Company & Sector Research

Europe

Woozle Research

Downgrades to Short / Sell based on findings from their recent surveys with store managers - Woozle’s H&M channel checks were much more negative than other names in their fashion coverage, many of whom outperformed targets over the Christmas period. Forecasts 1Q23 LFL sales growth of 0% y/y with 24% of respondents reporting that sales are falling below internal targets. This represents a meaningful deterioration in target meeting performances q/q as the latest product releases underwhelm customers. Furthermore, the number of customers trading down to cheaper ranges has increased considerably q/q as the cost-of-living crisis deepens.

ResearchGreece

Greek Banks: If not now, when?

What better time for the Greek state to dispose of its (sovereign crisis) leftover stakes in the country's banks? For totally risk adverse investors ResearchGreece recommends Piraeus Bank; sees ~50% upside based on RoTE/CoE estimated fair 2023 P/TBV of 0.55x. Investors worried about downside risk should go with NBG; sees 30% upside towards fair 2023 P/TBV of 0.80x. For all Greek banks, the current outlook points to RoTE >10% on higher NII offsetting additional MREL costs, controlled CoR (no recession), and the Mitsotakis administration renewing its mandate in the forthcoming elections.

Foveal Research

Contrary to market expectations, Dr Amit Roy believes NOVN is likely to win the $6bn+ early-stage breast cancer market, beating Lilly - Kisqali carries the lowest discontinuation rate, differing from Verzenio in lacking its compliance limiting troublesome diarrhoea side effect. NOVN is uniquely utilising a dose lower than its metastatic trials to further improve compliance, while additionally administering the drug for three years instead of two as seen with its competitors. Unrivalled metastatic overall survival efficacy compared to Verzenio leads Foveal to see Kisqali both meeting its endpoint in NATALEE, and likely demonstrating better efficacy than seen so far with Verzenio in MONARCH-E.

TT Equity Research

Quickly returning to its pre-Covid distress - according to Teun Teeuwisse, the key reason to be short pre-Covid was because ERF was an acquisition machine, whose acquisitions never actually added any value; the company failed to seriously generate cash and had a mounting debt position of >50x FCF. Additionally, Teun had doubts on transactions between the firm and its major shareholder’s, the family company of founder and CEO Gilles Martin. Now that Covid benefits are fading rapidly and with debt maturities getting closer Teun thinks this is a great time to re-short the stock.

the IDEA!

Delivery slip - now seeing clear evidence of the insourcing and rerouting by bol.com and at a faster pace than the team at the IDEA! had originally anticipated when they published their bearish report last Oct. On top of that, DHL has stepped up competition. In Belgium, PNL has lost part of its volume to bpost and is facing higher costs for the use of its subcontractors. The pressure on margins is particularly worrying. Reduced pricing power means that tariff increases are insufficient to offset the impact of the 2022 cost inflation, let alone that of 2023.

North America

Quo Vadis Capital

Restaurants: Negative surprise coming?

John Zolidis has published a bearish framework on the Restaurant industry and believes the Street is misunderstanding implications of commodity price declines which will disadvantage the industry vs. food-at-home as grocery stores pass on lower prices. Meanwhile, he sees no argument for a stronger consumer or better traffic this year. John predicts negative same-store sales in 2H23 (which is not reflected in analyst expectations). He is most bearish on value destroyer Shake Shack, investor favourite Chipotle, and overvalued growth name Dutch Bros.

Antya Investments

A contemporary gordian knot - after a complete failure at anticipating and forecasting demand trends and overseeing a decline of 71% in the stock price during FY22, management now predicts $1bn in combined FCF during FY23 & FY24. FCF has swiftly become important with Debt/EBITDA increasing from 2.96x (Sep 2019) to 6.03x (Sep 22) and set to deteriorate further in 1H23. Neeraj Monga does not buy into the turnaround story and believes the current rally in SMG’s stock price is the perfect time to bail out. Trading at a premium to its long-term pre-Covid mean valuation, Neeraj argues that after considering all plausible optimistic outcomes, the stock is at best worth $44/share.

Verbatim Advisory Group

Popular seasonal products and low-price points (down trading) drive strong Jan comps. According to Verbatim's latest channel survey, Jan SSS trends are stronger than Dec. Similarly, 4Q22 (Nov-Jan) trends are ahead of 3Q22. The current y/y comparison is more difficult than Q3 on a one-year basis and slightly easier on a two-year basis. In Q3, Verbatim required a bias of positive 240 bps. Based on stronger trends, and tougher y/y comparison, they are incorporating a bias of positive 200 bps in Jan. With a Jan Raw Comp of 10%, their Jan Comp Estimate is +12%. Their 4Q22 Comp Estimate is +10.2%. Click here to access the full report.

BWS Financial

A sea of profits - with expectation of no new ship builds to saturate anytime soon the current day rates should hold over the next 2-3 years. SDRL emerged from bankruptcy protection in early 2022 and listed its shares in Oct. Since then, it has undertaken asset sales to increase its cash balance, which has resulted in the group having more cash than debt - a rare trait for the industry. However, despite the lean balance sheet, the stock continues to trade at a discount to peers. Furthermore, the pending purchase of Aquadrill will substantially increase SDRL's liquidity and earnings power. TP $59 (40% upside).

Veritas Investment Research

Canadian Banks: Pivot or divot?

Nigel D’Souza believes Canadian banks could face an inflection point later this year when consensus expectations for rate cuts are pushed out to 2024 as the BoC signals a higher-for-longer pause. He forecasts a double-digit decline in adjusted earnings for the sector over the medium term, mainly due to lower risk-adjusted margins. On valuation, Bank of Nova Scotia offers the most attractive risk-reward skew among the Big Six banks. Nigel sees the greatest downside risk for Bank of Montreal and CIBC in a moderate recession on higher credit losses for the former and weaker NII growth for the latter.

Insight Investment Research

Reliable demand, strong unregulated pricing, high capital barriers and excellent returns - Robert Crimes initiates coverage with a Buy rating and TP of C$360 (100%+ upside). Insight’s key value added vs. The Street is application of their Global Infrastructure specific valuation framework focused on DCF and IRR, their assessment of long-term volumes, pricing and FCFs and their ability to rate CNR vs. the other Global Infrastructure stocks in their universe, rather than other North American transportation stocks. CNR enters at 4th of 24 on the Insight Stock Ranking System, after Ferrovial, Cellnex and Getlink.

Global Mining Research

David Radclyffe evaluates the impact of developing Reko Diq and benchmarks the project against 37 of the larger open pit copper mines covered by GMR - he estimates a 15% IRR which is attractive given a 2028 start and assuming a 20% capex hike and US$19/t operating costs. The 2023-28 average FCF yield reduces from 6.9% to 5.7% with Reko Diq but increases from of 3.3% to 4.1% during 2035-40. Sovereign risk may explain GOLD’s continuing discount to peers, but the copper project could have a material impact on the miner's production profile (+190kt CuEq from 2035E) and it appears attractive as GOLD's preferred mid-term growth option.

Gradient Analytics

Gradient's 17-page initiation report highlights a variety of fundamental concerns and earnings quality issues: 1) Increasing reliance on pricing to drive revenue growth and looming Performance Chemicals weakness. 2) Surging receivables suggest declining revenue quality. 3) Inventory levels have diverged from near-term demand estimates and appear at odds with expectations of gross margin expansion. 4) Facing margin headwinds from its accrued liability and prepaid expense accounts. 5) Analysts may be underestimating FY23 depreciation. 6) Trades at a massive premium to peers across a wide array of both trailing and forward-looking valuation metrics.

Radio Free Mobile

Code red - INTC reported a truly awful set of numbers, declined to guide for 2023 and appears to be losing market share left, right and centre. Richard Windsor thinks there is a good chance that INTC will need more capital. He argues management should cut the dividend and sell its stake Mobileye (he believes INTC has 24 months to dispose of its stake before the share price collapses). INTC could post negative EPS this year meaning that there is very little to support the share price from a valuation perspective now.

Battle Road Research

In the past few weeks, PSTG released a new environmentally friendly solution and achieved $1bn+ in ARR from subscriptions to the company’s products for the first time in its history. In addition, the company maintains its leadership and first-mover advantage in the all-flash data storage market, possesses a vast and expanding set of large and diverse customers, and generates robust gross margins vs. peers. Boasting a strong balance sheet, potential for substantial top-line growth and a 30-35% earnings improvement over the next couple of years, Battle Road remains bullish with a TP of $40 (40% upside).

Blueshift Research

According to industry experts interviewed by Blueshift, ARW faces an extremely challenging 2023, as multiple negative trends are building including an increasingly difficult relationship with one of its biggest suppliers, Texas Instruments - ARW is being relegated to smaller (and more economically sensitive) customers with low volume needs for commodity products as TXN continues to ramp up its direct sales operation to cater to bigger customers with custom requirements. To make matters worse, in the low-end market, sources reported that ARW is losing ground with some customers to catalog distributors such as Digi-Key Electronics and Mouser Electronics.

Paragon Intel

Having conducted 34 interviews on CEO Tobi Lutke and his management team (Paragon’s sources worked with these executives for 162 years combined), evidence suggests he lacks the operational acumen to oversee SHOP’s continued growth. Worrying traits include a disdain for expertise, lack of short- and medium-term vision, dearth of processes and professionalism, poor people management, and potential risk management issues around HR and data security issues. Management practices that worked when SHOP was a small start-up will not enable the company to scale.

Australia

Periscope Analytics

S&P/ASX Index Rebalance: High impact changes in March

Brian Freitas forecasts 1 change for the ASX20 Index (South32 replaces James Hardie Industries), 2 for the ASX100 Index (nib holdings and Technology One replace Star Entertainment and ARB Corp), 4 changes for the ASX200 Index (including Syrah Resources and PolyNovo gaining entry at the expense of Adbri and SmartGroup) and 9 adds / 6 deletes for the ASX300 Index next month. Passive trackers will need to trade over 3 days of ADV on 13 stocks, over 5 days of ADV on 9 stocks and over 10x ADV on 4 stocks. Shorts have been covering positions on stocks where there are expected to be passive inflows and increasing positions on stocks that are expected to have passive outflows.

Emerging Markets

AlphaBox Advisors

This bank's recent underperformance creates an attractive entry point for long-term investors looking to own a high-quality franchise with a best-in-class management team and fantastic capital allocation track record. HDFC has an impeccable underwriting history with the lowest NPAs across major credit cycles in the last 28 years. This is despite growing its loan book by over 2x the industry average. With a long runway for growth ahead, and the stock trading at a 20% discount to its own 5-year average multiples, investors can expect 16%-18% compounded returns from here over the next 5 years. Click here for AlphaBox's 60-page initiation report.

Galliano's Financials Research

Post 4Q22 results, Victor Galliano screens 6 large / mid-cap Thai banks to identify those that are attractive value, have good earnings growth prospects and have the potential to deliver sustainably higher returns going forward. KTB is Victor’s preferred pick; it ranks top in terms of post-provision profitability, as well as screening well on NPL coverage and valuations, including its low PEG ratio. He also likes Bank of Ayudhya, with its strong pre and post-provision profitability in 4Q22, and strong credit quality metrics. In the wake of its poor results (due to its very high cost of risk), Kasikornbank should continue to be avoided.

AceCamp International

The Street continues to underestimate the negative impact of IGBT capacity oversupply and BYD's vertical integration - StarPower faces a deteriorating competitive landscape and ASP / margin contraction. AceCamp expects Industrial IGBT gross margin to fall from ~40% in 2022 to less than 20% in 2025, while Automotive IGBT gross margins will drop from 50% to under 30% over the same period. Their net income forecast is 20-30% below consensus of Rmb1.3-1.5bn in 2023, and AceCamp thinks the stock could fall to 30-40x 2023/24 PE which implies c.40% downside over the next 18 months.

Aequitas Research

Sumeet Singh runs the rule over this state-owned power producer as it looks to raise US$650m in its upcoming Indonesian IPO - PGE currently manages 13 Geothermal Working Areas with a total capacity of 1,877 MW. From an investment perspective, PGE will tick the renewable energy box and probably fall into a lot of ESG investment lists, which will aid demand for the deal. However, Sumeet notes that the company has regularly missed targets in the past, which blunts the attractiveness of its lofty future ambitions (aims to nearly double organic production capacity over the next five years).

Macro Research

Developed Markets

Harlyn Research

The case for Europe

Three of the largest sectors in the European equities index – financials, industrials and consumer - are ranked in the top three in Simon Goodfellow’s models - unlike the situation in the US, where technology is in the bottom three. All three have forces driving their outperformance which should last most of this year. The region, its currencies and its equity markets were priced in October for a catastrophe which simply hasn’t happened, and which is now very unlikely. There may be some short-term profit-taking, but the excessive valuation discount and the currency misalignment will take longer than a few weeks to unwind.

Steno Research

When will QT end?

The Waller Rule states that quantitative tightening (QT) will either slow down or end if USD reserves are equal to 10-11% of GDP. Andreas Steno believes that the current amount of reserves in the system is higher than this threshold and predicts a withdrawal of $500-600bn before QT will end or slow. Temporary USD liquidity will be added to the markets through February and March, with a positive impact on risk assets but a negative impact on the USD. Expect the S&P 500 to bottom around 3250 in the second half of the year. Andreas’ recommendations include investing in equities (via defensive US sectors and countries linked to China), 2s10s flatteners in the EUR curve, USDJPY shorts, AUDNZD longs, and EURSEK shorts.

Intertemporal Economics

US FOMC: No action

Signs are abound for a rapid cooling of inflation in H1/2023, remarks Brian Pellegrini, with the inventory cycle heading from a situation of panic-driven accumulation to one of panic-driven liquidation. The doves will sing their tune at upcoming meetings and trends in the upcoming data will give them enough of an argument to cease further rate hikes after another one or two moves of 25bps – the statements will all agree that no action is the best course of action. The fourth quarter was too hot, the first will be too cold, watch for the second quarter to be juuuuuuuust right.

Talking Heads Macro

A low r* is inconsistent with a soft landing

Markets are expecting disinflation, a soft landing and a return to a low inflation regime, accompanied by 200+bps of Federal Reserve rate cuts to achieve a nominal neutral of around 3%. However, Manoj Pradhan asks, if the Fed can achieve complete disinflation and a soft landing with policy rates near 5%, then why does the Fed need to cut rates at all? Either the equity market or rate cuts are mispriced. A hard landing will eventually materialise, but not immediately, and the Fed will be able to ease aggressively, causing the 1y1y rate to fall rapidly from its current 4% level to 2.5%. The market mistakenly believes that the rightward shift in the aggregate supply curve for the US is less benign than it is, and that the Fed will have to remain hawkish until the supports fade.

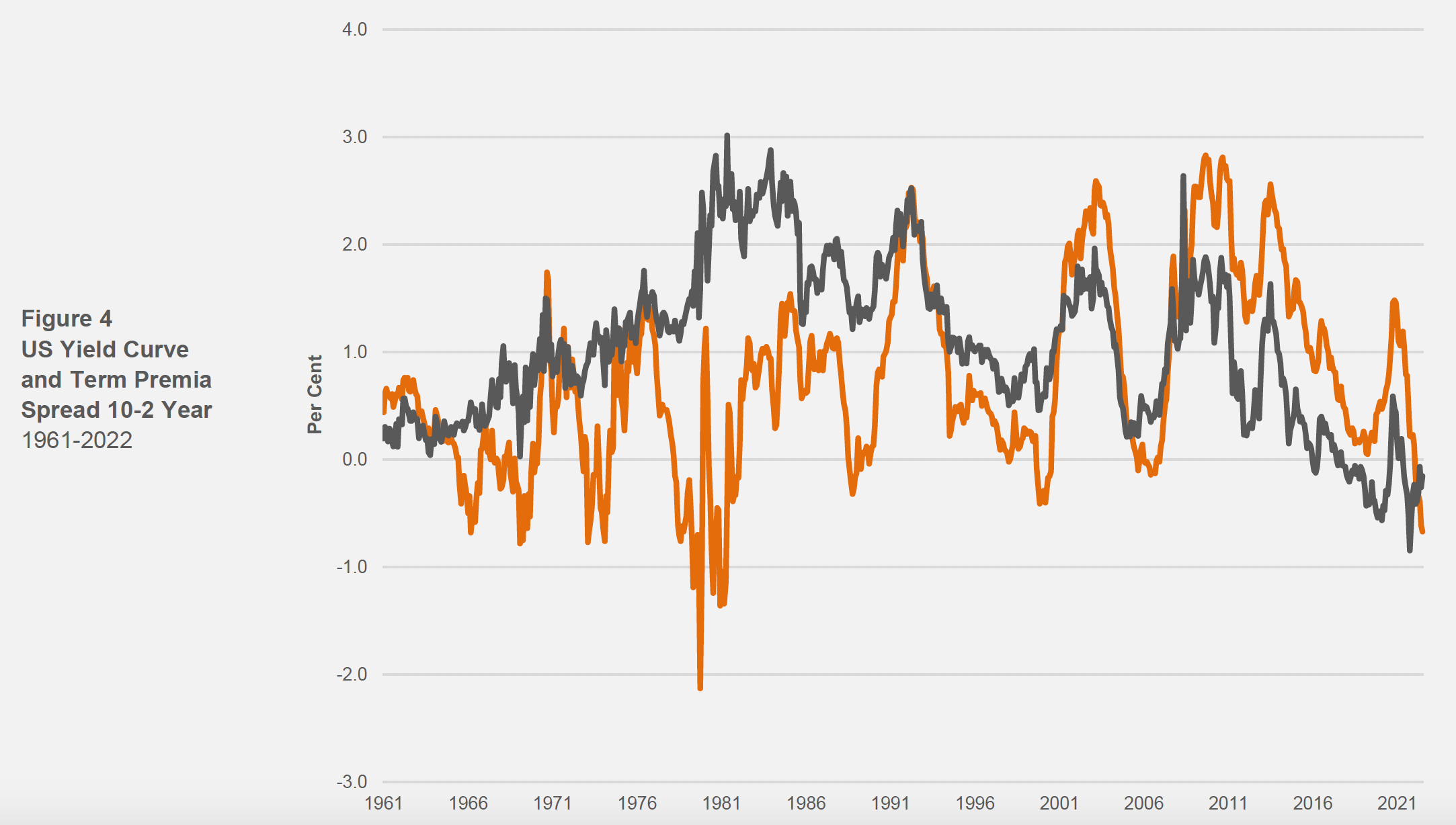

CrossBorder Capital

The US treasury yield curve is distorted

Many are worried that the large inversion in the US Treasury yield curve indicates a major recession ahead. However, Michael Howell comments that two factors are distorting the yield curve and weakening its signal: higher underlying inflation and negative term premia. The negative term premia is largely due to a structural shortage of collateral in the financial system, while the higher inflation trend implies a higher level of economic activity, not a lower one. The results suggest that removing the effects of negative term premia and faster underlying inflation gives the latest yield curve slope a far less negative reading, just sufficient to push it back into positive territory, thereby suggesting that the feared inversion and predicted subsequent deep US recession may be a phantom.

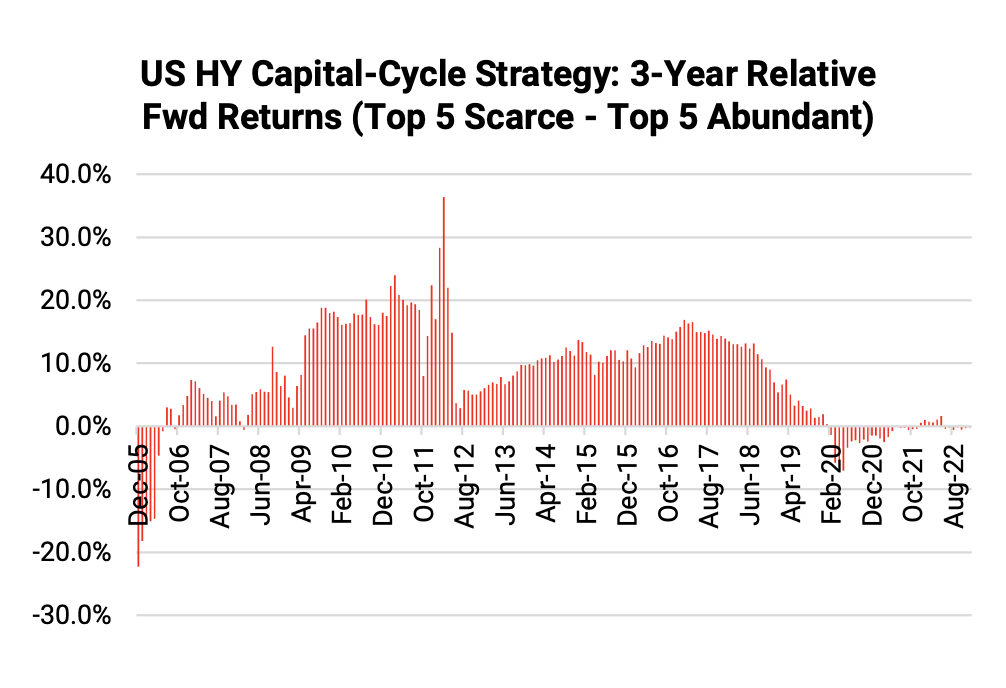

Variant Perception

Using the capital cycle to invest

Investing alongside the capital cycle would have shielded investors from 2022’s bear market. 2021’s everything-rally created excellent relative value opportunities, flagged by Variant Perception’s capital cycle framework; it is all about competition: too much investment in an industry destroys future shareholder returns. They are also powerful predictors of HY credit returns. Investors should use the capital cycle to 1) avoid credit events in industries with intense competition, and 2) aggressively buy capital-scarce companies as the business cycle turns up. The Variant Perception team also examine leveraged loans, which are at the centre of a major credit re-pricing.

Greenmantle

Canada: Resilient for now

Canada’s inflation remains at a near four-decade high, but households’ exposure to variable-rate mortgages has tied the hands of the Bank of Canada (BoC). In January, the BoC hiked the benchmark overnight rate by 25bps to 4.50%, as anticipated. Niall Ferguson now expects the BoC to pause for the rest of 1Q23 (75% probability). Combined with a tight labor market and a likely oil price rally, he reckons higher inflation expectations will persist in Canada, putting the BoC in an even worse position later in the year. Niall remains bearish Canadian real estate.

Emerging Markets

PRC Macro

China: Post-Party Congress, Post-ZCP, Now What?

William Hess continues to expect deregulation (big tech) and decentralisation (local fiscal) to be key investment themes for 2023. However, temporary policy reforms without structural political reforms will limit the systemic response. Despite the collapse of the ZCP, politics is not dead. The political leadership will decide the extent of easing in key areas (big tech and property). CCDI has downgraded anti-corruption efforts to focus on “integrating supervision with governance”, implying a focus on KPIs set in Beijing. For full-year 2023, William expects modest headline policy impulses, but in the short-term he expects fiscal and credit front-loading and overshooting…

Trivium China

China: Year of the RMB

The speed and size of the RMB’s decline against the USD in 2022 was unprecedented. The lesson of the past year is not that Beijing has become more willing to allow the market to guide the RMB’s value, but that the PBoC can no longer control its value, even if it wanted to. The bank’s waning influence is part of a deliberate trade-off to promote the country’s internationalisation, and it will become increasingly difficult for the PBoC to maintain the RMB’s “managed float” as the CNH market grows. It won’t be easy to make the transition, but the change will need to happen soon.

Alberdi Partners

Argentina: Central bank partially reverses two-day old measure

The central bank of Argentina has partially reversed its recent hike of the 1-day reverse repo rate for mutual funds, lowering the nominal rate to 61.2% from 68.4% just two days after the increase was announced. Marcos Buscaglia comments that the move was made to avoid the risk of a sudden drop in bank deposits and a potential decline in demand for 1-month fixed rate Treasury bonds by mutual funds. The bank’s initial hike was intended to tighten monetary policy and control the peso's movement in parallel FX markets. However, the original hike was too damaging for banks, but with the correction, the banks have regained competitiveness to keep the funds of money market mutual funds in their balance sheet.

Totem Macro

BoP crises and Egypt

Whitney Baker sees a juicy investment opportunity in Egypt due to its ongoing balance of payments (BoP) crisis. Indeed, Egypt's situation draws parallels to Argentina’s before the loss of power by Macri in 2019, where both countries relied on cheap dollar capital and leaned on the IMF for backstop dollar liquidity. Egypt has met the preconditions for a buy signal, including devaluation of the official FX rate, tightening of monetary policy, small dollar debt levels, and no political hurdles. BUY three-month Egyptian local currency T-bills, FX-unhedged, as a way to benefit from the stabilisation of FX. If the conditions for stabilisation and recovery that Whitney outlines are met, related investments can yield huge upside.

Emerging Advisors Group

Hungary: Getting dragged into the forint

Of course, the forint has done well, exclaims Jonathan Anderson. The big news now is the capitulation in Q4 macro activity. What kept Jonathan away was the idea that Hungary was still in an unsustainable boom, with money and credit growing at a rapid clip. Now, however, the picture is rapidly changing; there’s more contraction across key demand categories and credit momentum has fallen as well. Main question: how long can the MNB hold out? This makes Jonathan much more favourably inclined to HUF carry at the margin, as long as short rates are in the teens. He’s not scared of a gradual decline in the daily deposit rate per se, but he stresses that this doesn’t work if the MNB wants to take the base rate back down to neighbouring CEE levels.

Burumcekci Research & Consulting

Turkey: Strong loan growth

The trend of loan growth in Turkey continues to be strong, with the non-financial sector's loans and total deposits both increasing at a rate of 54.5% and 67.8%, respectively. The loan rate for most sectors decreased while deposit rates increased in the week ending January 20th. The Central Bank of Turkey's total OMO funding was at TL189bn and the average funding cost was 9.00%. Additionally, the supply and demand in the FX market are close to a balanced level, with the FX demand from foreign portfolio flows and rise in banks’ derivatives position remaining slightly below residents’ FX deposit decline.

ESG

View from the Peak

Two-tiered commodity pricing, a multi-billion dollar trading opportunity

We are entering an era of two-tiered pricing, according to Paul Krake. A price for a low-carbon good and a price for carbon-intensive equivalents. A two-tiered pricing system across every industrial input will create the most wide-ranging trading opportunities we have witnessed. Dozens of multi-billion dollar trading regimes ranging from corn to cement, steel to nickel. In the next five years, the commodity complex will see numerous new sustainable futures and options contracts designed to hedge and provide liquidity in the low-carbon version of most of the industrial products we use today. We are at the commencement of a new golden age for commodity trading that will dwarf the opportunity set delivered by China post-2004.

Queen Anne's Gate Capital

The sky is falling

Kathleen Kelley comments that the green revolution needs to be re-evaluated and that a greater emphasis needs to be placed on decarbonisation, rather than just electrification. Other technologies, such as hydrogen and geo-thermal, need to be part of the solution and that a full analysis of life-cycle emissions is critical to investment decisions. Investment in renewable energy and EVs reached $1 trillion in 2022, but other sectors such as storage, clean fuels and clean energy outside of wind and solar need to find governmental support to grow until they are economically viable. The current trajectory of EVs and electrification is unsustainable and environmentally unfriendly, and considerably more research and development is needed for a successful green revolution.

Commodities

Independent Strategy

Step on the gas

David Roche believes the coming year will see strong demand for oil as the world economy avoids recession and China recovers some of its shine, with the country’s oil demand likely to increase to 15-18mbd. On the supply side, underinvestment in fossil fuels and governments’ poor abilities to deliver on renewable alternatives will result in a decade-long supply shortage. Combined with the end of the shale bonanza and Russian sanctions, we will see oil price likely to get to USD $120/bbl by mid-2023 and average USD $140/bbl in 2024. This makes oil stocks very attractive in terms of valuation, cash flow and leverage.

HCWE & Co.

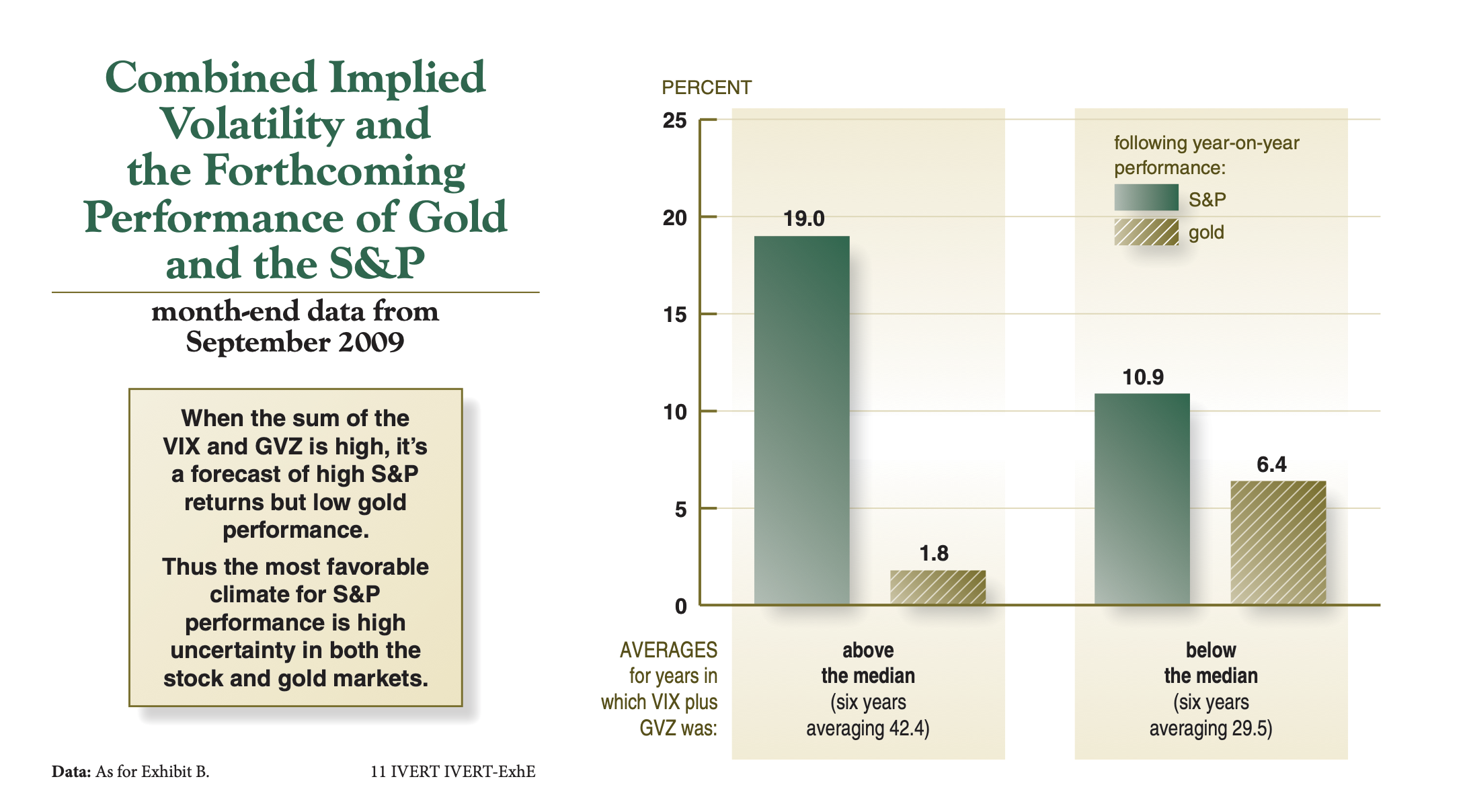

Implied volatility as a signal of performance

David Ranson’s latest report identifies relationships between implied volatility and subsequent performance between gold and stocks. He finds that fluctuating uncertainties play a significant role in explaining performance of stock and other assets such as T-bonds and gold. GVZ, a measure of implied volatility in the gold market, not only predicts gold performance but also S&P performance. The combination of VIX and GVZ better predicts both stock and gold market performance, and implied volatility in other asset classes like T-bonds and crude oil might be predictive too.

CPM Group

Let silver facts dispel your silver theories

In his latest video, CPM Group’s Jeffrey M. Christian elaborates on silver bullion and coin inventories, explaining the composition of physical refined silver inventories and the ebb and flow of these holdings over the past several decades. He then discusses the relationship between open interest and registered inventories, not only for silver compared to other precious metals but across commodities including oil, corn, and base metals.

Click here to watch.