Company & Sector Research

Europe

New Street Research

1&1 and United Internet both had a poor 2022 as concerns and lack of visibility on the network build continue to grow. New Street believes the situation is misunderstood - as either 1&1 goes ahead with the network build which should generate long-term EBITDA growth and mirror what Iliad has been doing in Italy (their base case), or it walks away and reverts to being an MVNO which would also generate substantial upside. An IONOS IPO could also be a further support for United Internet. An expected CMD in March could finally be a catalyst to bring this to a head. If the market continues to disbelieve after that, the case for a minority buy-in becomes even more compelling. TP €31 (150% upside).

ResearchGreece

ResearchGreece is concerned with Nova-Wind's more-aggressive-than-expected commercial policy announced on Jan 11th and the potential ARPU / EBITDA impact on OTE. The dividend & share buyback for 2023 is not necessarily at risk thanks to OTE's dividend-intended cash buffers. But 2023-2024 EBITDA could be, as they doubt OTE will let subscribers go. In the end, Nova’s zero margin / cash burning strategy could backfire, but the market damage will be done. Heightened competition could turn out to be strike No.3 for OTE, after higher interest rates and lower-than-expected remuneration in 2022.

Holland Advisors

Surprised? You shouldn’t be - following RYA's strong than expected third quarter, analysts are now running around tweaking sector spreadsheets, updating forecasts and their recommendations in a frenzy. But as Andrew Hollingworth observed last year, less discounting but still super low unit costs = much higher profits. He believes market leadership in scale and unit cost has been secured. Now demand resurgence will play out towards the endgame Andrew has previously outlined. What gives in all this is pricing. Some investors will catch on quickly to this change, many will assume short-term pricing gains will be given back. They will be wrong. Stay long and enjoy the ride!

Green Street Advisors

2023 Pan-European Office outlook

The sector is at a crossroads like no other time before, whereby solid demand for grade ‘A’ space is transpiring at the same time as fundamentals for 'B' quality offices are quickly deteriorating. This bifurcation in quality is likely to be further exacerbated by "green" building requirements, boosting already-burdensome capex needs for average-quality stock to remain relevant. Average-quality (B/B+) office fundamentals are unlikely to trough this year, and the recovery from '25 will be gradual. 2027 M-RevPAM is projected to still be ~7% below pre-Covid levels. Despite meaningful share price corrections during the past six months office continues to look expensive.

TT Equity Research

Heading for a brick wall - as occurs all too often with this cyber security firm, the latest trading update is of limited value as it includes too many numbers that cannot be verified. However, the key message, pressure on customer growth, is very important since customer growth has financed the business model so far. At the FY22 results, Teun Teeuwisse already noted the mismatch between sales commissions and reported ARR, client and revenue growth. As DARK’s shares slump below its IPO price, he is happy to remain short.

North America

ROCGA Research

Using Cash Flow Returns On Investments based valuation tools, Meta Platforms is looking significantly undervalued. ROCGA’s portal has been built using the Cash Flow Returns On Investments methodology. It allows you to identify, research and value listed companies. They have 15 years of clean fundamental data and you can model and assess companies in seconds. Current coverage: 1,010 North American, 515 UK and 440 European companies. Other companies identified include eBay, United Parcel Service and Adobe. More details on ROCGA’s systematic and interactive valuation tools can be found here. A free trial is available on request.

Huber Research Partners

Douglas Arthur doesn’t see any crisis occurring at the company as he initiates coverage with a Buy rating in this 70-page report - four aspects stand out: 1) the size and growth prospects of the DTC streaming business; 2) the magnitude and geographic reach of the Parks footprint; 3) the depth, richness and velocity of the company’s content production machine; 4) and, potential earnings power if and when the large streaming business starts to make money. Douglas forecasts adjusted EPS to increase from $3.53 earned in FY22 to $6.90 in FY26, an 18.2% compounded rate of growth.

JJK Research Associates

Innovation levels within the early spring performance apparel assortments looks very strong according to Janet Kloppenburg. She is also impressed with the increased newness in the On the Move assortment and thinks the recent hiring of Elizabeth Binder as chief merchandising officer will support ongoing gains. Janet continues to believe 4Q22 revenue will come in ahead of expectations, leading to an EPS beat ($4.33/$10 for 4Q/F22). Looking into 1H23, she expects top line gains to exceed consensus forecasts (+HTeens), however, 1H23 EPS may track below current buy-side estimates. For FY23, Janet models +17% y/y revenue and $11.80 EPS (vs. $11.40 consensus).

Valens Research

Considering the fixed costs of food and facilities management, many schools, stadiums, and more are re-thinking their decision to operate this business in-house vs. outsourcing. Meanwhile, for the 50% of the market that is already outsourced, the vast majority is owned by “mom-and-pop” providers. Many struggled to navigate the pandemic and there is an opportunity for larger players, like ARMK, to take significant share. The market isn’t recognising how ARMK’s large footprint has enabled it to improve offerings, including customised food and superior payment solutions. This helps it win premium contracts, leading to higher revenues and margins.

Cmind

4Q22 Earnings: A quantitative and predictive outlook

Cmind is rolling out 4Q22 earnings beats / misses predictions at both the sector level and company level. In the Energy sector, they have made predictions for 182 US public companies. Breaking down to cap level, there are 34 large-cap (28 predicted to beat vs. 6 predicted to miss), 37 mid-cap (20 beats vs. 17 misses) and 111 small-cap ( 52 beats vs. 59 misses) companies. Overall, the energy sector is predicted to outperform most other sectors. Stocks expected to beat: Schlumberger, Diamondback Energy, Halliburton and Plains All American Pipeline. Stocks likely to miss: Cheniere Energy, Williams Companies, Enbridge and Imperial Oil.

Veritas Investment Research

Canadian Oil Sands: Crack spread comedown

North American refiners had a banner year as demand for refined petroleum products surged and crack spreads hovered at record highs for most of 2022. However, we are starting to see signs of weakening demand and US crack spreads are already coming off their highs. In light of recent macro data points, Dan Fong lowers his crack spread assumption (to US$20/bbl from US$29/bbl) and updates his recommendations and valuations for Canadian Natural Resources (rated Buy), Suncor (Buy), Cenovus (Sell) and Imperial Oil (Reduce).

Portales Partners

Bank stocks continue to roar in January, defying “the recession”

Charles Peabody recommends fading capital markets names as the outlook is based on hope but continues to be bullish banks (as he has done since the summer lows) as NII forecasts are restrained by fear. The most predicted recession in history is being pushed out and bank prices are responding to the powerful revenues and stable asset quality on display, buttressed by the resumption of stock buybacks. Charles continues to favour Wells Fargo, JPMorgan, PNC and Truist Financial Corp.

Behind the Numbers

Restatements don’t erase its problems - in early 2022 BTN warned clients that XRAY’s 2021 EPS had benefitted from unusual one-time items including some sleight of hand with R&D expense. Soon thereafter, key management departed after announcing results would fall well short of its previous forecasts. To make matters worse, the company later announced that it had detected problems with its accounting and it would be unable to file audited financial statements for 1Q22. While the accounting problems may appear to be behind the company, BTN sees several barriers to XRAY’s return to consistent, meaningful growth.

Blueshift Research

Following interviews with several industry specialists, Blueshift finds ESTA will not reach anywhere near majority market share in the US with its Motiva breast implants and faces scepticism about its minimally invasive augmentation technique. Multiple sources cited Sientra as a cautionary tale: it launched in the US with a strategy similar to ESTA (premium pricing based on claims of improved safety) but has largely given up on its pricing goals and has peaked at about 15% market share. Sources forecast Motiva’s US market share at a similar level.

Singular Research

This small-cap biodefense specialist has recently won a $380m procurement contract to supply RSDL (Reactive Skin Decontamination Lotion Kit) to the US DoD - while near-term challenges remain, including lower branded NARCAN sales in the US commercial retail market (as a result of the generic launch in late 2021) and continued weakness in contract manufacturing (CDMO) revenues, EBS enjoys an impressive pipeline and is strengthening its business model through corporate development and opportunistic acquisitions. TP $26 (100% upside) uses a 50/50 blend of the price targets obtained from Singular's DCF model and a multiple-based (P/E and EV/EBITDA) valuation.

MYST Advisors

Accounting games create illusion of earnings growth - IBM is “misleading” investors into believing the company is growing EBIT at a considerable pace following the spin-off of its IT services business, Kyndryl Holdings. The perception of growth in the RemainCo has been the primary driver of the stock’s material outperformance. However, “real” EPS power is more like ~$8/share and applying IBM’s long-term average ~10x P/E multiple results in a TP of $80 (45% downside).

Inflection Point Research, LLC

IPR’s industry checks indicate a recent significant change in AAPL procurement - order cuts have been made across the board, including iPhones, Macs, iPads, Watches, and accessories. It is likely to take some time for supply and demand to normalise causing problems for suppliers in the near term. In a separate note, IPR also discusses the recent Bloomberg report re. AAPL's plans to replace Qualcomm and Broadcom iPhone chips with in-house solutions. IPR believes this is just the first round of a negotiation dance between Tim Cook and Hock Tan, that will ultimately lead to another LTSA.

Japan

LightStream Research

Currently trading close to the historical peak FY+2 EV/OP and FY+2 EV/EBITDA, Oshadhi Kumarasiri thinks Seven & i has little to no room for valuation multiple expansion. Earnings also seem to have peaked after reaching an all-time high in the third quarter. In addition, Oshadhi sees substantial downside risks to 7-Eleven US earnings estimates in the short to medium term with falling gasoline prices (3Q OP beat was mostly driven by an unexpected upside to the retail fuel margin, but this will correct over the next few quarters) and the yen appreciation. 40% downside.

Emerging Markets

Westlake International

From Westlake's primary research, they observed 4Q online ad spending fared better than offline and grew modestly Q/Q despite Covid disruptions, while industry professionals are cautiously optimistic about their ’23 ad spending outlook. Baidu can meet 4Q online marketing revenue growth expectation given budget shift from branding ads to performance ads and offline ads to online. Tencent likely saw 4Q revenue growth in-line with consensus forecasts. Its game biz remained weak, but can meet street estimates and return to growth in ’23 propelled by new game approvals and international game launches. They also saw strong growth momentum from WeChat Channels ads.

Silk Road Research

China Industrials: The ground is shifting…rapidly

Industry sentiment shows clear signs of improvement as risk of worst case Covid scenarios has diminished - SRR finds the near-unanimous positive feedback for prospects this year to be in stark contrast to the mixed / negative views from one month ago. The Aerospace sector remains SRR’s top pick for sector exposure owing to its still-depressed base. A conservative base case for 2023, would translate to a ~350% increase in domestic flight departures from the recent trough in Dec ‘22 by Aug ’23. SRR also favours Autos and Elevators, but expects 4Q results will disappoint and recommends investors wait for a reset of expectations.

RedTech Advisors

Overcoming its growing pains - RedTech turns bullish as YMM, which dominates the online market for connecting independent truckers with shippers, has made substantial progress in addressing the problems highlighted in their August 2021 report, resulting in consistent and impressive growth during the past year, despite considerable headwinds from Covid lockdowns and a temporary government ban on registering new users. YMM is one of the few names that RedTech covers where there are still outsized opportunities even after the recent sharp rise in China share prices.

AceCamp International

Fundamentals set to recover from 2Q23 - AceCamp expects non-recurring net profit to reach RMB0.4bn/0.7bn/0.9bn in 2Q/3Q/4Q23; FY estimates are RMB15bn/31bn/44bn/56bn (2023-26). Recent channel checks further support their bullish view as the semiconductor company continues to benefit from 1) secular growth of automotive CIS, CIS for VR/MR/AR, and medical CIS and 2) its market share gain in automotive ICs and driver ICs. The stock has the potential to trade at 30x 2025 PE (RMB1,42bn) vs. M/cap of RMB1,10bn.

Horizon Insights

This advanced ceramics manufacturer is expanding into MLCC and ceramic package markets, both of which have significant growth potential. MLCC demand, which had been stifled by the depressing eclectic devices demand, has now reached its low point, and an upturn is ahead. The top six MLCC manufacturers in the world control 90% of the market. With premium products, domestic manufacturers are expected to gain a global presence. The stock is one of Horizon Insights’ top picks for 2023.

Macro Research

Developed Markets

AAS Economics

The UK economy through a monetary lens

Frank Shostak comments that some of the trends that are characteristic of the global economy, including declining output growth and inflation, are also apparent in the UK setting. The PMI outlook is for a possible short term economic bounce, but a longer-term perspective, looking at import growth and employment growth, shows a contractionary environment. The annual RPI inflation rate should decline and weakness in housing activity is likely. Bond yields are, in Frank’s view, likely to decline and the yield curve should flatten. He expects reductions in policy rates before year-end. Frank’s business cycle asset allocation framework indicates Stage 1 of the cycle, which is the most defensive, and thus his template allocation favours very defensive settings.

Minack Advisors

There is good news driving markets, but will it last?

The bullish start to 2023 is based on good news: inflation is rolling over, China is backflipping on market-unfriendly policies, and warm weather is easing Europe’s energy crunch. Gerard Minack doesn’t expect this rally to survive a US recession, which remains his base case. But perhaps the nasty-first-half-buy-in-the-second-half consensus view will need to be tweaked to start-with-a-bang-sell-in-May view. The everything bubble is trying to reflate in 2023. Everything that fell last year is up, and the only thing that’s down (of course) is last year’s big winner: commodities (see graph). That performance in 2023 is a mirror image of 2022 suggests that positioning is a factor in the market moves.

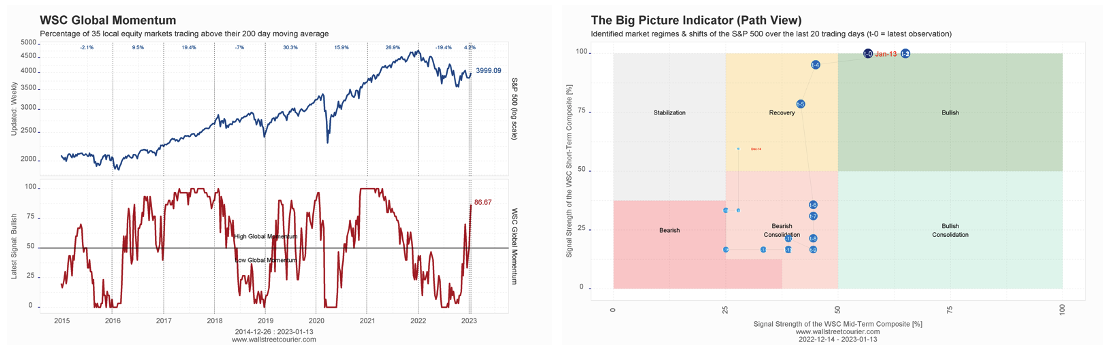

WallStreetCourier

An improving market outlook

The condition of the market improved last week, in line with WallStreetCourier.com’s strategic call. The fresh rally is not at risk of fading out soon. Thus, any upcoming weaknesses should be limited in price and time (and could be used to add exposure). It could be possible that the market is about to enter bullish territory. Even globally, the rally is broadening out strongly, as 87% of 35 local market indices are now trading above their 200-day MA (see graph 1). WallStreetCourier.com’s Big Picture Indicator tool, which provides a comprehensive macro view of global risky assets, is now signalling a bullish market regime for the S&P 500 (graph 2), after it already signalled a stronger recovery in asset prices at the beginning of the year, while being negative in 2022.

PPG Macro

Markets have got ahead of themselves

...claims Patrick Perret-Green. Risk assets rally on the idea of a benign, soft landing and a Fed tailwind. Unfortunately, markets are ignoring the reality that if a soft landing materialises, central banks will be much slower easing. Rates were overdone last week and there was another warning sign over the weekend with the FT reporting that bond markets had had their best start to the year in ages while completely ignoring that was because of the thin year-end sell-off and that yields were still higher than they were in the first half of December. Stay paid. 2y1y OIS was around 2.70% at publication. Now 2.82%. Patrick is sticking with this chart. 2y1y IRS vs 6th fed funds since 1995. Time for the carry bleed.

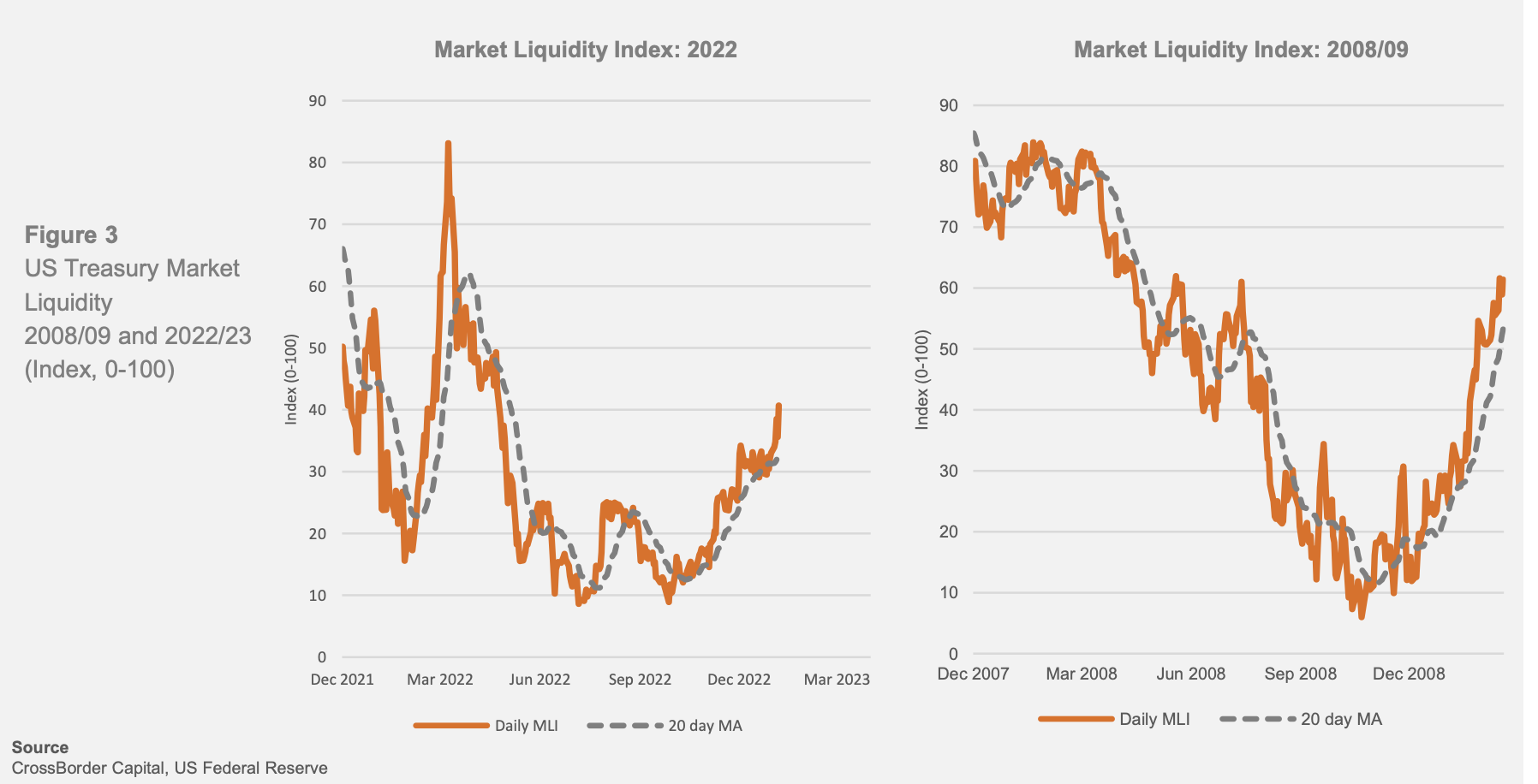

CrossBorder Capital

Is US QT already dead?

The Fed is saying one thing (headline QT) and doing another (adding liquidity). The reality is, according to Michael Howell, is that QE is easier to engage than disengage. The threshold for minimum US banks’ reserves is likely at least US$2.5 trillion and, at the latest QT pace, we could get very close to this danger point in a few months. Michael confidently expects liquidity to be higher by year-end. Watch bond market volatility for evidence of tensions, and the US dollar and the yield curve slope for signs liquidity is coming back.

Inferential Focus

US society gradually shifting from extremes to moderation

With extreme behaviour seemingly affecting nearly every walk of life, from politics to social media and from meme stock investments to cryptocurrencies, it might be a strange time to suggest that extremes are losing their appeal. In gathering observations of Americans settling down after an era of excess, Inferential Focus has pieced together four kinds of shifts from extremes: From Intensity to Practicality; From Extremes to Moderation; From Speculation to Stability; and From Rationalising to Discipline. Together with the extremes that comprise what they have called Uncharted Territory, American society is slowly turning away from its recent burst toward extreme practices to Settling Down to focus on the details of reality.

Aitken Advisors

Japan: Following the yen

Upon finding out about the BoJ's decision this week, James Aitken wondered: ‘if everybody is long yen & short dollars, how come we have roundtripped back to 129?’. If on a day like that the dollar cannot hold a bid versus anything for more than an hour, then it is probably heading a lot lower, versus everything. It is not news that Japanese institutions have recently been enormous net sellers of US duration, but what if they haven’t converted the proceeds back into yen and are still sitting on large dollar cash balances? Last February and August we saw Japanese institutions unwind large FX risk, impacting global currency markets. Might the opposite happen this year, that next month sees Japanese institutions rebalance back into yen, en masse?

Greenmantle

Japan: Holding steady

The BoJ held policy steady despite market pressure to relax YCC. Niall Ferguson sees the unanimous decision as indicating that the Japanese government and monetary authorities are confident that the country is fundamentally different from the US and Eurozone. They are prepared to overshoot the 2% inflation target substantially. Consistent with BoJ history, it also suggests that Kuroda’s replacement is unlikely to signal a hawkish pivot immediately following his appointment. Niall’s base case is that the BoJ unwinds YCC in a gradual fashion in 2023 but keeps its foot on the pedal with asset purchases and ultra-low rates, in contrast with the rest of the world. Of course, this runs a substantial risk of un-anchoring inflation expectations later in the year. For now, Niall is SHORT yen and OVERweight Japanese equities.

Emerging Markets

PRC Macro

China: Potential policy and macro upside

Earnings expectations in the US and China have both been falling, but with China seeing larger potential policy and macro upside this opens the door for relative equity outperformance. In China, upstream activity levels remain elevated heading into the holiday break, with the appearance of a strong rebound to traffic congestion/flows. This indicates that the first wave of Omicron cases has crested and the overall macro impact is smaller than originally expected. William Hess remains cautious towards the overall rebound to household demand and continues to see the potential for market disappointment once full-year fiscal and credit targets are announced. Where it comes to output, William still sees incentives that skew towards overproduction.

Alberdi Partners

Argentina: Challenging roll over scenario for ARS debt

The October presidential elections act as a cliff beyond which investors are scared to take ARS denominated government debt. Marcos Buscaglia believes that, as the elections approach, this fear is likely to become more acute. He thus provides two scenarios of debt roll over until the end of 2023, and estimates the BCRA support needed to avoid a default. In the first scenario, roll over rates remain at about the same levels as in previous months, and the central bank’s support in this case should be about ARS2tn in 2023 (on top of financing the primary deficit). In the second scenario, roll over rates drop as the elections approach, leading the total BCRA support above ARS3tn (2% of GDP).

Totem Macro

South Africa: A cheap currency

As the South African government fails to meet even the extremely low bar of keeping the lights on, assets have underperformed and cheapened materially, including the currency. Growth will be weak, inflation is already contained and likely to fall further, and yields already bake in a huge real yield premium. Whitney Baker comments that the currency is as cheap as it ever gets (outside of the balance sheet distress across EM in the early 2000s), without the normal high inflation differentials that usually erode that valuation without nominal appreciation. Contained imbalances, falling inflation, weak growth, and strong external commodity support all argue for a long currency position expressed with moderate duration for yield pick-up purposes. Whitney adds a new LONG position in rand, via 2yr bonds (FX unhedged).

Emerging Advisors Group

Turkey: On to the next lira collapse

As of last month, lira money growth has crossed the line into triple digits, now running above 100% y/y. Things are officially out of control, remarks Jonathan Anderson. At the same time, the lira has now been stable for more than six months, leading to astounding USD returns and making investors who hold the market look like geniuses. How long can this last? Not long. Money growth is skyrocketing, external deficits are huge and real interest rates are hopelessly negative; no matter what administrative tricks the government may pull in the near term, the lira still faces yet another looming collapse. Bottom line: If you made profits in the market, take them now and leave.

Commodities

Global Mining Research

Gold sector: 2023 looking positive (so far)

Gold prices will always be volatile but two of the unexpected headwinds of 2022, inflation and USD strength, have now peaked. David Radclyffe reviews the outlook for the sector in 2023. He expects gold equity inflows as price and margin pressures of 2022 abate and the potential for surpluses return. M&A is expected to continue, and significant C-suite turnover offers opportunities to reset stale strategies. Preferred stocks are Barrick, Endeavour and B2Gold for scale/value, Northern Star and Evolution for leverage to better gold/copper prices and Lundin Gold and Centerra for attractive potential in smaller caps.

Aitken Advisors

A core portfolio holding

James Aitken continues to believe that oil and gas should be a core portfolio holding. He remains LONG Hess and BP, and recommends that investors remain long, too. The recent (past three months) inelasticity of major oil and gas stocks to declining oil prices may be a hint that new (fed up with ESG) buyers are coming into these well-run, cash-flow vomiting businesses.

CPM Group

Who owns hundreds of millions of ounces of silver?

In his latest video, CPM Group’s Jeff Christian discusses the enormous amount of unreported silver inventory owned by banks and lent to industrial processors and users, and what that metal means to the market.

Click here to watch.