Company & Sector Research

Europe

Arete Research

With Liberty Global recently taking a 4.9% stake in its rival, it means there are now three major shareholders on VOD’s register who might be interested in acquiring assets. With the next CEO likely to be given a mandate to radically simplify the business, Alex Pound examines the impact of several deals that could be made include selling Vodacom to e& and reopening discussions with Iliad to sell Italy, with VOD aiming to slim down to an EU footprint spanning 6-8 geographies. His transaction-boosted fair value is 159p (~60% upside).

Woozle Research

100% of retailers interviewed by Woozle reported that the cosmetics giant is “clearly strategically outperforming” competitors such as Estee Lauder and Beiersdorf brands, due to quicker innovation and better positioning around the natural, sustainable themes for self-care products. Woozle's latest channel checks (across US, Europe and Australia) suggest OR is trading ahead of consensus forecasts in 1Q23, driven by outperformance in L'Oreal Luxe and Consumer Products, partly offset by weaker than forecast Active Cosmetics sales growth. On the subject of pricing, respondents reported an average increase of 10% Y/Y for OR brands (vs. 7% increase for EL).

Creative Portfolios

The share price has rocketed up 65% since Paul Hollingworth turned bullish in Nov 22 when he could see that the Greek bank was over delivering and undervalued. FY22 data showed that CET1 and NPE reached 11.5% and 6.8%, respectively (vs. targets of 11% and 8%). Return on TBV also beat forecasts, coming in at 10%. The bank’s overall profile has been transformed over the last 18 months. Its PH Score™ currently stands at 10, putting it in the top decile globally (bullish signal for higher returns going forward).

Entext

The stock is up more than 60% since Sean Maher added it to his energy transition basket (+240% since inception in 2019) towards the end of last year as both a power generation capex / China reopening play. RR's strong FY results come ahead of a sweeping restructuring from H2 to boost margins and ROE under its new CEO. Results showed an improvement in its civil aerospace and power systems divisions which is likely to accelerate over the next couple of years while crucially the highly indebted company generated £505m of FCF - smashing analyst expectations and buying time for the new far more commercial business strategy and inevitable recapitalisation to bear fruit.

TT Equity Research

Operating profit fell a long way short of Teun Teeuwisse’s expectations due to much higher than anticipated restructuring, rationalisation, impairment, and “other” costs. Only a mysterious inflow from working capital (exactly how ATO achieved this remains unclear for now) saved cash generation. This, alongside unjustified adjustments to profitability, meant ATO managed to remain within covenants reporting a lower debt equal to the FCF beat. Perhaps the clearest signal about the quality of the business is that it spent more than €200m on addressing underperforming contracts. Teun is happy to remain short as he still sees very little value for the combined businesses.

Forensic Alpha

Forensic Alpha always finds it interesting when a company flags on their system during a large capital raise since the incentive for manipulation is particularly high. GN's rapid increase in capitalisation of costs (especially since 2020) should be cause for concern. This pattern stands in sharp contrast to the amortisation of these intangibles remaining remarkably flat (aided by the "Useful Life" of the software intangible suddenly expanding from "1-7 years" in 2021 to "3-10 years"). If Demant is indeed actively looking at the company, some careful due diligence on the intangibles would be a good place to start.

the IDEA!

Newly created division offers compelling growth potential - the Corporate Performance & ESG division will be comprised of Corporate Performance (CCH Tagetik; US Corporate Tax), EHS / ORM Software (Enablon), Finance, Risk & Reporting as well as Internal Audit Solutions (TeamMate). The advantage of bringing all these activities together is that it offers an integrated multi-disciplinary solution for WK’s clients. With leading market positions in all areas, the new division is expected to grow at a double-digit rate (organically) going forward. The resilient nature of WK’s business provides a high degree of protection in these uncertain times.

North America

Two Rivers Analytics

Liquidity Risk Model: Best short candidates

ChargePoint (CHPT) - Burns $400m annually, a figure which is rising fast. Expected to run through most of its cash balance by early to mid-2024. Forecasts expect sales to continue slowing. Not expected to breakeven until 2026.

Floor & Decor (FND) - Requires nearly immediate outside financing, primarily due to very high capex spending. Net debt $1.8bn (vs. $200m in 2018). Sales are expected to slow further during 2023.

Natera (NTRA) - Diagnostics company will run out of cash by Sep having burned $700m+ in the past year. Not expected to breakeven until at least 2028. Trades at 5x 2023 and 2024 sales.

Huber Research Partners

While some may argue that its operations are “damaged goods” due to the elongated process with Standard General and the FCC, Craig Huber disagrees, especially with the current management team who he has long viewed as one of the best in the industry. Assuming the deal does not go through, Craig estimates 2023 & 2024 FCF after the dividend totals $1.15bn - enough to buyback >30% of the current M/Cap. That's too powerful to ignore, let alone if the company also levered up a bit to further repurchase stock. Patient investors will be rewarded.

Paragon Intel

Not only is Paragon Intel negative on CEO Kate Johnson’s ability to turn around the company, but their work suggests she is one of the most ill-equipped executives they have researched in their history to be in the specific CEO-seat! Paragon’s report is split into two documents: CEO Diligence Memo and CEO Interviews. Former colleagues questioned her lack of experience making capital allocation decisions and an inability to get in-depth on technical issues. They also pointed to an egocentric, insecure executive with “sharp elbows” who surrounds herself with like-minded colleagues, diminishing her credibility as a force for cultural change.

R5 Capital

Likely just the beginning - Scott Mushkin downgraded HD to Sell at the start of the year as he saw a high probability that the home improvement sector would experience challenges going forward. He believed this would become evident in 2Q23, with pressure increasing through the end of 2023 and into 2024. HD’s latest report and guidance issues have only increased his conviction. As a result, Scott has cut his FY23 and FY24 EPS estimates to $15.43 (from $15.73) and $15.77 (from $16.23), respectively. TP reduced to $248.

The Retail Tracker

Beauty bubble? Consumers may turn to “shopping” their beauty closets in 2023 - The Retail Tracker discusses increasing promotions, less customer loyalty, and how new partnerships may disrupt the space in this week’s edition of their Insights & Intelligence report. The growing de-influencing trend on TikTok, its current “hot” brands, and how celebrity brands are feeling saturated, and tired, are also covered. ULTA’s share price is up ~35% over the last year. This is not a good time to build a position, and investors should look to take profits. A less than perfect earnings call and forward guidance presents real risk.

Portales Partners

Charles Peabody upgrades the stock to Buy - he believes the marketplace will begin to appreciate the integrity of Citi’s balance sheet as management executes on its goals. Charles is projecting a $75 price target based on an 8.5% RoTCE and a projected TBV of $88 by the end of 2023. He thinks that following the successful sale of most of its international consumer banking operations, including Banamex, Citi could resume stock buybacks in the $3-4bn range in 2H23. The stock trades at less than an 8 P/E, 62% of last year’s TBV and offers a 4% dividend.

Badger Consultants

Tom Chanos reiterates his short recommendation following “stunningly horrible” 4Q22 results. Despite increasing commission rates and not paying interest on customer deposits, COIN is still very unprofitable. Despite cutting expenses and laying off employees, total operating expenses are increasing faster than revenue, which is decreasing. Meanwhile, regulatory scrutiny is set to intensify. Regulators have already forced exchange Kraken to cease and desist its staking program and fined them $30m. You can bet that they are looking at COIN as well. The share price has fallen 70% since Tom turned bearish, but his TP of $25 still offers 60% downside.

Singular Research

More than just a cyclical play - since new management took over in 2020 a transformation has been underway that has led to the streamlining and rationalisation of the company’s operations. MOD offers investors exposure to the rapidly growing European heat pump market (projected to expand at a CAGR of >8% from 2022 to 2030), the global data centre cooling market, and it is also expanding into battery thermal management, with potential opportunities in EV applications. The stock has risen over 160% in the past year, but Singular Research believes there is still a potential upside of 40% by FY24.

Gradient Analytics

Reports across-the-board misses and guides for lower-than-expected 2023 earnings - inventory growth continued unabated and Gradient remains concerned that management’s attempts to curtail production to right-size supply and demand may be too late to alleviate near-term gross margin pressure. Receivables continued to increase on an absolute and relative basis, suggesting the company faces an elevated risk of revenue shortfalls. A material relative decline in accrued employee costs, along with lower depreciation expense stemming from a recent accounting exchange, may have temporarily prevented a more material operating margin contraction.

Smart Insider

Jeff Lawson (Co-Founder, Chairman & CEO) purchases 158k shares at $63.26, spending $10m - this marks a reversal from a series of sales, most recently at $264 (Jan 2022). His only previous buy was at $23.43 in May 2017. Donna Dubinsky (Non-Exec since 2018) purchased $251k on the same day. This is her first time buying shares in TWLO and a reversal from sells at higher prices. She didn't acquire any shares at either of her previous Non-Exec roles. These purchases follow recently posted year-end results along with a workforce reduction and $1bn buyback.

Japan

LightStream Research

Mio Kato is extremely bullish on PSVR2 and believes volumes could massively surprise to the upside - he forecasts ~3.5m units in the launch quarter and ~10m units in the next full year. Even if Mio is wrong, all evidence suggests that market expectations are subdued enough that downside risk is limited. Pricing is unlikely to follow a loss leader model and thus while sales may initially not lead to additional hardware profit, as software sales pick up and/or if PSVR2 leads to additional PS5 sales, profit contribution overall should be strong. Marketing expense was also unlikely to be excessive, providing a further boost to operating profit.

Emerging Markets

Propitious Research

Following several years of sustained revenue share loss, Search’s digital advertising revenue market share has stabilised at ~10%. With China’s economic growth recovery, Baidu is perfectly positioned to accelerate its core marketing revenue growth, which is also a high-margin operation. This revenue mix effect, coupled with improvement in margins at its peripheral non-marketing operations, should boost operating margins (consensus forecasts of 14.2% in FY23 and 15.6% in FY24 appear conservative) and drive significant earnings growth acceleration. The stock is up 30% YTD, but continues to trade at a significant discount to its 5-yr average and global peer group.

Copley Fund Research

Fund Positioning Analysis: EM Restaurants

EM fund exposure in the Restaurants industry group is soaring to new heights - a record 51.1% of the active EM funds in Steven Holden’s analysis now have exposure with the largest increases in weight dominated by Growth and Aggressive Growth investors. Ownership increases were seen in Yum China Holdings, Americana Restaurants and Jollibee Foods over the last 6 months, whilst net positioning fell in Jiumaajiu International and Jubilant Foodworks. Invesco EM All Cap and First Sentier Global EM are allocating over 10% to the sector with a further 7 funds allocating more than 5%.

Galliano's Financials Research

4Q22 results confirm that NU is the benchmark among EM neobanks in terms of activity rates, as well as trends in revenues and costs per client and digital efficiencies. Victor Galliano sees further potential for broadening and deepening the product offer to customers, at little incremental cost especially in Brazil, to drive cost effective revenue growth. Victor’s proprietary NU model forecasts are broadly in sync with positive consensus estimates; he forecasts group ROE of close to 30% in FY25, despite high cost of credit assumptions.

AceCamp International

The Street is overly optimistic about the firm’s outlook in 2023/24 due to 1) gross margin and ASP contraction and 2) lower-than-expected gross margin and uncertainty for Apple’s OLED driver IC orders. AceCamp expects structural negatives for the display driver IC sector including 1) intensified pricing competition in large / small-sized display driver IC and 2) 20-30% dollar content decline for ram-less OLED driver IC despite a rising penetration. Their 2023/24 EPS forecasts for Novatek are 25-30% below consensus estimates and they expect 30-40% derating for the stock over the next 12 months.

Macro Research

Developed Markets

Totem Macro

Financial stability?

There is no question that banks have just experienced a massive capital shock. Just like during the Global Financial Crisis, explains Whitney Baker, equity losses have been outsized versus any expected range informed by recent decades. Like during the GFC, the losses have been outsized versus the overly generous capital and reserve buffers held against them. Because, like the GFC, the losses are coming from supposedly “risk-free assets”. But unlike the GFC, these are losses on yield risk – not credit risk. In almost all cases, zero risk-weightings and other regulatory nudges mean banks hold securities that are multiples of their capital and generating historic losses, even vs today’s elevated volatility. The Sharpe of shorting bonds has rarely been higher in centuries of history.

Blonde Money

UK: Not the Northern Ireland Protocol

Helen Thomas discusses how PM Sunak has played a significant role in the recent Windsor Framework agreement between the UK and EU, seeking to neutralise the impact of the Northern Ireland Protocol. Sunak’s consensual approach, which matches the EU’s desire to de-escalate the irritation of Brexit, has led to a more cooperative relationship between the two sides. Sunak's main goal is to ensure that his party accepts him as their true leader, and the agreement reflects a shift away from the weaponisation of the Irish Border and a commitment to working together to help each other. Indeed, Helen claims, this marks the end of the beginning of the Brexit negotiations.

PPG Macro

UK: Upside surprises

Patrick Perret-Green recently wrote about the excessive pessimism surrounding the UK. Since then, news has continued to surprise with sales, government finances and inflation all improving. The budget deficit is a whopping £30bn lower than the OBR forecast just three months ago, and much of it is down to the indexation of inflation debt. Patrick sees 20- and 30-year gilts as a long-term buy, and comments on the 10y10y implied yield at 4.4% being very attractive for pension funds. He’s also keen on sterling, especially vs the euro.

Talking Heads Macro

2y1y is mispriced globally – it’s all about r*

Central banks are finally beginning to grasp the true nature of inflation and the role of labour markets, exclaims Manoj Pradhan. The market must reassess where r and r* are as long as labour markets remain tight. r* depends on the regime: if inflation falls to target with an economic soft-landing, r* is higher than most are assuming. If inflation remains persistent along with strong labour markets, r must stay higher than r*. Only when the regime changes will rates move lower. This comes with the realisation that 2y1y is mispriced across DM and needs to move universally higher. The same goes for EM 1y1y with the most compelling points being in Mexico and CE3.

View from the Peak

Mean reversion – has the global narrative changed that much?

2023 was always going to be about mean reversion, explains Paul Krake. Central bank expectations will be less aggressive in 2023 than the year prior because 2022 was when all the heavy lifting was done. Expect the Fed to move 150bps in total in 2023, leading to lower interest rates, currency and risk asset volatility. With this subdued Fed movement, the path of least resistance is a softer USD with bear market rallies throughout 2023, including the one we are in now. There will be few home run opportunities this year. US equities are expensive, so re-establishing long EM and China equity trades should be done with some US growth equity shorts.

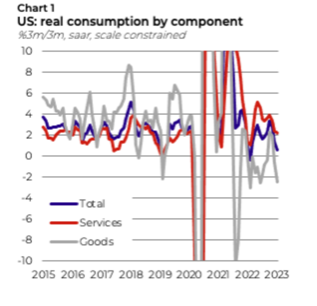

Suttle Economics

US: Fool me twice

US consumption strength continues to surprise financial markets, with real consumption up 1.1%m/m, the strongest monthly gain in two years. Growth remains above trend, although that doesn’t dissuade Phil Suttle from his Q4 recession forecast. He comments on the huge amount of noise in consumption, which needs to be smoothed out against a very weak Q4 (see graph) and what Phil believes to be a shift in the seasonal pattern of consumer goods spending across DM. Once you push past the noise, the “disinflation” trend remains intact, albeit slow. Expect the Fed to hike three more times by 25bps to 5.375%, especially once softening Feb data is revealed.

WaveTrack International

US recession looking likely as long-term dollar outlook remains poor

Central banks have overestimated the impact from 6-month declines in headline CPI prices, and market expectations of a Fed-pivot will likely go unmet. Elliott Wave analysis expects further interest rate rises through Q1/2 2023 before a collapse lower afterwards as risk assets sell off, triggering a short but sharp recession. The long-term outlook for US remains very bearish, with a depreciation of -55% before the end of the decade. A short-term counter-trend wave rally is expected soon, with the catalyst for USD strength coming from inflationary pressures, higher yields and safe-haven buying.

Pennock Idea Hub

Fight the tape or the Fed?

The market narrative is shifting to one of no recession and continued growth. As well, global liquidity is putting a floor on the price of risky assets, but at the same time the FOMC warned that a restrictive policy stance would have to be maintained. So, should investors fight the tape or the Fed? Edward Pennock believes the answer lies with investment time horizon. In the short-run, liquidity controls the tape. In the long-run, valuation and interest rates matter to returns. For now, European stock and cyclical industries are the leadership. Enjoy the ride and take shelter if their leadership falters.

Emerging Markets

Crystal Shore Alpha

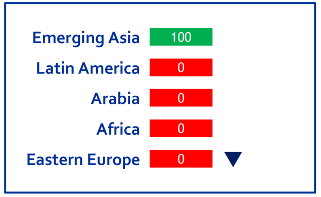

Eastern Europe downgraded, what’s left?

There is only one remaining bright spot in the global EM universe: emerging Asia. But even here, three of the smaller Asian markets—Malaysia, Vietnam and Pakistan—are already flashing red. So that leaves us with the big 5 (China, Taiwan, South Korea, India and Thailand) plus Indonesia and the Philippines, all still solidly in green. The GEM Dashboard is a data-driven roadmap of the 5 big Emerging Market regions and all 34 Emerging countries, from China to Romania and Saudi Arabia to Argentina. The binary risk data that is generated market by market on a weekly basis doubles as crystal clear buy/sell signal for EM money managers.

Trivium China

China: Recovery not on a solid footing

The econ numbers for 2023 so far show something of a strange disconnect: the parts of the economy that are performing the best are also those sectors with the weakest credit demand, while the areas that have not yet seen an improvement in activity are the ones that have taken out the most loans. Households are spending more but long-term confidence remains damaged, reflected by a dramatic decline in household borrowing. Corporate borrowing has recovered, but the Trivium team question whether this reflects government-directed lending rather than improved corporate confidence. Perhaps the post-covid boom isn’t sustainable, after all.

Horizon Insights

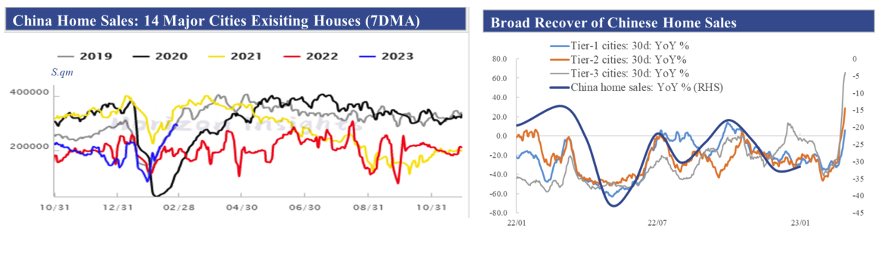

China: Home sales continue

Stronger than the seasonal pattern suggested, China's home sales continued to rise in the last week of February. So far, home sales of new houses in China's 30 major cities have surpassed 2022. Continuous improvements can also be seen in the second-hand market, where the market listing prices of existing houses continue to rise (see chart). With a broader recovery, China's home sales in the first two months of 2023 came in around -25% down from last year, up from -31.5% in December.

Alberdi Partners

Argentina: Inflation remains close to 6% m/m

Inflation in February was elevated among a wide range of CPI components, thus despite lower regulated inflation, Marcos Buscaglia expects headline CPI to stand close to 6% m/m. The depreciation of the official FX accelerated since the beginning of 2023, particularly since end-January. Regulated inflation is set to spike in March as public services are subject to price increases. The combination of a faster crawling peg, higher incidence of regulated prices and a seasonally decline of money demand leads Marcos to expect another high reading for the headline CPI in March.

IndiaDataHub

India: State of States dashboard

IndiaDataHub have introduced a new dashboard, allowing investors to track high frequency data for all the states of India. There are several indicators that can be tracked, ranging from car sales to credit growth, from GST collections to NREGA demand, from power consumption to mutual fund AUM. With more than a dozen indicators to begin with, more will be added over the coming months. Please contact us to find out more.

Emerging Advisors Group

The story is now looking towards Korea

On the equity front, Taiwan’s dramatic outperformance of the rest of EM in 2020-21 has been the big story. However, that theme is over for now, claims Jonathan Anderson - global trade is already in recession and will remain there through 2023, and China is losing industrial share at the margin, both of which will dampen Taiwan’s prospects. Going forward, Jonathan favours Korea; in a weak external environment, Korea still has “normal” external demand conditions compared to Taiwan’s stagflationary muddle.

Oxford Analytica

Thailand: Bangkok appears bullish about the economic outlook

Thai Finance minister Arkhom has said that infrastructure projects and post-pandemic revival of the tourism economy will boost the economy, with official forecasting 3.8% GDP growth in 2023. Last month the cabinet endorsed a framework for government spending in the year ahead, but this is unlikely to be smooth. Any delay in budget implementation will result in a small hit to GDP growth. Arkhom may be factoring this into the scenario he presents, but he appears to be downplaying the risks.

Commodities

Greenmantle

Oil: Trading sideways

Since early January, Brent has traded in a relatively tight band of $79-$89. Oil markets are attempting to price in a number of factors with substantial impacts on the balance between supply and demand: a possible global slowdown in coming quarters, the demand increase from China’s post-COVID reopening, and the uncertainty of future supply from Russia, OPEC+, and other major producers. Niall Ferguson is relatively sanguine on macro risks and expects a gradual increase in Chinese demand to accelerate in 2Q. On the supply side, he sees risks from Russia sanctions and OPEC+ production discipline, leading Niall to be cautiously LONG oil.

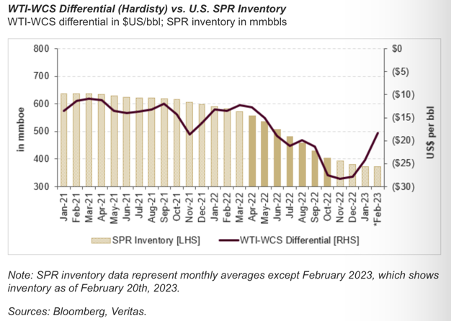

Veritas Investment Research

The narrowing of the WTI-WCS differential

Dan Fong highlights a recent and rapid narrowing of the WTI-WCS differential, which has generally positive implications for Canadian oil sands producers. Since bottoming out at ~USD$33/bbl last October, heavy differentials have narrowed to ~USD$18/bbl. This coincides with a pause in US Strategic Petroleum Reserve releases and the prospect of replenishment. In addition, with support from L3R and TMX, Canadian heavy has a line of sight into additional takeaway capacity and new markets. Price and spread volatility notwithstanding, these factors should be a net positive for WCS. Canadian Natural Resources and Imperial Oil have some of the highest cash flow sensitivity to differential changes.

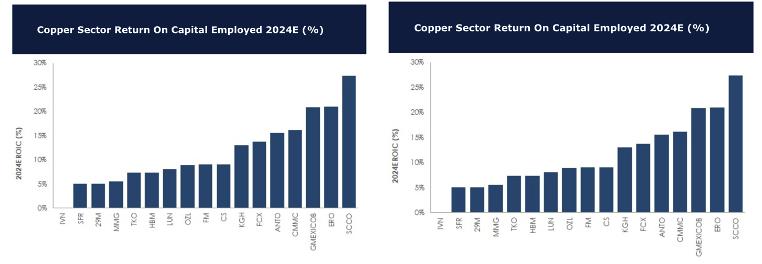

Global Mining Research

Returns on capital: Copper vs Gold

For 2024, David Radclyffe forecasts copper to enjoy an average ROCE of 11.1%. The standout is Southern Copper Corp, helped by some very low cost and long-lived assets. Relatively new to the market Ero Copper Corp does well, while at the lower end sit Ivanhoe Mines and Sandfire Resources. When it comes to gold, the forecasted average ROCE for 2024 is at 8.3%, with Gold Fields coming out on top and Lundin Gold close behind. The copper sector as a whole continues to generate better real returns on capital than the gold sector, with gold miners continuing to suffer from shorter mine lives and a commitment to M&A to create growth.

CHA-AM Advisors

White Gold: A classic over-earner

Inflation is a monetary phenomenon. As soon as the central banks start removing the excess liquidity commodity prices start their initial falls. This elicits the normal attempts to talk prices back up - the tomato shortage in the UK is a classic example. Low-cost producers smell blood and accelerate market share gains by cutting prices. They start to bring prices down to their break-even points. Industries consolidate around these low-cost producers even growth industries like solar panels. Next up the same people who are moaning about shortages will soon be calling for government help as their credit implodes. We're going to see this pattern across the board from sellers of tomatoes to EVs to wind turbines and solar panels. Stock selection has to reflect this permanently operating factor.

CPM Group

Digital currencies and what they mean for gold and silver prices

The long-term movement toward central bank issuing digital currencies has caused speculation about how digital currencies may affect gold and silver markets and prices. Jeffrey Christian provides expert analysis on the subject to help investors decide how they should approach and prepare for this inevitable transition. Jeffrey also provides a market update on gold and silver prices, discussing what happened the past week and how CPM Group sees prices moving through March and beyond.

Click here to watch.