling to get over 30% in recent years). TP 13.81 BRL (100%+ upside).

Horizon Insights

Closer to Chinese Markets: On the ground research & company surveys

The largest independent research firm focused on China - Horizon Insights conducts local surveys across multiple industries to ensure accurate information that goes beyond government data. Last month's research included...

Healthcare: Preclinical CRO industry updates. Covid vaccine / testing news. Surveys on ADC industry and High-end Medical Devices.

Technology: In-depth reports on Industrial Automation Software and VR / AR markets. Laser Device and Semiconductor surveys.

Consumer: Investment thesis on Ligao Foods. Report on Chacha Food. High-end Sportswear market channel checks.

New Energy: Surveys for Copper Plating industry; Quartz Material and Carbon-Based Composites Materials; Auto Exports.

Macro Research

Developed Markets

Aitken Advisors

UK: Looking bleak

Some positioning surveys suggest that speculators want to go long sterling, perhaps hoping the BoE might show as much resolve as the Fed. Barring a communications epiphany, we will continue to see the Bank of England claim it can ‘fix’ the UK’s inflation problem with the most steeply negative real rates in the developed markets, but James Aitken doubts this very much. The selling off of sterling and gilts together shows how bad global confidence in the UK is, and James comments that it has an EM crisis smell to it. For the foreseeable future, you have to minimise your sterling exposure.

Minack Advisors

After 15 terrible years, when will things look up for Europe?

With the MSCI Europe index almost 30% below its 2007 peak (in US$), it’s fair to say European equities have done poorly. The near-term outlook doesn’t look much good either, yet Gerard Minack is more upbeat on a medium-term view (3+ years). He argues that the next cycle will suit Europe; an investment-led cycle that will benefit sectors that produce tangible outputs. Also, European valuations look cheap relative to their expensive American counterparts. A cheap Euro will also help. Look past the near-future and things are looking up.

Eurointelligence

Russia war: The impact of sanctions is fading

Evidence that Russia is escaping the impact of economic sanctions is mounting, claims Wolfgang Münchau. Regimes are becoming more sophisticated in circumventing sanctions and exports to Russia have risen substantially, increasing 47% in April. The world we live in now is not one where sanctions can be as effective, and the sanctions regime against Russia is simply unsustainable for the West, especially if China is declared to be their main strategic adversary. Neither Russia nor the West is strong enough to inflict a decisive victory over the other. This war will go on, and time favours Putin.

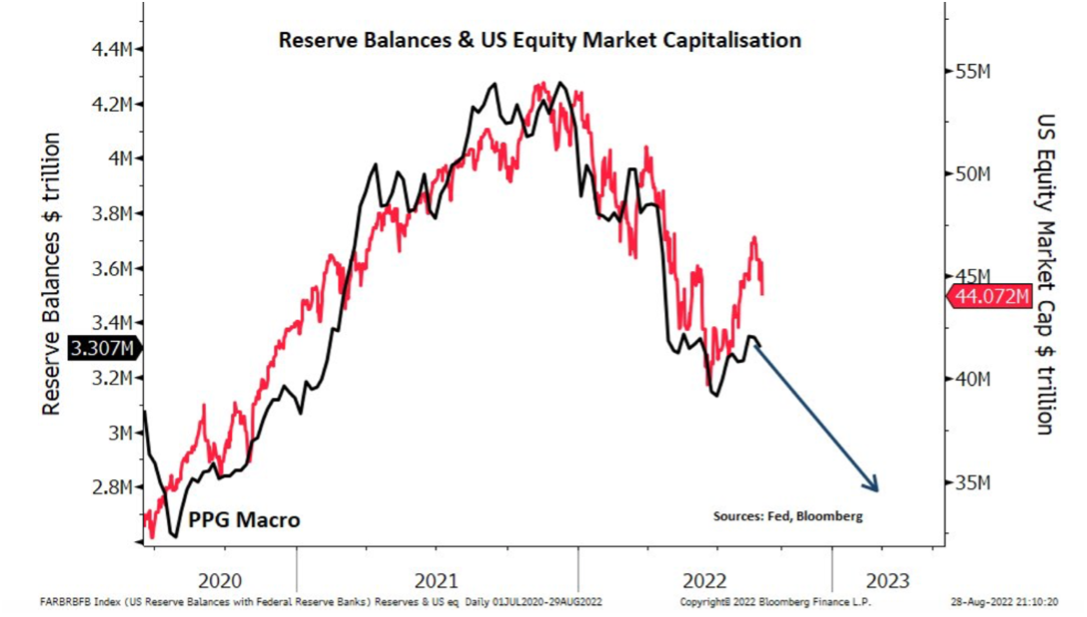

PPG Macro

US: The liquidity vacuum

Markets were shocked by Powell, having got carried away with the concept of a Fed pivot. There was no pivot; Powell’s comments about neutral were poorly communicated. What he should have said in his FOMC Q&A was that rates were now at the long-term projection of fed funds, but that policy was not currently neutral given the current background. Hopes of early easing were misplaced. Since the beginning of this year liquidity has been a core theme with the one chart to rule them all. It is going to get a lot worse. QT is set to rise to $95 billion a month. Moreover, the Treasury balance is set to rise, placing further downward pressure on reserves.

MRB Partners

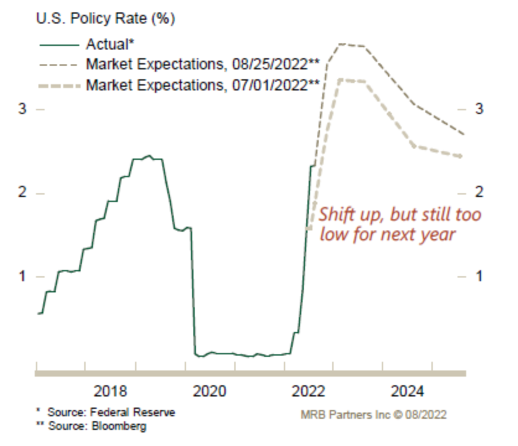

US: Next year’s policy expectations are up, but remain unrealistic

The Fed and the Treasury market’s expectations do not add up, argues Phillip Colmar. These include the Fed funds rate peaking around 3.75% in H1/2023, inflation steadily receding to ~2% in 2023/24, and no recession. Yet, one or more of these things will not occur. Phillip believes that when the consensus realises that achieving 2% inflation will not happen, we will see a replay of the market action in the first half of this year unfold. He remains cyclically bearish towards bonds.

Totem Macro

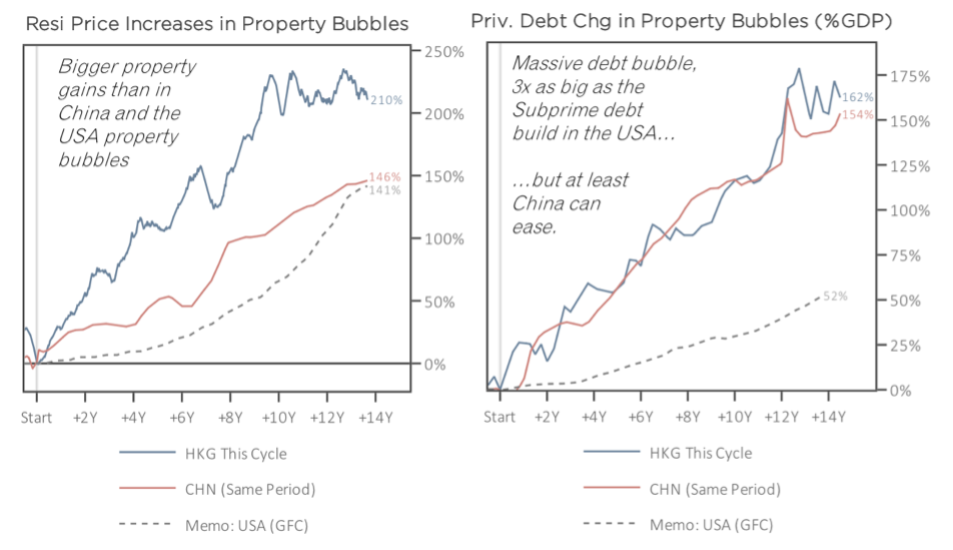

Hong Kong: The propocalypse

We’re on the verge of a big fed hiking cycle flowing through to Hong Kong with the vengeance of a spurned lover, declaims Whitney Baker. The problem with dollar-pegs is that they import US monetary policy, regardless of what domestic conditions warrant. This brings about inevitable mismatches, which went stratospheric in the age of QE; house prices are 2x higher than anywhere else on earth, driving huge debt that Hong Kong will soon be unable to afford whilst sticking to the dollar-peg. There’s material solvency risk in the property sector, and the most asymmetric way to play this is by SHORTING senior dollar credits of HK-focused developers, with spreads currently ranging from just 1.2%-2.3%.

High Frequency Economics

Japan’s widening trade deficit is appalling

With a current account gap that needs to be financed, Carl Weinberg explains how Japan will have to sell more bonds and stocks abroad, or use its foreign currency reserves. But selling JGBs with zero coupons and zero current yields will be hard. The Nikkei has also been on a downward trend for two years despite recent increases. It all spells trouble for the Yen, believes Carl. If the FinMin cannot sell securities abroad, it will have to draw down its foreign exchange reserves to pay for imports. FX reserves are finite. As they dwindle, the yen will come under downward pressure.

Emerging Markets

Topdown Charts

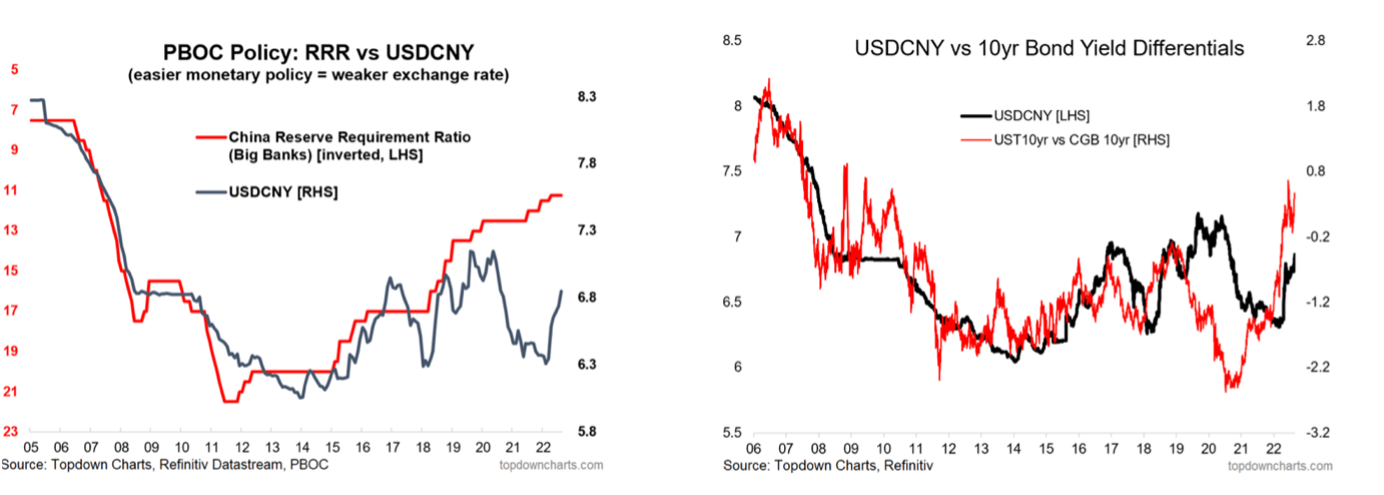

China: Currency weakness to spill over into EMFX

Inflation indicators point to a classic policy divergence between China and the US. Callum Thomas sees this as a devaluation risk for USD/CNY (see chart), which is confirmed with the path of RRR vs the exchange rate, and the path of the US 10-year treasury yield vs 10-year Chinese government bond yield differential. Further weakness in the Renminbi would likely ripple across to renewed weakness in EMFX. Although there is perhaps some compelling value in currently cheap EMFX, Callum claims bearish momentum is still rife.

Independent Strategy

The China conundrum

China’s debt problems persist and are increasingly evident in the housing market, explains David Roche. While he doesn’t see immediate economic collapse occurring, it highlights the growing list of threats to the country’s medium-term growth path. The country’s housing market and the associated local government and developers are the rotten core of the crisis, and the initiatives taken so far to solve the problem are simply not enough. He remains out of Chinese equities and SHORT the renminbi against the USD.

AAS Economics

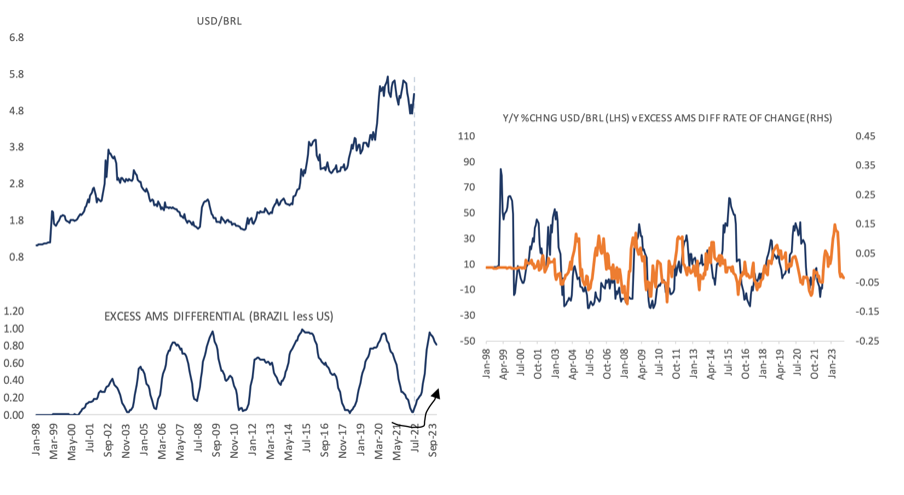

Brazil’s money printer working at a faster pace than US

Frank Shostak’s model indicates that the uptrend in the excess money differential between Brazil and the US implies that the Brazilian money printer is working faster than the US’s, providing support to the USD. The excess Adjusted Money Supply (AMS) differential (left chart) and its rate of change (right chart) generates his leading signal, suggesting a tendency for the USD/BRL to rise. For the two currencies in 2022 thus far, Frank’s FX strategy has seen a 30.35% return relative to a 7.67% increase in BRL/USD.

Oxford Analytica

Outlook for India-China relations is dim

Failure to resolve the long-standing border standoff in the Western Himalayas, which began in May 2020, is putting a heavy strain on bilateral ties between China and India, despite several rounds of talks aimed at resolving the situation. Trade between the two may be growing but Chinese foreign direct investment in India is stagnating. We will see the relationship remain under strain in the short-term, and India will look to work harder to reduce its dependence on Chinese imports and retain measures to reduce Chinese FDI.

Greenmantle

Mexico: AMLO under pressure

Facing intensifying criminal violence, a major international trade dispute over energy policy, and high inflation, Mexican President Andrés Manuel López Obrador (AMLO) remains focused on pet projects and priorities. Niall Ferguson sees this as good news for the stability of the MXN but will undermine growth prospects and investment attractiveness over time. Still, solid macroeconomic indicators, orthodox monetary policy, and Mexico’s ability to benefit from the geopolitical situation keeps Niall constructive – for now.

Alberdi Partners

Paraguay: Activity improving, but growth still likely to be weak

Marcos Buscaglia comments on another strong month of activity in June for Paraguay but retains his estimate of a 0.5% YoY contraction in real GDP. The tightening cycle has now reached an end and the central bank will start easing monetary policy at a moderate pace in 2023, with a forecast terminal rate of 6.5% as of December 2023. Lower rates and a retreat in commodities prices will cause a depreciation of the FX in 2023, which Marcos estimates will stand at USD/PYG 7,300 by the end of the year.

Commodities

Kailash Capital Research

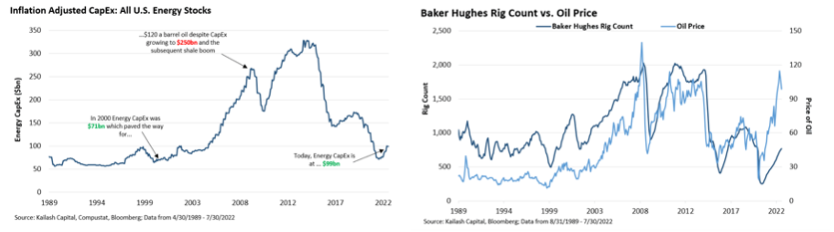

Improving energy investment could present lucrative opportunities

US energy companies need to spend more to remain a dominant global player. The good news is that we are now likely to be in the early innings of a long-overdue cycle of energy investing. The KCR team points to an interesting chart (chart 2) indicating that lower capex is expressing itself, predictably, in the deployment of fewer rigs than history would suggest. Yet despite this, the US has managed to smash production records thanks to large improvements in technology in land drilling. These new “super spec” rigs could present lucrative returns and Nabors Industries stands out as a terrific opportunity that will exceed very low expectations in the analyst community.

Commodity Intelligence

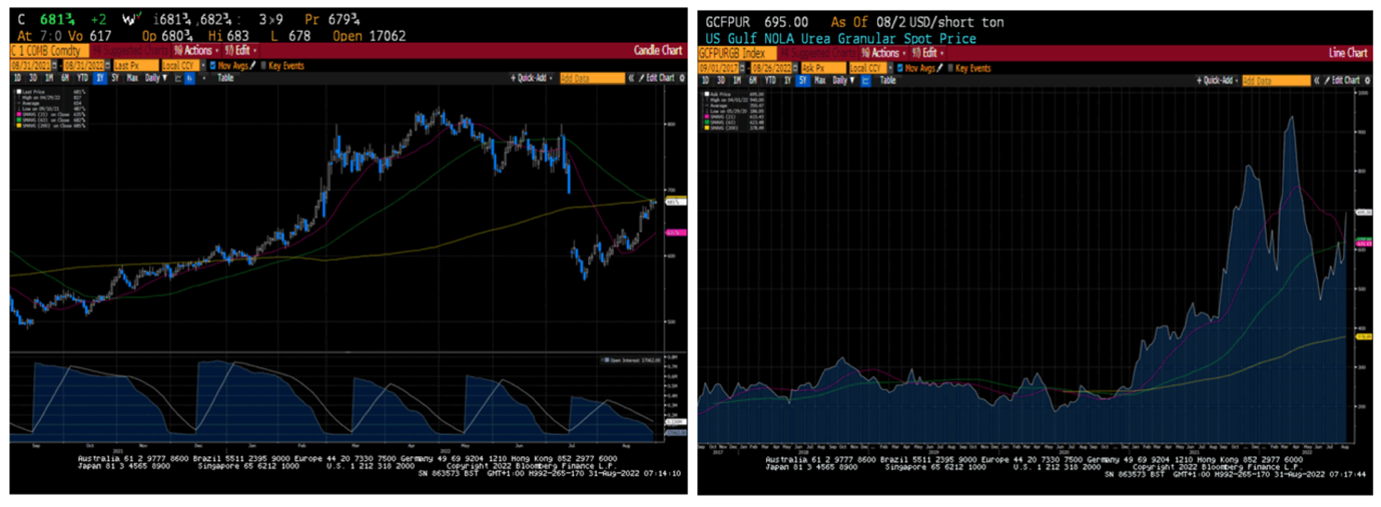

US agricultural futures close mixed

Corn is a market to watch, claims Mark Latham (see chart 1). He makes three points: the Ukraine export agreement caused the chart to break in July (chart 2); corn yields are correlated with urea usage, and the energy crisis has dented supply and the move from QE to QT has provoked a collapse in financial speculative activity. Add onto that the vagaries of the weather. It all sounds bullish, yet chart 1 says otherwise – the market is on the wrong side of its 200-day MA.

Vanda Insights

Saudi Minister lends crude a fresh prop, but Iran deal holds the key

Saudi’s Energy Minister has put oil bears on notice by hinting at OPEC+ production cuts, with such action involving the oil cartel slashing supply by 2.9m b/d, according to Vandana Hari. It is largely contingent on how much Iran releases into the market. With 100m barrels in storage the nation could ratchet up exports at a rapid rate, although the US may be looking to initially place limits on exports. If true, the volume may not exert too big a pressure on crude prices and will alleviate the pressure on OPEC+ to respond with cuts.

Ineichen Research and Management

The greatest malinvestment of all time

While the investment in renewable energy could be the greatest malinvestment in the history of mankind, gas and nuclear are now considered clean in Europe, the inflationary Inflation Reduction Act in the US includes support for nuclear, and Japan's PM asked government to consider building new nuclear power plants. These are positive developments suggesting, speculating a bit, that the grotesquely anti-humanist cultish eco-silliness (Net Zero, Green New Deal, Fit for 55, governments burning food (biofuels), bird blenders, bovine flatulence capture backpacks, etc.) might reverse soon.

CPM Group

When investors sell silver

Although it is an idea considered heresy by some, investors buy and sell silver as they would any other asset. In his latest video, CPM Group's Jeffrey Christian discusses how investors sometimes get better prices at dealers when they are buying and better prices at other dealers when they are selling. He also discusses the important distinction between gross and net investor purchases. CPM have recently updated their 10-year silver (and gold) projections.

Click here