Company & Sector Research

Europe

Holland Advisors

Covid has found management having to take far longer with the GKN turnaround than they initially thought. As a result, Andrew Hollingworth wonders if Mr Market has forgotten what they are capable of. He considers the price of success - i.e. what value to ascribe to MRO should its turnaround be broadly successful. The short answer is: £15.7bn. This being the EV that he postulates current pre-split MRO is worth c.3 years from now (~125% return). For some investors an assumption of the Aerospace division's growth in the coming years + margin recovery + re-leveraging + this capital being used to boost equity returns sounds like a super-unlikely tri-factor of events. Andrew disagrees…

Iron Blue Financials

An Iron Blue score of 37/60 (+2 Y/Y) is top quartile (fertile ground for shorting). Red flags include expanded use of stripped out restructuring (incl. start-up costs & depreciation) expense, widened gap between PPE capex and depreciation, and movements in bad debtor & inventory provisions. Against waning FCF (post 2020-21 PCR test boost), ERF's interest burden is increasing (6.75% €600m hybrid priced in Jan, implied cost = 17% of 2022 FCF). Additional governance red flags include deepened corporate structure complexity, audit fee up to 2-3x peers and CEO’s brother shifted from executive to non-executive director. A new 2022 risk factor was added about risk of accounting error / fraud.

Silk Road Research

China channel checks reveal underperformance in order activity - rather than being driven by the expected differences around pricing / financing terms between major OEMs, SRR’s industry contacts cite a combination of above-average exposure to distressed developers, replacement of an industry veteran with an outsider to lead its China business, and increased competitiveness of OTIS and domestic brands as key drivers of its underperformance. SRR estimates KONE may have lost up to ~150 bps of share over the past 12 months.

Forensic Alpha

While most investors in ASM are focused on the impact of macro headwinds in the semiconductor industry, Forensic Alpha’s systems noticed an odd movement in the profile of aged receivables - 20% of receivables are now past-due, with 10% now past due more than 30 days (vs. 2% in 2021). By the standards of the industry this is significant and should elicit more questions from investors around the current state of ASM's customers.

ResearchGreece

Announces the acquisition of Enel's assets in Romania for a total EV of €1.9bn - ResearchGreece likes the transaction because a) it was completed at a 50% discount to recent RES deals in Greece, namely Motor Oil’s €2.0m/MW or 12x EBITDA acquisition of Ellaktor wind assets; and b) it is evidence PPC is delivering on its business plan targets as laid out in 2021. ResearchGreece expects the same to follow with Greek RES targets (+5GW by 2026). TP €12.8 (60% upside).

North America

Trivariate Research

Are you finding short ideas the right way?

Adam Parker of Trivariate Research provides a framework for finding “melting ice cubes” - he evaluated prior price performance (momentum over previous 12 months), accruals (disconnects between earnings and FCF), revenue (share loss), gross margins (relative to industry group contraction), earnings declines and downward earnings revisions as potential candidates for “cube identification”. Adam found that no other major fundamental attribute comes close to achieving the level of success at predicting subsequent underperformers as either accruals or momentum. Fundamental analysts who focus disproportionately on revenue share gain and margin contraction to find short ideas are wasting their time. Short ideas include Home Depot, Equinix and Micron.

Inferential Focus

Technology loses its cultural currency

Digitisation continues to move businesses toward digital-first operations. Yet as a cultural force - guiding behaviour, individual thought processes, interpersonal communications, the popular arts and society’s values - digital tech is losing leverage. It is facing changes in personal attitudes among individuals who now worry about the “addiction” that social media and smartphones trigger, and more lawsuits have arisen claiming high tech is responsible for several societal ills. Much of tech has lost its influence in the cultural realm, as the “real world” regains appeal. In short, tech has lost its “cool”.

MYST Advisors

TMT Idea Forum

It was not surprising to hear several AI-related ideas given recent fervour for plays on the burgeoning technology, but it was unusual to see so many hardware / semiconductor ideas presented at a broad TMT event. Participants were focused on stocks that were relatively inexpensive even when valued on GAAP earnings. While most participants did not dispute their fellow presenters’ large earnings forecast deltas vs. consensus, many heavily debated the appropriate multiples to apply to those earnings. The most compelling ideas included:

Corning (GLW) - “Green shoots” emerging from cyclical bottom while margins structurally higher. TP $50 (45% upside).

Nu Holdings (NU) - “The best FinTech in the world” completely mis-modelled by the Street. TP $10 (100%+ upside).

Shutterstock (SSTK) - Leading photo "Arms dealer” with generative AI to drive new leg of growth. TP $150 (100%+ upside).

Radio Free Mobile

Zuckerberg giveth and he taketh away - the benefits from another round of job cuts look set to be offset by the decision to cut prices on VR headsets due to flagging sales. Richard Windsor suspects that META has been losing >$200 for every device shipped and if volume returns to ~1m per month this will increase the losses at Reality Labs by anything up to $800m per year. Richard still thinks there is far more that Zuckerberg could do to increase profitability and if this were to occur then the stock would look very cheap indeed. However, he is not convinced this will happen meaning the value proposition remains uninteresting with >20x PER ratio being demanded for negative growth.

Gordon Haskett Research Advisors

Freight spinoff? - Bobby Mollins was not surprised to hear that management is considering its options having published several bullish notes on UBER’s freight business over the past ~20 months. He thinks an IPO next year is the most likely outcome and it could be worth $5bn. Bobby uses CH Robinson and XPO as comps and runs a valuation estimate based off of revenue for 2022-24E. He remains bullish on UBER as a company that continues to further engrain itself in the everyday lives of consumers. His TP is $48 (45% upside).

Hedgeye

The biggest player in the best market - Todd Jordon thinks the Las Vegas Strip has huge potential over the next 12 months+ and MGM is in pole position to harness the positive market forces. Outperforming RevPAR, stable gaming and stickier margins create a very compelling setup. He argues that Street estimates are not bullish enough, and regardless of framework the stock is cheap on an absolute and relative basis. Todd sees MGM’s stock north of ~$60+ in the NTM (45% upside).

Todd presented his bull thesis at IRF’s recent Consumer Equity Conference. Click here to access the audio / slides.

R5 Capital

The volume declines and market share losses from a large, financially sound, supermarket chain are unprecedented in the 20+ years Scott Mushkin has been researching the industry - while he finds no “smoking gun” around exactly why the market share losses are so severe, reduced promotions (industry-wide) and some store slippage will have had an impact. Given the current business challenges, it throws into question the amount of net synergies KR will realise following its merger with Albertsons. Furthermore, vendors generally shift support away from companies that show sustained market share declines. The situation is unsustainable. TP $36 (25% downside).

Portales Partners

SVB failure triggers historic sell-off: A buying opportunity for Bank stocks

Charles Peabody provides a post-mortem on Silicon Valley Bank and points out that historically when banks perform so badly, they turn out to be good buys. Charles thinks rates have peaked on an interim basis, and bank earnings should be a calming influence. Revenues are strong and credit issues remain benign (albeit “normalising”). Most banks have sensible deposit beta assumptions, few are exposed to crypto, and few banks took on interest rate risk like SVB. As these fundamental facts become apparent during previews and actual results in April, bank stocks should snap back. Top Buys include JPMorgan, Citigroup, and Wells Fargo.

Smart Insider

Six insiders spent a total of $4.8m buying stock at ~$57 per share. Gregory Norden (CEO) splashed out $3m. John Adams (Non-Exec) purchased $297k of stock in his largest buy and his first since 2016. Stephen Ellis (Non-Exec) spent $379k - his only purchase in the last 10 years. Furthermore, Peter Crawford (CFO), Richard Wurster (President) and Todd Ricketts (Non-Exec) all bought stock for the first time. While this is likely a co-ordinated cluster of buying post SVB's collapse, these are material purchases. Stock Rank +1.

Alembic Global Advisors

Post 3Q23 results Pete Skibitski increases his two-year outlook (through FY25) for revenue, EBITDA and cash flow - AVAV's funded backlog grew an impressive 41.2% Q/Q to $413.9m, which also followed a 43.7% increase in 2Q23. Ukraine wardriven demand continues to propel firm order flow for small UAS and tactical missile systems. At this point, FY23 revenue looks set to grow in the double-digits; management is targeting DD growth in FY24 as well. Product mix is improving, as are margin rates. With more order flow expected due to global defence spending demands, Pete sees AVAV outperforming the S&P 500 over the next 12 months.

Veritas Investment Research

InterRent's entire portfolio is located in provinces with rent controls (with renewal caps set below the prevailing inflation rate) and coupled with the trend for declining turnover rates, Veritas estimates that InterRent's NOI per unit growth will moderate to MSD by the end of FY23. In addition to being the most vulnerable REIT within Veritas’ residential coverage to a further rise in interest rates, InterRent’s potential for unitholder returns and distribution growth is also the weakest in the group. The stock trades at a ~40% premium to sector peers. TP C$9.25 (30% downside).

Arete Research

Semis Inventory: DEFCON 1

Semis days inventory build from 4Q21 to 4Q22 has happened more quickly than at any point since 2001/02. A toxic combination of sales decline and inventory build has added 22 days in a year (to a total of 64 - anything >40 historically has been red zone territory). To put this in context, the 2018/19 peak-to-trough build only added 9 days and in 2008/09 it added 12. Memory is by far the worst offender. Relying solely on demand to reduce inventory days looks unrealistic. Jim Fontanelli thinks we will see write-downs and further ASP reduction. A rapid 2H23 revenue bounce, needed to move stocks up further (especially given the moves already) looks unlikely.

Japan

Aequitas Research

Looking to raise US$375m in its upcoming IPO - TH operates a network of retail stores in Japan that offer one-stop shopping under its EDLP model. On the back of store addition (added 40 stores FY19-1H23; plans to add >20 more each year from FY24 onwards) and strong SSSG, FY22 sales were up 12.4% Y/Y, while 1H23 sales were up 10.9% Y/Y. However, the company’s net profit margin remains wafer thin at just 1%. In addition, TH's focus on low prices might make it difficult for it to pass on some of the recent price increases in food items. Finally, there are a lot of small shareholders who will still own ~16% of the company. Post lock up (180 days) they may well look to sell more shares.

Asymmetric Advisors

Amir Anvarzadeh turns bearish after discussions with Ushio which supplies Lasertec with its EUV lamps for its mask inspection systems. Ushio states that it sees little room for growth in unit sales of its EUV light sources next term (3/24) after this term's poor sales which is set to drop by around two-thirds. As a reminder, Lasertec had already slashed its order target (6/23) by a whopping 40% which came as a big shock. It appears that we are starting to see real competitors emerging in EUV mask inspection systems that Lasertec had been seen as dominating.

Singapore

New Street Research

Given the cyberattack in Australia, and recent share price weakness, it is perhaps foolhardy to talk of SingTel joining a Golden Age as New Street believes has happened for Chinese, Korean and Japanese telcos. However, ROIC has inflected and almost all meaningful parts of the group have started to grow again, suggesting MSD top-line and DD EPS growth going forward. New Street expects net profit and hence the dividend to double between FY22 and FY26. If this doesn’t constitute a Golden Age for a low risk, well managed telco, what does? TP S$4.4 (85% upside).

Emerging Markets

LightStream Research

Revenue growth has underperformed consensus expectations in all quarters since management decided to cut costs to ensure its long-term survival. The share price sank ~20% leading up to 4Q22 earnings and has dropped more than 10% since then to $12.86 per ADS. However, the valuation remains expensive compared to regional peers - CPNG still trades at an 80% premium to the second most expensive e-commerce name in the region. With the share price breaking the trend line, Oshadhi Kumarasiri sees the stock falling below last year’s bottom of $8.98 per ADS.

Entext

Much deeper automation looks like the only realistic solution to S.Korea’s fertility / working age population crisis - Doosan with its 90.9% stake is aiming to IPO Doosan Robotics in H2 this year, which is expected to be worth 1trn+ KRW, and the spin out will become one of the few global pure-play ‘cobot’ names. The group also fits the energy transition theme - Doosan Enerbility has been busy strengthening its small modular reactor and liquefied hydrogen businesses. Sean Maher replaces THK (+67% since inception; more fully valued) with Doosan in his automation basket (+120%), and once the robotics IPO is complete, Doosan will move into his energy transition basket (+230%).

AlphaBox Advisors

SJVN is a promising play on the growing renewables sector in India. It is an efficient hydropower generation public sector enterprise with an installed capacity of ~2GW. It shall see its capacity more than double to 5.5GW by FY24 through a mix of hydro, other renewables, and one thermal power project. While such an expansion will lead to an increase in debt, the impact would be offset by an expected increase in operating leverage as and when new plants commence operations. Trading at a reasonable trailing valuation of 12.6x P/E, 0.9x P/B, and 1 mln USD/MW EV-to-capacity, the stock offers a decent dividend yield of 5.5% and an upside potential of 30%+ in 12-18 months.

Macro Research

Developed Markets

Marex

Further bullishness in various currencies

On March 9th, the Marex team cited a positive reversal in the British Pound. The team now sees further bullishness in various currencies. Swiss Franc vs USD: monitor for a positive MACD crossover from below the Zero Line on a close above 1.0681 (lower pane on top chart). Prior similar setup via green vertical line. Aussie Dollar vs USD: monitor for a positive RSI close above 30 (lower pane on bottom chart). Prior similar bullish setup via green vertical line (bullish Aussie).

Greenmantle

The Ostrich Strategy: Europe in Cold War

China is increasingly competitive with Europe in complex manufactured goods, particularly autos, explains Niall Ferguson. In Germany, Chancellor Olaf Scholz’s coalition partners—the Greens and Free Democrats—want to use trade policy to confront Beijing. But business leaders, the Social Democrats, and Scholz himself are more cautious. Other EU economies are still adjusting to life without Russian energy. They too believe they cannot afford a major trade spat with Beijing. In the near term, the EU is therefore unlikely to respond decisively to Beijing via further high-tech export controls, outbound investment screening, or trade measures on Chinese autos. But this could change quickly if China starts sending lethal aid to Russia. Niall is underweight EU industrial and automotive stocks that face competitive pressure from Chinese rivals.

Independent Strategy

ECB: Backwards to the future

The justification for the ECB’s recent rate hike was Lagarde economics, which David Roche criticises, explaining how the ECB and US Fed will ignore its stability mandate and pursue monetary policy until the economic machine busts. This should be seen in the context of central banks seeking to re-establish their credibility after their systemic failure to control inflation – which they helped generate. It’s all denial economics. In a world rotten with excess leverage, unrelentingly increasing the cost of it will cause the system to crack. Expect the ECB to reduce rates in a few months.

Pennock Idea Hub

False dawn?

The US stock and bond markets are in disagreement again. Cyclical industries are in relative uptrends, indicating expansion. The 2s10s yield curve disagrees, with the deep inversion indicating recession. Which one is right? Current market expectations of a cyclical recovery is unrealistic in light of the Fed’s focus on 2% inflation. While history doesn’t repeat itself but rhymes, the current situation is reminiscent of the 1980-82 double dip recession. Technical conditions are bullish for stock prices, but investors should be prepared to revise their risk profile as conditions change later this year.

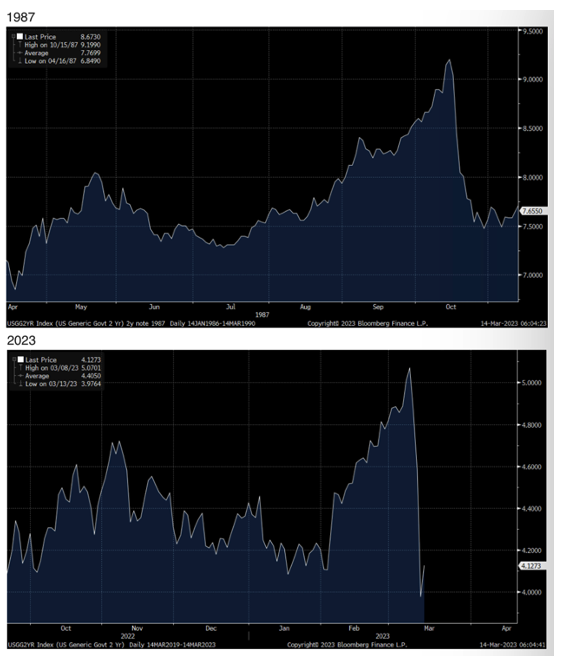

PPG Macro

Bond bear

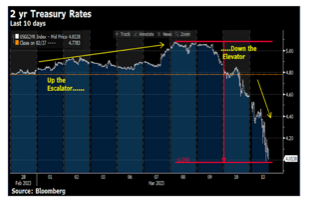

Patrick Perret-Green is the most bearish he has been on rates in a very long time. This is a liquidation event with rate bears decimated and largely stopped out – it all reminds Patrick of December 2008. Once stop losses are exhausted the rebound in rates could be substantial. Further fed tightening will be limited at best. There’s been a lot of talk this week about October 1987: back then the drama was portfolio insurance, now it’s some US banks. Patrick notes the price action of the 2yr note at the time and today (see chart). Mind how you go…

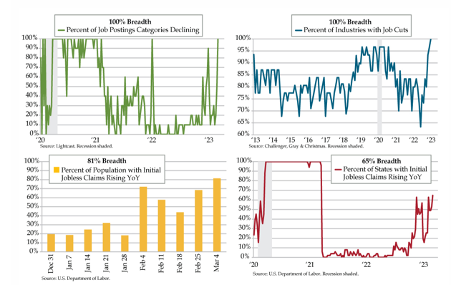

Quill Intelligence

Yes, the US labour market is in recession

Whether this is validated by what’s recognised as being corrupted Bureau of Labour Statistics data is semantics at this point. The ASA’s staffing index was 4.5% below last year’s levels and fell for three straight weeks. We’ve also seen for the first time outside of Covid lockdown that Lightcast job postings were falling across all 10 subsector categories. 81% of the US population is now living in a state with rising jobless claims, up from 73% last week. Powell can nominally remain in recession denial, but the markets have no such luxury.

Capital Alpha Partners

Biden’s big $6.9trn budget

President Biden’s budget includes $1.7trn in total discretionary spending. The budget is primarily paid for with some $5trn in new tax increases as there’s very little in the way of spending cuts. This is a tactical budget, designed to preview his 2024 campaign, but Biden’s budget is aspirational: it is a messaging document. It is also meant to contrast with Republicans and jam them on virtually any proposal to cut spending, exposing rifts in the GOP. More importantly, while it’s DOA since Republicans aren’t interested in pursuing tax increases or increasing mandatory spending, it is a preview of what Biden and the Democrats will try to do if they sweep the 2024 election.

Ollari Consulting

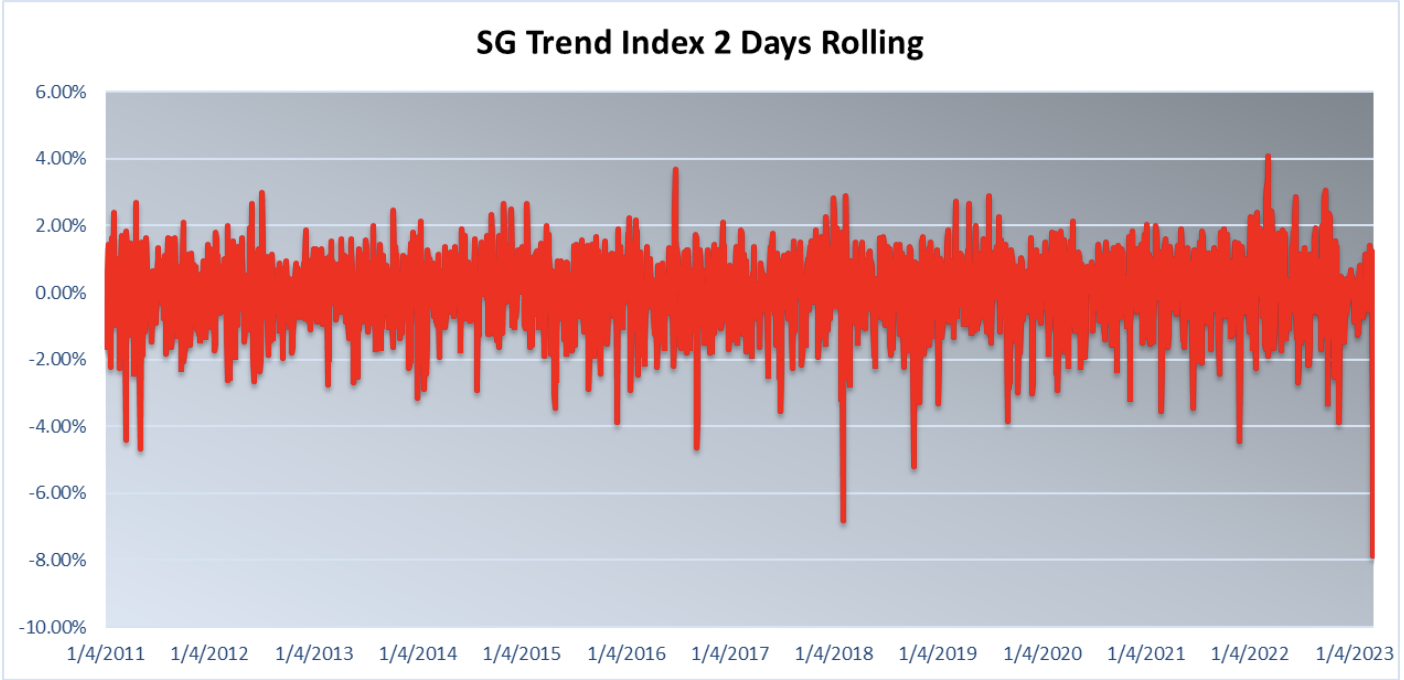

An epic positioning unwind

Christophe Ollari discusses the horrendous deleveraging from the CTAs community, going into the SVB’s failure close to max long equities and max short fixed-income (positioning focused on the short end of the curve). To visualise, he looks at the SG Trend Index rolling 2 days performance (see chart). Two days, a 7.87% drawdown: worst print since the start of the series – 6.5 SD move. CTAs stopped out in almost 90bn worth of equities in those two days. Almost 130bn of STIR, reducing their 100% short down to 19% short. As feared, says Christophe, CTAs have once again started and amplified the deleveraging. The modern market structure is all illusionary stability breeding temporary but epic instability.

Eurointelligence

What central banks must do, and must not do

As financial stability spreads across sectors and continents, central banks are being pressured to go slow in interest rate increases. Wolfgang Munchau argues that it would be a big mistake to yield to financial dominance. Instead, central banks should address inflation and financial instability with separate instruments. Postponing QT together with more flexible collateral policies would go much further to stabilise the financial system, leaving central banks free to use the short-term interest rate to deal with fluctuations in the economy, as it should be.

DeSaque Macro Research

Active equity portfolio management trumps passive in the post-easy money environment

The reaction of central banks to the GFC was a boon for the surge in passive investment funds after 2008, comments Said Desaque, with easy money and rising passive fund flows helping to create bubbles in equity and fixed income investment benchmarks. Attitudes changed and attention was paid no more to corporate profits. In today’s world of higher economic and inflation volatility, Said believes that the nature of post-GFC investment environment will not return, paving the way for much bigger opportunities in active fund management.

Emerging Markets

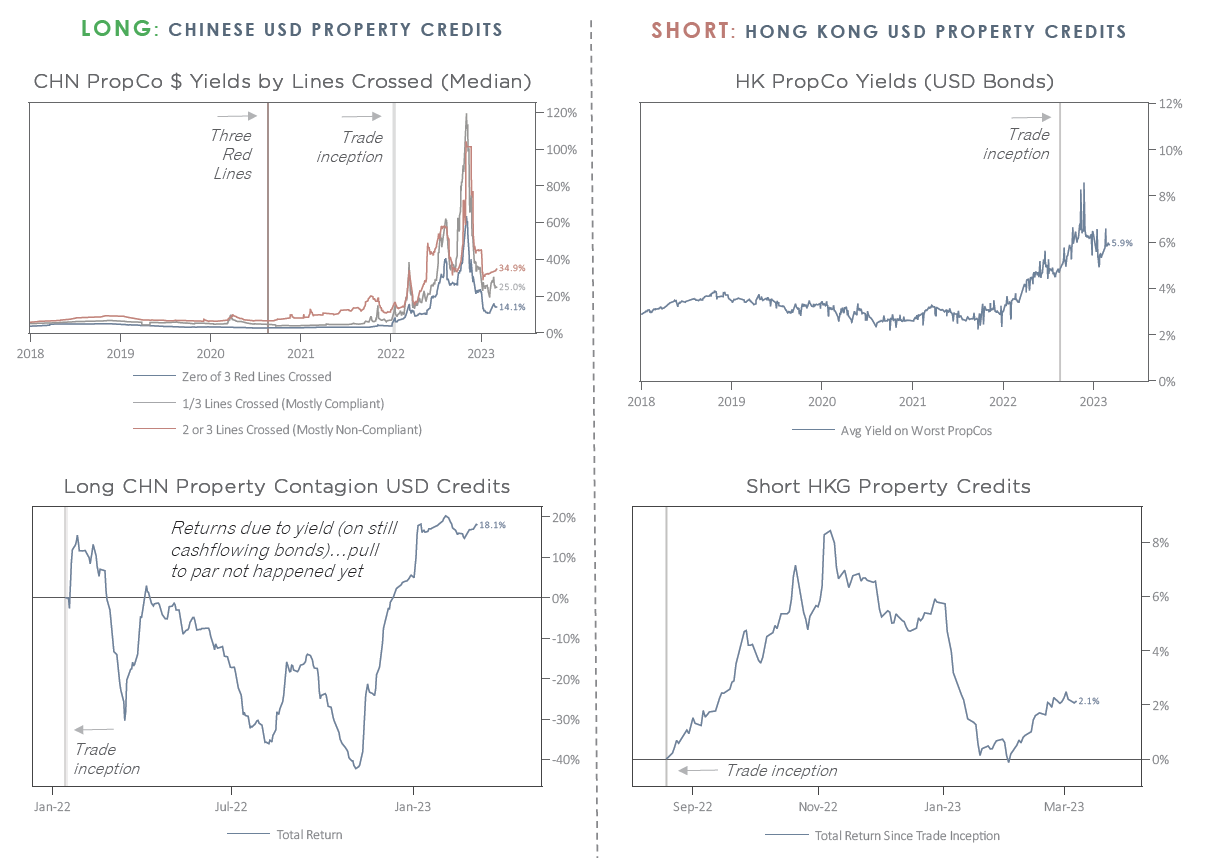

Totem Macro

Long CHN vs Short HK PropCos

China voluntarily restricted credit with Three Red Lines, leading to sector-wide stress, while the Hong Kong peg ensured a bubble and now guarantees vicious asset deflation. With HK property twice as expensive as the next global market, incremental buyers require rising debt to fill the gap. Residential prices are only 15% off their peak, with developers highly leveraged, but bonds are only just reflecting the potential for stress there; their book values will mark lower with prices in their next reports, and the leverage to that price drop will be revealed. Meanwhile, China’s reopening is causing property prices to rise again sequentially with activity picking up. Whitney is profitable in both trades, and while the Chinese trade is now a little less asymmetric it remains a LONG, while the HK SHORT has become even more asymmetric.

CrossBorder Capital

China throttles down

China’s large liquidity impetus from late-2022 has rapidly faded through March. Michael Howell suspects further doses of stimulus will come, but the latest fall-off will feed through. As it does, markets will likely pull-back as cyclical and ‘Risk-On’ concerns build. This does not alter Michael’s longer-term view that the major stock and bond markets will be range bound in 2023. Within this framework, he continues to prefer cyclicals and still favour EM, on weakness.

Emerging Advisors Group

Bangladesh: The taka is still under pressure

Since Jonathan Anderson’s latest report on the taka, it has depreciated another 15%, with complaints of exchange controls from the corporate and banking sectors. However, Bangladesh is not a fundamentally stressed economy. In contrast to Pakistan and Sri Lanka, the country has no wide fiscal imbalances, public debt pressures and large external debt overhangs. Rather, the problem lies in “run of the mill” flow external deficits, with the country needing to adjust domestic demand. There’s no hurry to get back in, but Jonathan wants to watch and make sure tightening holds, especially as global trade heads into recession.

IndiaDataHub

India: All about food

CPI inflation remained above 6% for the second consecutive month in February. At 6.4% YoY, it came in unchanged from January and slightly above consensus expectations. Whilst weakening growth will bring down core inflation, some of this impact will be offset by persistently high food inflation. The MPC raised the policy repo rate by 25bps and maintained a hawkish stance, but the last two readings have come in higher than projections. The risk to inflation remains on the upside, especially when considering the risk of an El Nino – expect rates to rise by more than just another 25bps hike.

Burumcekci Research & Consulting

Turkey: Short FX changes

Last week, the overall short FX position of the banking system improved by $201mn to $971mn. The public deposit banks' short FX position deteriorated by $51mn to $813mn, while local private banks' short FX position worsened by $204mn to $204mn, and foreign banks' short FX position improved by $48mn to $80mn. The upper limit for the net FX position of banks relative to shareholders' equity was reduced from 20% to 5% in January 2023, causing a drop in private banks' long FX positions. However, as a new development, the upper limit for the share of banks' net foreign exchange position in shareholders' equity has been raised from 5% to 10%. The sector's shareholder equity is at $93.1bn.

ESG

Sustainable Market Strategies

A Two-Speed Transition: Why it’s time to park the EV frenzy in EMs

Almost all developed countries have fairly aggressive zero-emission vehicles targets, and shockingly, some of these targets could actually be met! However, it is a different story in EM countries. This means that the real automotive transition in EMs will be from highly polluting cars to less polluting ones, providing a tailwind for emission control technologies such as catalytic converters and their metallic components: platinum, palladium and rhodium. Companies featured in SMS' report include Umicore, Johnson Matthey and Sibanye Stillwater.

Saltmarsh Economics

Changing climate, changing finance

David Owen’s latest note examines the quarterly data on UK and EU-72 greenhouse gas emissions. If trends seen in recent decades are maintained, UK net zero 2050 could very well be achieved. However, much of the improvement has been driven by changes in energy usage and going forward there needs to be more fundamental changes in behaviour, driven by government. As David has highlighted before, the increasing focus on climate change by central banks and rating agencies could eventually lead to major changes in the global benchmarks. Climate change has yet to be priced into the sovereign bond space. However, led in part by the ECB, could that be about to change?

Commodities

ERA Research

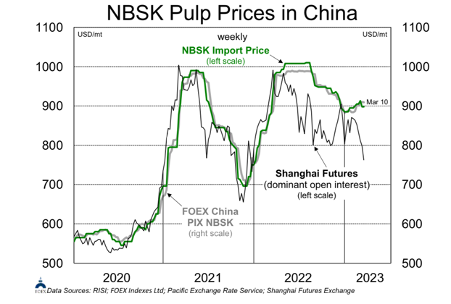

NBSK Pulp prices in China

After a spike in January, the Shanghai pulp futures have reversed course, ending last week at $769, a price level not seen in the front contract since late 2021. Following the Western Canadian closure and downtime announcements, in combination with expectations of robust China demand, an optimism that pulp prices would make early gains had pervaded the market. This has been unmet, largely in part due to extremely soft paper and packaging markets in Europe and North America and poor Chinese demand. Downward pressure may be exacerbated by expectations for market expectations for new hardwood supply from two new greenfield mills coming online in LATAM. Tissue producers will benefit from lower pulp prices, including Cascades and Clearwater Paper. Mercer continues to be the preferred route to pulp exposure for long-term investors, with the softer outlook already priced in valuations.

Vanda Insights

Crude succumbs to rate hike fears again but may remain rangebound

Crude prices dropped in response to Powell's testimony to the US congress. There may be more turmoil ahead, but Vandana Hari believes the relatively narrow range that Brent futures have been mostly pinned to the past 15 weeks will hold. Chinese crude imports were slightly lower YoY but this may be a red herring; high-frequency data on mobility and consumer spending, as well as an expansion in manufacturing and services activities, indicate a positive trend. US crude inventories dropped for the first time in 10 weeks, but WTI futures remain in a mild contango for the first two months. The WTI/Brent spread narrowed, and with US refineries expected to start ramping up, it may come in some more.

Queen Anne's Gate Capital

Contagion is the real economic threat for commodities

Last week was truly one for the record books. Hawkish central bank rhetoric and strong data were completely eclipsed by bank failures and financial stability concerns. Fed funds futures have priced in almost 50bp worth of rate cuts by December and US 2yr rates have swung wildly. Flight to Quality trading rules dominate activity: lower rates, softer commodity prices and higher gold. The exception is that the DXY remains subdued, which could be a positive for commodity prices.