Company & Sector Research

Europe

the IDEA!

Although the IDEA! considers some parts of the arguments used by TWKY to support its upward guidance revision more credible than other parts, they believe it is not just based on wishful thinking - the tailwind the company has created for itself by means of last year’s rationalisation programme will last for at least another 2-3 quarters and any additional support from its commercial performance will provide further impetus. While the IDEA! still finds it hard to believe that management will find a solution for Grubhub in the near term (but expects a 'real' share buyback if they do!), at least the healthy balance sheet gives TKWY time to wait for a better opportunity.

Iron Blue Financials

An Iron Blue score of 27/60 (+2 Y/Y) is top quartile (fertile ground for shorting). Red flags include: 1) Industry leading use of stripped out restructuring and other one-off costs. 2) A change in the calculation behind the headline LFL sales growth metric to now include hyperinflationary countries (Turkey, Argentina & Iran) up to 26% p.a. 3) A seeming mismatch between bad debtor provisions at a decade low and overdue receivables at a decade high. 4) Reduced disclosure around the goodwill impairment test inputs. 5) Additional risks commentary re. Russian operations (5% of 2022 group sales).

Alembic Global Advisors

As management guides to a 1Q23 EBITDA figure significantly ahead of consensus, Hassan Ahmed expects to see positive earnings revisions and share price outperformance throughout the year. Nearly 75% of company revenues come from APAC and EMLA, where both regions experienced higher costs and weaker demand in 2022. With China reopening, and with natural gas prices currently significantly lower in both Europe and the US, Hassan expects last year's earnings headwinds to become tailwinds. He increases his 12-month TP from €35 to €47.

ROCGA Research

ROCGA’s proprietary Cash Flow Returns On Investments based platform helps identify and value companies. UMI has been identified on an enhanced GARP screen. The company has been modelled, valuation back tested, and projected forward using expected earnings. It looks undervalued using the systematic DCF analysis, as well as historic valuation ratios. A total of 123 companies appear on this screen and warrant further investigation. ROCGA currently covers c.2000 companies across Europe and the US. More details on ROCGA’s systematic and interactive valuation tools can be found here. A free trial is available on request.

New Street Research

New Street takes advantage of recent share price weakness post WISE's 4Q23 update to upgrade the stock to Buy - whilst TPV was a touch light, they think the market's focus should be firmly on the new steer for NII which drives material upgrades to EBITDA (40% in fiscal 2025). The market has been contorting itself to keep near-term EBITDA margins at ~20% (as per mid-term guide) when in reality it will be nigh on impossible to reinvest a significant portion of NII gains on any sort of near-term basis. Along with street upgrades, potential MSCI inclusion (May) is another catalyst. TP increases to £6.75.

Willis Welby

Willis Welby wonders if the ebb and flow of revisions might be obscuring the bigger picture at CAP - the Altran deal was a master stroke and on top of that it feels like there is a secular change in margins that will stick. Maybe any material slowdown will be an issue, but the implied to Y3 EBITM ratio of 49 already seems consistent with that happening. Willis Welby thinks the market is fighting historic battles and does not find it hard to envisage CAP's share price back at its late 2021 peaks of €220 (35% upside).

North America

Behind the Numbers

POST’s last Qtr saw pricing up $231m vs inflation costs up $157m adding 86-cents to EPS of $1.08. Much is egg-related. After Easter, eggs have fallen to $1.62/dozen from $5.33 in late Dec. BTN expects pricing to drop. Earnings are also helped by cutting marketing as competitors are spending more. POST is a roll-up story but its borrowing costs on new money is 8-9% and even with pricing ROI is ~6%. BTN estimates a 5% ROI on the latest pet food deal. Net debt is 5.1x forecast EBITDA and that assumes all this pricing holds. Losing $100m of pricing that exceeds inflation would push debt close to 6x EBITDA.

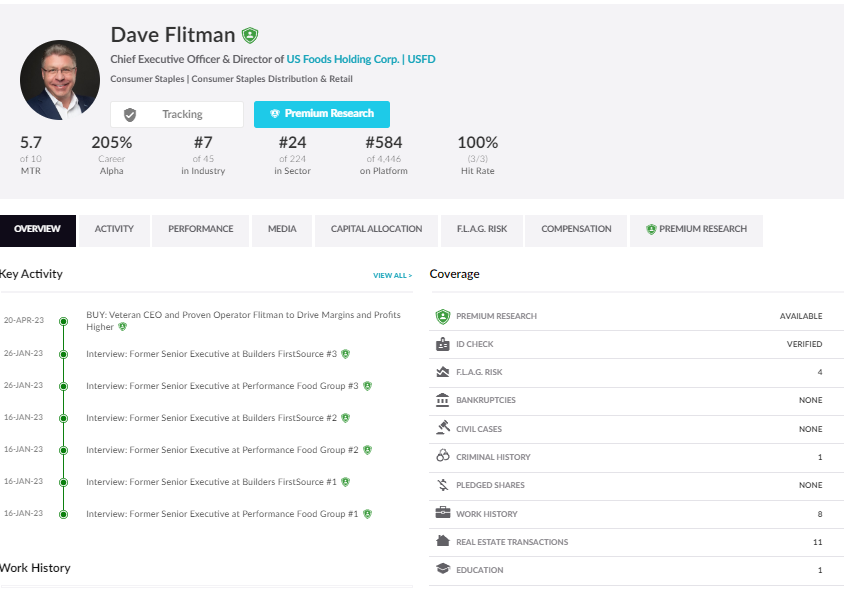

Paragon Intel

New CEO David Flitman to drive margins and profits higher - former colleagues interviewed by Paragon described Flitman as a strong operator who excels at driving costs out of businesses. He is a rigorous, data-driven, and profit-focused executive who quickly understands the largest levers to pull to improve performance at distribution businesses. He drove significant shareholder value at BMC and its merger partner Builders FirstSource where the combined stock performance of the two companies outperformed the S&P 500 more than two-fold.

Housing Research Center

2Q23 results smash expectations - Alex Barron believes FY23 will prove to be the trough in earnings. His EPS estimate for this year is $12.25 and sees it heading towards $18.00 in FY24. Alex considers DHI to be one of the two strongest companies in the industry and therefore deserves to trade at a much larger premium to the group in either P/E (currently at 8.0x based on his 2023 forecast vs. 14.3x for the group) or P/B (1.5x vs. 1.4x for the group) than it is currently trading at. He increases his TP from $117 to $167 (55% upside).

Cmind

At the end of March, Cmind predicted the 1Q23 earnings for 573 firms within the financial service sector. Their model predicts an 84% probability that ALL will miss street forecasts. Besides the sector-level volatility, they find that its financial metrics such as Cash/Operating Profit, Current Assets/Capitalised Expenses, and Receivables - Estimated Doubtful are excessively high when compared against its peers. Additionally, the sentiment extracted from the analysts participating in previous earnings calls has been consistently negative over the last several quarters. ALL is scheduled to release its earnings on 3rd May.

Holland Advisors

It’s ROE & long-term growth rates are as good as Coca-Cola’s, but CACC never trades on more than 10x EPS. Today’s outlook is even stronger and yet bizarrely the PE even lower (8x on Dec 22 earnings). CACC should be looked at closely by those that seek wonderful compounding. Instead, Andrew Hollingworth expects many investors will be quick to dismiss the idea of it as a good investment given that it lends money to sub-prime borrowers to buy cars. In this report, he provides a compelling argument as to why that decision would be a mistake.

BWS Financial

Purchases Spectrum Pharmaceuticals in an all-stock transaction that adds ROLVEDON to its product portfolio - despite the negative market reaction to the news, Hamed Khorsand is constructive on the deal as it diversifies ASRT's product portfolio and creates a larger organisation that can benefit from further M&A. The acquisition is expected to be accretive to ASRT's earnings and FCF in 2024. Hamed believes this is achievable based on ROLVEDON achieving sales materially higher than the current street consensus. The stock is up c.70% since he turned bullish in May 2022, but still offers 60% upside to his 12-month TP of $8.00.

Foveal Research

In newly published data from MRK / MRNA’s PD1 + mRNA cancer vaccine trial at AACR last week, headline efficacy may be flattered by Keytruda alone control arm underperformance by c.11% compared its historic phase III performance, with the vaccine combination arm performing similar to previous monotherapy Keytruda alone trials, suggesting the phase III confirmatory trial may have a higher than expected hurdle to beat.

Gradient Analytics

Initiates coverage with a negative outlook due to a variety of fundamental concerns and earnings quality issues including: 1) Demand headwinds in defence and industrial businesses are pressuring other units. 2) Margin targets appear disconnected from recent performance. 3) Inventory levels have diverged from near-term demand estimates. 4) Outsized growth in receivables. 5) An unusual spike in other current assets. 6) Trades at a significant premium to its closest industry peers.

Badger Consultants

The true economic returns on capital are below the cost of capital and it is getting worse not better. Private equity are turning from buyers to sellers of data centres. DLR trades at close to 90x this year's earnings and is burning $230m cash per month! It is highly leveraged with $18bn in debt and needs to do a combination of asset sales, dividend cut and an equity raise. Current data centres are being put up for sale at cap rates in HSD. At a 8-10% cap rate, DLR is a $23-$45 stock, implying 50-75% downside. The current bullish narrative is a far cry from reality as investors are going to find out the hard way.

Verbatim Advisory Group

Q3 trends are strong as net new customer business grows - 100% of respondents to Verbatim’s latest channel checks tell them that they are meeting their internal sales targets. The outlook for Q4 is also positive due to ongoing price increases and a strong sales pipeline. FY23 is expected to be up significantly Y/Y (by 20% on average). TEAM continues to gain market share (particularly from ServiceNow) as they maintain best-of-breed products and customer experience. Respondents expect project management software growth to be dramatic over the next 12 months as a large push for the Jira line of products helps drive big licensing sales.

Trivariate Research

Don’t use valuation as a reason to avoid AI stocks

Portfolio managers should use AI names as hedges against other growth stocks - despite the strong YTD move in Trivariate Research’s AI-basket, it is still 5 turns cheaper on price-to-forward earnings and 1.5 turns cheaper on EV-to-forecasted sales than the growth universe excluding AI. Every PM needs some hyper growth exposure in their portfolio, but this universe currently has very low company-specific risk vs. its own history. Trivariate recommends assessing the correlation of each portfolio stock against their AI basket to make sure you are not under-weight.

Emerging Markets

Primaresearch

Primaresearch reviews 1H23 results and cuts their forecast FY23 diluted HEPS from 1,267cps to 1,137cps (+8.3% Y/Y), with a DPS of 633cps (+5.4% Y/Y). They lower their 12-month TP from R230.00 to R210.00 on an exit forward P/E of 14.5x. The TP is in line with their DCF valuation of R209.59. While SHP is well-positioned relative to the other food retailers, Primaresearch thinks the likely impact of loadshedding challenges in the period ahead is not fully reflected in the current share price. If loadshedding intensifies to Stage 8, SHP’s diesel costs could increase to R1.9bn, this would amount to 17% of its operating profit. They maintain their Sell recommendation.

Silk Road Research

China Autos: Price war talk overdone

A barrage of headlines of OEMs and dealers cutting price and offering promotions has led to the perception that there is an intense “price war” ongoing in the Chinese automotive market. However, SRR’s analysis suggests MSRPs have been relatively stable YTD, with the vast majority of recent announcements reflecting limited promotions designed to reduce inventory. SRR also flags increased downside risk to 2Q production expectations (more likely to be flat Y/Y than industry forecasts closer to +20% Y/Y), while recent data indicates that demand is picking up. They prefer ICE over NEV exposure near-term given better inventory / pricing dynamics.

Hemindra Hazari

The backdoor entry of Uday Kotak into the board of directors of KMB after he steps down as the CEO at the end of the year should be recognised for what it is, namely, a method of exercising control over the bank without being saddled with executive responsibilities. This decision also reflects poorly on the board of directors for not taking CEO succession seriously for two decades. When a prominent entity in the financial system has a history of disdain towards the regulators and finds loopholes to permit the founder to exercise control, stakeholders should be concerned.

Aequitas Research

Looking to raise US$1bn in its upcoming Hong Kong IPO - JDP has been growing via acquisitions which has resulted in strong sales growth (99.6% CAGR FY20-22). However, its surging finance costs have brought the firm to adjusted net loss territory. With a net debt to equity ratio of 77% in FY22, it could potentially put a ceiling on its future expansionary plans (or the firm will likely need to tap equity markets post-listing for further financing). As much as JDP has made attempts to diversify away from its parent, it remains largely dependent on JD.com. Also, its pre-IPO shareholders don't appear to have subscribed to a lockup undertaking.

AceCamp International

More derating risks for Chinese power device vendors

Latest channel checks indicate that AceCamp’s negative thesis is starting to play out - sees another 25-40% downside risk for stocks including StarPower, Silan and Macmic. 1) Automotive IGBT price cuts - expects the global IGBT wafer supply/demand ratio to rise from 101% in 1H23 to 109%/137% in 2H23/1H24 and 131%/117% in 2H24/2H25. 2) Expects another 5-10% ASP erosion for commoditised power devices in 2H23 due to the aggressive power capacity expansion of Chinese tier 2/3 foundries. 3) PV IGBT price hikes are unsustainable - expects oversupply in 2H23 and an industry shift to SiC at a faster pace in 2024/25.

Arete Research

Latest reset to FY outlook represents the last cut - the sales recovery into 2H23 now looks far more realistic (+20% vs. 1H23). The growth outlook for 2024 and 2025 is on track to return to the 15-20% CAGR target as N3 builds up to reach $25-30bn in annual sales (although near-term depreciation headwinds will temporarily weigh on margins). TSMC is also committing nearly $50bn in cumulative capex to build out overseas fabs which should lift some of the geopolitical concerns that have weighed on the shares. TSMC trades at just 13.8x earnings, a 30% discount to the SOX. For a dominant franchise that offers superior growth and returns to the wider sector, this looks very harsh.

Macro Research

Developed Markets

Economic Perspectives

UK: Recession denial

The recent improvement in the GfK measure of UK consumer confidence, from -45 in January to -30 in April, is welcome but does not signify that recession will be avoided this year. The tightening of monetary conditions operates with a lag. The greatest cumulative impact of higher borrowing rates – and the tightening of lending conditions following an exodus of bank deposits, as customers rebel against puny savings rates – has yet to be seen. Disappointing retail sales data for March has been blamed on the weather, but that does not explain why non-store sales volumes are still 10 per cent lower than a year ago. The noose around the neck of UK households is still tightening. Peter Warburton’s recession forecast remains.

Saltmarsh Economics

UK: Greedflation and the BoE

Contrary to popular belief, David Owen estimates that for the year, profit margins in the UK fell to a record low in 2022 as a whole. However, it was a year of two halves. As with the euro area, profit margins of UK non-financial corporations appear to have rebounded strongly in Q4/2022. A key question for the BoE is whether this margin expansion continues in 2023, or whether they bounce around their pre-Covid average. In any event, David sticks to his long-held view of the Bank Rate going over 5%.

CrossBorder Capital

What matters to investors, falling inflation or faster growth?

We are too frequently warned that a widely-predicted approaching global recession is likely to trigger a stock market sell-off. Despite these well-flagged fears, market indexes have been trading higher. In his latest report, Michael Howell argues that investors may be looking through any recession and instead taking succour from the parallel and bigger fall in expected inflation rates. Investors may be more sensitive to lower inflation than slower growth, after all.

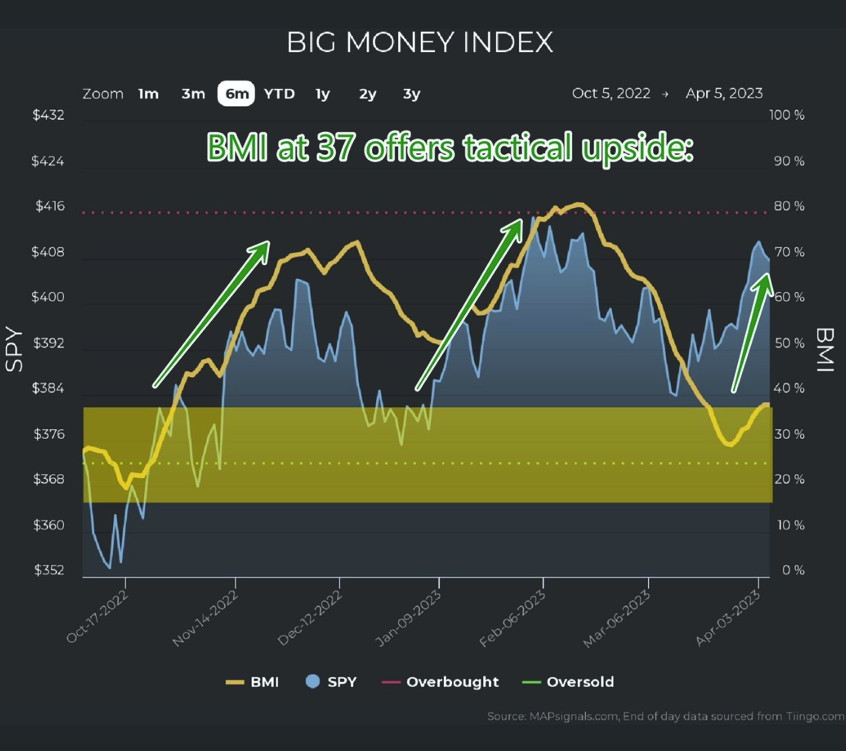

MAPsignals

Why stocks will keep going up

Alec Young points to numerous factors that will result in stock prices continuing to rise. On the matter of the Fed, he claims it’s only a matter of time until it begins easing. This will help to blunt the impact of weaker regional bank lending on the broader economy. Some investors claim valuations are stretched, but they’re missing the forest for the trees; the top 15 names in the S&P500 warrant a premium valuation, but the rest of the market is much cheaper. The Big Money Index (BMI), a contrarian indicator Alec believes to be one of the best, also says to BUY (see chart). Stick to quality, and overweight counter-cyclical defensive sectors like staples and healthcare.

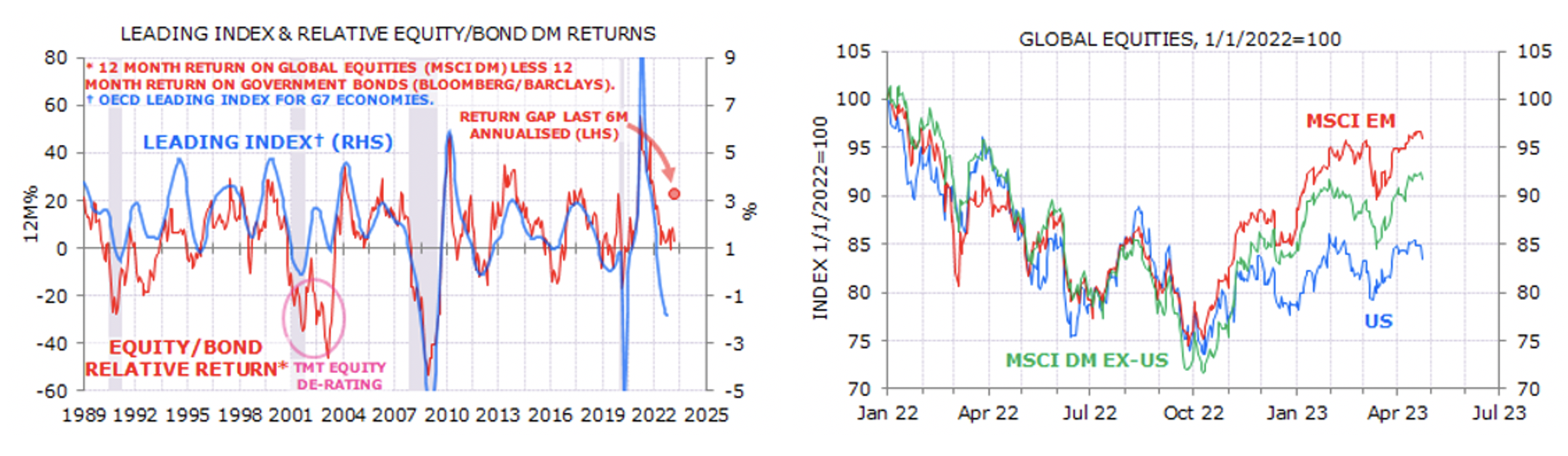

Minack Advisors

The equity rally will end when recession fears rise

Equities have been rallying for six months, which Gerard Minack points out has opened an exceptional gap between cycle indicators and the relative return on equities versus bonds (chart 1). Last year’s sell-off was largely driven by rising yields, and long-end yields seem to have peaked. What’s not priced in is a recession, which Gerard expects in the US in H2/2023. Equities don’t look far ahead, and the markets have been defying central bank tightening and recession chatter, so they could remain resilient until just a few months before the recession hits (chart 2).

TenViz

US: Sleepwalking into recession

As the US heads into trouble, Tenviz’s AI-driven forecasts have pushed out recommendations across the board. In their latest report, investors are advised to SELL economically sensitive Transports and Semiconductors, and Big Tech. Yet, as the team forecasted all along, housing is going strong and generates a BUY signal on US residential real estate (See chart). Ignore the bearish outlook on US Industrial Real Estate and BUY.

Vermilion Research

“Sell in May” another reason to favour Defensives

The S&P 500 made a high of 4169 last week, tagging the Vermillion team’s 4165-4200 resistance range. They still believe 4165-4200 will cap upside in 2023, with a reach to 4300-4325 also within the realm of possibility. Considering limited upside in both scenarios, and with the seasonably weaker "sell in May and go away" period approaching, they continue to recommend higher allocations to defensives including Utilities (XLU, RYU), Consumer Staples (XLP), Health Care (XLV, PPH), and gold miners (GDX). Downside targets on the S&P 500 continue to be at the December 2022 lows (3765) and/or the 2022 lows (3490).

WilmotML

Explainable AI and Macro based Predictions

WilmotML provides a set of predictive signals, for global equity indices, bond indices, commodities, and currencies. The team’s Artificial Intelligence based platform has been developed using their many years of quantitative, machine learning, and macro investing expertise, and provides both short-term (days) and medium-term (monthly) predictions. Their system is explainable - it links these predictions to key drivers or factors, which are combinations of macro indicators, sentiment, and price-based signals.

Emerging Markets

Greenmantle

Argentina: The next president

Niall Ferguson’s team spent the week meeting all of the relevant Argentine presidential candidates at the Llao Llao Patagonian retreat. He expects Fernandez to back out of the race soon, and the lack of viable candidates is quickly becoming an existential risk for Peronism – a positive for markets. Right-wing populist Milei may be able to gain some support in the Peronist part, but not from regional governors who are wary of his libertarian revolution; Niall expects his chances of success to be 10-15%. Bullrich’s chances continue to grow and will likely rise further as inflation and security fears undermine more centrist candidates. Niall is wary in the short-term but is optimistic that a political transition will bring the right policy mix come December.

Totem Macro

Brazil: From bearish to bullish

Whitney Baker finds herself more bullish real and local assets than at any time in the last five years. BRL is now nearly as cheap as ever in real terms, rates having moved dramatically, the credit washout happened, and growth contracted. Whitney expects to get meaningful disinflation here, further BRL strength, and a re-acceleration of commodity prices and the associated windfall, which will further strengthen the already manageable external and fiscal balances and juice earnings. The country remains the most geared play to a China recovery, which is now showing up large. Expect stocks to be as geared to falling rates as they were to rate hikes.

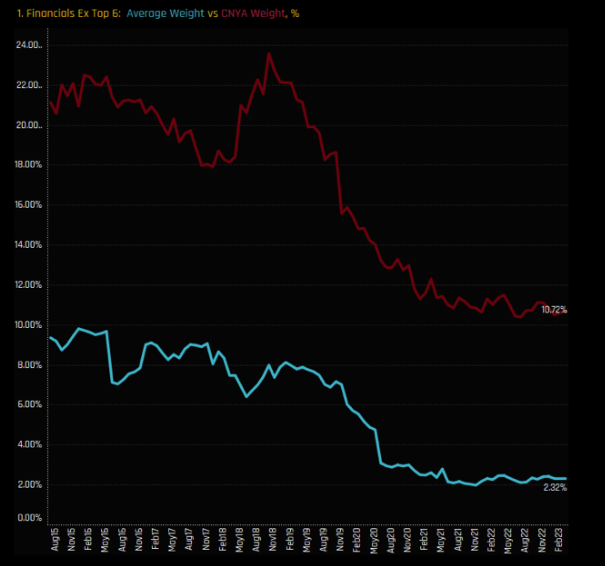

Copley Fund Research

China A-Share Financials: Out of love

Ownership levels in the China A-Share Financials sector are at their lowest ebb, driven by lack of confidence. The top 6 most widely held Financial stocks make up 5.5% of the average active A-share fund and 5.75% in the iShares MSCI China A-Share ETF, but it’s outside of this where the divergence between active and benchmark occurs. Across 83 companies, active A-Share funds have allocated just 2.32% whereas the iShares MSCI China A-Share ETF has allocated 10.72%. The message is clear – stick to the top 6 and avoid the long tail.

PRC Macro

China: A long-awaited reversal

Jerome Powell’s egomaniacal campaign against evaporating inflation will bring about sharply weaker USD and deterioration of US activity, benefitting the RMB and RMB assets, including equities. A sharp downturn would of course hit China via multiple transmission channels, but William Hess points out that a further loss of confidence in Fed stewardship in the US - not to mention the debt ceiling showdown - could begin to reverse the long-term underperformance of Chinese equities.

Teneo

Kenya: FX struggles

Hard currency shortages show little sign of easing as Kenya’s forex reserves have fallen to 3.63 months of import cover and the shilling has come under increased pressure. The central bank has long been focused on exchange rate stability to facilitate debt servicing; the overdue adjustment is compounding Kenya's current challenges. An ‘experimental’ oil import deal might merely end up postponing FX problems. The IMF has reiterated its long-standing concern that the shilling is overvalued. The Fund first got into a standoff with CBK Governor Patrick Njoroge in 2018 when it argued that the KES was overvalued by 17.5% (something Njoroge strongly denied) and re-classified Kenya’s forex regime from a floating to a managed currency.

Cribstone Strategic Macro

Turkey: An opposition win

There is loud debate about the post-election outlook for the Turkish lira following its significant real appreciation, with many arguing that a major currency adjustment is inevitable regardless of the election outcome. Michael Harris points out that this is ultimately about a combination of post-election monetary policy, and - probably more importantly - confidence. The outlook for the Turkish currency and the investment case for Turkey is binary, dependant almost fully on the election outcome. Michael expects a 50% chance of a Kilicdaroglu win, leading to a transformation in sentiment and a policy shift, with TRY ending the year close to 20 per USD, implying a significant further real appreciation of the currency.

Deep Macro

EM economies among those expected to see big gains

Jeffrey Young’s Turning Points Trade Tool (TPTT) takes the position of economic growth, inflation, and GRI factors, mapping them into one-month forward asset returns based on point-in-time data since 2004. In this latest report, Jeffrey’s equities TPTT model expects 16 out of 20 markets to rise in the next month. Turkey, China, Brazil and Taiwan are all expected to show the strongest positive gains, with composite returns of 15.08%, 11.30%, 10.21% and 10.04%, respectively. For government bonds, expect India, the US and South Africa to see the highest yield increases.

ESG

Sustainable Market Strategies

Finding real returns in artificial intelligence

Artificial intelligence has important applications for resource optimization, enabling energy efficiency, improved water management and waste reduction. Sustainable minded investors looking to gain some exposure to the AI boom should look for innovators in automation, IoT devices and digital design that serve impactful purposes. These companies are likely to benefit from AI progress and the macro context of structurally tight labour markets, nearshoring and the fiscal tailwinds emanating from the IRA and CHIPS and Science Acts.

Commodities

RW Advisory

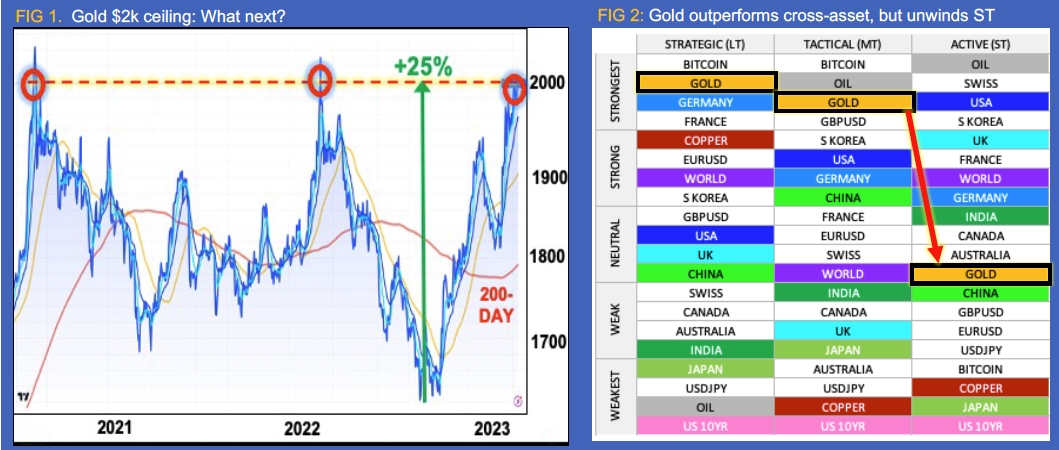

Gold at $2k, what next?

Gold to consolidate before climbing to $2,800. ST Tactical analysis warns of a sharp unwind ahead, pressured by a triple whammy confluence of price exhaustion, momentum divergence and cycle timing. However, over the LT horizon, investors are still cautious, with sentiment indicators setting up for a future buying opportunity. Gold’s more resilient and broader rising tide is found across a basket of key FX rates, led by ZAR and JPY. From a macro perspective, broad gold strength continues to highlight the necessary FIAT hedge, as global debt levels balloon. Rather perversely, central banks (CB); the instigators of this policy, are on course for a “generational high” of gold purchases. Furthermore, CB gold purchases are now significantly outshining USTs.

Grey Investment

Nerves of steel

The NYSE ARCA Steel index has been rangebound for 14 years between ~500 and ~2,000. It has been testing the top end of the range for almost two years, making no progress since reaching 1,956 in May 2021 (chart 1). The price action (chart 2, weekly) is forming a 22-month Broadening Range, which Chris Roberts believes peaked in March. The implication is a significant decline below the lower green line of the pattern, currently around 1,250. Go 50% short at the market, the stop is a daily close above 2,128.

Vanda Insights

Crude’s upward trek remains in check from recession fears

Vandana Hari said that crude, which had been catapulted to three-month highs on April 12 by surprise, was ripe for a pullback. That is exactly what happened. This week, the animal spirits were back, weighing on market sentiment. All eyes are on the Fed, with money makers overwhelmingly betting for a 25bps rate hike before pivoting to rate cuts in H2/2023. Economists disagree, arguing it will take the higher-for-longer route. As consumers across the US and Europe tighten their purse strings, the one country enjoying a strong retail rebound is China. In her latest report, Vandana also looks at the tsunami of Chinese macroeconomic data and why it left oil market participants sitting on the fence.

CPM Group

Record silver prices and the realities of $50

CPM Group expects record silver prices in the next few years. Jeffrey Christian discusses what CPM means with its projected record silver prices and puts past spikes to $50 into perspective. Jeff also updates CPM’s current gold and silver prices expectations, and the short-term economic factors CPM Group analysts are monitoring.

Click here to watch.