Company & Sector Research

Europe

Woozle Research

60% of Gucci store managers interviewed by Woozle over 1Q23 noted that they were underperforming QTD LFL sales targets, marking a severe deterioration vs. last year. Downtrading continues with lower value apparel and ready-to-wear sales trends stronger than premium handbags. Menswear sales continue to underwhelm store managers across Europe. Inconsistent trends reported for Gucci China reopening with the majority of stores indicating softer than expected footfall. Promotional activity in China maintained throughout the quarter in an attempt to attract customers to stores.

Smart Insider

Smart Insider ranked this stock +N on March 10th based on a €438k purchase from Carlo Pesenti (CEO since 2014, joined 1999) at €25.30 per share. He has made several option-related sales but this was his first open-market purchase. Pesenti has continued to purchase shares and has now spent a total of €2.2m at an average price of €25.09. Alarico Melissari (Senior Officer) purchased 2,000 shares from March 17-27th at €24.92, spending €50k, the most he has spent over his 9 purchases dating back to early 2019. With this additional buying, Smart Insider are upgrading the stock further, from +N to +1 (highest ranking).

Forensic Alpha

The level of accrued revenue on the balance sheet stands at a massive CHF 739m - this might not seem like such a big increase from 2021 level of CHF 719m, but consider that performance fees in 2022 were only CHF 269m vs. CHF 1,197m in 2021. It therefore seems odd that the accrued revenue balance increased even while performance fees declined drastically. It is also odd that the "long-term" portion (not expected to convert to cash in the next 12 months) has hardly declined at all. Investors should seek clear explanations from management, especially given the risk around the recognition of performance fees has been picked up as a "Key Audit Matter" in the Auditor's report.

Vision Research

Not as resilient as bulls believe - glass packaging is losing market share with paper cartons, plastic bottles, and aluminium cans increasingly preferred. These alternatives are cheaper, lighter and more durable. From an environmental perspective, glass has the highest greenhouse gas emissions, uses the most fossil fuel / water, and sees less benefit from recycling than aluminium. Additional headwinds flagged include declining alcohol consumption (>70% of VID sales), a deteriorating macro outlook, difficult ASP comparisons, and accounting concerns. The stock trades near all-time highs and short interest is <1%.

Robert Prather presented Vision Research's short thesis at IRF's latest Equity Shorting Conference. Click here for further details.

New Street Research

Chip design is going through a Copernican revolution, switching focus from “small is good” to “big is good”, and hybrid bonding is a key enabler going forward. Like ASML did in lithography, New Street expects BESI to strengthen its competitive position towards the domination of die attach, as it continuously improves the accuracy and throughput of its tools. They expect the shipment of hybrid bonding tools to take off this year, and to grow steadily, as the technology is increasingly adopted across all leading-edge manufacturing segments. This, along with an upcoming cyclical recovery, gives BESI’s EPS the potential to grow 18-26% p.a. over the next 5 years.

North America

Off Wall Street

Investors looking for short ideas with exposure to tightening credit conditions might consider current OWS recommendation EAT (TP $23; 40% downside), which has two tranches of senior notes totalling $650m that are set to mature over the next 19 months. The company is likely to have to refinance both notes at less attractive terms, which will impact profitability beginning in FY24. Given OWS’s expectations for EAT’s operating margins to fall towards 1-2% over the next few years, the higher interest payments should further pressure the company’s razor thin margins, potentially creating additional downside for shares.

The Retail Tracker

Investors taking the long view, to the back half of the year, will likely be well rewarded - Gap brand is already showing improvements, many of which The Retail Tracker began to note during holiday but became more evident with spring sets. The same is true for Old Navy, which was in worse shape. Deliveries are timely and sets look much more cohesive. The core assortments at Banana and Athleta are still selling well, it is just the fashion hits and new colours that are problematic. This is fixable. At the very least a stable Banana and Athleta, improving Gap and Old Navy, and a good CEO choice should allow the stock to appreciate to the teens by summer.

Quo Vadis Capital

Stock soars on revenue, earnings beat - after two years of the share price moving sideways despite consistent upward revisions to earnings, John Zolidis thinks these results could be the event that sets off a round of valuation expansion and vaults the name firmly back into the momentum camp. His model is generating both EPS and FCF per share above $20 by FY26 (vs. FY23 ~$12 for EPS and $10 for FCF). A P/E of 30x (justified by ~29% EBITDA margins and vs. a ten-year average P/E of >33x) suggests a $600 per share value by early 2025. John remains bullish the stock and would look to add on any market weakness.

Badger Consultants

Profitability keeps getting pushed out, which is a problem because growth is slowing and while INSP currently has a monopoly in its business, there is competition on the way. Tom Chanos notes that there are currently 20+ companies working on drugs for sleep apnoea; if any one of those companies breakthrough with a drug that is safe and works, INSP will be out of business overnight. By the time INSP can earn $1 per share, assuming it can, top line revenue growth will most likely be <20%. Why would anyone want to pay 240x earnings for a company that earns $1 growing at 18%?!

Foveal Research

Dr Amit Roy remains concerned over the added benefit of TIGIT to established PD1 therapy for MRK and GILD / RCUS. As expected, the street’s expectations over MRK’s TIGIT in cancer was misplaced again, as it failed to beat chemo in later line lung cancer. GILD / RCUS 1st line TIGIT data also appears equivocal with large imbalances in baseline characteristic and an underperforming PD1 arm in high PDL1 expressers. Moreover, the TIGIT + PD1 response of 41% still falls short of response rate seen with Keytruda alone. Amit also remains concerned about MRK’s prospects in first line lung, with, again disappointing response rate of just ~33% in patients naïve to PD1 therapy.

Insight Investment Research

The STB approved CP’s acquisition of Kansas City Southern which will lead to the creation of Canadian Pacific Kansas City (CPKC) on 14th April. Robert Crimes expects extensive revenue synergies from the only single-line railroad to link Canada, US and Mexico. He considers CPKC best positioned to benefit from cross continental American trade that has grown notably strongly since the USMCA in mid-2020. Robert estimates total revenues +4.6% CAGR (volumes +1.6%, prices +3.0%) and EBITDA +5.7% CAGR in 2024-50E. His DDM based TP is C$218 (+110% upside) which implies an EV/EBITDA of 25.9x in 2024E, reducing to 16.1x in 2030E given high EBITDA growth.

New Constructs

Street Earnings are higher than New Construct’s Core Earnings for 339 stocks in the S&P 500 with 186 companies overstating EPS by >10%. One of the worst offenders is CARR, where the difference between Street Earnings and Core Earnings is $1.76/share, or 76% of Street Earnings. The company’s GAAP Earnings Distortion is even higher at $3.54/share. CARR’s Stock Rating is Very Unattractive, largely due to its low ROIC of 4% and the expensive valuation of its stock. Despite trading at $45/share CARR has an EBV, or no-growth value, of -$16/share. Low ROIC and an expensive valuation also land CARR in New Construct’s Most Dangerous Stocks Model Portfolio.

Valens Research

NVT’s products are the vendor to the “electrification of everything” movement and it is a market leader of its segments, with products ranging from electronic component enclosures to thermal management solutions that protect wiring. The firm continues to add products to its portfolio to serve the electrified smart infrastructure movement through both organic growth and a smart roll-up strategy. As it continues to gain wallet share and solidify itself as a smart infrastructure investment vendor, NVT has a massive tailwind to expand profitability.

Alembic Global Advisors

Hassan Ahmed forecasts MEOH cumulatively generating >45% of its current share price in excess cash flow over the next five years. The recent higher methanol price regime is sustainable throughout the year on the back of cost curve support. Beyond 2023, Hassan expects limited new methanol capacity builds, with demand growth outstripping supply growth and global utilisation rates tightening. He raises his 2023 & 2024 EPS estimates from $3.05 to $3.45 and from $4.05 to $4.60, respectively. His 12-month TP is increased to USD60 (from USD40), reflecting the start-up of Geismar 3.

Global Mining Research

After several years of market speculation TECK is set to spin off its coal business. The Canadian mining group plans to create via a complex scheme of arrangement the jettisoning met coal on the one hand and keeping the cash flow on the other. Financial markets and media are split. Clearly, some have called the move a positive one, while others use terms like “climate placebo” and “greenwashing” and “have your cake and eat it”. Having examined the proposal in detail, GMR is not in favour of the move. If anything, it simply brings to the fore TECK’s reliance on coal. That aside, as a base metal play TECK isn’t cheap vs. peers.

Japan

JapanConsuming

Supermarket sector under unprecedented strain

With food inflation exceeding 8% in December, prices have become the focus for all supermarket retailing. This is good news for those that are set up for price competition but it presents a serious challenge to the majority of chains. Without some relief from inflation and settling of consumer worries, 2023 could prove a watershed for the supermarket sector. Click here to continue reading and for access to the rest of the stories in this month's issue of JapanConsuming, the essential monthly analysis and data update on Japan's retail & consumer markets.

Emerging Markets

RedTech Advisors

ByteDance passed a significant milestone in RedTech's latest survey, capturing nearly 33% of estimated ad spending. However, peak short video, tougher competition and tougher regulation (both domestic & overseas) complicates the story. While growth usually trumps uncertainty, ByteDance is a more mature company than it was and it will only get harder to generate the kind of breakneck growth that investors like to see. The upshot of all this is that the optimal window for an IPO is likely in the next 12 months. Unfortunately for the Chinese tech giant, while it was eyeing a valuation of ~$400bn in 2021, in the current environment RedTech believes it would be lucky to get $300bn.

Hedgeye

The most well-communicated beat in TME's history happened last week and it wasn't impressive. That is according to Felix Wang, who says the market is pricing TME as a high growth company which it is certainly not. 2023 will be no different. The stock is way ahead of itself (up >75% since Q3 earnings) even though the revenue decline in Q4 improved from 6% to 3%. Big whoop. The huge lift from the new music albums (Jay Chou, BLACKPINK, etc) will dissipate in 1Q23. The profitability gains in 2022 is mainly due to a 60% decline in marketing costs (ex stock comp) but that bottomed as a % of revenues. Felix believes TME does not deserve to trade at a forward P/E multiple higher than 10x.

Radio Free Mobile

The empire breaks up - shareholder value has little to do with Alibaba’s decision to reorganise and much more to do with providing the state with better visibility and control over the large range of its activities. This is a very different environment from the one that the group enjoyed during its glory years, and it now must adapt to ensure that it can still operate to its full capacity. On a SOTP analysis, it is easy to get to HKD140 per share but Richard Windsor suspects that Alibaba’s return to the good books of the state and an economic bounce could push it much higher.

AlphaBox Advisors

Bloomberry owns and operates integrated casinos in the Philippines. It has strong fundamentals supported by robust domestic demand and accommodative local regulatory environment. Its under-construction casino, Solaire North, will likely commence operation by early 2024 and will significantly boost its capacity in the non-VIP segments. That along with an expected stronger resumption in foreign visitation going forward should help the company post pre-pandemic level profitability. The stock is up 25% since recommendation (Dec 22). Trading at a 2 year forward P/E of 10.3x and 7.6x forward EV/EBITDA, the stock still has an upside potential of 35%-40% in 12-18 months.

Copley Fund Research

Tobacco back en vogue?

After a multi-year decline in investment EM Tobacco stocks are turning a corner - Steven Copley notes that no other industry group is so underowned vs. its own history whilst also capturing positive rotation among active EM fund managers. Fund level activity between 30th Apr 2022 and 28th Feb 2023 highlights the widespread nature of the allocation shift. All Style groups saw investment levels rise, with 16 funds opening exposure to Tobacco vs. 1 closing over the period. GQG Partners EM Equity, Virtus EM Opportunity and BNY Mellon EM Income were among the larger buyers. ITC and KT&G dominate the holdings picture on a stock level, owned by 14.8% and 7.8% of managers, respectively.

Galliano's Financials Research

LatAm Banks

Victor Galliano examines key balance sheet ratios of the LatAm Banks looking into liquidity, credit quality and capital adequacy, at a time of investor nervousness and concern - Victor likes Bradesco and Bancolombia as value plays with Banco de Chile, BanBajio and BanRegio as high quality names. His bearish picks are Banorte (even though it is a quality name in terms of capital and credit quality, it is more exposed on the importance of its securities portfolio) and BCI, despite its strong liquidity, with its small US (Florida) banking subsidiary.

Macro Research

Developed Markets

Willis Welby

UK: Economies are not following the misery script

The Consumer Squeeze narrative still looks wrong to Tony Willis and Julius Welby. They’ve tweaked the maths to confirm that from pre-Covid there’s been no consumer squeeze; consumers won first by quite a margin, and prices have since just caught up. Indeed, the markets are quite miserable, expecting a cyclical recession or one brought on by central bank rate hikes. Tony and Julius would characterise it differently: central bankers try to judge what glide path of expansion is consistent with inflation staying under control, and recent data suggests this path may be higher than many people expect. If correct, there’ll be less need for an increase in short rates, and long rates should rise a bit after falling over the last month.

Belkin Report

Portfolio change in the face of a credit crunch

Bank failures are causing a credit crunch which is probably just starting, exclaims Michael Belkin. Anything that depends on easy credit is vulnerable. The credit crunch should also produce a psychological shift in which consumers and companies retrench and delay or suspend purchases, developing a recession. Reduce long exposure and shift out of tech, financials, energy, industrials, materials and real estate into consumer staples, utilities and healthcare, all three of which Michael expects to take FAANGMT’s place when it bites the dust. For hedge funds, close long positions and short tech and financial stocks.

CrossBorder Capital

US: The Fed is engaging again in QE

Despite being far from the consensus view, Michael Howell believes that the world’s central banks, led by the US Fed, appear to be starting a QE program. The issue is that many pundits focus solely on the Fed’s treasury holdings as their criterion for QE, but this angle is both fussy and wrong because QE should be a measure of the new liquidity injected into money markets, whatever the ultimate efficacy or impact of the cash injection. With Michael’s calculations of a rising shadow monetary base and a stable-to-higher collateral multiplier, he remains constructive and broadly positive about the future path of Global Liquidity.

HCWE & Co.

US: Don’t credit the Fed for the dollar’s strength

The idea that the FX value of the dollar is chiefly driven by interest rates is at best an exaggeration, claims David Ranson. Causation runs rather from the USD to interest rates, and it would be unsafe to assume that further tightening of Fed policy will strengthen the dollar. There is another, less-watched, variable that correlates with and explains the USD’s back-and-forth between weakness and strength: that is, the implied volatility of the FX markets. It is this, rather than the Fed, that explains the USD’s sudden advance in 2022, its peaking about six months ago, and its recent decline.

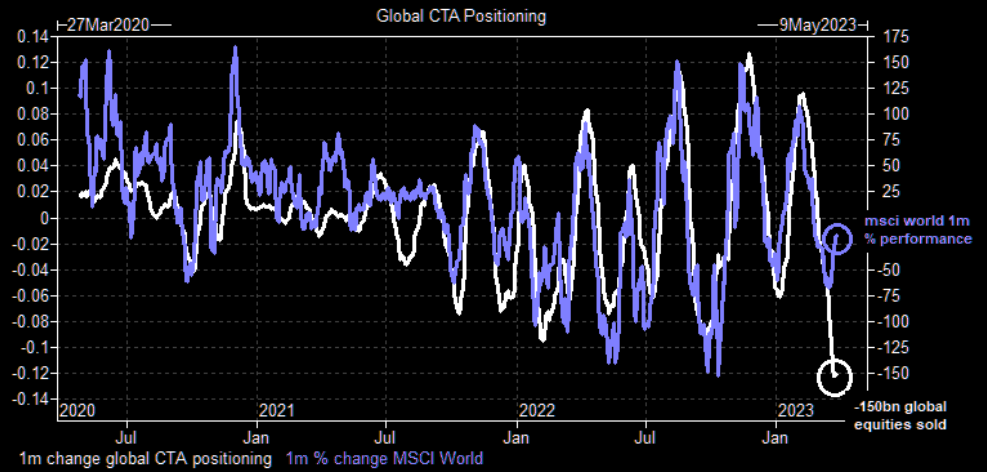

Ollari Consulting

Asymmetrical again

Christophe Ollari comments on the equity vol reversal, meaning that the systematic crowd can potentially step in again. This is the largest risk for equity bears – the risk is asymmetrical again. Christophe will never repeat it enough: CTAs have given the tempo and triggered all the major squeezes of 2022. 2023 has been nowhere different: covering their legacy equity short late 2022/Jan 2023 to go into SVB max long equity + max short FI + max long Euro. With the end result we all know… The current state of affairs show a short positioning that has reached mean reversion levels. Estimated projects are that CTAs will be big buyers of equities in flat/up scenarios. 1 week: flat 23bn to buy, up 63bn to buy, down 13bn to sell. 1 month: flat 41bn to buy, up 157bn to buy, down 77bn to sell.

AAS Economics

Australia: Remaining very defensive

The monetary headwinds continue in Australia and Frank Shostak remains entrenched in stage 1 of the Business Cycle for the upcoming quarter, remaining very defensive. The concern is that these headwinds may continue into H2/2023 as pressure mounts due to further slowing in the money supply, and further rate rises may be due, putting further downward pressure on the money supply growth rate. On a relative basis, Frank’s Aussie equities asset weighting slips to UNDERWEIGHT, compared to maximum overweight for global equities. He is also OVERWEIGHT domestic government debt and MAXIMUM OVERWEIGHT global government debt (hedged AUD).

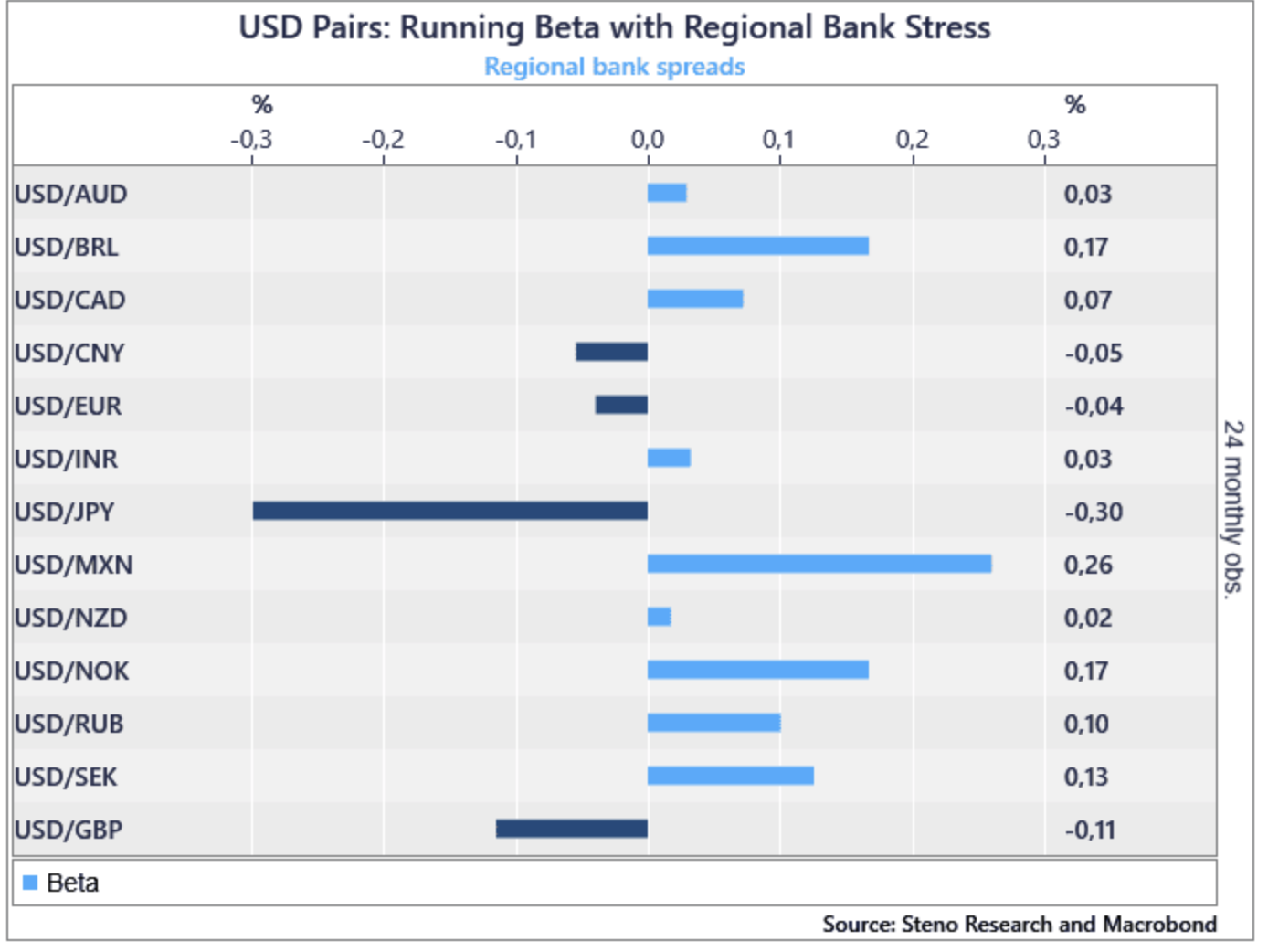

Steno Research

Positioning yourself amongst the banking frenzy

So what happens in the FX and equity space when banking stress accelerates? There is one clear winner in the FX space, JPY, as the rates spreads will be closed between Western currencies and the JPY, while the BoJ gets a once in a decade window of opportunity to widen the YCC gap without harming local bonds too much (see chart). Meanwhile, in equity space you can expect Consumer Discretionary and similar high duration bets to outperform when the central banks need to step in with liquidity and rate cuts. Energy is also a sector that suffers big time from banking stress, and Real Estate and Financials will obviously be big losers.

Emerging Markets

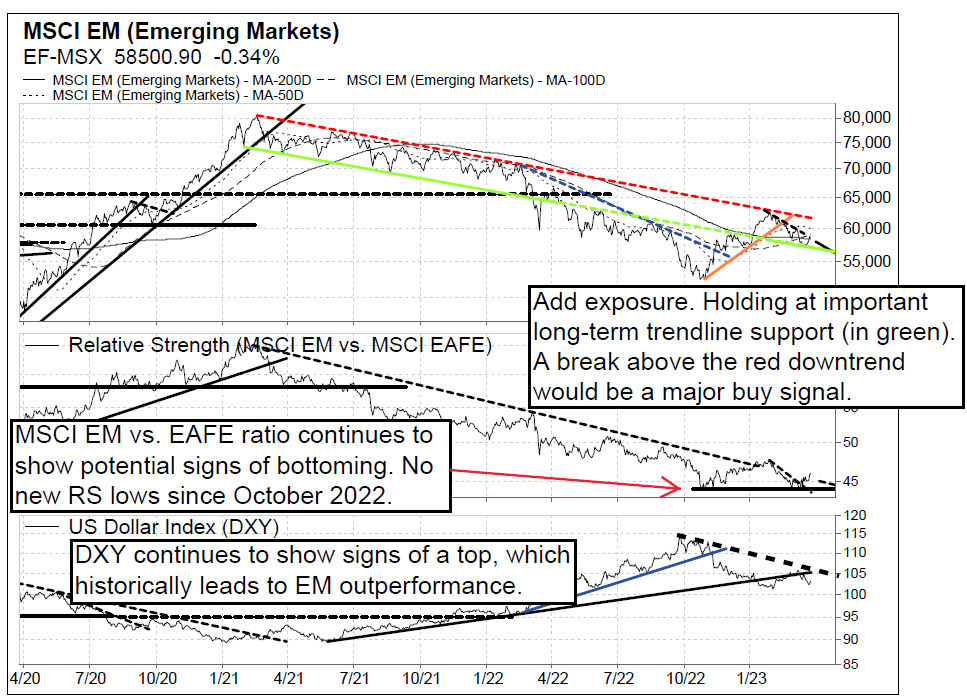

Vermilion Research

MSCI EM 2-month downtrend reversal at support

In Vermilion Research’s February EM Strategy, the team mentioned they were buyers of the MSCI EM (EEM-US) on a pullback to the 50-day MA. The pullback went a bit deeper but managed to hold at their $37.50 line-in-the-sand. The EEM-US now displays a bullish 2-month downtrend reversal -- add exposure. Additionally, the MSCI EM index (local currency) is holding at an important long-term support level (see chart, green trendline). Signs continue to point to a topping U.S. dollar (DXY), and a declining DXY has historically resulted in EM outperformance relative to EAFE. As long as the DXY remains below $105.50, the team expects to see the MSCI EM form a relative strength bottom (vs. EAFE).

Horizon Insights

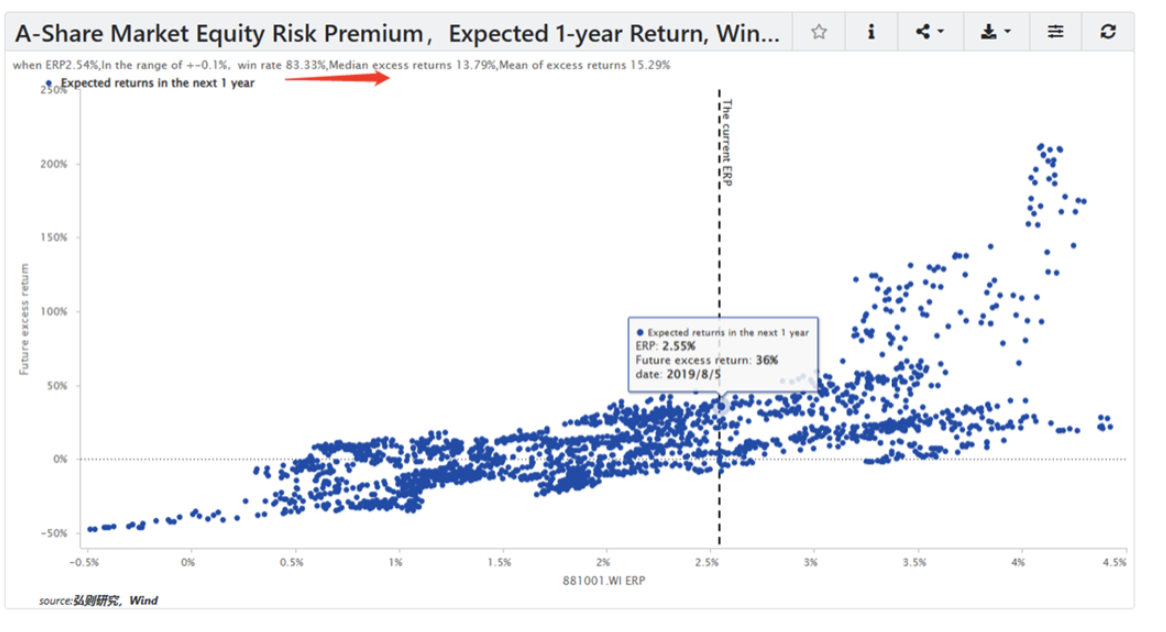

China: The volatile nature of the A-share market

Being volatile in nature, the A-share market displays a robust positive relationship between market valuation change and market investment returns. That is to say that valuations drive the A-share market's investment return in the short run, while in the long run it is company earnings that determine the market performance. With China's economic recovery, company earnings will start to bottom out in Q1 of 2023. With benchmark index valuations hovering around middle-and-low ranges, the A-share market appears an attractive deal with limited downside risks. With the equity risk premium of around 2.5%, there is a fairly high possibility (83.3% probability) that the market will deliver a 13% excess investment return in the next 12 months (against the 10-year treasury yield).

High Frequency Economics

A dearth of high-return investments dooms China to disappointing growth

Since the turn of the country, China’s economic growth has been propelled forward by economic spending. However, Carl Weinberg notes that the roster of viable investment projects is fast becoming depleted. There comes a point where the rate of return on capital falls below the rate of interest, which is where China has been for a while, investing under direction from the state in low-return projects. The strategy has also pushed China right onto the verge of a debt trap, and the obvious way out – encouraging households to save less and spend more – would be a hard sell tactic in China. This is a formula for slowing economic growth, expect GDP growth of 3% or less.

MES/Falconridge Advisers

China: He who controls the Eurasian continent controls the world

We are seeing China do exactly that in moves it has recently made in Russia and the Middle East, remarks Paul Markowski. The latest headlines include the peace deal it is brokering between Saudi Arabia and Iran and the current visit of Xi Xinping to his Russian minion Vladimir Putin, who depends on energy sales to China and India to bolster his cash needs, and needs Chinese weapons to bolster what it is receiving from another partner in the Axis of Evil. With Pakistan and Afghanistan helping its effort to grasp South and Central Asia, China is on the move.

View from the Peak

China: Trade, not own

The breakup of Alibaba Group marks the grasp of Xi Jinping’s common prosperity agenda. Investors can be rich, but not too rich. Companies can innovate but with Beijing first. The government is taking it too far, sapping the culture of innovation that was a driver of China’s technology rise since 2012. Its tech influence is now restricted within Asia. Its geopolitical realm is diminished greatly – the Belt and Road Initiative is now barely mentioned outside of debt renegotiations. To structurally invest in this market is to believe an intervention can support equity multiples. Paul Krake notes this can be true in some cases, such as climate infrastructure, but there is a big difference between government support and interference. Chinese equities remain a trade and nothing more.

Greenmantle

Argentina’s woes could be medium-term bullish

Niall Ferguson discusses Argentina’s deepening economic crisis as the government forces public entities to sell their dollar bonds for pesos, increasing intervention in the FX market at the expense of bond holdings. Annual inflation is over 100%, with February's inflation at 6.6% and core inflation at 7.7%. Inertial inflation is difficult to control, and the worst drought in a century worsens the situation. The IMF will revise its agreement to accommodate the harsh reality, favouring Peronists. The outlook for 2023 is bleak, with more recession and inflation. Yet Niall sees reasons to be bullish in the medium term as the situation makes political change towards a more market-friendly government all but certain.

Emerging Advisors Group

Peru: Don’t be scared away

Politics are a mess and have impacted local sentiment and activity, visibly disrupting domestic consumption and investment in the last six months. However, Jonathan Anderson stresses that there’s no change in Peru’s underlying fundamentals. It still remains an export outperformer by regional standards with relatively solid external and fiscal balances. Jonathan is agnostic on markets but sees no reason to run away. The country isn’t a must invest tiger growth economy or an imperative FX/yield play but, assuming political tensions don’t spiral further out of control, he sees it performing in line with broad EM.

Commodities

Marex

Corn weakness spills over into soy markets

The Marex team believes there’s been a ‘lazy long’ in the corn spreads: people didn’t want to commit to a flat price, brought spreads instead and those positions have come under pressure on this move. There’s been solid volumes so a lot of the length has probably been cleaned up already, but the chart does not look great by any means (see chart). Market response over corn weakness has spilled over into soy, but the Marex team aren’t seeing an abundant new crop balance sheet. Be a bit wary of taking too much risk right now, vol levels making options are still the attractive way to play the market.

PRC Macro

China Iron Ore: Sell in May, come back in October

Iron ore prices in China are a function of steel production in the short-term, credit growth and restocking in the medium-term and property new starts in the long-term, explains William Hess. He still expects a secular decline in the long run against a backdrop of falling property new starts, voluntary steel production cuts and substitution from increased scrap recovery. However, iron ore is currently oversold. Production rates are still relatively high and near-term credit growth will provide a floor for demand. William expects prices to rebound to USD 140 per metric ton before a major retreat to 90-100 per metric ton in late May.

Metals Focus

Palladium: A weak outlook, but expect some recovery

Palladium’s medium- to long-term outlook remains weak as ICE loses market share to EVs. This is already weighing heavily on investor sentiment and, in turn, the price. However, expect to see a recovery from the recent decline, driven by healthy fundamentals this year. A number of upside risks remain, including Russian sanctions, that could provide palladium with a more blustery second wind, even if only on a short- term basis. However, a worse than expected outcome from the auto sector poses a key downside risk to prices.

CPM Group

Why solar demand will not use all of the world’s silver

Recent suggestions that silver demand for solar panels will use 85% - 90% of the world’s silver supply have spread like a plague in the silver investment community, claims Jeffrey Christian. Questions have arisen regarding whether there is enough silver available to keep up with the amount of silver necessary for expected increases in demand in solar energy. In his latest video, Jeffrey discusses the economic realities of the silver market that will serve to prevent this, including why the projections for solar power demand may be overly bullish, the emergence of new technologies, and the significant amount of above ground refined inventory available for secondary supply.

Click here to watch.