Company & Sector Research

Europe

Arete Research

Two for the price of one - TNET’s 66.8% / 100% equity stakes in NetCo / ServCo are each worth more than the current M/Cap. Investors are more than discounting retail broadband competition / No. 4 mobile entrant risks. Opportunities for ServCo include Wallonia expansion, B2B, plus numerous initiatives (e.g. AI) to continue driving down market leading churn. Compares the situation to Telecom New Zealand, which conducted a similar split in 2011 with both units re-rating to double digit EBITDA multiples. Meanwhile, investors are being paid to wait with >7% dividend yield. TP €30 (100%+ upside).

TT Equity Research

Based on the turmoil caused by the announced price increases and the delayed dynamics of price elasticity, Teun Teeuwisse’s view remains that the current positive profitability will not be lasting. This will be aggravated by the current macro conditions where consumers will increasingly cut back on services like food / grocery delivery. Meanwhile, Teun also sees little opportunity for TKWY to further increase income per order as this may have an accelerated impact on the existing contraction of orders.

Iron Blue Financials

Accounting red flags include stripped out broadly defined restructuring expense (44% of PBT adj over the past six years), share-based payments and acquired software amortisation. FY22’s +11% organic sales growth is difficult to reconcile against annual report acquisition revenue contributions disclosure (implies negative organic growth), cross-checked by subsidiary accounts analysis. Headline net debt excludes £29m contingent consideration while floating debt implies c.£2m extra net finance charge with the rise in SONIA since year end. Iron Blue also notes sub-optimal governance with non-independents controlling the board.

Insight Investment Research

New Terminal One at New York’s JFK airport offers unique exposure to almost pure intercontinental traffic with high ticket yields for airlines, enabling high aeronautical fees and high retail spending - within Insight’s 16-page flagship report, Robert Crimes’ key value add vs. the Street is his assessment of future capacity in the New York Air System, appraisal of the strategies of competing terminals, benchmarking of peer airports (aeronautical fees and retail) and full detailed DCF valuation (values FER’s 49% stake at $2.1bn vs. $1.14bn invested; IRR on equity invested is 13.0%, 326bps above Ke of 9.2%).

Forensic Alpha

New forensic red flags - sharp rise in DSI is particularly noteworthy for a company that is fanatical about managing its working capital cycle. DSI broke out of its narrow range in Q3 rising by 26% y/y to 226 days. With nearly €7bn of inventory now on the balance sheet, if ASML is slow to resolve its supply chain issues, inventory would remain elevated into 2023, leaving it vulnerable particularly if the outlook for customer capex takes another step down or if geopolitical tensions continue to escalate. In this context it is also concerning that the reserve against inventories fell LY to just 7.5% of the gross inventory balance (5-yr low).

Willis Welby

UK growth stocks

One easy response for equity investors faced with such a radical change in the backdrop for equity pricing this year is to assume that growth stocks can get further derated. Willis Welby, who use expectations analysis to help decode share prices, differentiates between duration stocks which require a transformation in business models and growth stocks which do not. They draw particular attention to IHG, Burberry, Compass, Sage, Auto Trader and Experian. Notable absentees from their analysis are the industrial fan club stocks of Croda, Halma and Spirax which did not make their consensus Y3 revenue growth criteria.

North America

Singular Research

Searching for opportunities in small / micro caps

Hall of Fame Resort & Entertainment Co. (HOFV) - Building a compelling set of American football themed assets that can derive material revenues through visitation, media and gaming channels. 1-yr TP $1.30 (130% upside).

Independence Contract Drilling (ICD) - An exciting opportunity to purchase a company that is capitalising on significant drilling rig supply shortages for oil and natural gas exploration.

Superior Group of Companies (SGC) - Developed a proven track record of helping companies increase brand strength. Recent operating segment realignment will unlock synergies and provide new growth avenues.

Gordon Haskett Research Advisors

Upgrades to Buy - combination of multiple catalysts and overly negative sentiment creates a favourable risk:reward dynamic - 1) Improving driver supply (GHRA’s proprietary data shows positive performance in wait times). 2) Improving conversion rates (highest in several years). 3) Continued shared ride adoption. 4) Employees are returning to offices (Sept was a turning point). 5) Lyft Media is an underappreciated and potentially high margin business segment. GHRA also highlights the valuation gap with Uber (70% discount is unjustified) and why LYFT is increasingly looking like a prime activist target.

Paragon Intel

New CEO Bernard Kim will rejuvenate Tinder and refocus MTCH’s product roadmap - to reaccelerate growth, Kim will drive better-than-expected payer and revenue-per-payer growth by applying his mobile gaming expertise, introducing new product features, and more efficiently balancing investments in high ROI properties. A forward P/E of 19x, sets up a more compelling risk:reward today than at any point since the stock went public in 2015. Adjusted EPS to increase to $3.83-$4.11 in 2024, which is 14%-22% higher than consensus of $3.37.

Huber Research Partners

Race against time - faces a material slowdown right when the company is desperately trying to right-size costs, boost GPU per unit and improve cash flow to address a mountain of debt. Ironically, slower sales volume may ease some of the cost pressures, but Douglas Arthur still envisions a large 3Q EBITDA loss and a FY loss of over $1bn with FCF to be a negative $2bn. At this rate, Douglas believes management will somehow have to tap the debt markets for over $2bn of capital in 2023, further straining the financials. Does not expect CVNA to be EBITDA positive until 2026E.

A Line Partners

In their weekly report A Line uses a proprietary ranking system to build individual company performance history. Companies are graded A-C based on factors including product design, promotional activity and store feedback. Key takeaways last week:

ATZ - Grade A; scores 28/30, +2pts vs. previous week. Consistently positive feedback across the stores. The Super Puff is flying off the shelves (gone TikTok viral).

ROST - Grade B; 18/30, +2pts. Improved traffic trends driven by markdowns. Discounts are deep (e.g. women’s jeans at $7.99, $3 cheaper than last year). Sales boosted by cold weather.

Michael Kors - Grade B; 14/30, -3pts. Oct has slowed vs. Sept (lack of tourists and domestic customers who are not shopping as much in anticipation for the holidays). Increasingly aggressive promotions.

Daniel Insights

Corporate access - Daniel Insights will be hosting a call with AEO’s Shekar Natarajan (EVP / Chief Supply Chain Officer), on Wednesday, 9th November at 11am EST. Shekar will be discussing Quiet Platforms’ strategy of building a collaborative commerce network for retailer and consumer brands. The new network enables customers to gain instant nationwide coverage through a trusted portfolio of carriers using a universal delivery label, eliminating the need for multiple integrations, complex invoicing or lengthy contract negotiations. It currently has 46 brands / retailers utilising the network and is scaling rapidly.

Alembic Global Advisors

Pete Skibitski forecasts double digit organic top line growth in 2022/23, with mid/high single digit growth in 2024/25. This drops down to solid double digit adjusted EPS growth through 2025. In a potentially challenged 2023 macro environment, Pete prefers aerospace stocks with commercial OE exposure as opposed to aftermarket. His current deliveries forecast for commercial jets shows double digit growth in units through 2024, with 2025 at high single digits. HWM's $437m of structural cost reductions (2019-21), along with $214m of core price increases, augers well for margin expansion on expected higher volumes.

Valens Research

“Capex supercycle” beneficiary - US assets are at an all-time high average age, necessitating investment, even amid deteriorating economic conditions. ATKR, a supplier of critical, but often-overlooked, parts to data centre and IoT-related end-markets, has become a leader in niche infrastructure markets. By consolidating the space and focusing on parts that represent a small portion of total project spending, ATKR has been able to offset inflationary supply pressures. As such, with secular demand drivers and the capacity to expand profitability, equity upside may be warranted.

BWS Financial

Earnings miss underscores Hamed Khorsand’s ongoing concerns - his short thesis is based upon slower demand for WDFC’s products and rising inventory levels. The group’s reliance on price increases will lead to further earnings misses as input costs remain elevated at a time when customers could experience sticker shock as further price hikes are rolled out this quarter. WDFC generated negative FCF in fiscal 2022 and there is no assurance FCF will turn positive in fiscal 2023. TP $88 (45% downside).

Veritas Investment Research

Two years too late - persistent delays to the launch of MAXR’s next-generation Legion constellation of satellites has severely weakened the investment case. MAXR will incur higher capex and lower organic growth than estimated by the Street. As a result, the company will fail to meet its de-leveraging target by the end of 2024. Deleveraging is a key tenet of the bull case; without a cleaned-up balance sheet, MAXR will be unable to close the persistent trading multiple gap vs. peers.

CTFN

CTFN provides in-depth news on mergers, event-driven situations and major corporate developments. The news service, in conjunction with their PressRisk platform, delivers content and resources that increase the value and efficiency of their readers’ research efforts. Recent coverage includes:

Activision - The state of play meeting with the EC for Microsoft’s acquisition of ATVI was 21st Oct. MSFT can offer Phase I remedies by 28th Oct.

Black Knight - The FTC sought a declaration from a vendor in the loan origination space as part of its review of Intercontinental Exchange’s purchase of BKI.

VMware - Market power in virtualisation software likely to take centre stage in EC’s examination of Broadcom merger.

Click here to access the three news stories.

Japan

LightStream Research

Price hikes appeal to investors - Calbee's decision to raise prices across its product range has led to renewed interest among institutional investors for Japan’s largest snacks maker, having fallen out of favour for several years. In fact, after a seven-year fall, the stock is threatening to break its downtrend with the shares up ~37% in the past six months. While investors bet on earnings growth over the long term through regular price revisions, Oshadhi Kumarasiri thinks there could also be short and medium-term gains as operating profit growth turns positive after many years.

Emerging Markets

Copley Fund Research

Mexican allocations continue to surge higher

Over the past 6 months there has been some aggressive country repositioning among active EM managers - Mexico is now the largest country overweight position (vs. the benchmark iShares MSCI EM ETF). Despite this sentiment shift, Steven Holden says allocations look far from stretched (avg. weights among active EM funds: 3.4% today vs. nearly 5% in 2015). On a Style basis, Yield managers have increased weights the most. On a stock level, Grupo Financiero Banorte and Wal-Mart de Mexico have been instrumental in Mexico’s rise up the ranks.

JL Warren Capital

Deliveries plummet in Oct and the XPeng G9 faces weak demand and unstable supply - JL Warren has noticed a sharp decline in delivery posts on social media for the P7, P5 and G3, and no mention of G9 deliveries posted by owners. They have also heard that the new plant in Guangzhou (which makes the G9 exclusively) is still operationally unstable, and not ramping up volume as expected. Expects <1-2k production of G9 in Oct and total deliveries to be well under 8k. The EV manufacturer is suffering from increasingly negative PR, both on the product and corporate level.

Galliano's Financials Research

Withdrawal from Banamex bidding is positive, but current valuations don't reflect 2023 risks - Victor Galliano highlights the pressure on credit spreads from rising funding costs in the system; Banorte, despite its loan to deposit ratio of 101%, has avoided this so far by improving its funding mix but this can't continue indefinitely. There are early signs that credit quality may be worsening, despite the benign NPL trends, stage 2 loans increased from 0.85% in 2Q22 to 1.09% in 3Q22. Going forward, non-bank subsidiaries may also prove harder to continue to squeeze higher returns and the investment in the digital bank adds to opex.

Smart Insider

Jun Li (GM) and Xiangjun Chen (Chairman) have sold a total of 2.8m shares at CNY9.35 - while these trades are modest relative to their holding (both own 10% of the company), they are rare enough to be a concern, especially at this price level. Li started to sell shares at CNY8.79 in Sept and is now selling an additional 1.4m shares. Chen's last sale goes back to Dec 2020 when he sold 1.6m shares at CNY21.32 and he is now selling at a price 2x lower.

Horizon Insights

Policy catalyst in China's software industry

To combat uncertainties caused by sanctions and rising geopolitical tensions, and more importantly, to improve the rate of self-sufficiency in the critical process of production in various industries, the government has implemented and heavily promoted the Xinchuang Standard Pilot Program, which is one of Horizon Insights’ long-emphasised investment themes for the tech sector. Investors should be focusing on office automation and the industrial software industry with companies such as Kingsoft Office, Hundsun Technologies, Weaver Network, Seeyon, Kingdee and SUPCON well placed to benefit.

Macro Research

Developed Markets

Talking Heads Macro

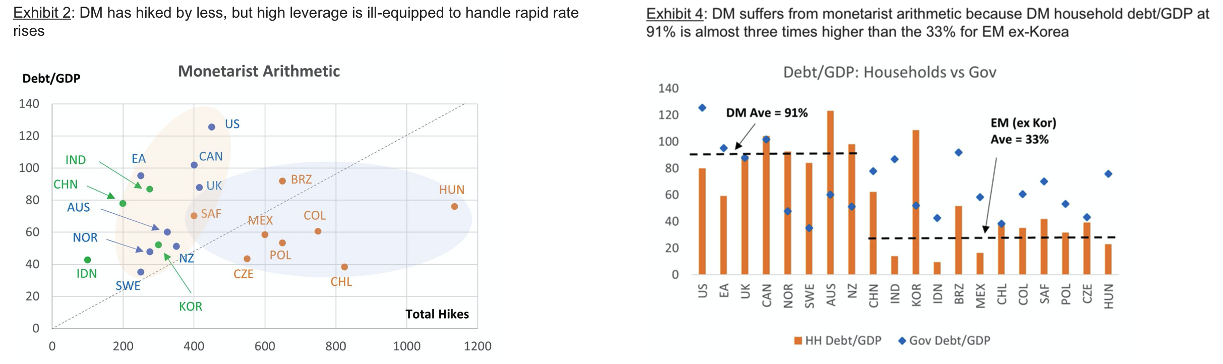

DM risks greater than EM – some unpleasant monetarist arithmetic

The Fed’s new put option is centred around bond auctions, not the equity market, which Manoj Pradhan explains is due to the ‘unpleasant monetarist arithmetic’ argument. In a highly leveraged economy, any sharp increase in interest rates creates two effects. First, it directly increases the cost of refinancing debt. Second, it slows the economy down and creates a larger cyclical deficit. Eventually, as the overall deficit increases, the central bank is forced to monetise an even bigger deficit than the one it sought to offset. This argument is what central banks in highly leveraged DM economies are up against today (see charts). The speed at which DM central banks have belatedly hiked policy rates and the distributional fact that DM household debt/GDP is miles higher than EM only makes matters worse.

Greenmantle

UK: Sunak in power

Gilts and domestically focused equities rallied in response to Sunak’s appointment as Prime Minister as Niall Ferguson sees UK asset markets moving into a period of relative stability. Sunak will change little with Hunt’s fiscally punitive budget; the budget will still feature large-scale fiscal consolidation and take some pressure off the BoE to enact a steep rate-hike path, with Niall expecting a 75bps hike in the next BoE meeting, but the UK economy still faces real headwinds and growth will grind to a halt over winter. He remains neutral UK assets with a bearish medium-term macro outlook.

True Insights

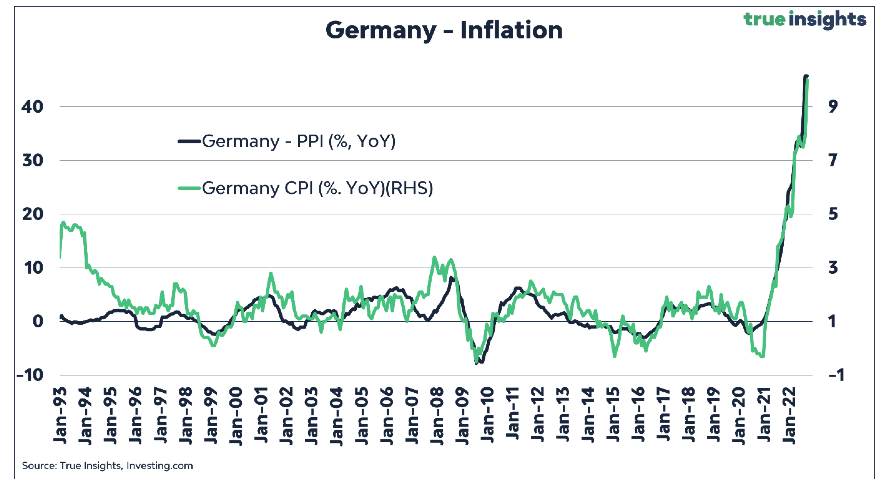

Calling peak German headline inflation

German producer prices rose by a staggering 45.8% yoy in September, matching the biggest increase ever recorded (August). However, with energy prices down massively in recent weeks, Jeroen Blokland says the peak in German headline inflation, and the inflation level in many other countries, is imminent. This will likely be a catalyst for another bear market rally, but central banks will prove reluctant to hint at a pivot at this stage. To restore credibility, central banks must remain hawkish for longer. Therefore, Jeroen thinks it too early to position for an inflation-driven central bank pivot.

Independent Strategy

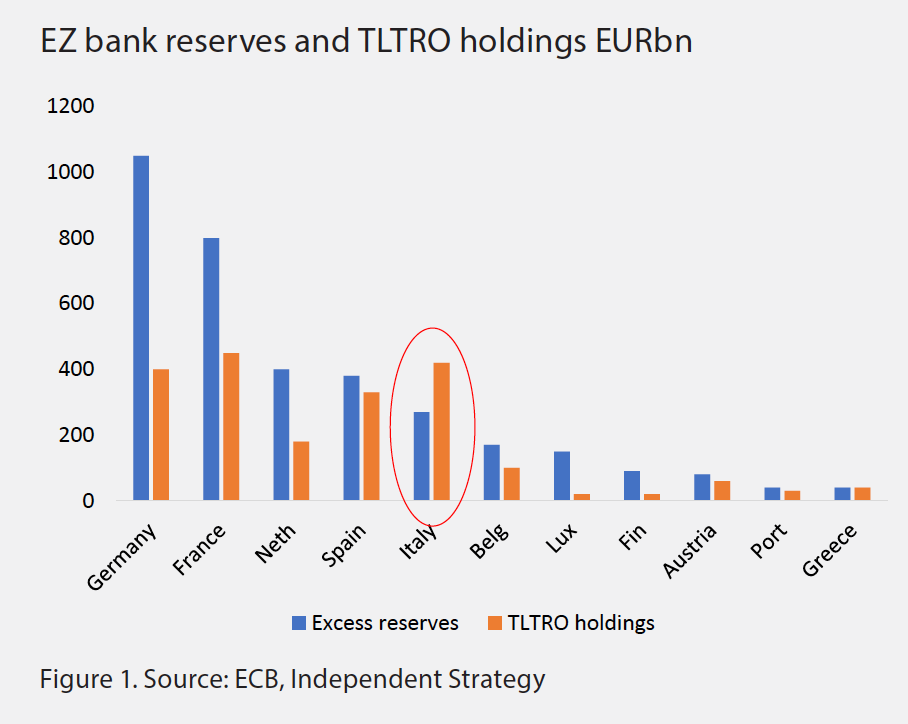

ECB: Unintended consequences

The ECB raised its policy rates by 75bp but made no change to the reinvestment of bonds maturing on its balance sheet. The big change came in amendments to its Targeted Long Term Refinancing Operations (TLTROs), which are legal changes and will damage the ECB’s ability to use such instruments in future crises. This change is undoubtedly a tightening of monetary policy; but not one that favours the currency because it raises the risks of unintended consequences from liquidity tightening. With TLRTO-III amounts over EUR2.2trn, a liquidity fallout is inevitable and Italian banks are most vulnerable (see chart).

Andrew Hunt Economics

Bonds are interesting, and the UK is not alone

The UK has made clear the problems of prolonged exposure to QE. Although the supply of US Treasuries to non-bank investors has already surged by $500bn or more so far this month, we still have another $1trn of US debt issuance to absorb before year end. In the near-term, Andrew Hunt expects this to unsettle debt markets and reveal fragilities in many of the world’s long-term savings companies. However, once the glut of issuance subsides, the disinflationary recession should allow bond markets to rally, and we may see US yields finish this quarter lower than they began it.

AAS Economics

Yield curve flattening ahead

With inflation numbers continuing to surprise many analysts, Frank Shostak explores the outlook for the slope of government yield curves in a range of countries, including the US, Germany, UK, Japan and Australia. Using his proprietary metric “liquidity”, which is a measure of excess money, Frank finds that the trend toward yield curve flattening that he predicted over a year ago is likely to remain in place for most markets through to the middle of 2023. The one standout appears to be Australia, where there are clear advance signs of a possible reversion to curve steepening emerging around mid-year.

Asymmetric Advisors

BOJ’s policies likely to sink Japan’s government and its economy in 2023

With Japan’s inflation rate approaching its 40-year high, more market participants are now pointing to Japan as potentially the next epicentre of economic turmoil. Ironically, Liz Truss’ short lived UK government was sunk as she was blamed for not listening to her economic experts and the BoE, yet in Japan the likely downfall of Koshida’s government could stem from abiding by the BOJ’s recommended policies and we will see his exit in 2023.

Deep Macro

Profit margins won’t keep inflation from falling

Consumer-related price indicators have been sticky, which Jeffrey Young remarks may have to do with efforts in some industries with average and falling margins to push through price increases. But Jeffrey doesn’t see any strong reason to suggest that, on the whole, firms will be more eager to pass through cost pressures. Should such efforts continue, the pressure on prices will be met with resistance in the form of weaker demand. Make no mistake, most signs point to lower inflation in the near-term.

Emerging Markets

Topdown Charts

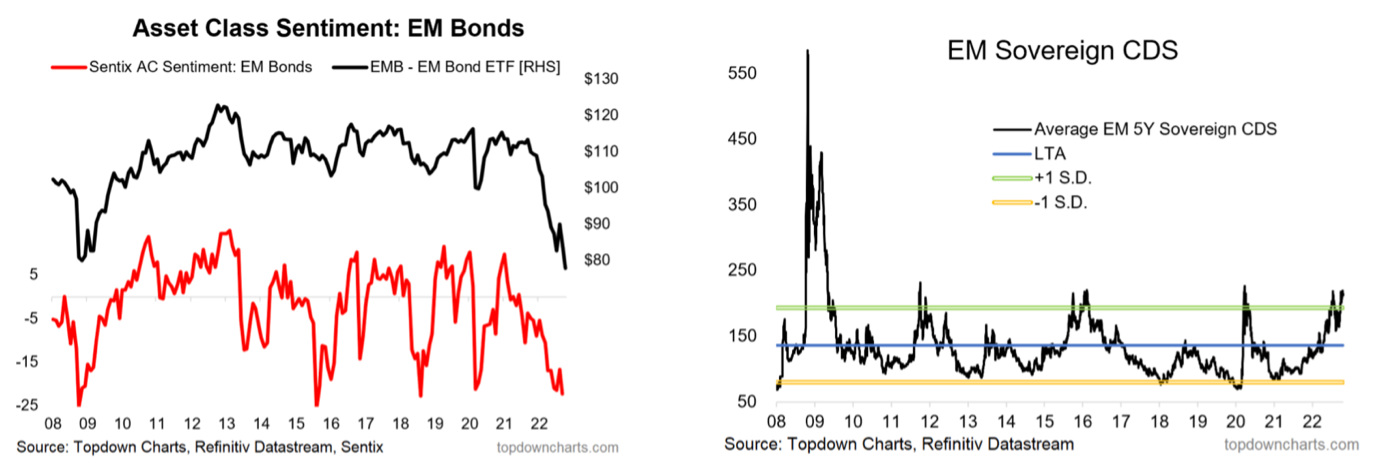

Stay the course bullish on EM bonds

EM 10yr yield have, alongside DM, made another push higher, but there is a tentative technical topping signal. Callum Thomas also notes the extremely bearish sentiment by investors on EM bonds, and EM sovereign CDS premia being pushed to “cheap” levels (see charts); add to that a compelling valuation picture with EM sovereign yields massively overshooting the fair value model. With leading indicators pointing to recession, it’s just a matter of time until more join the rate cutting camp in EM, making for a bullish medium-term setup for EM bonds.

JST Advisors

China to end the year as one of the lowest yielding countries in the world

China is trying to become Germany, with low yields, a big external surplus and low nominal yields. Jonathan Turek asks the question: how does China maintain this position as a low yielder without FX going through a material adjustment? Despite CNH weakening a lot vs USD, the CFETS basket is still at a very elevated level and Jonathan ponders over how sustainable this is. He wonders if the next Covid trade to fall back to trend is the massive move in the CFETS basket where CNH outperformed every other FX other than USD over the past two years.

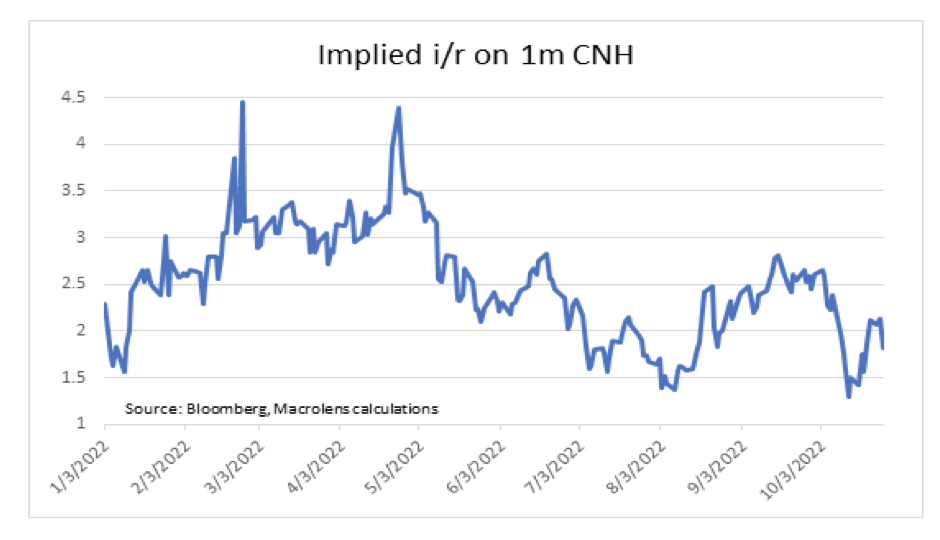

Macrolens

China: Don’t be dissuaded from playing USDCNH from the long side

In light of the second bout of PBoC dollar selling in recent weeks, Brian McCarthy tells investors not to be spooked from playing USDCNH. Even if the peak in Fed Funds rate gets pulled forward to December at 4.375%, the RMB is unlikely to find meaningful support so long as China growth continues to disappoint. Remember to maintain long-dated CNH funding. We’ll know the PBoC is serious about drawing a line in the sand when they squeeze liquidity in the CNH and onshore FX markets, which has yet to happen. When it does happen, you’ll want to be long the 1-year, not the 1-month, as spot drops and the forward points blow out.

Variant Perception

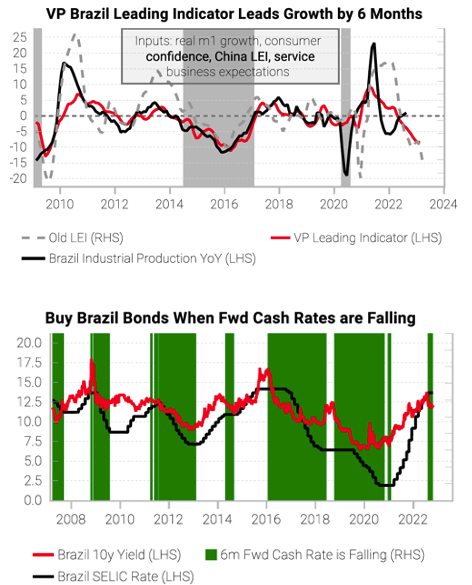

Brazil: Investment opportunity in local currency debt

Variant Perception’s Brazil growth LEI continues to fall as domestic liquidity contracts and external conditions remain very weak (see chart 1). CPI has dipped to 7.2% as tax cuts and subsidies work their way through fuel prices, and the team see it falling further in coming months. Brazil local currency government debt still remains the team’s favourite EM investment. The CPI rollover and continued weakness in growth LEIs gives them confidence that the market can move to pricing in cuts, with chart 2 showing that this is a great regime to hold Brazil debt.

Oxford Analytica

Nigeria: Islamic finance sector has growth potential

The government has increasingly resorted to Islamic financial instruments to fund infrastructure projects, with sukuk funds currently being invested in 44 road construction and rehabilitation projects spread roughly evenly across Nigeria’s geopolitical zones. The market for sukuk and other non-interest bearing financial instruments has considerable longer-term growth potential, particularly among the 55% of Nigerians who do not possess a bank account, and will attract new entrants in terms of full-fledged non-interest banks and conventional banks opening ‘Islamic windows’.

Commodities

Global Mining Research

An opportunity for gold stocks to acquire non-gold assets?

Gold companies have been actively acquiring base metal assets in the last year, and David Radclyffe wonders if this makes sense in the current market. In his latest report he finds that base metal assets can lower gold company group costs and boost cash flow, and over the last year base metal stocks have outperformed gold stocks when adjusted for the performance of the underlying metal. His preferred gold stocks with diversification of commodity mix are Barrick with 16% copper, Evolution with 20% copper exposure and Agnico which may still be 99% gold but has a growing potential for more base metal exposure.

Metals Focus

Precious Metals Investment Focus 2022/23

Metals Focus recently published its latest flagship report on investment in gold, silver, platinum, palladium and rhodium. Forecasts include an expected fall in gold price by 10% in 2023 as the challenging macro backdrop weighs on gold, with the overspill affecting silver prices, which, despite robust fundamentals, will decline 17%. Expect palladium prices to be affected by the drag of battery vehicles, with a forecast 7% fall in price. Yet, precious metals will continue their relative outperformance of equities as gold benefits from safe-haven and portfolio diversification inflows. Expect PGM prices to remain firm in 2023 with the metals subject to annual deficits.

CPM Group

The energy transition and Platinum Group Metals

CPM Group's Jeff Christian discusses some of the realities surrounding the "Energy Transition" and specifically what it means for Platinum Group Metals. Additionally, Jeff discusses the coming recession, gives an update on some of CPM Group's public theoretical hedges, and provides data refuting the claim that gold is moving from west to east.

Click here to watch.