Company & Sector Research

Europe

Holland Advisors

Enjoying a strong recovery in margins and ROE following a period of heavy investment that had depressed returns - recent results surprised many analysts with the strength of profit growth and Andrew Hollingworth thinks the group will soon get back to 10% net margins. Were it to do so on this years’ sales of c.€3.5bn then net income would be €350m. This compares with a M/Cap of c.€3bn so a PE of just 8.5x. That's too cheap for a tech leader in its field (c. 90% market share in aluminium brake callipers) that has compounded book value per share at c.16% for 20+ years.

JL Warren Capital

China survey reveals brand sales trended flat Y/Y in Q3 negatively impacted by the surge in Covid cases / lockdowns in some of the company’s high-volume markets. JL Warren models a DD Y/Y decline in retail traffic, offset by a 5% Y/Y price increase as well as a 5% incremental revenue contribution from private events in Sept capturing the brands heat from the 70th Anniversary Fashion Show. In Q4, they forecast a 25-30% Y/Y increase in sales, breaking down to 1) flat retail traffic Y/Y; 2) 10% price increase for the best sellers; 3) 5-10% retail area expansion; 4) 5% incremental revenue from Tmall.

Churchill Research

One of the top banks in Georgia and has grown to be the 8th largest position in Mike Churchill’s Classical Insights portfolio - Georgia has been a banker's paradise for several years now, helping TBC to outperform many struggling East European peers. The bank has a strong balance sheet (20.3% tangible equity to loans), low default rate (on pace for 0.8% provisioning this year), low price/book (0.69x) and high ROE (on track for 18.5% this year). The dividend yield is ~7% and the shares offer over 75% upside to Mike’s target price.

the IDEA!

Underestimating FCF strength / resilience - only temporarily under pressure due to a sharp increase in working capital. Ongoing price increases that are being implemented and the continuous efficiency measures combined with the integration benefits particularly from the Cooper acquisition, will see profitability improve. Gross margin to return to c.38.5%, and looking beyond 2023, a realistic objective is an adjusted EBITA margin of 13%+. Expects the FCF ratio will quickly return to 8% of sales next year and in the long-term 10%+ is achievable. TP €39.95 (50% upside).

Insight Investment Research

Insight’s global Infrastructure stocks offer avg. upside of 78%

Valuations attractive vs. history on SOTP discount, IRR-Ke, Recurring FCF yield and dividend yield - stock prices over discounting higher real bond yields / credit risk not a concern. Robert Crimes sees significantly higher upside in Europe (+104%) than Asia Pacific (+44%) and South America (+11%). Highest weighted average upside for Towers (+121%), where Robert prefers Cellnex (+143%). Second highest upside in Contractors (+98%) and Ferrovial (+158%) remains his top pick. Less upside in Airports (+79%) but European Airports (+112%) have strong potential, with Aena, ADP and FH Zurich all offering 85%+ upside.

Messels

FTSE 100 Momentum Portfolio

Messels position themselves as a dedicated technical research team who work for fund managers at a fraction of the cost of a typical sell-side analyst. Highlights from their weekly report: 1) Informa - new Buy as it rallies from support at the bottom of the 12m range and gains relative momentum. 2) Rio Tinto - develops bases at medium term support. 3) Croda - finding 7-year price and relative uptrend support. 4) Imperial Brands - renews uptrends from support above 2-year price and relative bases. 5) GSK - reaching support at the bottom of the 10-year range.

North America

New Constructs

Model portfolios outperform by 32% YTD

After beating the market by 71% in 2021, New Constructs research pays off again for clients so far in 2022 - underscoring just how important reliable fundamental research is in turbulent markets their long portfolio contributed 5% while their short portfolio contributed 27% of the outperformance vs. the S&P 500 through 3Q22. New Constructs’ latest piece focuses on why Wall St analysts are far too bullish on third quarter earnings expectations (Street overstates EPS for 340 S&P 500 companies) and lists 5 companies including Twitter who are most likely to miss expectations.

Behind the Numbers

Higher rates and the FASB may be about to break up the supply chain finance party

BTN have been warning investors about companies enjoying an unsustainable tailwind to cash flow growth by accelerating their use of short-term financing vehicles. However, rising rates are about to end the SCF party. They highlight Keurig Dr Pepper, JM Smucker and Procter & Gamble who have utilised SCF arrangements to a material degree and offer a simple framework for assessing the impact on their earnings and cash flows. They also discuss the implications of the FASB announcement this summer that it will be requiring enhanced disclosure regarding these programs (new rules go into effect in 2023).

Thompson Research Group

Positive results from TRG's Q3 Contractor & Surety survey

2H22 and 2023 will be a strong period for non-res construction and maintenance spending activity - backlogs / pipelines are sizable and increasing at a solid rate (and comes before the infrastructure bill which has yet to hit the ground in a material way). In keeping with trends over the past 18 months, data centres, warehouses and healthcare are very strong. Although labour and material challenges remain, TRG expects bullish results from several stocks including WillScot Mobile Mini, Herc, Vulcan Materials and Beacon Roofing.

Abacus Research

An underappreciated platform - over the last few quarters UBER has clearly demonstrated that it can make the driver / consumer equation work despite severe driver shortages and high oil prices. Abacus’ DCF analysis suggests upside to $49 in a ‘new normal’ scenario based on i) ~15% revenue growth next few years (vs. consensus ~20%), fading to 10% growth. ii) FCF of $4bn in 2025 (vs. management’s target of 2024). iii) Discount rate of 9%. Two years from now they expect UBER to be a very different company in terms of margins and have a more certain growth profile. Favourable risk:reward 80%+ upside vs. ~25% downside.

Gordon Haskett Research Advisors

In Adrian we trust - CFO Adrian Mitchell continues to impress; his experience / background has armed M with more discipline and retail acumen. Having swiftly adjusted the composition of inventory to non-pandemic winners, M's sales performance has been impressive, particularly vs. its direct peer group. Concurrently, inventory levels remain healthy (up only 7% at the end of 2Q22 vs. a 41% average increase at peers). GHRA does not believe 3Q22 comp trends have deviated materially from the company's implied guide and highlights a number of tailwinds heading into holiday ’22. Stock trades sub 4x EPS and EBITDA. TP $24 (40% upside).

Badger Consultants

Rubbish business pre-covid and least believable guidance Tom Chanos has seen in years - it was not until the pandemic, when consumers were flush with cash and stimulus money, that TGT did very well. Tom argues that we are only in the beginning stages of a recession, yet Wall St forecasts no decline in sales over next 3-4 quarters and has margins increasing! 18x earnings is not cheap. TGT would have to earn $13 per share to justify today's stock price. Tom sees 12x $9, or $108 share price as more realistic, but if the recession lasts longer than expected, it could easily go to 10x and earnings could fall to $7, or $70 worst case basis.

Portales Partners

Has been one of the best performing large cap bank stocks in recent years, but at current prices, the stock is not discounting potential capital constraints, a reduced buyback (Charles Peabody expects it to be cut in half), and near-term risks that include capital markets challenges and the Twitter ‘hung loan’. At 2x TBV the stock is more expensive than JPMorgan yet offers discounted returns. For dividend yield support there are other sources of high yields among other banks with less risk.

Gradient Analytics

Key concerns highlighted in Gradient's 18-page initiation report include: 1) Semiconductor downturn to result in a material revenue gap for NATI. 2) Surging receivables suggest declining revenue quality (2Q22 AR to 3 month revenue reached its highest level in over 5 years). 3) Declining deferred revenue indicates less balance sheet support for future revenue growth. 4) Faces margin headwinds from a previous drawdown in accrued compensation and from outsized growth in prepaid expenses. 5) Trades at a significant premium to its industry peers.

Etalon Investment Research

Spin-off from Enovis (formerly Colfax) provides investors with a classic spin-off situation with realistic growth potential and good FCF generation. Overweight to emerging markets vs. other US-based industrial companies. The product mix is 70% consumables & 30% equipment. Currently trades at 7.6x EV/EBITDA and 10.7% FCF Yield (FY22 guidance). 400 bps margin improvements (to 20%+) are well within reach in 3-5 years no matter the sales. Long-term sales growth to $3-3.5bn, the lower end is achievable from organic activities. Successfully navigating an inflationary environment.

MYST Advisors

Despite being the one of the fastest growing publicly traded Ag-tech companies (FY23 / FY24 Revenues & EBITDA expected to grow at least ~25%), BIOX is largely off the radar for most Investors. Its ability to reduce chemical applications, improve soil quality and conserve water puts the company at the forefront of environmental sustainability and positions it as the Ag leader in the transition to carbon neutrality and sustainability. TAM estimated to reach ~$100bn+ within the next 5 years. TP $27 (100%+ upside).

Sales Pulse Research

Security vendor with the strongest momentum

For some time now CrowdStrike has scored very well in Sales Pulse’s survey results - although much of the input is anecdotal, in their latest survey CRWD has taken the top spot with a notable increase in channel sentiment. Click here to read more.

Japan

Asymmetric Advisors

Analysts are starting to adjust down their estimates of the global no.1 precision motor maker since Asymmetric provided a negative review on 29th Sept. However, there are still 18 BUYs vs. 2 SELLs, consensus OP is in line with CoE (PER >30x) but there is strong potential for a downward revision when it reports 1H. Meanwhile, its core HDD motor business is in long-term decline, its product offering is vulnerable to a global economic slowdown including the Machine Tool business whose prospects CEO Nagamori is very excited about and the EV e-axle business which won't make a significant contribution to profits for a few years.

Emerging Markets

New Street Research

EM Telcos are in a bull market

Most generalist EM fund managers are Telco bears - they don’t like the industry; they think returns are poor, regulatory risk is high and growth is weak. However, all these factors have improved in the majority of EM Telco markets. Bharti Airtel hitting new all-time highs says it loud and clear: despite weak (and weakening) macro, EM Telcos are in a bull market. Investors who retain a bearish view of the sector based on how things used to be are missing an ongoing opportunity to generate Alpha.

Westlake International

China eCommerce primary research report

Westlake observed online discretionary spending (except for cosmetics) recovered gradually in Jul & Aug, but softened slightly in Sept & Oct given rising community lockdowns. They expect Alibaba, JD, Pinduoduo, Vipshop and Kuaishou will meet 3Q Street expectations. Given modest improvements in business and consumer confidence, they anticipate further 4Q sales recovery for leading Chinese eComm players driven by 11.11 promotions and likely continued government consumption coupons. If Covid restrictions gradually ease after the 20th party congress, a broad-based recovery will help boost consumer spending.

Propitious Research

The stock has meaningfully outperformed local peers, the Hang Seng index, and broader Emerging Markets index in the last 6 months, when Wium Malan argued that VIPS’ valuation multiples had de-rated to levels where it was an attractive takeover target. Trades on a paltry 3.8x forward PE ratio (ex-cash) and looking purely from an infrastructure perspective, trades at a c.50% discount to JD.com on a per square metre basis. Given the recent rebound in Chinese retail / apparel sales growth and the pessimistic expectations from the sell-side, Wium expects the current earnings upgrade cycle to continue.

Galliano's Financials Research

On the back of 2Q22 results, Victor Galliano screens 9 large Chinese commercial banks’ core profitability, and their credit quality and coverage, to identify banks that are attractive value, have good earnings growth prospects and have the potential to deliver sustainably higher returns going forward. Ping An Bank stands out on valuation (especially PEG ratio). Victor believes that its returns could improve over the medium term especially from lower cost of risk given its credit quality strength. He also retains a positive view on CCB. However, Victor is negative on China Minsheng due to its low ROE, poor delinquency and NPL coverage.

Macro Research

Developed Markets

Aitken Advisors

The ‘everybody gets a trophy market’ is over

Extraordinarily, the financial system is suffering from collateral scarcity, writes James Aitken. This, combined with the ‘receive fixed rates unwind’, could drive cash equivalents – such as treasuries – higher; James wonders whether 10-year treasuries are a buy here (388 basis points), a view predicated on market dysfunction, a result of ongoing deleveraging. He also comments that in a world of zero rates, investors were incentivised to be long risk, of all kinds. Now, we’re back in a world where you value the asset on its merits, and wait. If a central bank eventually supports your thesis, great, but don’t count on it. A difficult time lies ahead for markets, but as things unravel let’s be sure to take full advantage of good assets flogged by weak hands.

Blonde Money

UK: The credibility doom loop

The government and the Bank of England are now locked in a mutual credibility doom loop, exclaims Helen Thomas. The Bank has put a target on its back by setting a deadline that is tough for the cautious LDI industry to meet while the Government cannot recover fiscal credibility without political decapitation. The markets are on an unstoppable collision course with policymakers. Pension funds are naively waiting around, mistakenly believing that the government wants to change course and that the market will restore its faith. Gilts and GBP will fall further.

PPG Macro

UK: Gilts, the bank & real yields

Another day, another change by the Bank of England. Their piecemeal approach is not enough and they need to do more, claims Patrick Perret-Green. Financial instability is becoming too much of a problem. Although actions have been extended until October 14th, Patrick doubts this is long enough, and direct action in the market, over and above auctions, remains a possibility. He points to the 2055 linker, issued in 2005 (see chart 1) and comments that, across the water, TIPS are also at extremes (see chart 2 for the 2041, issued in 2011). Real yields at these levels are unsustainable. Indeed, it feels like a generational opportunity.

CrossBorder Capital

Just how much have central banks tightened this year?

Michael Howell comments that the latest weekly balance sheet data from major Central Banks show policy liquidity shrinking at 19% in USD terms. USD strength has exacerbated the tightening, such that in USD terms aggregate liquidity has been tightening at double that pace. Delving below the headline figures shows that the rate at which the major Central Banks are tightening has varied significantly over time (viz. US Fed), is not always in line with official policy statements (Bank of Japan) and has not really started (ECB and BoE). What’s more, BoE data has yet to reflect the emergency £65bn QE launched a week ago.

Belkin Report

Market psychology will change

Market sentiment believes Fed rate hikes and inflation are the major threat to stock prices. Michael Belkin argues otherwise; the real threat is the economic downturn and subsequent collapse in corporate earnings. The European economy is in trouble and manufacturers face a reckoning as energy prices take their toll, yet European sector rotation is mispriced for this scenario. This mismatch between sentiment and reality also extends to government bonds. To prepare for the coming months, look for defensive consumer staples, utilities and healthcare.

Ineichen Research and Management

S&P 500 to fall a further 65%

Earnings estimates for the S&P 500 are currently at $236 and are only falling mildly so far, which Alexander Ineichen claims is weird, given that GDP forecasts have been revised lower throughout the whole year. If earnings fall by 40% like in the Great Recession and PE remains at 15.4x, the S&P 500 falls, well, by 40% from here (3,639). If, in addition, PE falls to 9x, S&P 500 falls to 1,274 ($236*(1-0.4)*9), i.e., -65% from here.

Click here

View from the Peak

With blood on the streets, triage is coming

Heightened market volatility prevents leveraged investors who cannot accept outsized drawdowns from buying. However, the lower equities and bond prices fall, the more compelling they are for investors with a 3–5-year time frame. After the bursting of the 1999 tech bubble, China’s rise led to five years of leadership from commodity, industrial and cyclical stocks. Will climate infrastructure spending for the balance of the decade be the catalyst for again re-rating these sectors? This is Paul Krake’s thesis, therefore his dip buying strategy focuses on global miners and climate infrastructure. Buy equity, investment grade credit and sovereign bonds into weakness. Don’t use leverage. The lower it goes, the more you buy.

Emerging Markets

Greenmantle

China: Further to fall

U.S.-listed American Depository Receipts (ADRs), domestic Chinese tech companies, and real estate developer stocks face stiff headwinds as the global economy slows, domestic stimulus disappoints, the zero-COVID policy continues, and U.S.–China tensions mount. Markets are betting that Xi Jinping’s smooth transition to a third term will provide a short-term boost to markets. Niall Ferguson thinks they are more likely to be surprised by the ideological tone of the meeting and the appointment of Xi loyalists to top economic positions. Expect CNY to keep weakening against the dollar.

Entext

India has become a momentum trade comfort blanket

Sean Maher believes that Indian stocks are now trading on a historically expensive premium versus wider EM, propped up in part by the ‘India as the next China’ soundbite (see graph). The country is attempting to embark on the China path but lacks the ingredients. As stimulus rises in China and the pro-growth Li faction in the ascendant, Sean has opened up a LONG MSCI China versus India position in anticipation of a mean reversion over the next few months.

Rosenberg Research

India: Long-term still bullish, but short-term bearish

India has been one of David Rosenberg’s favourite regions over the last two years, but the bullish trade has become too crowded for his liking. Ominously, the message from India’s macro markets (both bond and currency markets) is clear: “risk-aversion”, and David believes that the vaunted decoupling in risk markets (credit and equity markets) cannot continue for too long. He is short-term bearish on risk assets in India in this contrarian view!

Alberdi Partners

LatAm: Slow growth

Marcos Buscaglia expects Latin America to experience a big slowdown in 2023. Activity has already slowed for most of the region, bar Brazil. Recession pressures will bubble in 2023 as Latin America is struck by a triple whammy of shocks: significantly worse external conditions, tight monetary policies and domestic political turmoil that drags investment down. Marcos remains more optimistic than consensus about Brazil, especially since Lula is likely to implement centrist macro policies if he wins. Expect credit rating stability as the norm with the exception of Colombia, which is at risk of a downgrade.

Churchill Research

Turkish stocks are crazy cheap

The Istanbul equity index has excelled in recent months, rising 40%+ in since mid-July in USD terms (see chart). This is a function of falling interest rates, semi-stabilisation of the currency and the catch-up of Turkish street prices in the wake of the sharp preceding lira devaluation. Should Erdogan be replaced with a more orthodox leader in 2023, improved monetary policy could be a further boon for equity valuations. Just don’t hold your breath.

Copley Fund Research

Asia ex-Japan Q3 performance was challenging for active managers

Steven Holden examines Q3 performance among the Asia ex-Japan active funds, breaking down this quarter’s performance relative to the iShares MSCI Asia Ex-Japan ETF (AAXJ). The last quarter was a challenging one for active Asia Ex-Japan managers. The return distribution shows the managers losing between -18% and -14% over the period. Aggressive growth and value managers were the only Style groups to outperform over the period, driven by stronger returns from the Small/Midcap end of the spectrum.

ESG

Global Mining Research

More gold miners addressing greenhouse gas emissions (GHG)

David Radclyffe’s latest report examines the GHG reporting structures and emission reduction/mitigation plans for gold stocks covered by Global Mining Research (GMR). Interestingly, scope 1 & 2 GHG intensity increased by 35% for CO2-e t/GEO from 2015 to 2021, highlighting the challenges ahead for miners to achieve reduction targets. Within the GMR universe, Barrick continues to provide the clearest pathway. Newmont has a list of GHG initiatives, while GFI and NST provide timelines to 2030. Most other gold miners need to lift their game as few show a tangible commitment to GHG reduction.

ERA Research

ESG report on pulp, paper, packaging and tissue

ERA Forest Products Research released their latest report on ESG commitments, progress and gaps for pulp, paper, packaging and tissue companies. Within the sphere of pulp producers, Mercer and Sappi are cited as examples of companies with strong disclosure and targets. In European paper, pulp and packaging, ambitious targets appear common but data and disclosures are healthy, with firms including UPM and Billerud mentioned. In the packaging, paper and tissue industry, WestRock appears to lead the way, with Graphic Packaging also referenced as having good targets that could spur near-term action.

Commodities

Longview Economics

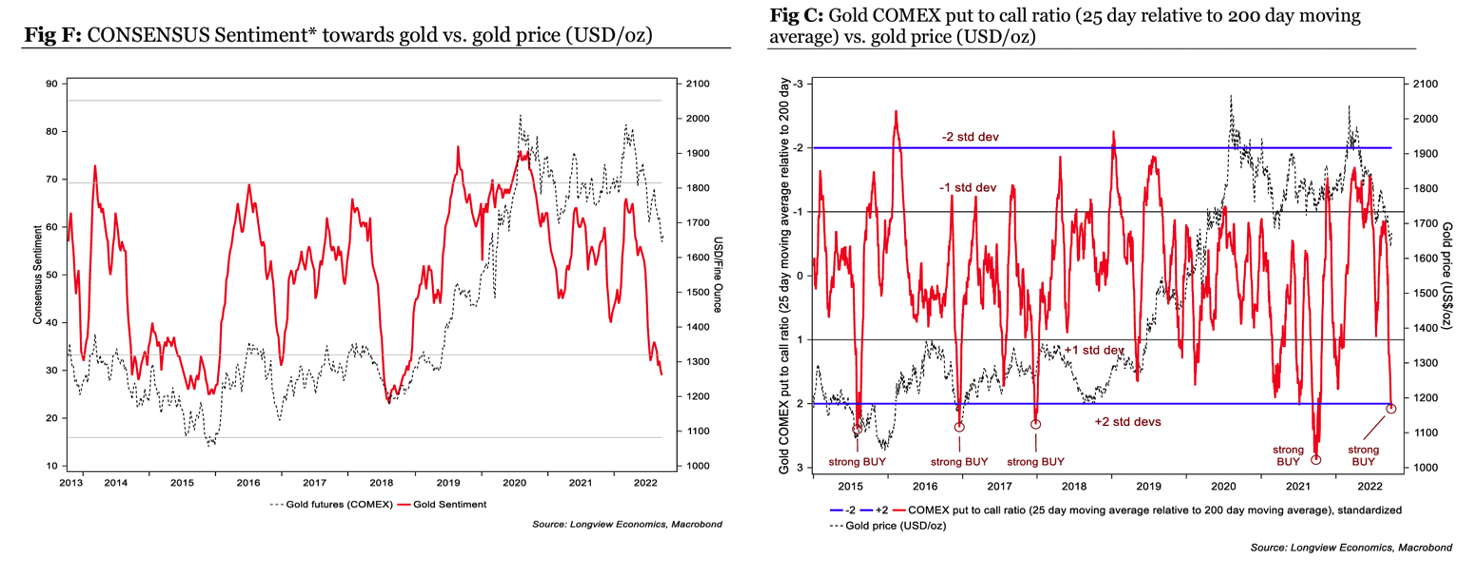

Gold: Poised to rally?

Harry Colvin is aware that, on the surface, the outlook for gold and other precious metals is poor. That doesn’t dissuade him. Right now, positioning and sentiment is at extreme/bearish levels, generating its most extreme BUY signal since 2018 (see chart 1). Add that to a high downside put protection (see chart 2) and a US economy teetering into recession, and you have the recipe for a gold rally. Move LONG gold December futures with ½ the position at current prices and ½ on weakness (1t $1,680). Place stop at $1,610 and risk 125bps on this trade.

New Normal Consulting

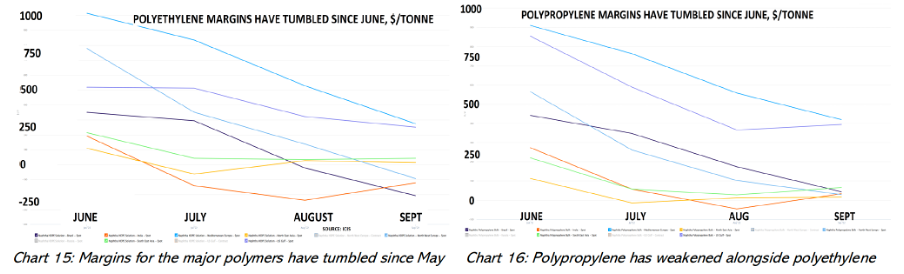

Polymer prices highlight extent of the summer downturn

Paul Hodges has long praised the bellwether role of the chemicals market, and recent trends are concerning. Pricing for the major polymers is flashing warning lights about the impact of falling demand and high energy costs on margins, suggesting a major shock to earnings now building up along the value chains. It served as an early warning on inflation last year and on recession this year, yet mainstream commentators prefer to follow central banks in focusing on the detail of yield curves rather than on events in the real world. Don’t make the same mistake.

Metals Focus

Despite recent price upside, silver still faces considerable headwinds

Expectations that the Fed may adopt a less hawkish stance provided some respite for silver’s price. Even so, the price action may be disappointing for some investors given the strength of physical demand, particularly from India. Institutional investors remain cautious about the outlook for the complex, the biggest headwind for silver prices. While rate expectations have been trimmed, further tightening is expected, pushing yields higher and lending further support to the USD. Expect silver prices to face renewed selling pressure toward year-end which will continue into 2023.

CPM Group

What the rising dollar means for gold

With the US dollar continuing to rise, CPM Groups’ Jeffrey Christian discusses what it may mean for gold. Jeff compares the current situation to 1985 and discusses whether we are likely to see another agreement like the Plaza Accord.

Click here to watch.