Company & Sector Research

Europe

New Street Research

UK Altnets Review

Base case for Openreach is the altnets (ex-Infravia JV) reach 13m unique passes and 25% penetration. However, with Equinox 2 on the horizon, life will be tougher for most altnets, especially those that are retail facing, as the major ISPs accelerate their migration to the Openreach FTTP platform. For CityFibre, which relies on wholesale contracts and has commitments with leading ISPs, their position should be stronger and they will emerge as the market leader, and yet New Street’s base case EV is still negative. In this note, they assess the implications of this, what can happen to increase value and next steps for the UK market.

Arete Research

Management exodus continues - ASC’s interim CFO is the latest to go. The lack of internal controls brings into question the firm’s ability to work through their long to-do list (growth outside UK, brand partnership expansion, extending target audience, stretching wallet share and its Partner Program roll out) and near-term challenges (cash, management, etc.). In their previous report, 'Online Fashion: Predator or Prey?', Arete cut their TP to 200p (from 300p) - believes ASC could end up facing a stark choice between a set of acquirers, possibly Zalando or PE, before seeing its equity being wiped out by rising costs / debt burdens.

Woozle Research

Woozle remains bearish based on their findings from recent surveys with store managers in France and Brazil - French Carrefour stores report +1% LFL sales growth in 4Q22, missing street estimates of +4.4% Y/Y. The majority of respondents revealed pricing levels higher than discount retailers and expressed worries surrounding customer retention going forward. Several stores reported flat or decreased foot traffic in early signs of reduced demand. Widespread supply issues are affecting inventory levels and SKU availability. Brazilian Carrefour stores report +17% LFL sales growth, also missing expectations.

ResearchGreece

Doubles its stake in Hellenic Bank to 26% to become the largest shareholder in Cyprus’ second biggest bank - valuation wise, EUROB is paying a higher multiple than when it bought its original stake (July 2021), but the truth is the outlook has improved a lot, thanks to higher rates by the ECB and HB’s enormous cash balance of €5.3bn (excl. TLTRO) equal to 27% of its total assets. ResearchGreece expects HB to revise its RoTE target >10% from c.7% previously. Using 12% CoE they find the fair P/TBV to be closer to 1.0x, which implies EUROB bought the stake at a 50% discount to fair value.

Insight Investment Research

Robert Crimes remains very bullish re. prospects for global airports given the strong recovery in traffic from Covid, high lifetime FCF and a global weighted average IRR of 11.6% - his top pick is AENA, whose share price is down c.30% since Feb 2020. Robert expects 2019 traffic to be exceeded by 4% in 2024E and Equity FCF post all capex of €1.6bn in 2023E (same as 2019). Return on RAB of 6.4% to exceed Insight’s WACC of 6.0% in 2024E. Commercial growth is highly value accretive with >80% EBITDA margins and c.85% of terminal capex funded by decent returns on Aeronautical RAB. TP €302 (140% upside).

ROCGA Research

Looks undervalued using ROCGA’s proprietary Cash Flow Returns On Investments based DCF valuation tools - ROCGA gives you the ability to identify, research and value companies. Current coverage is just over 1,850, with 930 NA, 505 UK and 415 European companies. Model the company, back test the assumptions up to 15 years, forecast forwards with EPS, DPS and growth estimates, and the valuation engine will crunch the numbers for you. More details on ROCGA’s systematic and interactive valuation tools can be found here. A free trial is available on request.

North America

MYST Advisors

Bear’s Den Idea Forum

The average life-to-date alpha of the ~100 short ideas presented at MYST events over the trailing 12 months is an impressive 22.2% (vs. SPX), with ~80% of the ideas generating positive returns. Their latest event saw participants produce a fascinating collection of idiosyncratic ideas with meaningful potential downside including:

Automatic Data Processing (ADP) - “Obviously mispriced” and trading at all-time highs despite facing a contracting labour market. TP $112 (55% downside).

Canadian Tire Corp (CTC/A CN) - Accounts Receivable “exploding” higher as company “stuffs the channel” to hit revenue targets. TP C$100 (35% downside).

ICU Medical (ICUI) - Misguided Smith Medical acquisition is “a bad deal at a bad time”. TP $100 (35% downside).

A Line Partners

In their weekly report A Line uses a proprietary ranking system to build individual company performance history. Companies are graded A-C based on factors including product design, promotional activity and store feedback. Biggest movers last week:

BOOT - Grade B: scores 18/30, +3pts vs. previous week. Surprisingly strong Black Friday weekend and then managed to avoid the typical post-holiday lull. Seeing a lot of success with the relatively new men’s private label brand (Brother’s & Sons).

BBWI - Grade B: scores 15/30, -3pts. Missed sales over Black Friday weekend and Candle Day. The stores have been refusing shipments because they didn’t sell enough and cannot fit anything else on the floors.

Compass Restaurant Consulting & Research

One of the standout performers in Steve Crichlow’s latest Restaurant Industry Pulse Report - the burger giant enjoyed a strong performance in the US during Nov which has continued into Dec driven by an exceptionally successful marketing campaign of running multiple promotions simultaneously and all being profitable (something it has been unable to achieve since 2012). 82% of contacts interviewed stated they were pleased with the recent shifts in promotional focus. Steve now expects Dec SSS to be at the top end of his current estimates of 5-7%.

Cmind

NCLH released its Q3 earnings on Nov 8th reporting that it marginally beat consensus estimated EPS and revenue. This week Cmind predicts that the company will miss both targets in Q4. Cmind provides insights including financials (e.g. its historical “Receivables - Estimated Doubtful” being at high risk) and executive linguistic patterns (e.g. its CFO is overly bullish vs. peer companies’ CFOs). They will keep updating their predictions until NCLH’s Q4 earnings release on Feb 23rd. In predicting NCLH’s quarterly earnings target in the past 4 years, their EPS (Revenue) predictor achieved a success rate of 72% (78%).

Behind the Numbers

MO's appeal is its 8.2% yield. However, smoking income is essentially equal to the dividend. The company is already missing forecasts, and smoking income tailwinds are about to become headwinds as volume decay is already accelerating. BTN does not see much cushion for the dividend going forward. Not for the first time the tobacco giant finds itself on BTN's Quarterly Focus List - companies they believe have a higher risk of reporting an earnings disappointment based on their analysis of earnings quality. MO's EQ score is 2- (Weak).

R5 Capital

Another shoe to drop - Scott Mushkin's research reveals a worrying lack of staff in stores and it is exacerbating the distribution and logistics issues that he has been documenting for about a year. Scott estimates that adding more labour hours will cost DG at least $300m and the longer this is left to fester the more damage there will be to the business. He argues that improvements must also be made around retaining quality employees (DG ranks lowest in R5’s universe on Glassdoor). Furthermore, a loss of focus on its core strengths and over-expanding is likely to hamper results. Street expectations remain too high.

Blueshift Research

E&P outlook for 2023

1) Blueshift's oilfield sources expect capital spending to increase 10-15% Y/Y in North America next year. 2) There is a new trend underway in E&P structural realignment that may slow the hiring of more rigs. 3) Helmerich & Payne, Patterson-UTI Energy and Precision Drilling to benefit the most from a tight drilling market in 1H23. 4) Increases in wellsite intensity to benefit integrated pressure-pumping companies such as Halliburton and Liberty Energy; ProPetro is one to watch. 5) Strong demand for offshore drilling remains intact. 6) Nabors Industries’ new robotic rig technology is gaining traction.

Favus Institutional Research

Elliot Favus sees CORT being forced to “wind down” over the coming months - his earlier research revealed how the company's salesforce was paying doctors (who had no business receiving any money) substantial amounts to prescribe its drug for treatment outside of the exceedingly rare medical condition for which it is approved. Since then a Federal criminal investigation has begun, but Elliot believes the Street is misreading the nature of the investigation - he expects the prescribers who have been “bribed” to be targeted, and once this happens, CORT’s prescriber base will rapidly disappear along with its revenues.

Memphis Research Group

Built for the good times - demand has just begun to fall off which will expose the hyper-cyclicality of XMTR’s business. Long term, the company services, contrary to what bulls think, the smallest of niches within the 3rd party manufacturing ecosystem…essentially prototyping, a single digit percentage of the overall R&D budget of its customers. The structural design of XMTR’s business model will prohibit it from breaking into any meaningful production business…yet the crux of the bull story rests on this thesis.

Hedgeye

The fundamental back drop has weakened significantly for this non-cycle-tested business - Rob Simone argues the SFR industry has been a beneficiary of a tight housing market and low interest rates over the last decade. He sees a huge deceleration in SSRev coming next year with bad debt as a percentage of revenue returning to pandemic levels. He models topline growth of 3-4% and 7-8% expense growth - there is no way that INVH is going to grow SSNOI at 7.5%; Street forecasts are way too high. INVH is a consensus long, over-owned name, and Rob sees the REIT as a potential “source of funds” into long duration.

Summit Insights Group

Adult supervision to finally payoff - for the first time in several years, we are finally seeing SPLK focus on disciplined execution under the new CEO Gary Steele. Having beaten revenue expectations and EPS forecasts in 3Q23, Srini Nandury has significantly increased his EPS forecasts for this year and next (his estimates were already materially above consensus). While nobody is immune to a spending slowdown, Srini expects SPLK to fare better than many other players in the market, yet the stock trades at 3.0x EV/C2024 sales vs. a security peer group multiple of 4.9x. TP $125 (50% upside).

CTFN

European Commission officials appear to be examining whether AVGO’s proposed takeover of VMW will harm rival component manufacturers who rely on VMW’s software to test their products, a source told CTFN. The EC’s detailed questionnaires are probing what type of information customers require from VMW, as well as how easily manufacturers can switch away from its products. The EC’s questions appear designed to test a theory of harm that AVGO might have an incentive to reduce or delay information shared by VMW with AVGO’s rivals involved in the production of network-interface cards and host bus adapters.

Click here for the full story.

Off Wall Street

Stay short - while the Street recognises that ZM’s Online segment has likely peaked, it is still too bullish about growth prospects for the Enterprise segment - OWS argues that competition from Microsoft Teams and Google Meet is likely to impede ZM from attaining its mid-20s targeted revenue growth rate. Operating margin may also be lower than bulls anticipate due to mix shift to lower margin Zoom Phones and the need to up spending in R&D / S&M. The magnitude of the company’s SBC expense is starkly exposed by the fact that it has spent ~$1bn YTD on stock buybacks while lowering the share count by a paltry 1% Y/Y. TP $55.

Japan

Asymmetric Advisors

Normalisation on steroids - this M/Cap $400m e-ticketing and artist fanclub merchandising company is benefitting from the return of live events in Japan and as the No.1 e-ticket resale company is benefitting from 1) the structural shift from paper-based to digital tickets and 2) a 2019 law banning trade in paper tickets and thus take-off of the high margin e-ticket resale business. Asymmetric Advisors thinks earnings can comfortably overshoot its FY3/23 company forecast of operating profit +31% Y/Y and see further strong growth into FY3/24 which more than justifies the PER at mid-20s next FY.

Redex Research

Rakuten expanded its Mobile segment disclosure at Q3 which is great for investors but the message is not very positive as roaming costs remain elevated and hopes for a recovery are now being pinned to the receipt of platinum band spectrum but that is years away even if the regulatory outlook is improving. With a continued reliance on KDDI for roaming and the associated costs that come with it which are higher than total service revenue, Rakuten is unlikely to step up its customer acquisition efforts and that is great news for incumbents but market expectations that mobile is value destructive are unlikely to change.

Emerging Markets

Propitious Research

Outsized beneficiary from a recovery in Chinese retail sales as the fiscal and monetary stimulus, coupled with a gradual easing of China’s Zero Covid policy, stimulates demand throughout 2023. Having seen a recovery in margins YTD, Wium Malan continues to believe that JD.com can sustainably generate above 5.0% NOPAT margins vs. 1.5% YTD. Net cash of RMB186.6bn ($26bn) is equal to 32% of its current M/Cap. The stock trades on an extremely attractive 13.4% NTM FCF yield - a significant discount to its historic average trading range and global peer group.

Galliano's Financials Research

An end to Castillo’s chaotic, market-unfriendly administration with its high turnover in ministerial posts should be a catalyst for improving investor sentiment, as well as encouraging increased foreign investment. As the largest financial group in Peru, Victor Galliano expects Credicorp to be a key beneficiary of the more positive domestic political and economic backdrop, especially given its attractive valuation vs. its own history and LatAm peers. Shares to rerate higher in the coming months.

Hemindra Hazari

India: Is bank loan growth to industry really robust?

Hemindra Hazari points out that once we factor in WPI inflation, the real growth in loans to the corporate sector may be marginal or even in decline. It also appears that the working capital cycle is lengthening; if that is leading to a rise in bank credit, it is not a healthy situation. This appears to be in line with the 2Q23 GDP data on manufacturing, which too have underlined the poor state of the industrial sector. Such a scenario is worrying for the sustainability of corporate credit. And how long can retail credit continue to carry the burden of bank credit growth in these circumstances?

Radio Free Mobile

China vs. US: Digital iron curtain

As attention turns to 6G it is clear that China has no intention of repeating its semiconductor dependency meaning that two standards are likely to be developed - this will begin what Richard Windsor has long forecasted which is the splitting of the Internet into two incompatible pieces. Just as Metcalfe’s Law of Networking has made the digital ecosystem grow exponentially in value on the way up, the same will be true on the way down. Furthermore, as China continues to set its own standards in other technologies the more pronounced the negative effect will be. Revenues generated by global tech may have already peaked.

Macro Research

Developed Markets

Aitken Advisors

A new world of rising real interest rates

As important as real yields are to investors, James Aitken wonders if we should actually be looking at real interest rates. They are still negative and still historically low (see chart), but it is obvious they will rise, begging the question of whether markets have fully discounted what this truly means. For years we’ve lived in a world of ‘zero cost of borrowing’ and where - if your forecast for the price of money was ‘zero in perpetuity’ - anything that could create positive cash flows over time was worth a shot. But now this ‘double zero’ business activity and speculation is now unravelling and the hurdle rate for everything has gone up, which points to continuing de-risking. Cash flow is king, remarks James, and the sectors offering the highest, predictable cash flows remain under-owned by investors.

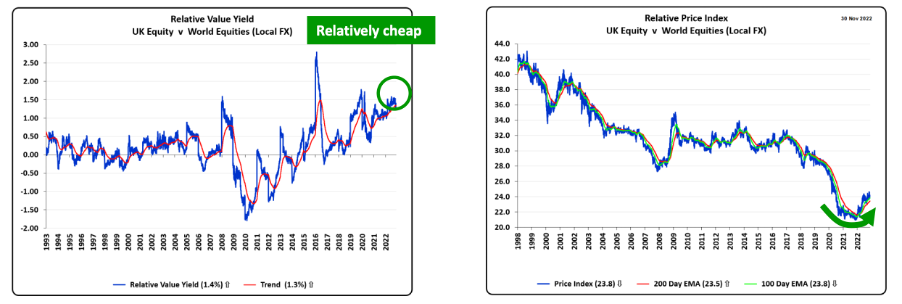

Ekins Guinness

Bullish UK

Charles Ekins and Tim Guinness’s Regional Equity model continues to be positioned significantly overweight the UK. The bullish price trends remain in place; the relative value yield is still cheap versus its long-term history as the UK has been a serial underperforming region for the past 25 years.

Eurointelligence

Germany: Labour shortages are fuelling inflation

Wolfgang Münchau asserts that the wage-price spiral is a 1970s bogeyman; modern labour markets are organised in a way that makes this particular scare story unlikely. Look at aggregate supply instead - not only physical supply chains, but also labour supply. There is robust labour market data everywhere – German unemployment is near an all-time low and job openings at a record high. Wolfgang also sees more anecdotal evidence about business closures and reduced production as a direct result of labour shortages. A fall in aggregate supply due to shortages constitutes the main engine for inflationary pressures, forcing governments to rethink their immigration laws.

Talking Heads Macro

Sweden: A path to a crisis

Sweden hasn’t had a crisis or near-crisis in the last two decades, and Manoj Pradhan sees that as a problem. The rapid increase in interest in Sweden carries a greater threat than in other economies due to household and corporate debt being linked to the property sector, financing rates being linked to short-term interest rates and a lack of savings or unfinished homes. Receive 5y+ outright, and go LONG AUD/SEK as demand growth from China becomes priced into commodities and further into AUD.

RW Advisory

USD: King of rock ‘n’ roll

The USD king of rock ‘n’ roll previously trended up by over 20%, defying gravity, sporting the equivalent of portfolio “blue suede shoes” – while other major assets collapsed! But market history teaches us that the strongest trends often give way to the greatest falls once they inevitably roll. Ron William shared early tactical warnings; notably DeMark© price exhaustion signals, coupled with overcrowded positioning that led to a sizeable bull-trap capitulation. The current DXY mean-reversion into its 200-day trend is likely to extend into support zone at 100-99. Downside risk is also pressured by a softer inflation print and the US10YR interim top which targets 3%.

Greenmantle

US: Growth scare

With every strong jobs report, US financial markets seem to experience a ‘growth scare’— a fear that the economy might perform well, defying the Fed’s planned deceleration and thus threatening markets with higher rates and lower multiples. Niall Ferguson thinks last week’s scare is overblown: it is unlikely to move the Fed off course, and in any case, strong (catch-up) wage growth will be necessary for the US to avoid recession during its current inflationary episode. Niall maintains his more-dovish-than-the-market view that the Fed will hike by 50bps in December.

PPG Macro

US: Entering the unknown

Liquidity has always been a core theme for Patrick Perret-Green. Monetary and fiscal largesse drove the ‘buy everything’ rally and as the world normalised so have markets. Patrick began this year highlighting how reserves at Federal Reserve banks had started to fall, long before QT started, and that risk assets were vulnerable. The ‘one chart to rule them all’ has worked remarkably well.

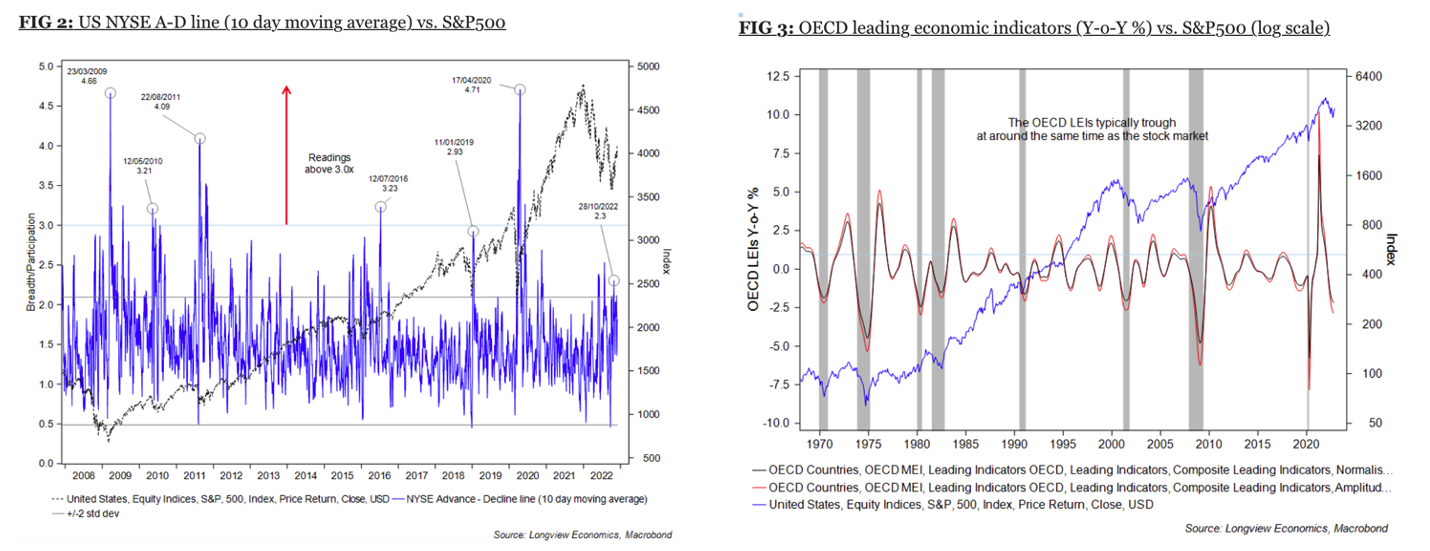

Longview Economics

Signs that the bear market is alive and well

Chris Watling questions whether the bear market is truly over. He points to breadth signals in the NYSE broad US market which, at only 2.3x, is notably below the usual breadth thrust at the start of bull markets (see chart 1). Chris also doesn’t expect LEIs to trough anytime in the next few months (chart 2), especially with the ongoing tightening of liquidity. Add to that the fact TED spreads remain elevated, and something usually breaks when that is the case during tightening phases. Pessimism may be here to stay for a while longer, after all.

Andrew Hunt Economics

Japan: The days of yield curve control are clearly numbered

As we move into the New Year, Andrew Hunt expects the BoJ to begin moving against inflation, albeit in a way that may make it difficult for people to short JGBs in the near term. YCC, playing with the mechanics of the JGB market, and FX intervention all now seem de riguer in the current micro-focused BoJ. If the BoJ tightens, the JPY may rally but its longer-term trend will be decided by how much the central bank acts and whether the social contract between policymakers and savers survives the current inflation.

Emerging Markets

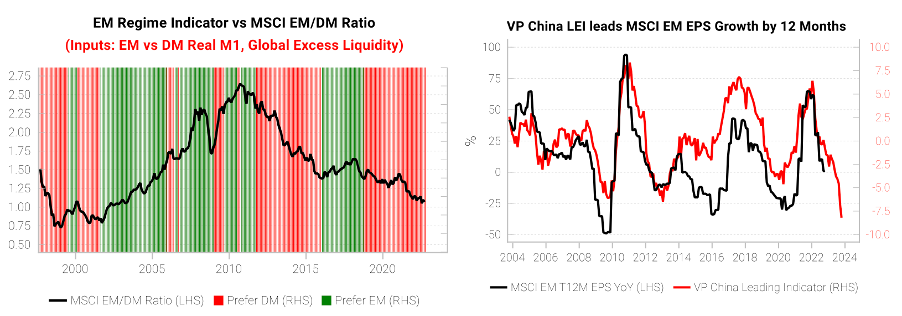

Variant Perception

EM: Consensus focused on peak rates, but LEIs not aligned

With the market narrative focusing on EMs first-in/first-out hiking cycle and getting excited for an EM outperformance trade in 2023, Variant Perception reminds clients that the best time to buy EM is when global excess liquidity is positive and EM real M1 is outpacing DM (see chart 1), and when China LEI upturns (chart 2). Their US recession signal likely delays the timing of this EM equity outperformance trade. For EM local-currency bonds to rally, markets need to price in a rate-cutting cycle. We are getting close to this.

PRC Macro

China: Limited developer bailouts

Beijing’s resumption of developer equity refinancing, among other policies, will not revive land purchases and property construction, nor will it put the property sector back on track and prompt a cyclical recovery. According to William Hess, the policies represent a “whatever it takes” moment from regulators to shore up select market traded private developers, prevent broad write-downs on bank assets and protect collateral values. William remains bullish on bonds and share prices for developers on the designated survivors list, but he is still deeply bearish for property sales, new starts, and correlated metals demand.

Emerging Advisors Group

Come on, Colombia

Whilst other oil exporters moderated import spending over the last decade, Colombia has partied, with import demand exceeding EM-wide levels, resulting in consistent external deficits. The country remains seriously imbalanced, with no sign of the necessary macro adjustments that would rein in external deficits and reduce dependence on foreign borrowing (which has surged). With Colombia heading for potential debt stress and default, expect further depreciation of the peso and a widening of sovereign spreads. Stay away from the equity market on FX concerns.

Teneo

Ghana: Budget approval doesn’t clear all IMF deal and debt hurdles

The recent parliamentary approval of the draft 2023 budget brings the government one step closer to securing a deal with the IMF for a bailout. However, contrary to some suggestions, the budget proposal does not contain details of debt restructuring plans and does not provide a green light for the government to enact any such decisions. These details can still be legally challenged and/or fiercely debated in parliament, although the risk is somewhat mitigated by the finance ministry’s decision to get ahead of the pushback.

Smart Insider

Asia Insider Trading highlights

Smart Insider tracks insider trading activity in 13 countries in Asia, including China, India, Indonesia and Pakistan. As revealed in their latest Asia report, insider trading volume increased in the region by more than a quarter in November vs October, with China and India representing 70% of the Sells. Overall, insider sentiment deteriorated from bullish to neutral with the highest Sell/Buy Ratio seen this year (1.54); the buying volume fell to its second lowest level in 2022 and the selling volume jumped 91%. In China, insider sentiment has turned bearish for the first time this year, with the highest ratio since December 2021 (S/B ratio 5.25).

Commodities

Global Macro Investor

FTX isn’t a crypto story, but a sham story

Raoul Pal has played in the crypto markets since 2013 and has seen these stories time and time again. First was the Mt Gox collapse, then came the fall of Bitfinex, and now it’s the CeFi/FTX collapse - the people screaming “scam” and “ponzi” are back out again. The real value of crypto is driven by its network adoption, which is the fastest of any technology in human history. We’ve seen the liquidity cycle and fear push prices down to the secular trend, but we’re about to see it turn (see chart), not to mention the new upcycles in new users that will drive network values to new highs. BUY ETH below 1100 or buy the breakout above 1550. Keep an eye on Solana; it may have fallen 95%, but ETH also once did before it went on to produce a 66x return…

Metals Focus

Hydrogen economy: A report

With hydrogen becoming a key component in the quest for global decarbonisation and a focal point of the automotive industry, Metals Focus’ latest report assesses the trends, policies and technology that is driving this market and their implications for platinum and palladium metals demand. The annual report includes a focus on green hydrogen production and PGM based technologies, hydrogen applications, opportunities for adoption and associated risks, key commercial players, and policy developments. Please contact us to find out more.

J Ganes Consulting

Softs complex: Bearish outlook but rallies present selling opportunities

Whilst sugar’s fundamentals remain bearish, Judith Ganes notes that there has been a recent counter-trend rally based on delivery worries. However, the rainy weather should only delay but not limit crop production. In the cotton market, Judith questions the USDA’s seemingly unfounded belief that Chinese domestic mill demand will increase this season. Touching on cocoa and FCOJ, Judith remarks that we are heading into a period where both commodities could become more weather sensitive but, absent any issues, prices could retreat. Judith remains bearishly biased the softs complex as the year winds down.

ERA Research

Expect a sharp fall in demand for lumber & OSB in 2023

Demand for both lumber and OSB is expected to decline precipitously next year on weaker homebuilding activity. For lumber, overdue capacity closures in British Columbia (BC) should help offset supply growth from the US South, but BC producers can’t solely remove enough supply to match the expected collapse in demand. ERA Forest Products forecast lumber prices cycling either side of BC cash-cost levels, with S-P-F 2x4s averaging $450 on the year, and SYP 2x4s averaging $440. Risks are to the downside. In OSB, declining supply due to a combination of mill conversions, fire-related downtime and a pullback in offshore imports should keep some tension in the market through H1/2023.