Company & Sector Research

Europe

Copley Fund Research

UK Fund Positioning Analysis

Steven Holden looks at Energy allocations among UK active funds, highlighting a rotation back into the sector. So far, it is confined to a few select investors, with the majority still underweight and Growth funds missing from the picture. He also examines holdings in UK Airlines as allocations and ownership falls to all-time lows, whilst Apparel & Footwear soars to new highs. In the final part of his report, Steven focuses on the continued selling of shares in Vodafone (led by Growth managers, whilst Value investors are not stepping in) - with such a positioning overhang, more selling appears the most likely outcome.

Woozle Research

Upgrades the stock to Buy - Woozle’s primary research reveals LFL sales +4% Y/Y in Europe this quarter, with 50% of stores beating targets. UK And Italy foot traffic levels are beating expectations due to new perfume and fragrance offering. In APAC, LFL sales trends are +2% Y/Y in 4Q22 as intra-Asian tourist activity increases. Local customer demand rises in Nov vs. Oct resulting in higher units per transaction. Male formalwear outperforms expectations. Also noteworthy, 70% of total sales have been made at full price across Europe and APAC, marking similar Y/Y trends in pricing mix.

ROCGA Research

ABF looks undervalued using ROCGA’s Cash Flow Returns on Investments based DCF tools - they have modelled this company, back-tested the model driven valuations, and then used the same assumptions along consensus EPS to estimate a target price. Being prudent and given the uncertainty, they also add 2% to WACC. The adjusted target price offers significant upside. It takes about a minute to model and value a company using ROCGA’s systematic and interactive valuation tools. More details can be found here. They currently cover over 1,800 companies (500 UK, 400 European and 900 NA). A free trial is available on request.

New Constructs

PEBV ratio of 0.3 means the market expects NOPAT to permanently decline by 70%. This expectation seems overly pessimistic for a company that has grown NOPAT by 30% compounded annually since 2016. Even if the energy company’s NOPAT margin falls to its five-year average of 7% (vs. 12% TTM) and revenue falls 1% compounded annually for the next decade, the stock would be worth $75+/share today (30% upside). Should TTE grow profits more in line with historical levels, the stock has even more upside.

Creative Portfolios

It is remarkable that given the monumental restructuring / reorganisation (based on survival) a leaner de-risked bank has emerged with a solid sizeable revenue-generating model and ROE of 14%, LDR of 63%, NPL ratio of 5.6%, and CIR of 47%. 3Q22 results showed progress on several fronts and with €18bn of cash on the balance sheet, the shares are lowly valued. Franchise Value and PBV stand at 3% and 0.3x respectively. Given that TPEIR is now reporting better ratios and trends than peers, Paul Hollingworth argues it does not merit to trade at such a wide discount. A PH Score™ of 10 (out of 10) only increases his conviction.

Iron Blue Financials

An Iron Blue score of 28/60 is top quartile - fertile ground for shorting. Accounting red flags include: margin recovery supported by falling D&A (partly following stripped out asset impairments), above avg. use of provisions accounting, contract cost capitalisations at a decade high, widening gap between headline net debt and Iron Blue’s measure, and €99m Y/Y increase in reverse factoring. Governance red flags: combined chair/CEO/controlling shareholding, disparity between shares and votes, Bellon cross holding, above avg. non-audit payments and auditor tenures of 19 and 28 years. FY23 brings a change in auditor.

North America

Hedgeye

Stock surges after Bob Iger returns as CEO, but Andrew Freedman has a really hard time seeing how you make money being long DIS over the next several months - while he is an Iger fan, the reality is that the business is incredibly challenged on many fronts. Tough decisions are required. Andrew thinks they should be moving as much of the linear content over exclusively to streaming as fast as possible and start raising the price on the DTC bundle in the process. Consensus has EPS going from $4.17 in FY23 to $6.57 in FY25, but he doesn’t expect to see $5.00 in EPS again until FY27. Don't chase the shares higher and look to short $110-120.

Arete Research

You can’t fight gravity - Arete previously discussed how TTD’s messianic rhetoric perpetuated a set of misconceptions about its business to help it maintain valuations several standard deviations above everything else in ad tech. They now see this coming to a “pinch point” in ‘23E, when growth reverts to a mean closer to industry averages, when TTD’s efforts to inflate its take rate get exposed, and the gap between its “save the industry” rhetoric and own operations collapses. Trades at 33x ’23E consensus Adj. EV/EBITDA despite having ~40% of net revenues at risk from pending policy / regulatory changes. TP $27 (50% downside).

Smart Insider

Jill Hazelbaker (SVP, Marketing and Public Affairs) sold 113,100 shares from Nov 11-15th at an avg. price of $30.57, reducing her holdings by 58% to 80,750 shares. This follows an Aug sale from her of 46,875 shares at $32. Smart Insider ranked this stock -N on Aug 8th based primarily on selling from Tony West (Chief Legal Officer and Secretary since 2017) at $31.26, where he reduced his holdings by 38%. These are concerning sales from key operating officers. They are downgrading the stock further, from -N to -1.

Quo Vadis Capital

John Zolidis thinks this could be his number one short call ever in terms of market cap destruction - analysts are forecasting an 18%-30% increase in profit per average restaurant over the next two and three years, respectively. John’s call is that this cannot be achieved with the current combination of aggressive price increases, cuts to labour and customer losses. He predicts negative M-HSD transactions in 2023 and a miss to total sales and earnings forecasts. A re-rating to a low-mid-20s P/E gets you 30%-40% loss in equity value for CMG.

Gordon Haskett Research Advisors

Time to add more Off-Price Retail exposure - while Chuck Grom turned incrementally more positive on the OPR space when he recently upgraded TJX to Buy, he has been waiting for more “evidence” that middle-income shoppers would begin to trade down, while simultaneously looking for proof that inventory levels would improve. Commentary from Walmart, Target and Kohl’s suggests that this trade down is now occurring, while most retailers have made commendable progress since 2Q on the inventory front. As a result, Chuck upgrades ROST to Buy and increases his EPS estimates for FY22 to $4.30 and FY23 to $5.40.

Cmind

3Q22 Earnings: A Quantitative and Predictive Outlook

For 3Q22, Cmind made 396 US company predictions on EPS beats / misses in the consumer discretionary sector. Among them, 300 companies representing 76% are predicted to miss and 96 (24%) are predicted to beat their consensus forecasts; 29% of large caps are predicted to beat their consensus while 83% of small caps are expected to miss. On a market cap adjusted basis, the predicted misses vs. beats is a more balanced 57% vs 43%. Additionally, Cmind provides financial and linguistic drivers behind the predictions.

Portales Partners

“DJ Sol” remix uninspiring - Charles Peabody at a loss as to what the new strategic plan / organisation will do to improve the operation of the firm. This effort comes at a time when earnings are pressured, especially in the Investment Banking division, which is CEO Solomon’s heritage. The traditional conflict between ‘Trading’ and IB typically flares during bonus season, and, this year, GS faces the additional burden of the money losing Consumer Bank initiative. Recent media reports of certain cultural aspects at GS are no coincidence and reflect both dissatisfaction and possible tumult.

Paragon Intel

FTX’s collapse sparks interest in the different actors in the crypto space - Paragon to begin vetting COIN’s CEO Brian Armstrong and CFO Alesia Haas. While they have no reason to believe that anything not "above-board" is occurring at the company, key executive departures, large insider selling, and self-assessed internal controls in a very volatile asset class should always require further examination.

Thompson Research Group

Rebuilding from Hurricane Ian: Feedback from the field…

TRG recently spoke with a Florida based independent building product distributor on the expected rebuilding cycle for Hurricane Ian which caused ~$50bn in damage to the state. Their contact anticipates a new residential construction dynamic to Florida not seen after previous destructive hurricanes and that ~50% of the homes lost will not be rebuilt due to building codes and insurance constraints. This event highlights the need for specialty building products that are more resistant to extreme weather fluctuations. TRG's upcoming report will focus on outlining opportunities in this space.

Inflection Point Research, LLC

NVDA's dominance in AI workloads, both in cloud computing infrastructure and other implementations, remains very much intact - Michael Fox believes the bevy of current start-ups will have a steep uphill climb to get any traction in high volume AI deployments (i.e. cloud), and while Advanced Micro Devices and Intel have competing solutions that look good on paper, both fall short in ecosystem and support. Ultimately, Michael expects the real competition for NVDA’s dominance will come from internal chip developments at the hyperscalers. Fortunately for NVDA, any true competition is years down the road.

Summit Insights Group

Earnings beat expectations and Next-Gen security ARR surpasses $2bn for the first time, in what Srini Nandury describes as a “stunning achievement” - PANW continues to see strong demand as security remains the most resilient of IT budget priorities within the enterprise and the group now possesses arguably the broadest offering in the industry. Srini expects Cisco will continue to cede share to PANW (as it has been doing for the last several quarters). The stock trades at 5.3x EV/C2024 sales vs. peer avg. of 5.0x, but a premium multiple is warranted. Srini's $200 TP translates to 6.7x EV/C2024 sales of ~$9bn.

Australia

Global Mining Research

GMR’s two preferred junior copper names - in addition to offering growth at attractive valuations, their scale, longer mine lives and exploration upside also highlight potential corporate upside as industry peers seek to increase their exposure to copper and the EV materials thematic. The two miners are rapidly evolving businesses; a year ago they each had half the number of producing assets as they do in 2022. SFR is GMR’s cheapest copper stock. It trades at a P/NPV multiple of 0.5x and prospective FY24 FCF yield of 11%. At +200kt/yr from 2023 CS offers scale / leveraged exposure to copper.

Japan

Asymmetric Advisors

Whilst Nikon shares have recovered 90% from early ’21 lows when Asymmetric Advisors first recommended the stock and earnings will slow into next FY, the company seems on course to make a major transition from a contrarian / value to growth name. This is because not only has it restructured and reoriented its camera business but due to the emergence of one new earnings pillar (lenses for EUV inspection) and the potential for a second (the purchase of metal 3D printing machine maker SLM). Meanwhile, PER at 11x, 0.78x PBR and potential for further buybacks provide valuation backing.

Singapore

LightStream Research

Shares were up over 30% following a relatively small topline beat of 4.8% and a narrower than expected operating loss of $495.6m - Oshadhi Kumarasiri sees this as a great opportunity to make substantial gains on the short side in the near term as e-commerce and fintech remain unprofitable after cutting down necessary expenses such as logistics facilities and senior management cash compensation. Oshadhi estimates fair EV at ~$10bn (Gaming: $2bn, e-commerce: $5bn, Fintech: $3bn) vs. the current EV of $33.1bn, which implies 66% downside to Sea’s post-3Q22 price.

Emerging Markets

Aequitas Research

US$20bn overhang for Meituan as China's social media giant slashes its stake in the food delivery firm from 17% to just 1.6% - the share distribution follows the template of the US$16bn worth of JD.com shares that Tencent paid out after its dividend announcement at the end of 2021. In this note, Sumeet Singh discusses the implications of the deal and thinks next on the list for stake divestment is likely to be Pinduoduo, but that will have to be via a placement as it trades in the US.

Silk Road Research

China Autos: Production cut risk rising

SRR's channel checks reveal a significant softening in auto demand despite positive seasonals and an expiring stimulus programme - auto registrations turned negative in Oct vs. normal seasonal patterns that would have implied >20% Y/Y growth a couple months ago. As production was less impacted, implied dealer inventory levels have likely reached unsustainable levels, increasing the risk of production cuts in the coming months. For perspective, wholesale sales were ~40% above retail sell-through in Oct, bringing YTD production ~20% above retail. This is the highest in SRR’s data history going back to 2012.

Macro Research

Developed Markets

Eurointelligence

UK trade deals under scrutiny

The rancour over the planned UK-India trade deal that PM Sunak pushed for in Bali, in addition to the earlier one with Australia, has a lot to tell us about the gap between rhetoric and reality of making Brexit work, explains Wolfgang Münchau. In the 2016 referendum leavers touted the ability to sign new trade deals as a central benefit to leaving the EU, but the rush to sign new deals is doing more harm than good. Wolfgang believes Brexit could still work, but the opportunity, which would involve deep structural changes to the British economic model, is passing the government by.

Deep Macro

Discussing the Fed

In Jeffrey Young’s latest episode in his podcast series “The Future of Finance”, he talks with Bill Dudley, former President of the Federal Reserve Bank of New York and FOMC Vice Chair 2009-2018. They discuss issues related to the inflation surge, the Fed’s “flexible average inflation targeting” framework, crypto, a Fed “pivot”, and what markets get wrong about the Fed.

Click here to watch.

Macro Hedge Advisors

US: Monetary perspectives in the aftermath of US elections

In the political marketplace and financial markets, dominant speculation is that the oncoming recession will only be mild. Brendan Brown disagrees, with his central scenario being a severe US recession. Actual monetary disinflation most likely came very late – much later than when the propaganda from the Fed took its hawkish turn. If a severe recession emerges, questions will emerge over how we can reform the monetary system so that the inflation shock can never happen again. In his latest report, Brendan explores these possibilities, including restoring a monetary base for which there is a strong and broad demand, and repealing legislation that enables the Fed to pay interest on reserves placed with it by the banks.

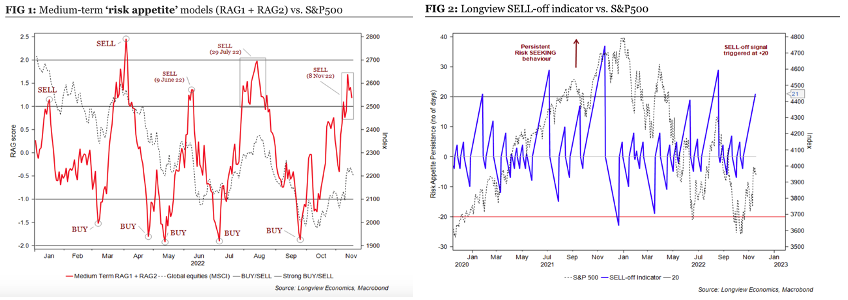

Longview Economics

US: Bear market rally over?

Earlier last week, Chris Watling moved underweight equities on a tactical basis (1–4-month). His rationale was essentially two-fold; first, we are still in a cyclical equity bear market, and markets should continue to trend lower into H1/2022; second, his market timing models (including Chart 1) - which have been timely and effective this year at picking the local highs and lows in this downtrend - have changed their message. In addition, his sell-off indicator, which generates a signal after periods of excessive short-term greediness in global financial markets, moved above its key +20 level (chart 2). Expect more outperformance from the defensive areas of the market as we move into 2023.

CrossBorder Capital

US: Has the US Fed already paused and started to pivot?

Liquidity matters to markets, exclaims Michael Howell. However, the recent sharp rally in stock prices hints that again there is more money around. Digging deeper into Fed operations shows that the effective QT (quantitative tightening) programme has stalled so far in Q4, even reversing to the tune of US$167bn of QE. This plainly goes against the tenor of Fed policy rhetoric and supports those (including Michael) who feel we may be close to a policy ‘pivot’. This move back to QE shows how hard it is operationally to remove liquidity, especially with the mighty Treasury market itself looking technically vulnerable. It will pay to watch this space.

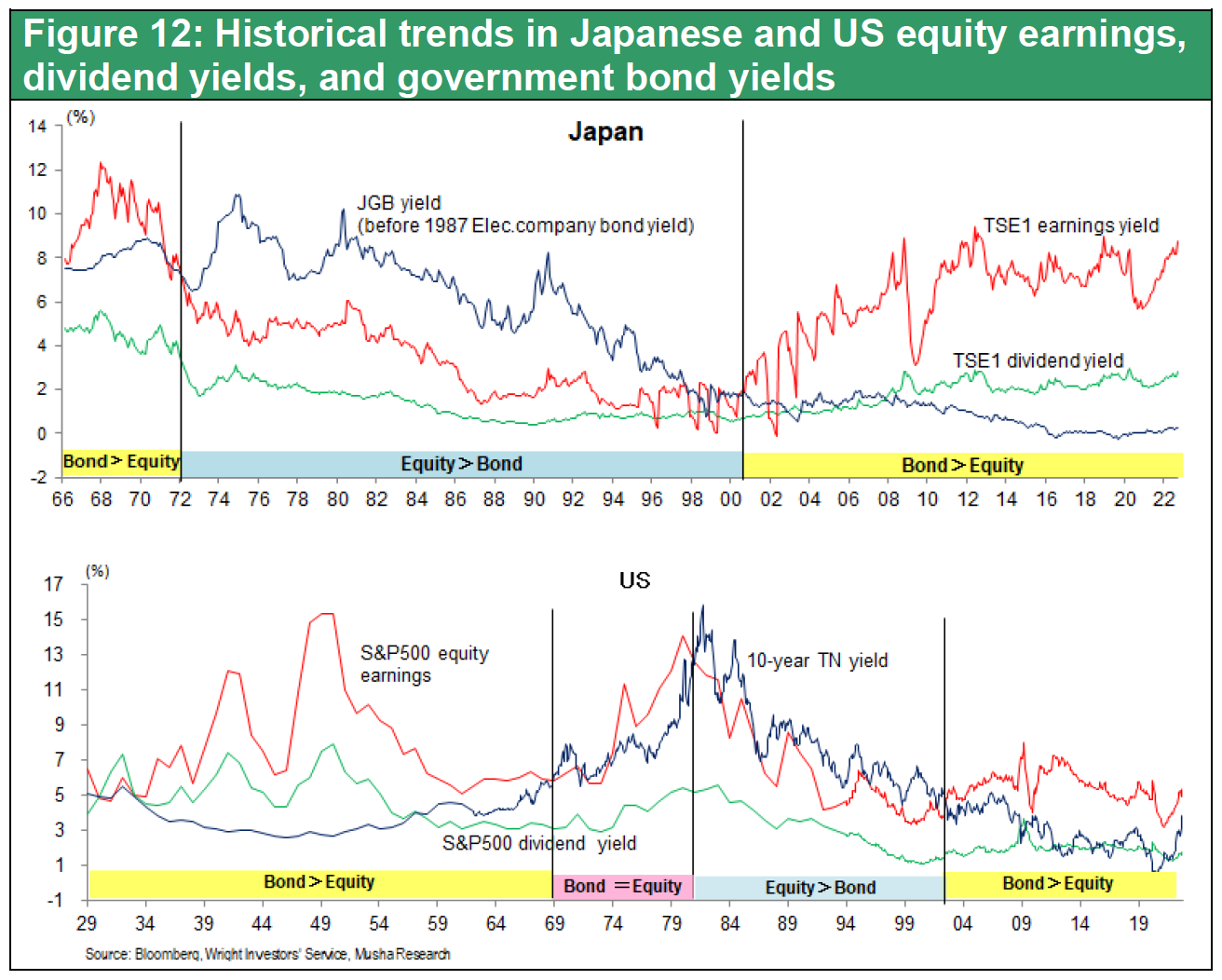

Musha Research

Now is the crucial moment for Japan

Ryoji Musha claims that 2023 will be a turning point for Japan’s great revival. The rapid depreciation of the yen will bring factories, capital, business and opportunities to the nation, the shift accelerated by the growing US-China conflict. However, Japanese companies will need to adapt. The supply chain portfolio must be radically transformed toward one of domestic production and a major change in corporate financial and capital policies is also needed. Ryoji ends his report by emphasising that we are at an era of unprecedented equity investment opportunities, one where the money from selling bonds or withdrawing deposits can be used to buy stocks to gain tremendous advantage (see chart). Don’t miss out!

Harlyn Research

Upside protection: The need to hedge against unexpected good news

Simon Goodfellow’s models are slightly conflicted at the moment. The multi-asset models, which mimic sophisticated institutional portfolios, are significantly more bearish than his simple equity vs government bond models, which are more retail-orientated. Simon ponders an explanation behind the difference. Retail investors may be trying to hedge against the possibility of unexpected good news: a shallow US recession; a peace deal in Ukraine; or an end to zero-Covid in China. Any one of these could result in significant upside for global equities, and the joint probability that none of them will happen is lower than you think.

Emerging Markets

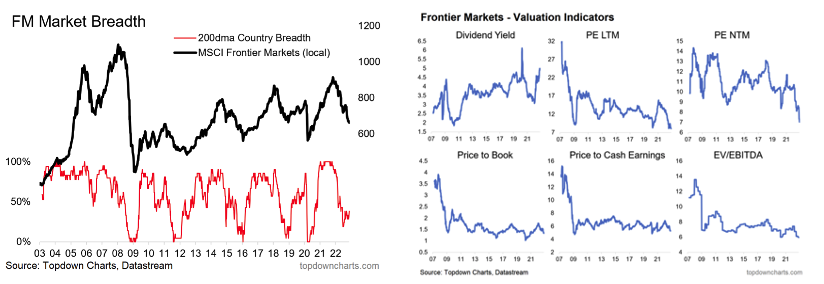

Topdown Charts

The underlying strategic case for frontier markets remains compelling

Despite a worsening frontier market (FM) outlook, Callum Thomas remains optimistic. On his breadth indicators, there is an initial bullish divergence in the 200DMA country breadth indicator (chart 1). He also comments how the recent underperformance has been precipitated by the global slowdown, but this now makes FM valuations particularly attractive with most indicators either at the bottom end of the range or at record cheap levels (chart 2). FM has the best demographics, and with the valuation adjustment it sits at the top of the table in expected returns across global equities, double digits expected.

Andrew Hunt Economics

Asia’s forex reserves are falling

The rate at which the Asian economies are depleting their forex reserves has re-accelerated. Andrew Hunt sees this rate of reserve loss as evidential of the extent of problems within the region’s credit system. The weak balance of payments / reserve loss implies that any counter-cyclical policies in afflicted nations would result in severe impacts on their currencies and inflation rates, with the PRC and Hong Kong among those most affected. As weak growth and credit trends add to immense pressure building on the HKD peg, should the HKMA to attempt to ease the pain, expect the peg to break.

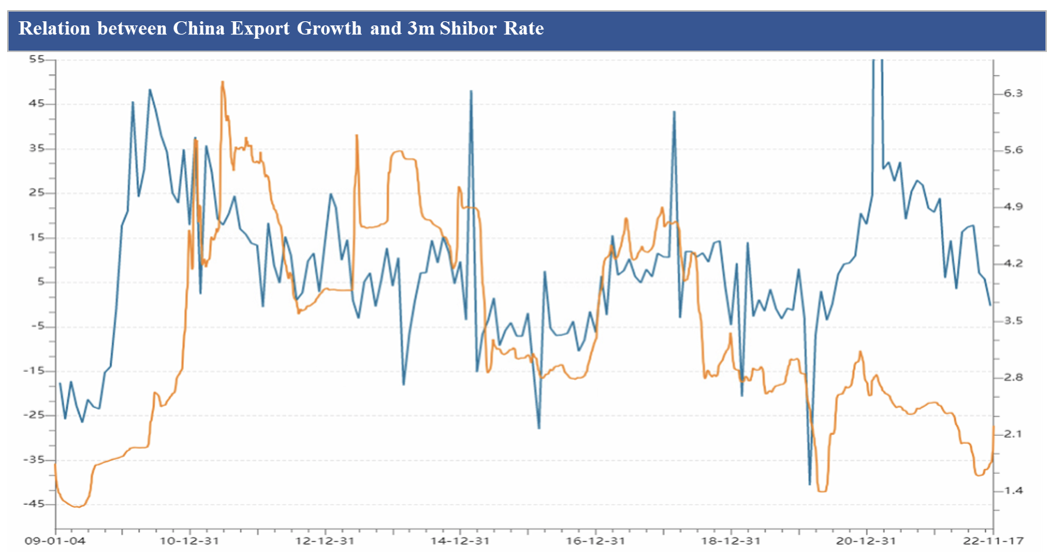

Horizon Insights

China: Bond market panic & downward risks in Q4

With positive changes in Covid policy and easing property measures, China’s benchmark interest rates have shot considerably higher in November. However, the Horizon Insights team believes that the still-weak fundamentals don’t support such a sharp increase, especially with the simultaneous slowdown in Chinese exports and real estate – expect benchmark rates to stay at relatively low levels in coming months (see chart). As we pass through Q4 the major risks of a US and Chinese tumble are growing, which could bring a huge shock to the global economy.

Trivium China

China’s economic recovery clicks into reverse

Economic indicators for October missed expectations across the board. The impact of a Covid-induced fall in consumer spending has been compounded by a muted policy response, with Beijing unwilling to unlock enough stimulus for an infrastructure-led recovery. More concerningly, the business environment at home and abroad is becoming less favourable, with an elevated demand for Chinese goods overseas rapidly fading. The announced Covid and real estate policy changes will not be enough to repair the complete and utter destruction to consumer confidence.

Alef Advisory

Russia: The macro implications of sanctions

Following the initial shock of sanctions being imposed on Russia, most macro data initially appeared encouraging; the currency was stable and even strengthened, inflation was moderate, and budget revenue from exports was robust. However, in the short- and medium-term, Hani Sabra expects the data to worsen and reflect the economy’s decline. Next year we are likely to see a shrinking economy and workforce, stagnant consumption, and more pressure on the budget – all of which limit the government’s ability to mitigate sanctions by throwing money at the problem.

Greenmantle

The struggle for Taiwan

If Washington loses the ability to prevent a Chinese move on Taiwan, it could turn to a strategy of economic and political punishment, explains Niall Ferguson. Both sides could withstand months of economic punishment, but which side can tolerate more pain? In any such scenario, commodity markets would break up, with gluts in some places and shortages elsewhere. Supply chains would seize up, followed by a severe global financial crisis. With markets in full risk-off mode, emerging markets would need emergency financing. Most would turn to the Fed, Treasury, and IMF for assistance. This would ensure that the dollar prevailed. Russian assets, gold, and the Swiss franc would be among the biggest winners.

Emerging Advisors Group

A chance to buy Vietnam cheap

Vietnam markets have taken a sudden beating this year, with a dramatic reversal in equity prices, capital outflows and the first VND devaluation in a long time. However, explains Jonathan Anderson, the reality is threefold. First, Vietnam has been caught in the same wave of outflows that has taken out the rest of EM. Second, despite some wobbles, there’s no signs of serious imbalances in the domestic economy. Third, Vietnam’s underperformance in the equity market is about sentiment and valuations, with multiples falling from a sharp premium to EM levels to “just in line”. Vietnam’s export story is as strong as ever, use the current sell-off to BUY continued medium-term growth.

ESG

View from the Peak

Voluntary Carbon Markets: A Gold Rush

Paul Krake’s first major report from Climate Transformed looks at the world of Voluntary Carbon Markets (VCM). In his 175-page report, stemming from 28 hours of interviews with executives from around the globe, Paul explores the future of VCM, potential technologies (including blockchain and Web3), the state of supply, transparency, and implications for investors and companies. The conclusion is clear: there is a tremendous opportunity for growth and the price of all voluntary carbon offsets will move dramatically higher in the years ahead. Please contact us to find out more.

Commodities

Queen Anne's Gate Capital

Current trends prove Russia is the ”new” ESG

Kathleen Kelley has long touted Russia to be the “new” ESG, i.e. the theme that will define the energy markets for the next decade. As if the energy transition wasn’t enough, the world is attempting to navigate away from Russian oil and gas at the same time. So far it has been a disaster and idealism on clean energy has been thrown out of the window; more and more European countries are returning to burning coal or oil for power. There is a land grab for any and all energy, and most of it is dirty.

CPM Group

Cryptos are not precious, gold and silver are

The FTX bankruptcy is only the most recent in a long line of cryptocurrency scandals. Jeffrey Christian discusses CPM Group's view on cryptocurrencies as well as some of the major differences between gold, silver, national currencies, and crypto. He also discusses the short and long-term effects of cryptocurrencies on gold and silver investment.

Click here to watch.